Data Observability Market Report Scope & Overview:

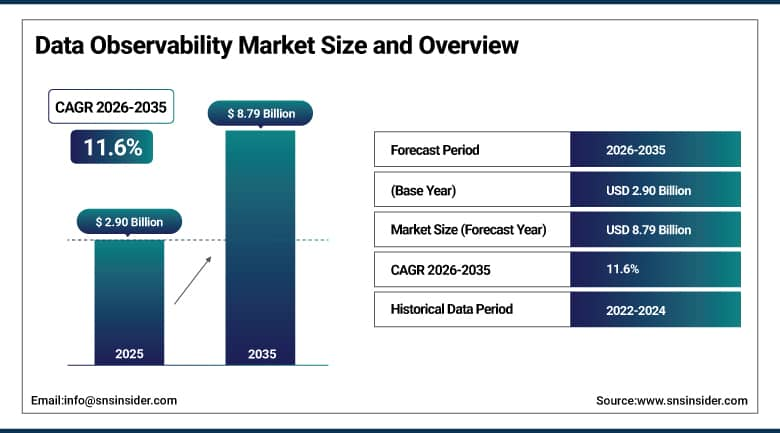

Data Observability Market Market was valued at USD 2.90 billion in 2025 and is expected to reach USD 8.79 billion by 2035, growing at a CAGR of 11.6% from 2026–2035.

The Data Observability Market is becoming increasingly significant because companies are beginning to understand that the reliability, accuracy, and timeliness of their data are just as important for running their business as having access to their technological resources. Through the implementation of data observability tools, businesses will be able to continuously monitor their data, detect any anomalies, analyze the cause, and measure the quality of their data through a multi-cloud data ecosystem, thus preventing data quality problems from affecting business intelligence platforms or ML models.

Data Observability Market Size and Forecast

-

Market Size in 2025: USD 2.90 Billion

-

Market Size by 2035: USD 8.79 Billion

-

CAGR: 11.6% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Data Observability Market - Request Free Sample Report

Data Observability Market Trends

-

Growing adoption of AI-powered automated anomaly detection within data observability platforms reducing mean time to data incident detection and resolution.

-

Expanding integration of data observability capabilities into modern data stack components including cloud data warehouses, ETL tools, and orchestration platforms.

-

Rising demand for real-time data quality monitoring across streaming data pipelines supporting operational analytics and AI inference applications.

-

Increasing focus on data lineage tracking and impact analysis to understand downstream consequences of upstream data quality failures across complex pipelines.

-

Growing adoption of data observability as a core component of enterprise DataOps and MLOps practices ensuring reliable AI and analytics operations.

-

Rising demand for unified data observability platforms replacing fragmented point solutions across data quality, metadata management, and pipeline monitoring.

-

Expansion of data observability into unstructured and semi-structured data environments supporting AI model training and enterprise knowledge management.

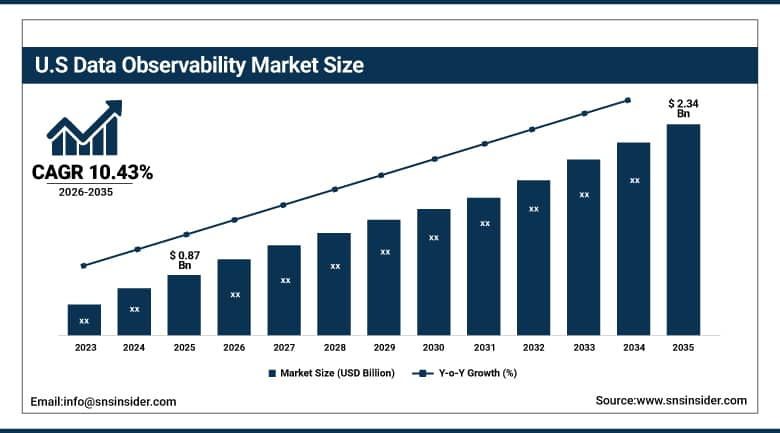

U.S. Data Observability Market was valued at USD 0.87 billion in 2025 and is expected to reach USD 2.34 billion by 2035, registering a CAGR of 10.43% during 2026–2035.

