Micro Data Centers Market Report Scope & Overview:

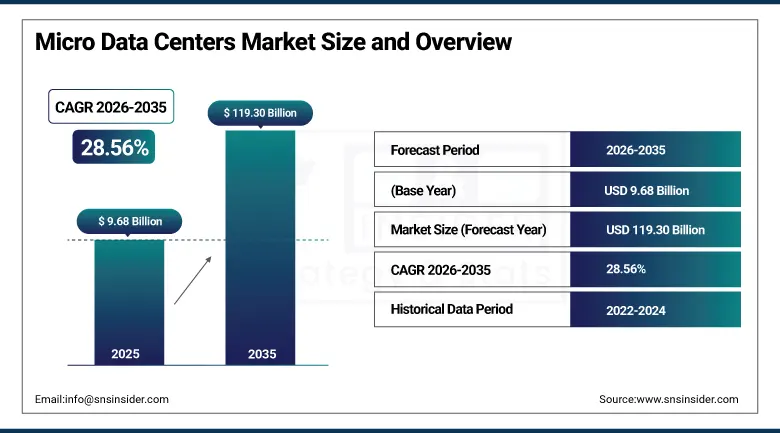

The Micro Data Centers Market was valued at USD 9.68 Billion in 2025 and is projected to reach USD 119.30 Billion by 2035, expanding at a CAGR of 28.56% during the forecast period 2026–2035.

The global micro data centers market is witnessing rapid expansion due to increasing deployment of edge computing infrastructure, growing enterprise demand for low-latency data processing, and rising adoption of distributed IT architectures. Growing deployment of edge computing infrastructure, increasing enterprise demand for low-latency data processing, and rising adoption of distributed IT architectures are anticipated to drive the market growth. The rapid deployment of 5G networks, industrial automation platforms, cloud-native applications and intelligent edge environments is fueling a surge in global investment in scalable micro data center infrastructure. Enterprises are investing in localized computing resources to reduce network congestion, improve application responsiveness and increasing business continuity in geographically dispersed operations.

Over the 2025-2026 period, multiple infrastructure providers bolstered their AI-ready micro data center portfolios with sophisticated power management systems, smart cooling architectures, remote monitoring platforms and edge computing optimization capabilities.

Market Size and Forecast

-

Market Size 2026E: USD 12.43 Billion

-

Market Size 2035: USD 119.30 Billion

-

CAGR: 28.56% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Micro Data Centers Market - Request Free Sample Report

Micro Data Centers Market Trends

-

Increasing deployment of edge computing infrastructure supporting AI and real-time analytics.

-

Rising investments in distributed data center architectures for low-latency operations.

-

Growing integration of intelligent cooling, power optimization and remote monitoring systems.

-

Expansion of 5G-enabled micro data center deployments across enterprise environments.

-

Increasing adoption of modular and scalable edge infrastructure supporting IoT ecosystems.

U.S. Micro Data Centers Market Size Outlook

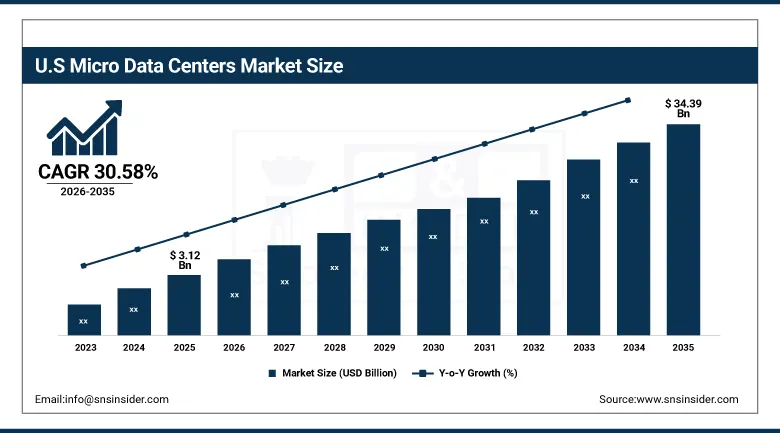

The U.S. Micro Data Centers Market was valued at USD 3.12 billion in 2025 and is expected to reach approximately USD 34.39 billion by 2035, expanding at a CAGR of 30.58% during 2026–2035.

