DC Circuit Breaker Market Report Scope & Overview:

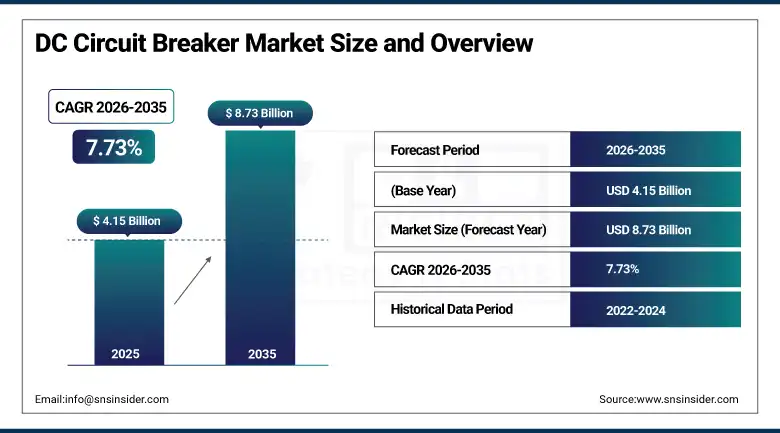

The DC Circuit Breaker Market size was valued at USD 4.15 Billion in 2025 and is expected to reach USD 8.73 Billion by 2035, growing at a CAGR of 7.73% from 2026–2035.

The global DC circuit breaker market is growing at a commercially broad-based pace. DC circuit breakers are protective switching devices designed specifically to interrupt direct current electrical faults, overloads, and short circuits in DC power systems. The market is driven by the proliferation of renewable energy generation and battery storage systems whose DC architecture requires dedicated DC protection, the extraordinary expansion of EV charging infrastructure creating DC fast charging protection requirements, and the growing deployment of HVDC transmission systems connecting renewable energy resources with consumption centers. Trends in technology adoption indicate a move toward solid-state and hybrid breakers due to their small footprint, fast switching speed, and high reliability.

In 2024, ABB launched the Tmax XT DC series of moulded case DC circuit breakers for utility-scale battery energy storage and commercial solar PV applications, incorporating enhanced DC arc quenching technology. The launch reflects the commercial urgency created by grid-scale battery energy storage deployment’s extraordinary pace whose DC bus protection requirement has substantially outpaced available DC circuit breaker product capability, creating premium procurement for technically qualified DC protection solutions.

Market Size and Forecast

-

Market Size in 2026E: USD 4.47 Billion

-

Market Size by 2035: USD 8.73 Billion

-

CAGR: 7.73% from 2026 to 2035

-

Fastest Growing Region: North America

-

Largest Region: Asia Pacific

To Get more information On DC Circuit Breaker Market - Request Free Sample Report

DC Circuit Breaker Market Trends

-

Solid-state DC circuit breaker adoption is accelerating in HVDC transmission and energy storage systems due to ultra-fast fault interruption capabilities.

-

Grid-scale battery energy storage deployment is increasing demand for DC circuit breakers capable of protecting 800V–1500V DC systems.

-

EV fast-charging infrastructure expansion is driving procurement of high-voltage DC protection devices for 350kW+ charging stations.

-

HVDC offshore wind transmission projects are creating demand for advanced DC circuit breakers designed for high-voltage power networks.

-

Marine and offshore DC power distribution systems are expanding, increasing the need for reliable DC protection solutions in electrified vessels.

