Critical Infrastructure Protection Market Report Scope & Overview:

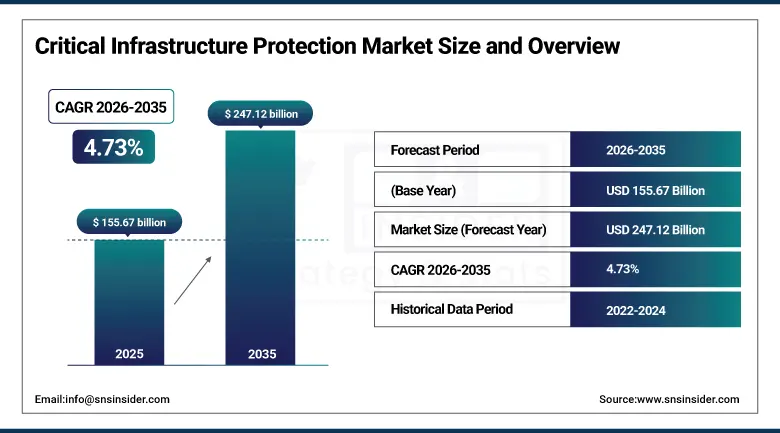

The Critical Infrastructure Protection Market was valued at USD 155.67 billion in 2025 and is expected to reach USD 247.12 billion by 2035, growing at a CAGR of 4.73% from 2026-2035.

The Critical Infrastructure Protection market is experiencing rapid growth owing to issues like cyber-attacks, terrorism, and geopolitics against the critical services. Digitalization and the usage of internet technology along with advancements in smart infrastructure have created greater vulnerability among countries. All governments are enacting strict policies for safety and adopting cybersecurity measures.

In 2024, FBI reports showed a 9% increase in ransomware complaints, with energy, healthcare, and transportation among the most targeted critical infrastructure sectors.

Market Size and Forecast

-

Market Size in 2025: USD 155.67 Billion

-

Market Size by 2035: USD 247.12 Billion

-

CAGR: 4.73% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Critical Infrastructure Protection Market - Request Free Sample Report

Critical Infrastructure Protection Market Trends

-

Rapid integration of AI and machine learning into critical infrastructure security platforms enabling real-time threat detection, predictive risk analytics, automated incident response, and behavioral anomaly identification across digital and physical security domains.

-

Growing adoption of IoT-based sensor networks and connected monitoring systems for continuous real-time surveillance of critical infrastructure assets including power grids, pipelines, transportation networks, and communication systems.

-

Increasing convergence of cyber-physical security frameworks combining IT cybersecurity with operational technology (OT) protection to address growing vulnerabilities in SCADA systems and industrial control networks.

-

Rising government investment in national cybersecurity frameworks, critical infrastructure resilience programs, and public-private partnership security initiatives driving sustained CIP market demand globally.

-

Growing adoption of zero-trust security architectures and identity-based access management systems across critical infrastructure organizations to mitigate insider threats and lateral movement risks from sophisticated cyberattackers.

-

Expansion of AI-enabled video surveillance and intelligent perimeter security systems utilizing computer vision, behavioral analytics, and automated threat alerting to enhance physical infrastructure protection at scale.

-

Increasing deployment of blockchain-based identity management and tamper-proof audit trail solutions for critical infrastructure operations, enhancing transparency, access control, and regulatory compliance.

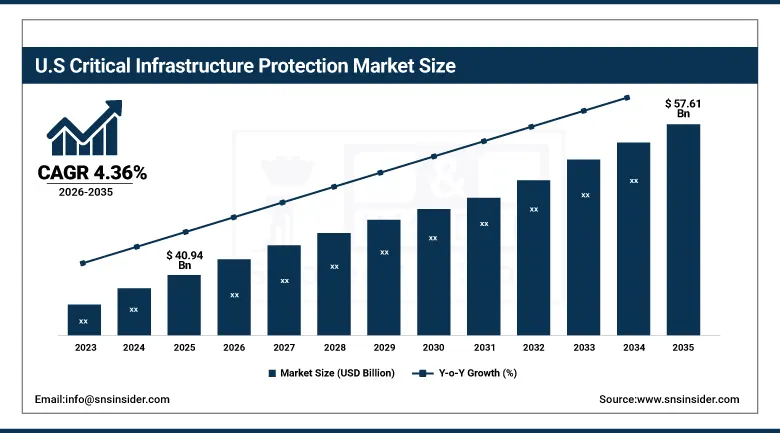

U.S. Critical Infrastructure Protection Market was valued at USD 40.94 billion in 2025 and is expected to reach USD 57.61 billion by 2035, registering a CAGR of 4.36% during 2026-2035.