The US continues to dominate the micro data center market, owing to the huge investments in edge computing infrastructure, growing cloud technology adoption, increasing AI workloads and digital transformation advancements. Companies are deploying smaller edge facilities to enable latency sensitive applications, industrial automation, intelligent retail operations and next-generation telecommunications networks. The proliferation of AI-powered applications, real-time analytics platforms and connected infrastructure solutions are also further accelerating deployment across enterprise environments. The presence of leading cloud service providers, hyper scale technology companies and advanced network infrastructure continue to fuel market growth. In addition, rising investments in 5G deployment, autonomous systems, and IoT-based operations are driving the demand for localized computing resources that provide higher performance, security, and operational reliability.

Between 2025 and 2026, leading U.S. technology and infrastructure providers increased deployments of AI-enabled edge computing combined with advanced remote monitoring, intelligent workload management and autonomous infrastructure optimization capabilities.

Micro Data Centers Market Segment Analysis

-

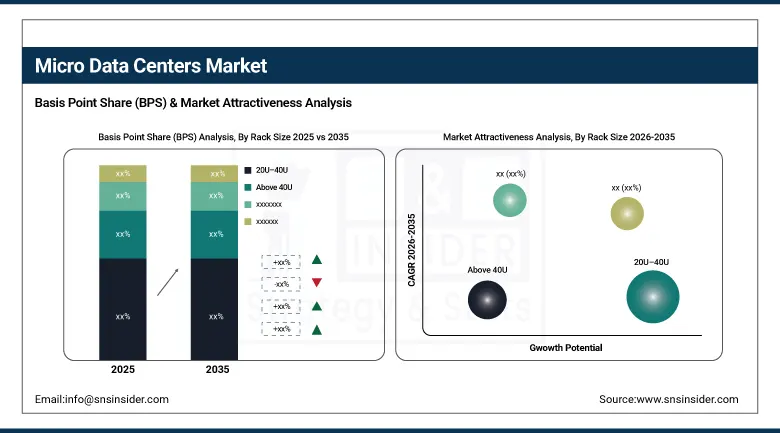

By Rack Size, 20U–40U dominated the market with 46.00% share in 2025, while above 40U is projected to witness the fastest growth with 30.76% CAGR during the forecast period.

-

By Solution Type, integrated micro data centers dominated the market with 52.00% share in 2025, while modular micro data centers are projected to witness the fastest growth with 31.31% CAGR during the forecast period.

-

By Application, edge computing dominated the market with 48.00% share in 2025, and is the fastest growing with 30.56% CAGR during the forecast period.

-

By End User, IT & telecom dominated the market with 32.00% share in 2025, while manufacturing & industrial is projected to witness the fastest growth with 30.44% CAGR during the forecast period.

By Rack Size, 20U–40U dominated, while above 40U is fastest-growing.

The 20U–40U segment held the largest revenue share of 46.00% in 2025 due to its perfect balance between computing capacity, power efficiency, deployment flexibility, and space utilization. Enterprises, telecom operators and colocation providers are more and more favoring mid-sized micro data center configurations to support edge computing, cloud applications and distributed digital infrastructure. They can support AI processing workloads, networking equipment and scalable storage systems, which makes them very appealing across various deployment environments. These rack systems provide a cost-effective solution for organizations looking for localized computing capabilities while maintaining operational efficiency and infrastructure scalability.

