Debt Collection Software Market Report Scope & Overview:

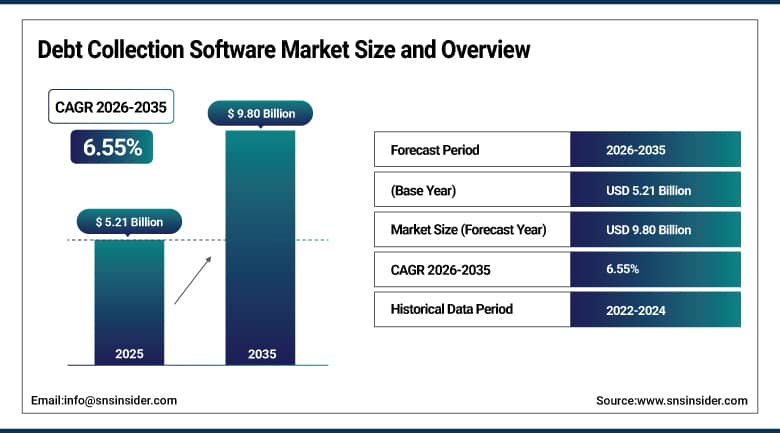

The Debt Collection Software Market was valued at USD 5.21 billion in 2025 and is expected to reach USD 9.80 billion by 2035, growing at a CAGR of 6.55% from 2026–2035.

The debt collection software market is experiencing high growth rates globally owing to increased demand for automated debt recovery and digital loan management systems. There has been an increase in demand for efficient and compliant debt recovery software within industries such as banking, financial services, telecommunications, and healthcare. Increased use of automation technologies and cloud-based collections have been contributing to high growth rates in the debt collection software market. Banking sector, non-banking financial companies (NBFCs), insurers, healthcare providers, and utility companies have been quick adopters of advanced recovery software solutions. There has been high investment made in intelligent collection software technology due to increased digitalization trends in these industries.

The development of debt recovery software will be fueled by rigorous compliance regulations for finance, data security, and ethical loaning policies. The need for GDPR-compliant systems, FDCPA compliance, and regulations in the banking sector are fueling the growth of transparent and secure debt recovery systems. In North America, there are developments in building financial technology infrastructure. Increased interest in credit scoring and automated debt recovery systems will boost adoption in the United States.

Market Size and Forecast

-

Market Size 2026E: USD 5.54 Billion

-

Market Size 2035: USD 9.80 Billion

-

CAGR (2026 - 2035): 6.55%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Debt Collection Software Market - Request Free Sample Report

Debt Collection Software Market Trends

-

Rising fintech expansion and digital lending platforms is increasing demand for automated debt collection software solutions globally.

-

Increasing adoption of AI and machine learning is improving predictive analytics and recovery efficiency in debt collection processes.

-

Growth in cloud-based deployment models is enhancing scalability flexibility and reducing infrastructure costs for organizations.

-

Expanding use of omnichannel communication tools is improving customer engagement and increasing debt recovery success rates.

-

Strengthening regulatory compliance requirements is driving demand for secure transparent and audit ready collection systems.

-

Integration of robotic process automation is reducing manual workload and improving operational efficiency in debt recovery workflows.

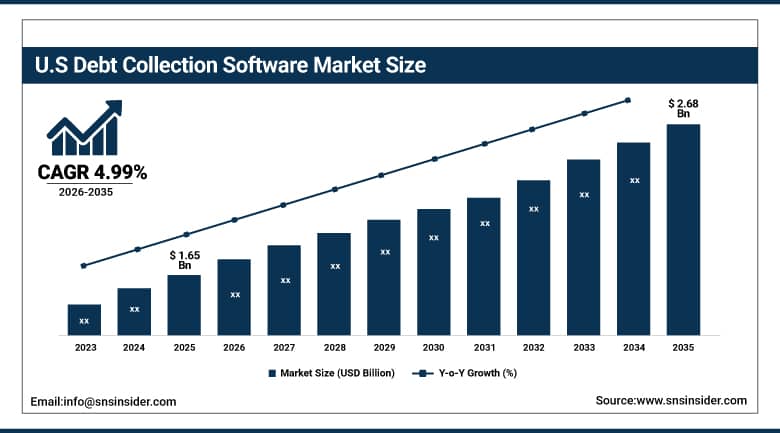

U.S. Debt Collection Software Market Size Outlook.

The United States Debt Collection Software Market was valued at USD 1.65 billion in 2025 and is expected to reach around USD 2.68 billion by 2035, growing at a CAGR of 4.99% from 2026–2035.