The United States' Critical Infrastructure Protection Market is experiencing growth owing to an increase in cyber-attacks, the threat of terrorism, and vulnerabilities caused by old infrastructure. The increase in IoT, cloud technology, and smart grid usage has exposed organizations to threats. Government rules and regulations, defense spending, and cybersecurity solution investment will further fuel the market.

Firms such as BlackBerry have played a key role in protecting critical infrastructure, reportedly thwarting more than 5.2 million cyberattacks in late 2023 indicative of the central position played by the private sector in safeguarding critical infrastructure, and the growing market for specialized CIP managed security services through 2035.

Critical Infrastructure Protection Market Segment Insights

-

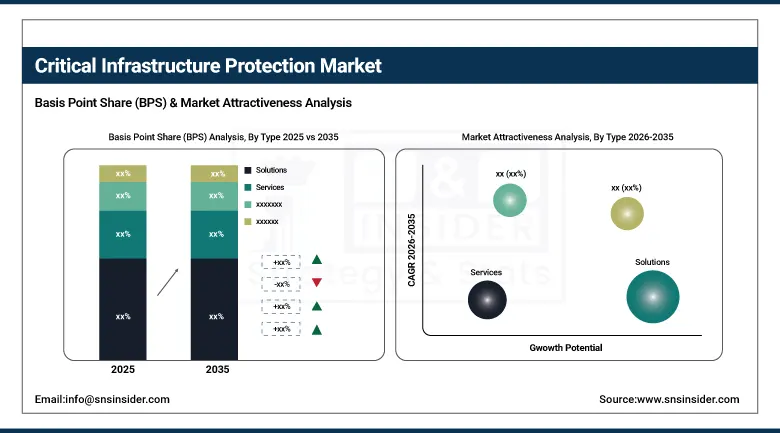

Based on Type, Solutions accounted for the largest market share (~74%) in 2025; Services expected to be the fastest-growing segment (CAGR of 5.80%).

-

Based on Security, Physical Safety & Security accounted for the largest market share (~69%) in 2025; Cybersecurity expected to be the fastest-growing segment (CAGR of 5.95%).

-

Based on End-User, BFSI accounted for the largest market share (~24%) in 2025; Oil & Gas expected to be the fastest-growing segment (CAGR of 7.13%).

Critical Infrastructure Protection Market Segment Analysis

By Type, Solutions dominate, Services expected to grow fastest

In terms of market shares, the solutions category accounted for nearly 74% of the CIP market revenues in 2025 due to their increased use of cutting-edge surveillance, access control, network security, and security management solutions. Security solutions have gained popularity because of the need for more flexible and scalable products in sectors like energy, transportation, and defense.

It is expected that between 2026 and 2035, the category of services will witness the maximum growth rate of 5.80% CAGR. There is a rise in the threat landscape and complexity in security stacks within enterprises, necessitating the need for organizations to depend on managed security services, cybersecurity consulting, and security systems integration services. This is more relevant for SMEs lacking cybersecurity experts along with legacy industrial control systems requiring continuous vulnerability management.

By Security, Physical Safety & Security dominates, Cybersecurity expected to grow fastest

Safety and Security held the highest share of around 69% in the year 2025. Video Surveillance systems, Intrusion detection systems, Perimeter security solutions, and Access control technologies are still considered to be the bedrock investments in protecting critical infrastructures. Safety solutions are important as they help in preventing any kind of unauthorised access and real-time detection of threats.

In addition to this, the cybersecurity segment is likely to witness a faster growth rate of 5.95% from 2026 to 2035. Increased cases of digital intrusion attacks, ransomware attacks, and breaches of data that especially target operational technology networks and SCADA systems are prompting the need for investments in firewalls, threat intelligence software, encryption services, and incident response management solutions. Increased adoption of digital infrastructure and costs associated with the breach per incident are pushing organisations towards predictive cybersecurity models.

By End-User, BFSI dominates, Oil & Gas expected to grow fastest

In terms of market contribution, BFSI was the highest in 2025 at about 24%. Financial organizations are primary victims of complex cybercrimes and frauds, necessitating the strictest security solutions that meet all regulatory requirements to protect data and financial stability. Constant improvements in threat detection, fraud detection and prevention, identity verification, and physical security of branches maintain BFSI's superiority.