The above 40U segment is expected to grow at the highest CAGR of 30.76% during the forecast period owing to the increasing requirement for higher-density edge computing infrastructure supporting AI inference, industrial automation, and real-time analytics workloads. Organizations are increasingly deploying larger micro data center systems capable of supporting advanced GPU computing, 5G traffic processing and industrial IoT ecosystems. These high-capacity solutions deliver the increased processing power, storage scalability and workload consolidation capabilities needed to support data-intensive enterprise operations. The rapid growth of generative AI applications, autonomous systems, smart manufacturing facilities and connected infrastructure projects is driving significant demand for larger edge deployments.

By Solution Type, integrated micro data Centers dominated, while modular micro data centers are fastest-growing.

The integrated micro data centers segment accounted for the largest market share of 52.00% in 2025 due to increasing demand for turnkey edge infrastructure solutions combining power, cooling, networking, monitoring and security systems within a single enclosure. Enterprises are increasingly implementing integrated solutions to reduce complexity of deployment, improve operational efficiency, and accelerate digital transformation initiatives. Their plug-and-play architecture and shortened installation timelines continue to support broad commercial adoption globally. These systems offer standardized deployment frameworks that facilitate infrastructure management while maintaining high reliability and consistent performance. Market adoption is further strengthened by growing demand for rapid edge deployment across remote sites, branch locations, industrial facilities and smart infrastructure environments.

The modular micro data centers segment is projected to record the highest CAGR of 31.31% during the forecast period owing to increasing enterprise requirements for scalable, flexible, and rapidly deployable infrastructure. Organizations are increasingly adopting modular architectures that allow for phased capacity expansion at lower up-front capital expenditure. Modular solutions allow businesses to match the growth of their infrastructure to changing workload needs, providing more agility and cost optimization. In 2025–2026, a number of infrastructure vendors introduced AI-ready modular micro data center platforms with autonomous operation, remote management, and intelligent energy optimization features. disorders.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

92.00% |

|

Europe |

Germany |

25.00% |

|

Asia Pacific |

China |

28.00% |

|

Middle East & Africa |

UAE |

6.00% |

|

Latin America |

Brazil |

6.00% |

North America Micro Data Centers Market Insights

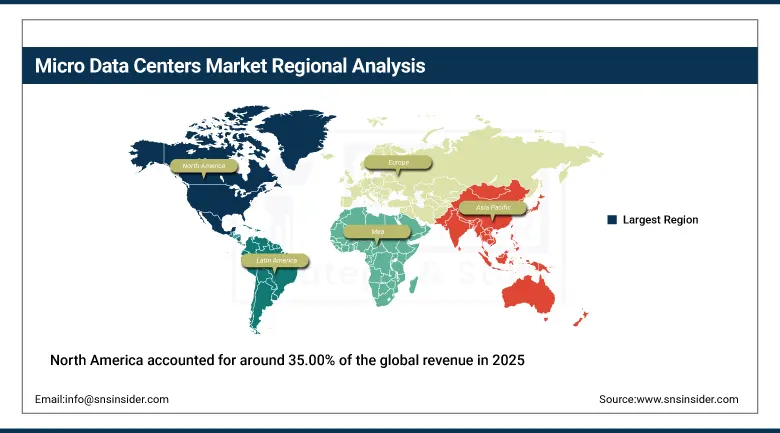

North America accounted for around 35.00% of the global revenue in 2025 and is expected to continue its dominance among all regional markets. Growth is supported by robust investment in cloud infrastructure, mature telecommunications networks, the proliferation of edge computing, and the fast commercialization of AI applications. Enterprises across the US and Canada continue to invest in distributed infrastructure to address digital transformation and low-latency computing needs. The region is home to leading hyper scale cloud providers, sophisticated data center operators and massive 5G network build out efforts. The growing uptake of AI-driven analytics, autonomous vehicles, industrial IoT applications and real-time digital services is fueling demand for localized processing capabilities.