The driving factors behind the U.S. Data Observability Market include the presence of an advanced data infrastructure, dense data-related sectors like finance, healthcare, and tech, and the leading companies that provide data observability solutions. The U.S. enterprises dealing with multi-cloud platforms and analytics pipelines serve as the main source of demand for data observability products. Regulatory pressures related to financial reporting, healthcare data, and AI model transparency are also shaping up the investments in enterprise data observability.

Data Observability Market Segment Highlights

-

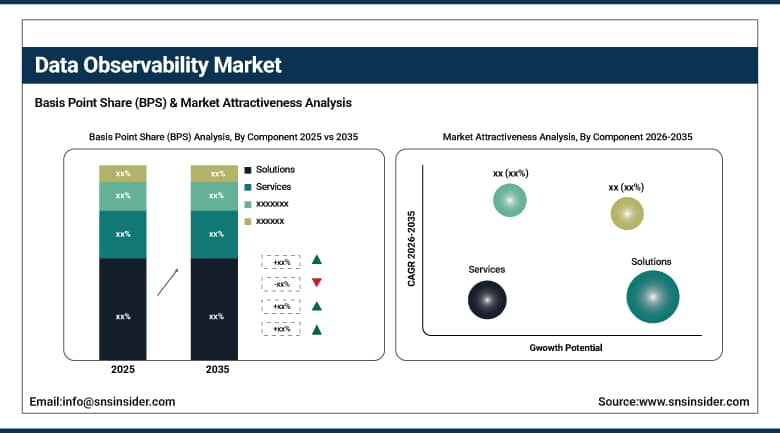

By Component, Solutions segment dominated the Data Observability Market in 2025 with ~64% share; Services segment is fastest growing (CAGR).

-

By Deployment, Public Cloud segment dominated the Data Observability Market in 2025 with ~72% share; Private Cloud segment is fastest growing (CAGR).

-

By End-use, BFSI segment dominated the Data Observability Market in 2025 with ~29% share; Healthcare & Life Sciences segment is fastest growing (CAGR).

Data Observability Market Segment Analysis

By Component, Solutions segment dominates the Data Observability Market, Services segment expected to grow fastest.

The Solutions segment holds a leading position in the Data Observability Market because of the high level of demand for integrated systems that offer real-time monitoring and data quality management for enhancing system reliability. It is preferable for organizations to invest in observability solutions that help ensure unified visibility, automated anomaly detection, and advanced analytics capabilities. The growing importance of data in decision-making processes and the need to ensure reliable and consistent data across different pipelines contributes to the leadership position of this segment.

The services category is experiencing fast-paced growth owing to high demand for implementation services, consultancy, integration, and observability management services. Companies are looking towards leveraging external knowledge to facilitate efficient implementation, minimize complexities, and boost overall system performance. The lack of internal data engineers and the growing preference for hybrid and multi-cloud infrastructure solutions is fueling the growth of this segment.

By Deployment, Public Cloud segment dominates the Data Observability Market, Private Cloud segment expected to grow fastest.

Public Cloud is dominant in the Data Observability Market, owing to its scalability, cost-effectiveness, and easy deployment. Public cloud platforms offer a wide array of benefits such as real-time processing of data, ease of integrating data with analytical platforms, and negligible management of infrastructure. The growing popularity of software-as-a-service observability solutions along with the generation of massive amounts of data due to digital transformation drives the segment. Flexibility and availability make up for public cloud's widespread adoption.

Private Cloud is experiencing rapid growth in the market of data observability due to rising concerns about data security and regulatory compliance. Companies operating in sectors where data security becomes necessary are opting for private clouds since the ability to govern data better ensures enhanced security. The growing rate of adoption in the private cloud space has been made possible by custom-built infrastructure, performance, and security of sensitive workloads.