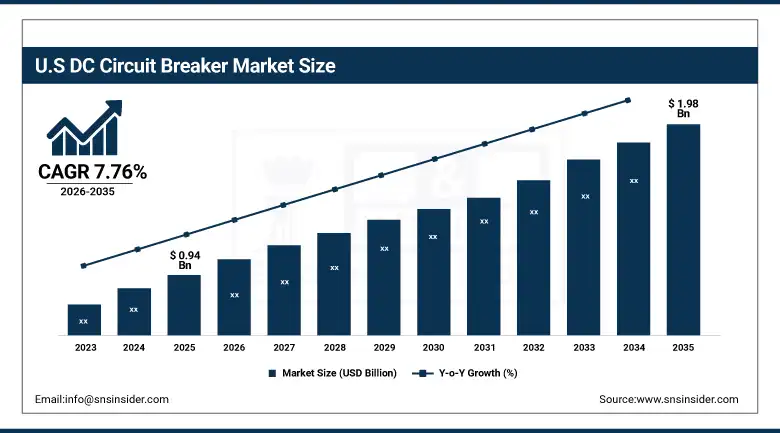

U.S. DC Circuit Breaker Market Size Outlook

The U.S. DC Circuit Breaker Market was valued at approximately USD 0.94 Billion in 2025 and is expected to reach approximately USD 1.98 Billion by 2035, growing at a CAGR of approximately 7.76%.

The U.S. is the most commercially dynamic DC circuit breaker market within the fastest-growing North American region. ABB, Eaton, Siemens, Schneider Electric, and Littelfuse’s U.S. operations serve the domestic market across EV charging, solar PV, BESS, and industrial DC applications. IRA’s domestic clean energy infrastructure investment is creating the most commercially concentrated domestic DC circuit breaker procurement opportunity in the market’s history. Tesla’s Megapack BESS deployment, the extraordinary solar PV installation pace, and the EV DC fast charging network’s commercial expansion collectively create structured DC protection procurement that compounds with each successive year of clean energy investment.

Eaton Corporation launched its new BUSSMANN series DC fuse and circuit breaker product line extension in 2024, specifically addressing the 800V-1500V DC bus voltage range created by utility-scale solar PV string combiners, battery energy storage system DC buses, and high-power EV charging infrastructure. The product line extension reflects the commercial recognition that clean energy infrastructure’s DC voltage architecture has progressively migrated above the 600V DC range.

DC Circuit Breaker Market Segment Analysis

-

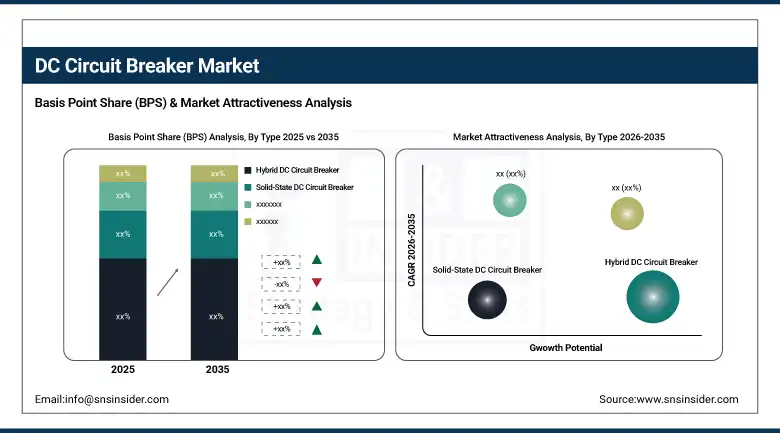

By Type, the hybrid DC circuit breaker segment dominated the market with 54.6% share in 2025, owing to its reliability, fast switching characteristics, compact design, and high cost-effectiveness, while the solid-state DC circuit breaker segment is the fastest growing.

-

By Voltage Level, the medium voltage DC segment dominated the market with 47.8% share in 2025 due to high usage in industrial, commercial, and renewable energy applications, while the high voltage DC segment is the fastest growing as HVDC transmission infrastructure investment and offshore wind power transmission link construction create procurement for DC protection at transmission voltage levels.

-

By Application, the renewable energy segment dominated the market with approximately 38% share in 2025 as solar PV array string combiner protection and battery energy storage DC bus protection create the largest aggregate DC circuit breaker application volume, while the EV Charging Infrastructure segment is the fastest growing as DC fast charging network expansion and ultra-fast charging station deployment create DC protection procurement.