During 2025–2026, several North American infrastructure providers expanded AI-ready edge computing solutions integrating intelligent infrastructure management and predictive operational analytics.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Micro Data Centers Market Insights

Europe accounted for a market share of nearly 25.00% in 2025 owing to increasing investments for digital infrastructure modernization, industrial automation, data sovereignty compliance, and edge computing initiatives. Organizations across Germany, the U.K., France and the Nordics are increasingly deploying localized computing infrastructure to support industrial AI, smart manufacturing and connected enterprise operations. “Driven by strong regulatory focus on data privacy, regional data processing mandates and digital sovereignty plans, enterprises are increasingly investing in edge infrastructure. The increased use of Industry 4.0 technologies, smart logistics networks and connected industrial ecosystems is creating demand for scalable micro data center solutions.

During 2025–2026, several European operators expanded deployment of distributed edge computing facilities supporting AI processing and industrial digitalization initiatives.

Asia Pacific Micro Data Centers Market Insights

Asia Pacific is anticipated to register the highest CAGR of 32.20% during the forecast period. Strong demand for distributed computing infrastructure continues to be driven by rapid urbanization, 5G rollout, industrial digitization, AI adoption and expanding cloud ecosystems across China, India, Japan, South Korea and South-east Asia. Government-backed digital transformation initiatives continue to support market expansion. The area is seeing large scale investments in smart cities, advanced manufacturing facilities, connected transportation networks, and intelligent public infrastructure, all of which require low-latency edge computing capabilities. Increasing internet penetration, growing adoption of enterprise cloud and increasing deployment of AI-enabled applications are also boosting demand for infrastructure.

During 2026, multiple technology providers across Asia Pacific introduced next-generation edge computing platforms integrating AI acceleration capabilities and intelligent workload management technologies.

Middle East & Africa and Latin America Micro Data Centers Market Insights

The Middle East & Africa market is gaining traction from smart city programs, digital infrastructure investments and growing deployment of edge-enabled computing platforms across the UAE, Saudi Arabia and South Africa. Continued adoption of AI, IoT and connected industrial ecosystems is creating new opportunities in both regions. Market development is being accelerated by government-led digital economy strategies, the expansion of 5G networks, and investments in intelligent transportation, energy, and public sector modernization projects. Furthermore, the growing demand for secure, scalable and energy efficient computing infrastructure is supporting the long term adoption of micro data center solutions in the region.

The market share of Latin America in 2025 was around 6.00% due to the growing digitalization of enterprises and cloud adoption in Brazil, Mexico, and Argentina. The demand for edge-enabled computing environments is driven by increasing investments in telecommunications infrastructure, fintech ecosystems, e-commerce platforms, and digital public services. In geographically distributed markets, companies are deploying localized infrastructure to enhance application performance, strengthen data security, and support real-time business operations.

Growth Drivers: Fast growth of edge computing and AI-based digital infrastructure.

The fast deployment of edge computing environments and AI-powered applications are one of the key factors boosting the global demand for micro data centers. The demand from enterprises for local processing capabilities is growing to support latency-sensitive workloads, real-time analytics, autonomous systems and intelligent automation platforms. The proliferation of connected devices, industrial IoT ecosystems, and next-generation telecommunications infrastructure continues to drive significant opportunities for distributed computing architectures. During the forecast period, investments in AI differencing capabilities and edge intelligence solutions are also expected to drive market growth. Micro data centers are being deployed by manufacturers, healthcare providers, retailers, transportation companies and financial services firms to enhance operational agility.

Restraints: Complexity of infrastructure integration and deployment costs.

While the growth outlook is positive, the main challenges are integration complexity, interoperability issues in infrastructure and the need for capital investment. Micro data centers generally have advanced cooling systems, power back-up facilities, network integration and cyber security architectures. Organizations that are modernizing often face operational and financial challenges in complex legacy infrastructure environments. The distributed nature of infrastructure assets at scale makes enterprise operational management complex. Connecting to existing IT environments often requires significant planning, specialized technical expertise and upgrades to network and management systems. In addition, ongoing performance, security and regulatory compliance at multiple edge locations can increase implementation costs and resource requirements.

Opportunities: AI-enabled edge infrastructure and industrial digitalization.

