Data Protection Market Report Scope & Overview:

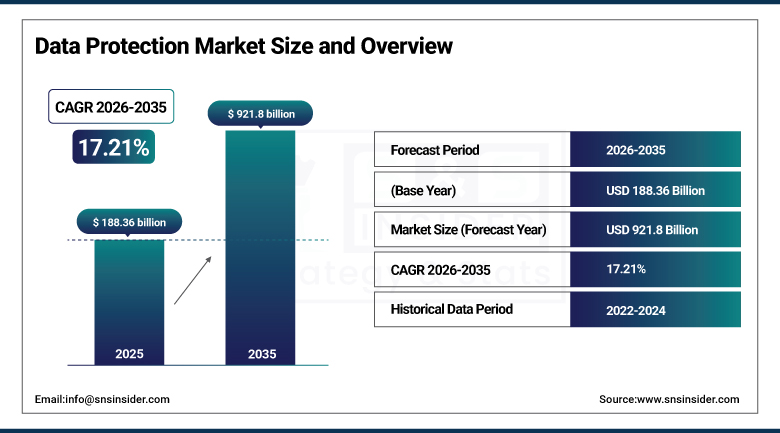

The Data Protection Market was valued at USD 188.36 billion in 2025 and is expected to reach USD 921.8 billion by 2035, growing at a CAGR of 17.21% from 2026–2035.

There has been tremendous growth observed within the Global Data Protection Market owing to cyber-attacks, growing use of clouds, and expanding regulations on data privacy on a global level. There is an immense generation of data that is quite sensitive and requires advanced security measures like encryption, backup & recovery, identity & access management, and data loss prevention solutions. With losses arising from data breaches escalating significantly, it is becoming imperative for enterprises to invest more in their cyber-security infrastructure and become more resilient operationally. Moreover, there are various legislations that make it mandatory for enterprises to adopt data protection. The rapid shift toward digital transformation, remote work environments, and cloud infrastructure is further accelerating demand for scalable and cloud-native data protection technologies globally through 2035.

The Data Protection Market's extraordinary 17.21% CAGR from 2026 to 2035 reflects the structural intersection of three irreversible megatrends — the exponential growth of valuable digital data created by AI, cloud, and IoT adoption; the escalating sophistication and frequency of cyberattacks targeting that data; and the global regulatory consensus that organisations bear legal and financial responsibility for data they collect, process, and store — creating a compounding demand dynamic that makes advanced data protection solutions as fundamental to modern enterprise operations as accounting or legal compliance infrastructure.

Data Protection Market Size and Forecast

-

Market Size in 2025: USD 188.36 Billion

-

Market Size by 2035: USD 921.8 Billion

-

CAGR: 17.21% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Data Protection Market - Request Free Sample Report

Data Protection Market Trends

-

Rapid integration of AI and machine learning into data protection platforms — enabling automated threat detection, behavioural analytics, anomaly identification, and predictive risk assessment that transform reactive security operations into proactive, intelligence-driven data protection architectures.

-

Accelerating adoption of zero-trust security frameworks that require continuous verification of all users, devices, and data access requests regardless of network location, fundamentally reshaping data protection architecture from perimeter-based to identity-centric models.

-

Growing deployment of data encryption, tokenisation, and masking technologies across multi-cloud environments — driven by the need to maintain data protection control as workloads migrate to hyperscaler infrastructure outside traditional on-premises security perimeters.

-

Growing importance of data sovereignty and compliance regarding data transfer between countries with conflicting data localization regulations, such as the EU, China, India, and Russia, thus prompting the need for a geographically dispersed data security infrastructure.

-

Wide-scale implementation of comprehensive data security platforms that bundle up features like DLP, IAM, encryption, and backup all managed through one vendor management console.

-

Increasing investments made by SMEs into cloud-hosted data protection services on a subscription basis owing to their cost-effectiveness and provision of enterprise-level security features, prompted by greater awareness regarding the susceptibility of SMEs to malware threats.