The U.S. debt collection software is expanding at a steady rate owing to the increasing demand for modern and effective digital debt recovery systems within banks and other financial organizations. Market growth can be attributed to the widespread use of automation cloud platforms powered by artificial intelligence as well as lending ecosystems facilitated by fintech. Growth in credit cards, personal loans, and buy now pay later options is contributing to the increase in demand for effective recovery mechanisms.

The US debt collection software market will be highly propelled due to high penetration of digital banking and credit based financial services in the region. A significant demand for automated recovery and compliance management solutions is noted from banks, non-bank financial corporations (NBFC), telecom, healthcare, and utility sectors. Rising pressure by regulations such as Fair Debt Collection Practices Act (FDCPA) and Consumer Financial Protection Bureau (CFPB) has increased the need for transparency and ethical practices in debt collections.

Debt Collection Software Market Segment Analysis

-

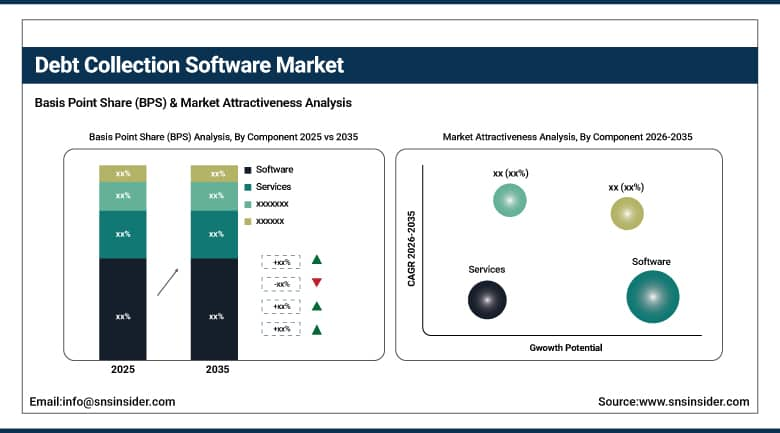

By Component, software dominated the debt collection software market with 63.40% share in 2025; while services is the fastest growing segment.

-

By Organization Size, large enterprises dominated the debt collection software market with 58.15% share in 2025; while small and medium-sized enterprises (SMEs) is the fastest growing segment.

-

By Deployment Mode, cloud-based dominated the debt collection software market with 67.25% share in 2025 and it is also fastest growing segment.

-

By End-User, financial institutions dominated the debt collection software market with 42.80% share in 2025; while collection agencies is the fastest growing segment.

By Component, software dominated the debt collection software market, while services is the fastest growing segment.

Software segment led the market with the dominated revenue share in 2025 owing to the high level of adoption of automated recovery solutions. The preference for software solutions lies in their capability for real-time monitoring, analysis, and process automation. Additionally, their integration with CRM solutions and banking software enhances the efficiency of the process. The growing need for artificial intelligence-based predictive scoring and compliance management solutions boosts the demand for software solutions.

Services segment is predicted to register the fastest CAGR over 2026-2035 due to the rising need for managed services, consultancy services, and integration support. Expert guidance is required in the implementation of the solution and for customizing the system. Furthermore, there is an increased requirement for compliance management due to the increasing complexity of debt collection and recovery systems.

By Organization Size, large enterprises dominated the debt collection software market, while small and medium-sized enterprises (SMEs) is the fastest growing segment.

Large Enterprises sector was the dominant segment of the debt collection software market in 2025. The dominance in this market arises due to the high volume of credit portfolios and elaborate debt recovery activities across multiple regions. These firms are well funded in terms of their IT spending and are capable of deploying new-age AI-driven collections platforms. They need systems that are scalable and compliance-ready while being integrated with banking CRM ERP, and analytical applications.

Small and Medium Enterprises (SMEs) segment was projected to be the fastest growing market segment during 2026-2035 in terms of its CAGR rate. SMEs are adopting cloud-based debt collections software applications in addition to their digital loan and credit operations. There has been a rapid increase in fintech adoption and availability of affordable software systems which can be deployed easily using the AI-enabled platforms.

By Deployment Mode, Cloud-Based segment dominates the Debt Collection Software Market and is also the fastest growing segment.

Cloud-Based segment dominated the Debt Collection Software Market with the highest revenue share in 2025 due to strong demand for scalable flexible and cost efficient deployment models. Organizations prefer cloud solutions for real time data access automated workflows and easy integration with banking systems. It reduces infrastructure costs and improves operational efficiency across financial institutions.

It is expected to grow at the fastest CAGR from 2026–2035 due to increasing adoption of SaaS platforms and digital lending ecosystems. Rising need for remote access secure data management and AI driven automation is accelerating growth. Expansion of fintech companies and preference for subscription based models is further boosting global adoption significantly across industries.