-

By End User, the industrial segment dominated the market with approximately 42% share in 2025 as industrial automation, variable speed drives, DC motor drives, and manufacturing DC power systems create the commercially established aggregate DC circuit breaker procurement category, while the utilities/T&D segment is the fastest growing as HVDC transmission project investment and grid-scale battery energy storage deployment create concentrated utility sector DC protection procurement.

By Type, hybrid dominates, solid-state grows fastest

Hybrid DC circuit breakers retained the dominant type position with 54.6% of the DC circuit breaker market in 2025. The hybrid architecture’s combination of a fast mechanical contact interrupter that carries normal load current at low losses with a solid-state power semiconductor commutation path that handles transient fault current creates performance advantages over both pure mechanical and pure solid-state alternatives. Renewable energy’s DC protection requirement, EV charging infrastructure’s DC bus protection need, and BESS’s DC switchgear specification collectively represent hybrid breaker application categories whose combined procurement sustains the type category’s dominant position.

Solid-state DC circuit breakers are the fastest-growing type because HVDC transmission’s sub-millisecond fault clearing requirement, whose protection speed necessity substantially exceeds hybrid and mechanical breaker capability, creates premium solid-state procurement from technically uncompromising transmission system protection applications. The solid-state breaker’s absence of mechanical contact wear creates maintenance-free operation advantage that sustains premium specification in remote or offshore HVDC applications where maintenance access is logistically constrained.

By Application, renewable energy dominates, EV charging grows fastest

Renewable energy retained the dominant application position with approximately 38% of the DC circuit breaker market in 2025. Each utility-scale solar PV project creates multiple circuit breaker procurement levels from string fusing through combiner box DC breakers to inverter DC switch disconnects whose combined per-project procurement creates commercially significant relationships. Wind farm DC collection system protection and battery energy storage DC bus protection collectively create additional renewable energy application categories whose procurement compounds with each successive year of clean energy capacity addition.

EV charging infrastructure is the fastest-growing application because the extraordinary global EV adoption acceleration is creating DC fast charging network expansion whose per-station DC protection requirement creates procurement that compounds with network density growth. Ultra-fast charging stations at 500kW-1MW per station, which are being deployed at highway charging hubs and commercial fleet depots, create premium DC protection procurement whose commercial scale grows with ultra-fast charging penetration.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America DC Circuit Breaker Market Insights

North America is the fastest-growing regional DC circuit breaker market, driven by IRA’s clean energy investment creating solar PV and battery storage deployment, the EV DC fast charging network’s commercial expansion, and HVDC transmission infrastructure investment connecting renewable energy resources. The United States accounts for approximately 87.4% of North American revenues through ABB, Eaton, and Siemens’ domestic commercial operations, the IRA-incentivized clean energy investment, and the extraordinary solar and storage deployment pace.

Canada contributes approximately 12.6% of North American revenues through its clean energy transmission investment, the growing EV charging infrastructure, and the industrial DC power systems’ consistent replacement and upgrade procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe DC Circuit Breaker Market Insights

Europe is a technically sophisticated DC circuit breaker market where offshore wind HVDC transmission investment, the EU’s clean energy infrastructure, and ABB’s and Siemens Energy’s European commercial operations create structured premium demand. Germany accounts for approximately 22.3% of European revenues through its industrial manufacturing sector’s DC power systems, offshore wind HVDC transmission investment, and the EV charging infrastructure’s growing DC protection requirement.

The United Kingdom, Denmark, and the Netherlands are significant secondary markets where North Sea offshore wind HVDC transmission links, the EV charging network’s expansion, and the industrial automation sector’s DC infrastructure create consistent above-average DC circuit breaker specification procurement.