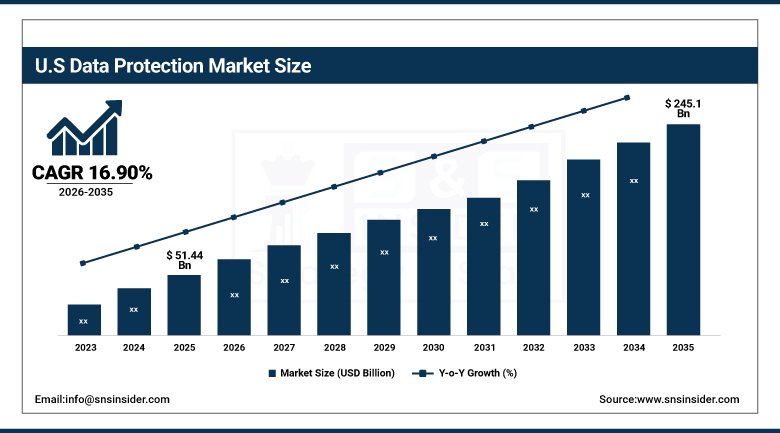

U.S. Data Protection Market

U.S. Data Protection Market was valued at USD 51.44 billion in 2025 and is expected to reach USD 245.1 billion by 2035, registering a CAGR of 16.90% during 2026–2035.

The United States is the biggest market for data security products in the world owing to growing cyber attacks, stringent data privacy laws, and the fast adoption of cloud services. There is an increase in spending by companies in the BFSI, healthcare, government, retail, and IT industries on data encryption, identity and access management, backup and recovery, and data loss prevention products. The growth in the adoption of hybrid working environments and cloud-based computing is boosting the demand for innovative data security technology.

In this regard, the American market enjoys an advantage due to the active involvement of prominent cybersecurity players who are constantly enhancing their capabilities in terms of AI-based threat detection systems, zero trust architecture, and cloud-native security platforms. Moreover, a huge financial loss resulting from a breach motivates businesses to build resilience against cyberattacks.

Data Protection Market Segment Insights

-

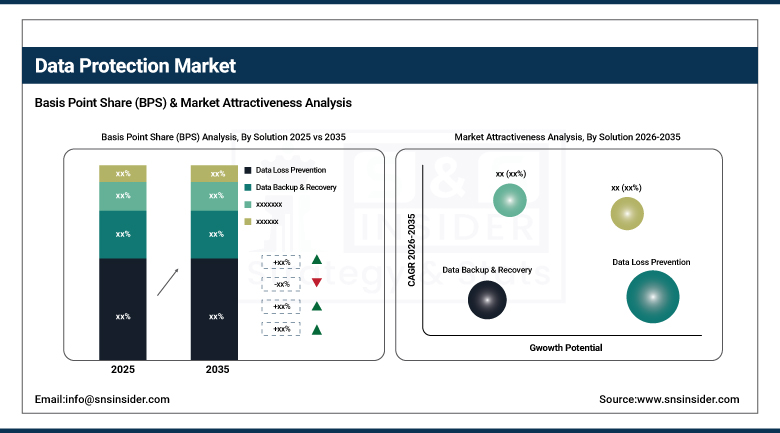

Based on Solution, Data Loss Prevention (DLP) accounted for the largest market share (~24%) in 2025; Data Encryption, Tokenization & Masking expected to be the fastest-growing solution segment (CAGR of 19.54%).

-

Based on Deployment, Cloud accounted for the largest market share (~56%) in 2025; Cloud also expected to maintain the fastest CAGR of 17.99% through 2035.

-

Based on Enterprise Size, Large Enterprises accounted for the largest market share in 2025; Small & Medium Enterprises (SMEs) expected to be the fastest-growing segment (CAGR of 18.40%).

-

Based on Industry Vertical, BFSI accounted for the largest market share (~24%) in 2025; Manufacturing expected to be the fastest-growing industry vertical (CAGR).