By End-use, BFSI segment dominates the Data Observability Market, Healthcare & Life Sciences segment expected to grow fastest.

The BFSI industry holds the largest share in the Data Observability Market owing to the industry's dependence on accurate and timely data for executing transactions, assessing risks, detecting frauds, and fulfilling compliance norms. The BFSI industry works with large amounts of data which needs constant surveillance and high accuracy. Additionally, regulatory pressures and the need for data integrity also help to boost the uptake of observability solutions. Growing digitalization of banking operations and fintech innovations fuel growth prospects in the industry.

Healthcare and life sciences segment is anticipated to record the highest growth rate during the forecast period. The rising trend towards digitization of patient information and clinical trials coupled with the growing demand for analytics drives the growth of the segment. Accurate and real-time data is highly essential in such an industry. Growing adoption of telemedicine platforms and AI analytics in the healthcare industry also drive demand.

Data Observability Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

72% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

India |

40% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

52% |

North America Data Observability Market Insights

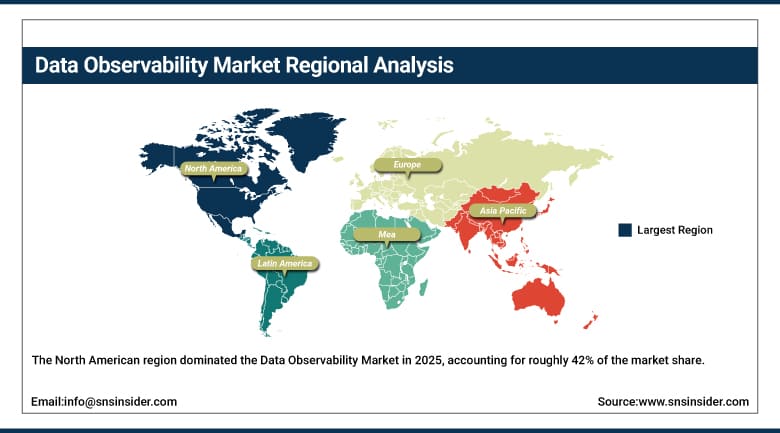

The North American region dominated the Data Observability Market in 2025, accounting for roughly 42% of the market share. The reason is the presence of many data-intensive companies in the financial services, healthcare, and technology industries, along with early adoption of data stacks and the dominance of data observability platforms such as Monte Carlo, Acceldata, and Splunk. As enterprises in the United States adopt cloud-based data warehousing in platforms like Snowflake, Databricks, and BigQuery, it becomes imperative to adopt cloud-native data observability solutions that can work within those ecosystems.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Data Observability Market Insights

The APAC region is likely to exhibit the highest growth rate over the forecast period, on account of fast pace of modernizing enterprise data infrastructures in countries such as China, India, Singapore, and Southeast Asia. Increasing use of cloud-based infrastructure, growth in analytics maturity, and spending on artificial intelligence solutions in enterprises in these regions are fuelling the need for observability platforms. The Indian tech industry stands out as one of the fastest growing markets for the same reason.

Europe Data Observability Market Insights

The European continent held a substantial share in the Data Observability Market in 2025 owing to its robust data governance framework due to its GDPR regulation, which generates demand for tools that can track data lineage and monitor data quality. The financial sector and the pharmaceutical industry, two key industries in Europe known for being data-intensive and requiring robust data quality measures, serve as major segments of the market.

Middle East & Africa and Latin America Data Observability Market Insights

The Middle East & Africa and Latin America Data Observability Markets are growth markets that align with digital transformation and the rise of the data economy in these regions. Companies in the Gulf Cooperation Council area investing in analytics and AI initiatives are just now realizing the importance of data observability. In Latin America, the finance and retail industries have been adopting cloud observability offerings through the efforts of Brazil and Mexico's data programs.