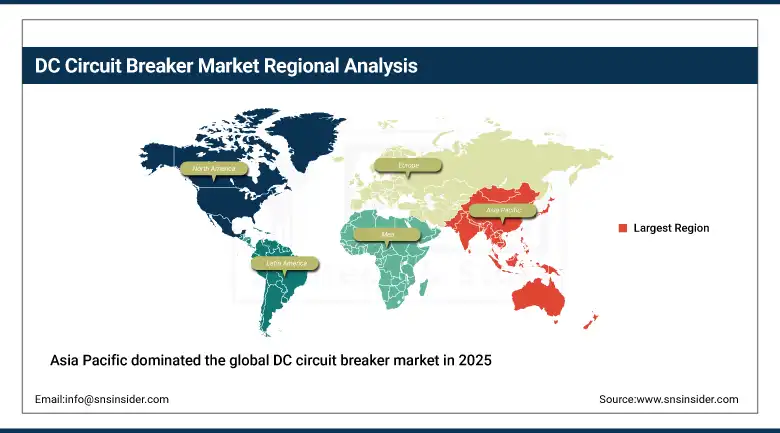

Asia Pacific DC Circuit Breaker Market Insights

Asia Pacific dominated the global DC circuit breaker market in 2025 as the world’s largest renewable energy installation region and most commercially significant EV market. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary solar PV and wind energy installation pace, the world’s largest EV market’s DC charging infrastructure, and the HVDC transmission network’s scale whose UHV DC lines at ±800kV and above create the most technically demanding DC circuit breaker procurement globally.

Japan and South Korea represent technically sophisticated secondary markets where offshore wind HVDC transmission investment, EV charging infrastructure, and the electronics manufacturing sector’s DC power systems create consistent above-average per-unit DC circuit breaker specification procurement.

MEA & Latin America DC Circuit Breaker Market Insights

UAE leads MEA revenues at approximately 38.4% through its extraordinary solar PV deployment’s DC protection requirement, the growing EV charging infrastructure, and the data center sector’s DC power distribution investment. Brazil leads Latin American revenues at approximately 44.2% through its solar energy deployment, industrial sector’s DC power systems, and the growing EV market’s charging infrastructure creating consistent DC circuit breaker procurement.

Saudi Arabia’s NEOM and Vision 2030’s extraordinary solar PV investment creates significant MEA secondary market DC circuit breaker procurement whose scale reflects the gigawatt-scale renewable energy deployment that creates structured DC protection infrastructure requirements.

Market Dynamics

Growth Drivers: Renewable energy DC architecture and battery energy storage creating structural DC protection investment

Renewable energy’s DC architecture is the DC circuit breaker market’s most commercially certain structural growth driver. Solar PV’s inherent DC generation creates proportional DC circuit breaker procurement that scales with each gigawatt of new solar capacity installed. The IEA’s projection of 5,000 GW cumulative solar PV capacity by 2030 creates commercial scale whose DC protection component creates extraordinary DC circuit breaker procurement opportunity. Battery energy storage’s simultaneous extraordinary deployment pace creates additional DC protection requirement whose BESS DC bus voltage levels progressively migrate toward 1500V DC to improve system efficiency, creating premium high-voltage DC circuit breaker procurement.

HVDC transmission’s strategic importance for renewable energy integration is creating the most technically demanding and commercially premium DC circuit breaker procurement. The HVDC grid’s progressive evolution from point-to-point links toward meshed multi-terminal networks creates even more demanding DC circuit breaker specifications whose fault selective protection capability requires solid-state or advanced hybrid technology.

Restraints: High cost of solid-state DC circuit breakers and technical complexity of DC arc interruption

Solid-state DC circuit breakers’ power semiconductor device cost creates purchase price premiums of 5-10 times equivalent mechanical alternatives whose commercial impact creates adoption barriers in cost-sensitive industrial and commercial DC protection applications where fault clearing speed requirements do not justify the premium. Each application whose DC protection specification can be satisfied by mechanical or hybrid alternatives at lower cost creates procurement competition that limits solid-state DC circuit breaker market penetration below the technically optimal adoption rate.