Data Protection Market Segment Analysis

By Solution: DLP dominates, Encryption/Tokenization/Masking grows at fastest CAGR

The Data Protection Market was led by the segment of Data Loss Prevention (DLP) tools in 2025 owing to its importance in blocking unauthorized access and transfer of sensitive corporate data. The real-time monitoring and policy management tools offered by DLP tools enable organizations to improve data governance and ensure regulatory compliance. Insider risks, adoption of remote work practices, and increase in the generation of sensitive data is expected to drive the demand for such solutions. Increasing concerns regarding protection of intellectual property and customer data have aided the leadership position held by the segment.

Encryption, tokenization, and masking solutions are forecasted to record the highest CAGR during 2026-2035. There is a growing preference for implementing data-centric security approaches to protect data in hybrid and multi-cloud environments. Growing regulatory compliance, increasing cybersecurity attacks, and high spending on next-generation encryption solutions, such as post-quantum cryptography, are likely to propel market growth.

By Deployment: Cloud dominates and grows at fastest CAGR

Cloud-based deployments accounted for the majority share of the Data Protection Market in 2025, mainly owing to the fast-paced shift of enterprise workloads to cloud-infrastructure-based applications. Cloud-based data protection services are highly scalable, reduce IT infrastructure cost, come with automatic updates regarding security patches, are easy to deploy, and provide efficient security of remote workers' environments and cloud-based data. The increased use of cloud-based platforms like AWS, Microsoft Azure, and Google Cloud Platform is pushing the demand for cloud-based security, back-up, encryption, and threat detection solutions.

On-premise deployment is still experiencing high levels of demand in industries that have sensitive government, financial, and healthcare data requiring compliance and data sovereignty. On the other hand, hybrid deployment has become highly popular since there is the need for consistent data security in both cloud-based and on-premises deployments. Rising investment in hybrid security management platforms is expected to support long-term market growth through 2035.

By Enterprise Size: Large Enterprises dominate, SMEs grows at fastest CAGR

Large enterprises retained the dominant data protection market share in 2025, reflecting their greater data assets, more complex regulatory compliance requirements, higher financial resources for security investment, and larger attack surface that collectively justify substantial, multi-solution data protection infrastructure. Enterprise-scale deployments encompass integrated DLP, IAM, encryption, backup, and threat detection platforms.

SMEs are projected to grow at the highest CAGR of 18.40% from 2026 to 2035, driven by the dramatic increase in cyberattacks targeting smaller organisations, which manages significant volumes of customer and financial data, combined with the growing availability of affordable, cloud-delivered data protection solutions at SME-appropriate price points. Government incentives, cyber insurance requirements, and supply chain security mandates from large enterprise customers increasingly compel SME data protection investment, creating a powerful combination of regulatory push and commercial pull driving SME market expansion.

Data Protection Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

41% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

46% |

|

Middle East & Africa |

UAE |

27% |

|

Latin America |

Brazil |

42% |

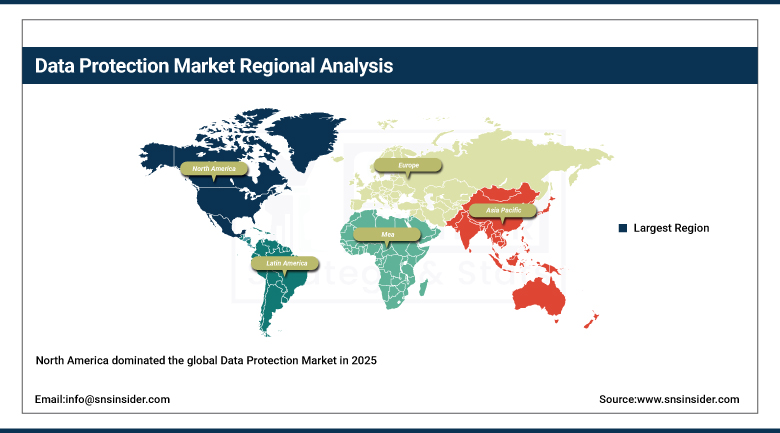

North America Data Protection Market Insights

North America dominated the global Data Protection Market in 2025, anchored by the United States — the world's largest economy, largest cyberthreat target, and most mature cybersecurity market. The U.S. market is driven by the highest incidence of data breach events, most comprehensive multi-layer regulatory compliance requirements, and the world's greatest concentration of data protection technology innovators. The U.S. Census Bureau's documented acceleration in cloud adoption creates parallel data protection investment requirements, while the growing volume of state-level privacy legislation following California's CCPA model is creating new compliance-driven demand drivers across the country through 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Data Protection Market Insights