The growing adoption of AI-powered enterprise applications, industrial automation platforms and smart infrastructure projects are offering substantial long-term opportunities for market participants. Organizations are seeking scalable edge computing environments for machine learning, predictive analytics, autonomous operations and real-time data processing applications. The AI-powered infrastructure management, intelligent workload orchestration and predictive maintenance capabilities are expected to be the key value drivers for future commercialization opportunities across industries. The need for advanced localized computing infrastructure is being driven by Industry 4.0 initiatives, autonomous mobility systems, intelligent utilities and connected healthcare ecosystems. Today, businesses need edge solutions that offer automation, operational intelligence and more scalability to meet evolving digital needs.

Recent Developments

-

2026: Schneider Electric expanded AI-ready edge infrastructure offerings supporting intelligent monitoring and high-density computing environments.

-

2026: Vertiv introduced advanced modular edge data center solutions featuring integrated AI workload optimization capabilities.

-

2025: Hewlett Packard Enterprise expanded edge computing infrastructure platforms designed for industrial and enterprise AI deployments.

-

2025: Dell Technologies enhanced distributed infrastructure portfolios supporting edge analytics and real-time business intelligence applications.

Micro Data Centers Market Key Players

-

Schneider Electric SE

-

Vertiv Holdings Co.

-

Dell Technologies Inc.

-

Hewlett Packard Enterprise Company

-

IBM Corporation

-

Huawei Technologies Co., Ltd.

-

Rittal GmbH & Co. KG

-

Panduit Corporation

-

Hitachi Vantara LLC

-

Fujitsu Limited

-

Zella DC

-

Canovate Group

-

Delta Electronics Inc.

-

Scale Computing Inc.

-

Vapor IO Inc.

-

EdgeMicro Inc.

-

Instant Data Centers LLC

-

Baselayer Technology LLC

Micro Data Centers Market Report Scop:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.68 Billion |

| Market Size by 2035 | USD 119.30 Billion |

| CAGR | CAGR of 28.56% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size Analysis, Revenue Forecasting, Segment Analysis, Competitive Landscape, Regional Analysis, Retail Automation Assessment, Smart Checkout Technology Trends, AI-Enabled Retail Infrastructure Analysis, DROC & SWOT Analysis, Investment Trends, Supply Chain Evaluation, Consumer Transaction Technology Assessment, and Future Market Opportunity EvaluationChain Evaluation, Industrial Packaging Demand Analysis, Sustainability Assessment, DROC & SWOT Analysis, Regulatory Framework Analysis, Innovation Benchmarking, and Future Market Opportunity Evaluation |

| Key Segments | • By Rack Size (Up to 20U, 20U–40U, Above 40U) • By Solution Type (Integrated Micro Data Centers, Modular Micro Data Centers, Customized Micro Data Centers) • By Application (Edge Computing, Remote Office & Branch Office (ROBO), Industrial & IoT Deployments) • By End User (IT & Telecom, BFSI, Manufacturing & Industrial, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Schneider Electric SE, Vertiv Holdings Co., Eaton Corporation plc, Dell Technologies Inc., Hewlett Packard Enterprise Company, IBM Corporation, Huawei Technologies Co., Ltd., Rittal GmbH & Co. KG, Panduit Corporation, Cannon Technologies Ltd., Hitachi Vantara LLC, Fujitsu Limited, Zella DC, Canovate Group, Delta Electronics Inc., Scale Computing Inc., Vapor IO Inc., EdgeMicro Inc., Instant Data Centers LLC, Baselayer Technology LLC. |

Frequently Asked Questions

The Micro Data Centres Market was valued at USD 9.68 Billion in 2025.

The market is projected to reach USD 119.30 Billion by 2035.

The market is expected to expand at a CAGR of 28.56% during the forecast period.

North America dominated the global market with a 35.00% revenue share in 2025.

Integrated Micro Data Centers accounted for the largest revenue share of 52.00% in 2025.

Get in Touch