Oil & Gas is expected to exhibit the highest CAGR of 7.13% between 2026 and 2035. Threats to SCADA systems, remote pipeline infrastructure, offshore oil and gas facilities, and geopolitical targets pose major risks to the sector. As the industry becomes more digitally connected via IIoT, remote monitoring systems, and automated control systems, the need to invest in both physical and cyber security increases significantly.

Critical Infrastructure Protection Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

83% |

|

Europe |

United Kingdom |

26% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

Saudi Arabia |

35% |

|

Latin America |

Brazil |

43% |

North America Critical Infrastructure Protection Market Insights

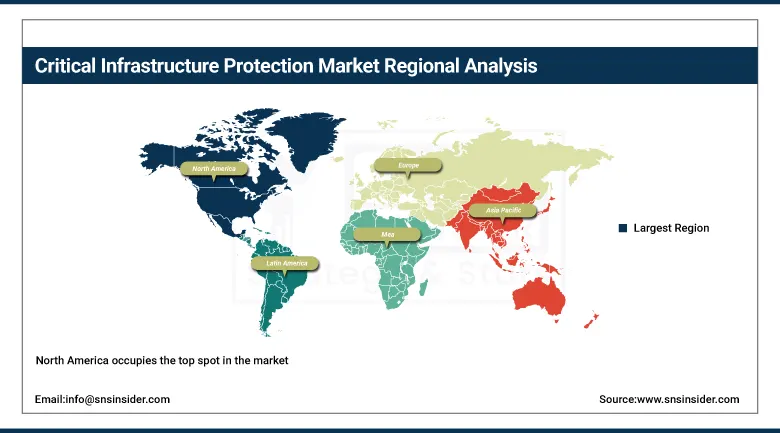

North America occupies the top spot in the market for Critical Infrastructure Protection owing to its superior digital infrastructure, robust cyber protection mechanisms, and substantial government expenditure in national security systems. The US is the frontrunner in regional demand because of standards set by regulatory bodies like NERC CIP, NIST, and the Department of Homeland Security. Federal organizations like the Cybersecurity & Infrastructure Security Agency and the Department of Energy have initiated numerous infrastructure resiliency programs in various industries. Growing threats to power grids, medical facilities, and financial institutions have increased the need for AI-driven monitoring, zero trust architectures, and advanced threat protection systems.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Critical Infrastructure Protection Market Insights

The Asia Pacific region is anticipated to see the most rapid growth in the market of Critical Infrastructure Protection. The fast pace of industrialization, development of smart cities, and increase in digital infrastructure are fueling the market’s growth. Nations like China, India, Japan, South Korea, and Singapore are making huge investments in their cybersecurity infrastructure. The leading country in the region is China, owing to its extensive government-sponsored initiatives related to infrastructure and cybersecurity. India’s growing digital economy and heightened cyber threat exposure are also creating opportunities for the market in the region.

Europe Critical Infrastructure Protection Market Insights

The position of Europe in the Critical Infrastructure Protection Market is well-established, owing to stringent regulatory measures and heightened geopolitical risks. The NIS2 Directive and Cyber Security and Resilience Bill in the UK are prompting obligatory cybersecurity enhancements in crucial industries. Some prominent nations like Germany, France, the UK, and the Netherlands are focusing heavily on protecting the country’s energy grid, finance systems, transport systems, and health facilities. The growing number of cyber-attacks and hybrid warfare threats have led to the adoption of more robust surveillance and risk evaluation technologies and resilient digital infrastructure systems in the region.

Middle East & Africa and Latin America Critical Infrastructure Protection Market Insights

In the Middle East and Africa, along with Latin America, there has been a rise in demand for Critical Infrastructure Protection products amid increasing infrastructural development and growing cyberattacks. In particular, countries like Saudi Arabia and the UAE in the Middle East have been making large investments in vision 2030 projects aimed at protecting their oil, gas, and smart city infrastructures from cyber-attacks. In Latin America, the increase in cybersecurity spending can be attributed to digitalization of finance, development of smart cities, and modernization of energy, transportation and other infrastructures.

Market Growth Drivers:

Rising Cyber Threats and Government Regulations Driving Strong Critical Infrastructure Protection Market Growth Globally: The Critical Infrastructure Protection market is witnessing a surge in demand owing to the rising number of cyberattacks, ransomware attacks, and nation-state attacks on vital infrastructure sectors like energy, transportation, healthcare, and utilities. The process of digital transformation, proliferation of IoT, and deployment of smart infrastructure has led to elevated levels of vulnerabilities in critical infrastructure systems. Governments around the world are implementing stringent cybersecurity policies, which include zero-trust architectures and compliance requirements, along with making large investments in their respective infrastructure resilience strategies.