Asia Pacific is projected to be the fastest-growing regional data protection market through 2035, driven by rapid digitalisation across China, India, Japan, South Korea, and Southeast Asia, accelerating cloud adoption among enterprises in the region, and the progressive strengthening of data privacy regulatory frameworks — including China's Personal Information Protection Law (PIPL) and India's Digital Personal Data Protection Act — that create new compliance mandates compelling organisational data protection investment. The region's extraordinary volume of financial services, e-commerce, healthcare, and manufacturing digital data represents a massive and growing attack surface driving rapid cybersecurity awareness and investment.

Europe Data Protection Market Insights

Europe's data protection market is shaped by the world's most comprehensive data privacy regulation — the GDPR — which has established a permanent, mandatory floor for data protection investment across all organisations processing EU resident data. The UK's own UK GDPR framework, the EU's NIS2 Directive for critical infrastructure cybersecurity, and the EU AI Act's data governance requirements are collectively reinforcing Europe's position as a regulation-driven data protection market with consistent, compliance-mandated demand growth through 2035. Germany, France, and the Netherlands are the largest European data protection markets, while the UK hosts one of the most active cybersecurity technology and services ecosystems globally.

Middle East & Africa and Latin America Data Protection Market Insights

MEA and Latin America are rapidly growing data protection markets, driven by accelerating digitalisation, rising cybercrime targeting financial institutions and government agencies, and progressive implementation of data privacy regulations. The UAE leads MEA with approximately 28% of regional revenue, anchored by its advanced digital economy, active financial services sector, and government-led cybersecurity investment.

Brazil dominates Latin American data protection revenues with approximately 43%, supported by its General Data Protection Law (LGPD), large banking sector, and the region's largest digital economy.

Data Protection Market Growth Drivers:

Escalating cyberattack frequency, global regulatory compliance mandates, and cloud migration creating irreversible data protection demand

The growth of the Data Protection Market is being propelled mainly by the rising number of cyber attacks, ransomware attacks, insider threats, and large-scale data breaches globally. Enterprises are looking for more sophisticated data protection solutions to protect their data, maintain their operational continuity, and minimize their risks of monetary losses and reputational damage from cyber threats. Furthermore, the rise of strict regulations related to global data privacy is turning robust data protection practices into a must-have for companies.

Another key factor supporting market growth includes the rising transition of enterprise applications to cloud platforms. Besides that, the fast-growing volume of data generated via artificial intelligence and the Internet of Things creates an urgent need for data protection. The heightened awareness of boards regarding cyber resilience and regulation compliance will ensure steady market growth during the forecast period until 2035.

Data Protection Market Restraints

Cybersecurity talent shortage, solution complexity, and budget constraints limiting SME adoption velocity

A significant restraint on the Data Protection Market's growth potential is the global cybersecurity talent shortage — with an estimated gap of approximately 3.4 million cybersecurity professionals worldwide — that limits organisations' ability to deploy, configure, and manage increasingly sophisticated data protection platforms effectively. The complexity and rapid evolution of the data protection technology landscape, encompassing dozens of solution categories with overlapping capabilities and complex integration requirements, creates decision paralysis and implementation challenges particularly for organisations without dedicated security architecture expertise. SME budget constraints can delay adoption of comprehensive data protection solutions despite growing threat awareness, while the pace of regulatory change across global jurisdictions also creates compliance uncertainty that can slow data protection infrastructure planning and investment commitment.

