Data Center Substation Market Report Scope & Overview:

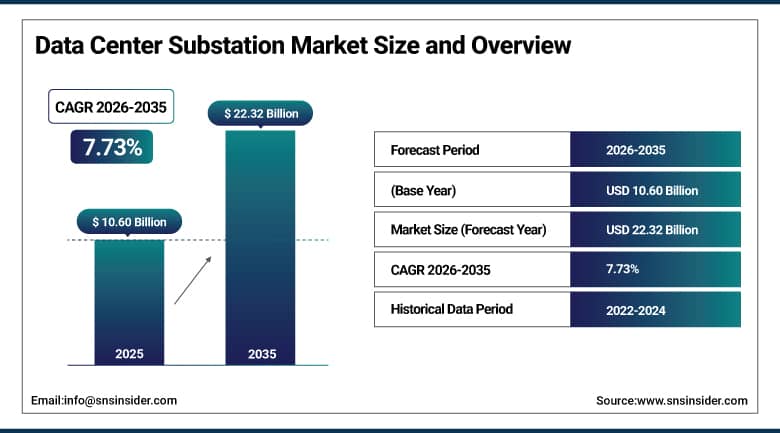

The Data Center Substation Market was valued at USD 10.60 Billion in 2025 and is projected to reach USD 22.32 Billion by 2035, expanding at a CAGR of 7.73% during the forecast period 2026–2035.

The global data center substation market is witnessing steady growth as the power consumption requirements of hyper scale cloud infrastructure, AI computing facilities, colocation campuses, and digital service ecosystems are further increasing. Data center operators are investing heavily in high capacity substations, advanced transformers, intelligent switchgear and automated power distribution systems in an effort to achieve uninterrupted power supply and operational resilience. The rapid deployment of AI workloads, high-density computing clusters, and next-generation data center campuses is driving strong demand for scalable electrical infrastructure that can support multi-megawatt operations while maintaining grid reliability and energy efficiency.

In 2025-2026, data center infrastructure providers ramped up investments in smart substations with digital monitoring, predictive maintenance platforms and AI-enabled energy management capabilities.

Market Size and Forecast:

-

Market Size 2026E: USD 11.42 Billion

-

Market Size 2035: USD 22.32 Billion

-

CAGR: 7.73% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Data Center Substation Market - Request Free Sample Report

Data Center Substation Market Trends:

-

Increasing deployment of dedicated substations for hyper scale AI data center campuses.

-

Rising integration of smart grid technologies and digital substation automation systems.

-

Growing adoption of real-time power monitoring and predictive maintenance platforms.

-

Expansion of utility-scale grid interconnection projects supporting cloud infrastructure.

-

Increasing investment in modular and prefabricated substation architectures for rapid deployment.

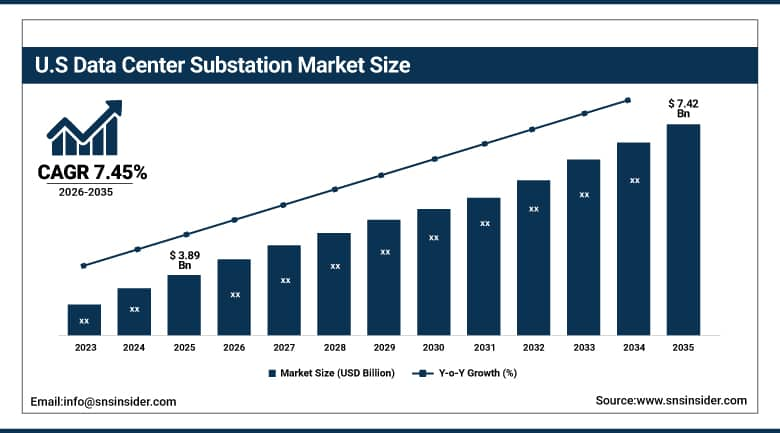

U.S. Data Center Substation Market Size Outlook:

The U.S. Data Center Substation Market was valued at USD 3.89 billion in 2025 and is expected to reach approximately USD 7.42 billion by 2035, expanding at a CAGR of 7.45% during 2026–2035.

The United States is the largest player in the global data center substation market, owing to the rapid expansion of hyper scale data centers, investments in AI infrastructure, the growth of cloud computing, and extensive digital transformation programs. Leading cloud service providers and colocation providers are increasingly constructing dedicated substations to ensure reliable access to power, increase redundancy, and power AI-rich, high-density computing environments. AI workloads are driving electricity demand increases that are prompting upgrades to utility grids and investment in transmission infrastructure in key data center markets including Virginia, Texas, Arizona and Ohio. Large-scale hyper scale campuses, attractive investment conditions, and robust demand for cloud-based services continue to underpin sustained infrastructure development.