By End-User, financial institutions dominated the debt collection software market, while collection agencies is the fastest growing segment.

Financial Institutions held the Dominated market share in terms of revenue in the global debt collection software market in 2025. High number of loans, credit cards and retail loans in their portfolio have led to their strong presence in the debt recovery activities. Advanced software is extensively used in banks and NBFCs to automate risk assessment and compliance activities. Regulations and large customer base have contributed significantly to the dominance of financial institutions in debt recovery technology.

Collection Agencies will record the fastest CAGR during the forecast period. The need for third party agencies for debt collection will drive the segment in the coming years. Increasing number of non-performing assets and cost pressures have led to outsourcing the process of debt recovery by businesses. Cloud-based tools and advanced artificial intelligence tools are being adopted rapidly by collection agencies.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

82.40% |

|

Europe |

Germany |

24.15% |

|

Asia Pacific |

China |

22.60% |

|

Middle East & Africa |

UAE |

7.25% |

|

Latin America |

Brazil |

6.20% |

North America Debt Collection Software Market Insights.

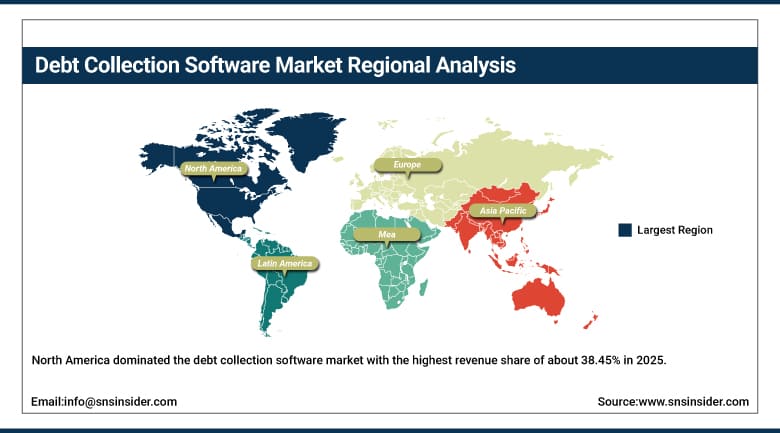

North America dominated the debt collection software market with the highest revenue share of about 38.45% in 2025 due to strong digital banking infrastructure and high credit penetration. The region benefits from widespread adoption of AI driven recovery platforms cloud based deployment and advanced fintech ecosystems across the United States and Canada. Strong presence of leading software vendors and mature financial institutions is further supporting market expansion steadily. Rising focus on regulatory compliance data security and automated recovery workflows is also accelerating software adoption across banking and financial services sectors.

Recent developments indicate that rising consumer credit card debt in the United States is driving strong demand for automated debt collection solutions. A large share of financial institutions in North America have adopted AI driven debt recovery platforms to improve efficiency and reduce delinquency risk. Increasing regulatory pressure from agencies such as CFPB is further pushing banks toward transparent and compliant digital debt recovery systems.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Debt Collection Software Market Insights.

Europe is considered as an advanced debt collection software market in terms of being highly regulated. In 2025, Europe’s market share would be largely influenced by the high adoption rates seen among banking, insurance, and telecom industries. Nations like Germany, France, UK, and Italy have been working to integrate digital debt collection systems amid stringent rules governing data privacy issues. Frameworks established by the European Union stress GDPR guidelines, ethical practices of debt collection, as well as protection of financial information.

Recent developments indicate strong adoption of digital debt management and AI driven analytics platforms among European banks by 2025, improving recovery efficiency. Rising household debt levels across Europe are increasing demand for structured debt collection systems. Strict GDPR enforcement is further driving investment in secure cloud based and compliant debt recovery technologies across the region.

Asia Pacific Debt Collection Software Market Insights.

Asia Pacific holds a revenue share of about 8.51% in 2025 and is expected to grow at the fastest CAGR from 2026–2035 due to rapid digital lending expansion and fintech growth. Growth is driven by rising credit usage increasing non performing assets and expanding banking networks across China India Japan and Southeast Asia. Government initiatives supporting digital financial services and cashless economies are further accelerating market expansion significantly. Increasing adoption of cloud platforms AI automation and SaaS based solutions is boosting debt recovery efficiency across the region steadily.

Digital lending in Asia Pacific is rising rapidly, driving strong demand for automated debt collection solutions. Banks and fintech lenders are increasingly adopting cloud based platforms to improve recovery efficiency. Growing smartphone and digital banking usage is further accelerating omnichannel debt recovery adoption across the region.