Data Protection Market Opportunities

AI-powered security automation, post-quantum cryptography, and SME cloud security democratisation

The integration of AI and machine learning into data protection platforms — enabling autonomous threat detection, automated incident response, and predictive risk scoring that dramatically reduce the skilled analyst time required for effective security operations — represents the most transformative near-term innovation opportunity in the market. AI-powered security automation directly addresses the talent shortage restraint, enabling smaller security teams to manage enterprise-scale data protection programmes with superior effectiveness relative to traditional manual approaches. Post-quantum cryptography — encryption algorithms resistant to quantum computer attacks — represents a premium, long-term innovation frontier that leading encryption vendors are already commercialising, commanding premium pricing from forward-looking enterprise customers in financial services, government, and defence. The massive SME market remains substantially underpenetrated by comprehensive data protection solutions, offering enormous growth runway for cloud-delivered, MSSP models through 2035.

Recent Developments:

-

2026: IBM launched IBM Sovereign Core to help enterprises and governments strengthen digital sovereignty, compliance management, and secure hybrid cloud data protection across AI-ready infrastructure environments.

-

2026: Rubrik introduced Rubrik Security Cloud Sovereign, enabling organizations to maintain jurisdictional control over sensitive data, metadata, and management systems to address rising global data sovereignty and compliance requirements.

-

2026: Rubrik expanded its cyber resilience portfolio through a new integration with Microsoft Defender, enabling automated identity threat detection, rapid remediation, and trusted recovery for enterprise environments.

Data Protection Market Key Players

Some of the Data Protection Market Companies are:

-

IBM Corporation

-

Microsoft Corporation

-

Amazon Web Services, Inc.

-

Palo Alto Networks, Inc.

-

CrowdStrike Holdings, Inc.

-

Fortinet, Inc.

-

Commvault Systems, Inc.

-

Carbonite, Inc.

-

Veritas Technologies LLC

-

Broadcom Inc.

-

Check Point Software Technologies Ltd.

-

Forcepoint

-

Digital Guardian

-

Varonis Systems, Inc.

-

Zscaler, Inc.

-

Imperva, Inc.

-

Thales Group

-

Proofpoint, Inc.

-

Rubrik, Inc.

-

Cohesity, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 188.36 Billion |

| Market Size by 2035 | USD 921.8 Billion |

| CAGR | CAGR of 17.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Solution (Data Loss Prevention, Data Encryption/Tokenization/Masking, Data Backup & Recovery, Identity & Access Management, Others) • By Deployment (Cloud, On-Premises, Hybrid) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By Industry Vertical (BFSI, Healthcare, IT & Telecom, Government, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation, Microsoft Corporation, Amazon Web Services, Inc., Palo Alto Networks, Inc., CrowdStrike Holdings, Inc., Fortinet, Inc., Commvault Systems, Inc., Carbonite, Inc., Veritas Technologies LLC, Broadcom Inc., Check Point Software Technologies Ltd., Forcepoint, Digital Guardian, Varonis Systems, Inc., Zscaler, Inc., Imperva, Inc., Thales Group, Proofpoint, Inc., Rubrik, Inc., Cohesity, Inc. |

Frequently Asked Questions

North America dominated the Data Protection Market in 2025, anchored by the United States, with the highest data breach costs, most comprehensive regulatory frameworks, greatest concentration of data protection technology innovation, and the highest organisational cybersecurity spending per enterprise globally.

Data Loss Prevention (DLP) dominated the Data Protection Market in 2025 with approximately 24% of global revenue, driven by its critical role in monitoring and restricting unauthorised data transfers, providing insider threat protection, and satisfying regulatory compliance documentation requirements across BFSI, healthcare, and government sectors.

The escalating frequency and sophistication of cyberattacks, with global average data breach costs at USD 4.45 million and rising combined with expanding global regulatory compliance mandates including GDPR, CCPA, and HIPAA creating new protection requirements, are the primary compounding structural growth drivers through 2035.

The Data Protection Market was valued at USD 188.36 billion in 2025.

The Data Protection Market is expected to grow at a CAGR of 17.21% from 2026 to 2035.

Get in Touch