Beginning in 2026, U.S. regulators and grid operators began efforts to speed up approvals for big-load interconnections and accommodate data center growth while ensuring grid stability.

Data Center Substation Market Segment Analysis:

-

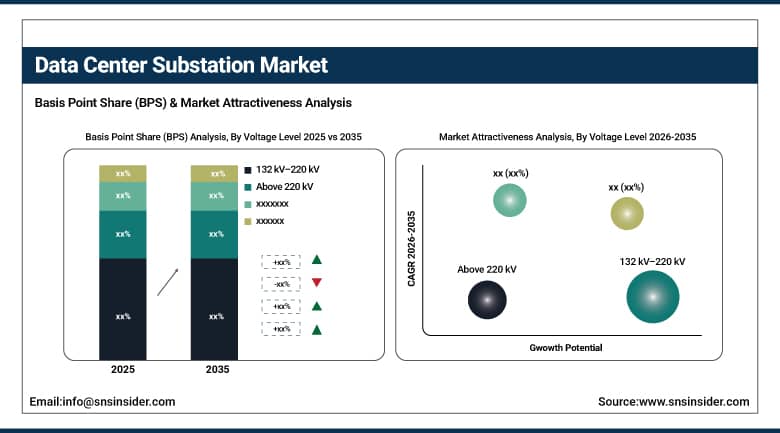

By Voltage Level, 132 kV–220 kV dominated the market with 48.00% share in 2025, while above 220 kV is projected to witness the fastest growth with 10.40% CAGR during the forecast period.

-

By Substation Type, dedicated data center substations dominated the market with 44.00% share in 2025, and is projected to witness the fastest growth with 9.75% CAGR during the forecast period.

-

By Data Center Type, hyper scale data centers dominated the market with 52.00% share in 2025, and is projected to witness the fastest growth with 9.46% CAGR during the forecast period.

-

By Component, transformers dominated the market with 38.00% share in 2025, while switchgear & protection systems are projected to witness the fastest growth with 8.38% CAGR during the forecast period.

By Voltage Level, 132 kV–220 kV dominated, while above 220 kV is fastest-growing.

The 132 kV–220 kV segment had the largest market share of 48.00% in 2025 owing to its widespread suitability for large hyper scale campuses and major colocation facilities. This voltage range is the best compromise between efficiency of transmission, cost of infrastructure and operational flexibility. The increasing deployment of medium-to-large-scale data centers worldwide has significantly strengthened the demand for substations operating in this voltage class. Grid modernization and utility interconnection initiatives continue to underpin sustained adoption across key digital infrastructure markets. The segment is especially attractive to operators looking for scalable power delivery systems that can support growing cloud workloads, enterprise colocation services and AI-enabled compute environments.

The highest CAGR of 10.40% is expected for the above 220 kV segment during the forecast period due to the massive power capacities needed by next-generation AI campuses. The deployment of high-voltage substations is increasingly supporting gig watt scale data center developments and future AI computing clusters. Recent utility planning activities show increasing demand for transmission-connected infrastructure to deliver reliable, high-capacity power to new hyper scale facilities. As the training workloads for artificial intelligence and the large-scale cloud operations continue to expand, operators are prioritizing direct access to transmission networks to ensure the long-term availability of energy.

By Component, transformers dominated, while switchgear & protection systems are fastest-growing.

The transformers segment accounted for the largest market share of 38.00% in 2025 as transformers are the core component for voltage conversion and reliable power delivery across data center infrastructure. Increasing power densities, increasing energy consumption and the proliferation of hyper scale facilities are putting huge demands on advanced transformer systems. Operators are looking at high-efficiency transformers that can support long-term scalability, grid reliability and sustainability goals. Additionally, the growing deployment of AI-enabled computing environments and high-density server deployments is also increasing the demand for transformers that can handle higher electrical loads while reducing energy losses.

The switchgear & protection systems segment is expected to record the fastest CAGR of 8.38% during the forecast period owing to increasing emphasis on fault management, operational safety and intelligent power distribution. The modern data center is requiring digital switchgear that can increasingly automate, predictively diagnose and monitor in real-time. During 2025-2026, manufacturers increased the development of smart protection systems to enhance reliability and minimize downtime in mission-critical facilities. With power networks in hyper scale and AI-centric data centers becoming more complex, the need for advanced protection technologies to detect faults, isolate disruptions and keep operations running without interruption is growing.