Middle East & Africa and Latin America Debt Collection Software Market Insights.

Middle East & Africa and Latin America, in totality, have an increasing share in terms of revenues in 2025 due to higher financial inclusivity and improvement in the banking infrastructure. Countries like UAE, Saudi Arabia, South Africa, Brazil, and Mexico are experiencing increasing acceptance of technology-based loans and credit collection systems. Increased investment in fintech firms, improved internet connectivity, and access to loans by Small Medium Enterprises (SMEs) have been aiding market growth. Rapid adoption of digital banking platforms and rising cross border financial transactions are further supporting structured credit recovery systems across these emerging economies steadily.

Market Dynamics:

Growth Drivers: Rising adoption of digital lending platforms and increasing need for automated credit recovery systems globally

Fast-paced growth of digital lending environments is causing a sharp rise in the demand for highly effective debt collection applications. Banks and other institutions need to cope with larger and larger amounts of loans, including those that do not work as expected. Cloud-based solutions and artificial intelligence technologies can help enterprises to manage their collections more efficiently. The integration of omnichannel communication tools helps reduce the risk of defaults successfully. Growing needs for compliance make the implementation of such solutions even more relevant for financial organizations. Data-driven approaches continue to drive market growth constantly.

Restraints: Data privacy concerns and strict regulatory compliance requirements limiting operational flexibility across regions

The financial regulatory framework and personal information regulations have an immense impact on debt collection system deployment. GDPR and FDCPA are some of the most important regional regulations that complicate the process for the providers. It is imperative for the companies to ensure the adequate safety of information, efficient communication, and generation of reports. Legal framework amendments constantly require software updates; therefore, additional costs arise. Privacy rights, among others, limit the utilization of any forceful methods by the firms.

Opportunities: Increasing adoption of cloud based SaaS models and omnichannel engagement tools driving market expansion globally

Transitioning towards cloud-based SaaS software solution services is giving rise to many opportunities for software for debt collection. It is evident that there is an increasing tendency for adoption of the software on the basis of subscriptions that involve less capital investment. Effective communication using omnichannel tools like SMS, emails, chatbots, and voice automation services is making the communication process more efficient. Efficiency in work can be observed due to real-time analysis features and smooth API integration. Remote access and mobile-based solutions are increasingly being used by many businesses.

Recent Developments

-

2026: FICO enhanced its AI driven credit decisioning and automated collections solutions to improve debt recovery efficiency for financial institutions globally.

-

2025: Experian expanded its cloud based credit analytics and debt management platforms with advanced risk scoring and real time consumer insights worldwide.

-

2025: TransUnion strengthened its credit intelligence ecosystem with improved data driven collections and fraud detection capabilities across global financial markets.

-

2024: Pegasystems advanced its AI powered CRM and omnichannel engagement solutions to support automated debt collection workflows across banking and financial services sectors.

Debt Collection Software Market Key Players are:

-

FICO

-

Experian

-

TransUnion

-

CGI

-

Pegasystems

-

SAP

-

Oracle

-

Microsoft

-

Fiserv

-

FIS (Fidelity National Information Services)

-

Tata Consultancy Services

-

Infosys

-

Wipro

-

Nucleus Software

-

Temenos

-

Finvi

-

C&R Software

-

Katabat

-

Applied Business Software

-

SAS

Debt Collection Software Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.21 Billion |

| Market Size by 2035 | USD 9.80 Billion |

| CAGR | CAGR of 6.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Organization Size (Small and Medium-Sized Enterprises (SMEs), Large Enterprises) • By Deployment Mode (Cloud-Based, On-Premises) • By End-User (Healthcare, Financial Institutions, Collection Agencies, Government, Telecom & Utilities, Others (Real Estate & Retail)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | FICO, Experian, TransUnion, CGI, Pegasystems, SAP, Oracle, Microsoft, Fiserv, FIS (Fidelity National Information Services), Tata Consultancy Services, Infosys, Wipro, Nucleus Software, Temenos, Finvi, C&R Software, Katabat, Applied Business Software, SAS |

Frequently Asked Questions

The debt collection software market is expected to grow at a CAGR of 6.55% from 2026 to 2035.

The debt collection software market was valued at USD 5.21 billion in 2025.

Rising demand for automated debt recovery systems, digital lending growth, and increasing need for regulatory compliant financial operations are driving the market.

Software segment dominated the market in 2025 due to high adoption of automated recovery platforms, real time analytics, and AI driven decision making systems.

North America dominated the market in 2025 due to strong digital banking infrastructure, high credit penetration, and advanced fintech ecosystem adoption.

Get in Touch