DC arc interruption’s technical complexity relative to AC systems, where natural current zero crossings do not occur and arc extinction requires active quenching by voltage reversal or current commutation, creates engineering design challenges whose resolution requires specialized expertise not universally available in the broader electrical protection engineering community.

Opportunities: HVDC multi-terminal grid protection and solid-state DC breaker cost reduction through semiconductor advancement

HVDC multi-terminal grid protection represents the most commercially transformative near-term technical opportunity. The evolution from point-to-point HVDC links toward meshed HVDC grids requires DC circuit breakers capable of selective fault isolation that conventional HVDC protection schemes’ converter blocking approach cannot achieve without interrupting the entire healthy network. Each multi-terminal HVDC project creates DC circuit breaker procurement whose scale reflects the number of network nodes requiring selective protection, creating above-average per-project commercial opportunity for technically qualified suppliers.

Wide bandgap semiconductor advancement through silicon carbide (SiC) and gallium nitride (GaN) power device development is progressively reducing solid-state DC circuit breaker cost and improving switching performance whose commercial consequence is a narrowing price premium relative to mechanical alternatives.

Recent Developments:

-

2026: Hitachi Energy strengthened HVDC grid infrastructure offerings with advanced fault-clearing technologies for high-voltage transmission networks.

-

2026: Littelfuse expanded high-voltage DC protection devices supporting fast-growing battery storage and electric mobility markets.

-

2026: Mersen expanded DC protection product development focused on battery energy storage systems and EV charging applications.

-

2025: ABB expanded its high-voltage DC protection portfolio for grid-scale battery energy storage and HVDC transmission applications.

DC Circuit Breaker Companies are:

-

ABB Ltd.

-

Siemens AG / Siemens Energy AG

-

Schneider Electric SE

-

General Electric (GE Grid Solutions)

-

Mitsubishi Electric Corporation

-

Fuji Electric Co., Ltd.

-

Littelfuse Inc.

-

LS Electric Co., Ltd.

-

Mersen S.A.

-

Sensata Technologies

-

Toshiba Energy Systems & Solutions Corporation

-

Hitachi Energy Ltd.

-

CBI-electric

-

Carling Technologies (Esterline)

-

ETA - Elektrotechnische Apparate GmbH

-

Schurter AG

-

Noark Electric

-

Hyundai Electric & Energy Systems

DC Circuit Breaker Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.15 Billion |

| Market Size by 2035 | USD 8.73 Billion |

| CAGR | CAGR of 7.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hybrid DC Circuit Breaker, Solid-State DC Circuit Breaker, Mechanical/Electromechanical DC Circuit Breaker) • By Voltage Level (Low Voltage, Medium Voltage, High Voltage) • By Application (Renewable Energy/Solar & Wind, EV Charging Infrastructure, Battery Energy Storage Systems, HVDC Transmission, Marine & Offshore, Industrial Automation, Others) • By End User (Industrial, Utilities/T&D, Commercial, Residential) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd., Siemens AG / Siemens Energy AG, Eaton Corporation, Schneider Electric SE, General Electric (GE Grid Solutions), Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Legrand S.A., Littelfuse Inc., LS Electric Co., Ltd., Mersen S.A., Sensata Technologies, Toshiba Energy Systems & Solutions Corporation, Hitachi Energy Ltd., CBI-electric, Carling Technologies (Esterline), ETA - Elektrotechnische Apparate GmbH, Schurter AG, Noark Electric, Hyundai Electric & Energy Systems. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 7.73% from 2026 to 2035.

The market was valued at USD 4.15 Billion in 2025.

Proliferation of renewable energy generation and battery energy storage systems requiring DC protection, and EV charging infrastructure expansion.

Hybrid DC circuit breakers dominated the market with 54.6% share in 2025.

Asia Pacific dominated the DC Circuit Breaker Market in 2025.

Get in Touch