Market Restraints

High Implementation Costs and Complex Legacy Systems Limiting Critical Infrastructure Protection Market Expansion: Though there is significant demand for Critical Infrastructure Protection solutions, their adoption has been constrained by the high cost of deploying highly sophisticated cybersecurity measures and monitoring systems. There are several companies with outdated infrastructure, which is not easy to update, thereby making them prone to cyber threats. Inadequate expertise in cybersecurity and the difficulty in managing hybrid information technology-operational technology environments act as additional barriers to the adoption of critical infrastructure protection solutions.

Market Opportunities

AI-Driven Security, Smart Infrastructure, and Public-Private Collaboration Creating New Growth Opportunities: The Critical Infrastructure Protection market is gaining some lucrative opportunities owing to the rising use of artificial intelligence, machine learning, and predictive analytics to detect and respond to threats in real time. The rise in smart city infrastructure and industrial Internet of Things is leading to a higher requirement for advanced protection solutions. Public and private sector collaboration is improving as governments and businesses focus on enhancing critical infrastructure resilience and cybersecurity readiness. Moreover, increased focus on the development of cloud security, edge computing, and digital twin technology will present several opportunities for innovation.

Recent Developments:

-

2025 (September): Thales Group unveiled a new suite of cybersecurity solutions specifically designed for the energy sector, addressing sector-specific SCADA and operational technology vulnerabilities with advanced AI-driven threat detection.

-

2025 (August): Raytheon Technologies announced a strategic partnership with a leading cybersecurity firm to integrate AI-driven threat detection capabilities into its critical infrastructure protection systems for defense and government clients.

-

2025 (April): CISA issued an advisory outlining critical vulnerabilities in widely used ICS systems from Siemens and Schneider Electric, resulting in a 15% increase in 30-day patching rates across affected critical infrastructure operators.

Critical Infrastructure Protection Market Key Players

Some of the Critical Infrastructure Protection Market Companies are:

-

Lockheed Martin Corporation

-

Raytheon Technologies (RTX Corporation)

-

Northrop Grumman Corporation

-

BAE Systems plc

-

Honeywell International Inc.

-

General Dynamics Corporation

-

Thales Group

-

Siemens AG

-

Schneider Electric SE

-

IBM Corporation

-

Cisco Systems, Inc.

-

Palo Alto Networks

-

CrowdStrike Holdings

-

BlackBerry Limited

-

Leidos Holdings, Inc.

-

SAIC (Science Applications International)

-

Booz Allen Hamilton

-

L3Harris Technologies

-

Fortinet, Inc.

-

SentinelOne, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 155.67 Billion |

| Market Size by 2035 | USD 247.12 Billion |

| CAGR | CAGR of 4.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Solutions, Services) • By Security (Physical Safety & Security, Cybersecurity) • By End-User (BFSI, Energy & Utilities, Transportation, Government & Defense, Oil & Gas, Healthcare, IT & Telecom, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Lockheed Martin Corporation; Raytheon Technologies (RTX Corporation); Northrop Grumman Corporation; BAE Systems plc; Honeywell International Inc.; General Dynamics Corporation; Thales Group; Siemens AG; Schneider Electric SE; IBM Corporation; Cisco Systems, Inc.; Palo Alto Networks; CrowdStrike Holdings; BlackBerry Limited; Leidos Holdings, Inc.; SAIC (Science Applications International); Booz Allen Hamilton; L3Harris Technologies; Fortinet, Inc.; SentinelOne, Inc. |

Frequently Asked Questions

Ans: North America dominated the Critical Infrastructure Protection Market in 2025, accounting for approximately 39% of global market revenue.

Ans: The Physical Safety & Security segment dominated the Critical Infrastructure Protection Market in 2025 with approximately 69% revenue share.

Ans: Escalating frequency and sophistication of cyberattacks on critical infrastructure combined with increasing digitalization of essential services, stringent government regulatory mandates, and the urgent need to protect energy, transportation, BFSI, and defense assets from both cyber and physical threats is the primary driver of sustained market growth through 2035.

Ans: The Critical Infrastructure Protection Market was valued at USD 155.67 billion in 2025.

Ans: The Critical Infrastructure Protection Market is expected to grow at a CAGR of 4.73% from 2026 to 2035.

Get in Touch