Data Observability Market Growth Drivers:

-

Increasing enterprise dependence on real-time, high-quality data for AI and business intelligence applications

Data Observability Market’s main growth factor can be attributed to the growing dependency of enterprises on data that is accurate and reliable when used for purposes of analysis and operation decisions within AI. As more companies rely on their data infrastructure, any problems with the data quality become increasingly expensive due to the fact that inaccurate information spreads in a company’s complex pipeline, leading to corrupt BI reports, incorrect results obtained from AI models, and failure of the business operations as well.

Data Observability Market Restraints

-

Integration complexity and organizational siloes limiting comprehensive data observability adoption

An important constraint for the growth of the Data Observability Market is the considerable technical difficulty that arises in implementing end-to-end observability capabilities that encompass on-premises databases, cloud data warehouses, data streams, and external data sources within an enterprise setting. Enterprises with siloed data governance policies will encounter organizational difficulties in establishing data quality standards, data ownership, and incident management practices in order to leverage data observability tools successfully. The lack of a cohesive data quality culture within data engineering and business departments can inhibit the benefits derived from such tools.

Data Observability Market Opportunities

-

AI-powered predictive data quality and DataOps platform integration for enterprise-scale observability

Predictive artificial intelligence features incorporated into data observability solutions offer an immense growth potential for enabling proactively identifying the early signs of any potential threats to data quality and prevent failures and inaccuracies from happening in data pipelines and reporting systems. Cutting-edge data observability tools capable of predicting future issues related to data volume changes, schema drifts, and proposing recommendations on how to deal with them based on historical incidents will significantly ease the burden of data engineering and yield better results. Data observability, combined with data catalogs, governance, and MLOps systems, is forming a holistic data reliability ecosystem with increasing value creation.

Recent Developments:

-

2026: Monte Carlo and Acceldata expanded AI-driven predictive observability, enabling 24–48 hour early detection of data quality anomalies, while Snowflake and Databricks deepened native integrations within modern cloud data stack environments.

-

2025: IBM enhanced Watson Studio with AI-powered data lineage visualization, automated root cause analysis, and workflow remediation tools for resolving complex data pipeline issues across hybrid multi-cloud ecosystems.

-

2025: Splunk introduced upgraded data observability in its Observability Cloud, combining pipeline, infrastructure, and application monitoring to provide unified visibility and correlation of data quality and performance issues.

Data Observability Market Key Players

Some of the Data Observability Market Companies

-

Monte Carlo

-

Acceldata

-

Splunk

-

IBM

-

Datadog

-

Microsoft

-

Amazon Web Services (AWS)

-

Google Cloud

-

SAS Institute

-

Oracle

-

Informatica

-

Talend

-

Qlik

-

New Relic

-

Dynatrace

-

ServiceNow

-

Sifflet

-

Bigeye

-

Anomalo

-

Datafold

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.90 Billion |

| Market Size by 2035 | USD 8.79 Billion |

| CAGR | CAGR of 11.6% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Deployment (Public Cloud, Private Cloud) • By End Use (BFSI, IT & Telecom, Government & Public Sector, Energy & Utility, Manufacturing, Healthcare & Life Sciences, Retail & Consumer Goods, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Monte Carlo, Acceldata, Splunk, IBM, Datadog, Microsoft, Amazon Web Services (AWS), Google Cloud, SAS Institute, Oracle, Informatica, Talend, Qlik, New Relic, Dynatrace, ServiceNow, Sifflet, Bigeye, Anomalo, Datafold |

Frequently Asked Questions

North America dominated the Data Observability Market in 2025.

The Public Cloud segment dominated the Data Observability Market.

The major growth factor of the Data Observability Market is the increasing need for real-time monitoring and management of complex data systems to ensure data quality and performance.

The Data Observability Market was valued at USD 2.90 billion in 2025.

The Data Observability Market is expected to grow at a CAGR of 11.6% from 2026 to 2035.

Get in Touch