Regional Insights:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

94.00% |

|

Europe |

Germany |

24.00% |

|

Asia Pacific |

China |

28.00% |

|

Middle East & Africa |

UAE |

5.00% |

|

Latin America |

Brazil |

4.00% |

North America Data Center Substation Market Insights

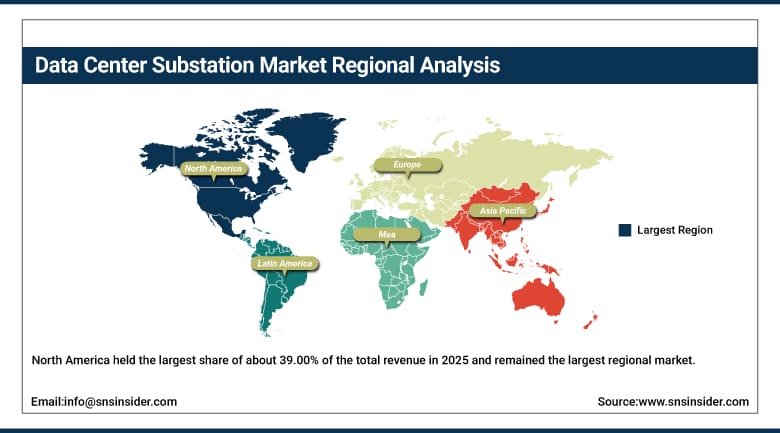

North America held the largest share of about 39.00% of the total revenue in 2025 and remained the largest regional market. Strong hyper scale investments, large-scale cloud infrastructure deployment and rising demand for AI computing continue to support extensive investment in electrical infrastructure. Power demands are growing, and data center operators are intensifying utility partnerships, transmission interconnections and dedicated substation builds to support the increasing power needs. The region has a mature digital infrastructure, significant capital investment and favorable conditions for hyper scale development. Big tech companies are rapidly building out AI training and inference facilities, creating unprecedented demand for reliable, high-capacity power networks.

In 2025-2026, the states took a number of grid modernization and regulatory actions to facilitate large-load interconnections for AI-driven data center projects. These efforts are expected to spur investment in substations, transformers and sophisticated power management infrastructure across North America.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Data Center Substation Market Insights

In 2025, Europe contributed to around 24.00% of the global market revenue, owing to the growing digitalization, cloud adoption, and investment in sustainable data center infrastructure. Germany, the UK, France and the Netherlands are expanding their data center capacity, with a focus on energy efficiency and grid reliability. An increasing number of data center operators are installing intelligent substations with advanced monitoring and automation systems to facilitate operational resilience and sustainability targets. Investments are being driven by the region’s high emphasis on reducing carbon, integrating renewable energy and developing environment-friendly infrastructure in advanced power distribution technologies.

During 2025-2026, European operators increased investments in smart grid integration, renewable energy connectivity and advanced power infrastructure technologies to boost efficiency and support future AI workloads.

Asia Pacific Data Center Substation Market Insights

The Asia Pacific region is projected to exhibit the highest CAGR of 10.77% over the forecast period, driven by the rapid adoption of cloud, accelerating digital transformation, increasing internet penetration, and substantial investments in hyper scale infrastructure. Data center construction activity continues to grow significantly in China, India, Japan, South Korea, Singapore and the South-east Asian markets. The increasing need for AI services and digital platforms in the region is creating a need for strong electrical infrastructure and sophisticated substation deployments. Governments and private investors are backing mega digital infrastructure projects to meet the growing uptake of enterprise technology and data consumption.

In 2025-2026, regional operators accelerated the deployment of large-scale AI-ready facilities with dedicated substations, digital power management platforms and smart grid integration technologies

Middle East & Africa and Latin America Data Center Substation Market Insights

The Middle East & Africa market is experiencing steady growth due to modernization of digital infrastructure, expansion of cloud services and increasing government investments into technology ecosystems. Countries such as the UAE and Saudi Arabia are investing in hyper scale facilities, smart city initiatives and digital transformation programs that require a reliable power infrastructure. Developers of data centers are turning more and more to sophisticated substations equipped with monitoring and automation systems, to underpin their performance in the long term. Strong government support of economic diversification and technology-driven development is creating the right conditions for expansion of digital infrastructure.

Latin America held a share of about 5.00% of the global market revenue in 2025. Increasing demand for cloud services, colocation facilities and enterprise digital transformation are supporting growth in Brazil, Mexico, Chile and Argentina. Operators are investing in dedicated electrical infrastructure and smart power distribution systems to improve reliability and to enable future digital expansion. Global cloud providers and colocation companies are investing more heavily in the region, spurring the growth of new, modern data center facilities. Also, the enhancements in connectivity infrastructure, favorable digital policies and increasing enterprise adoption of cloud-based technologies are driving demand for advanced substations and power management solutions.

Growth Drivers: Rapid growth in artificial intelligence and hyper scale data center infrastructure.

The rapid growth in deployment of AI computing facilities and hyper scale data centers is driving strong demand for advanced substation infrastructure around the world. AI workloads require much higher power densities than traditional computing environments, requiring operators to invest in dedicated substations, high-voltage transmission connectivity and intelligent power management systems. Global capacity is added by cloud service providers and digital infrastructure companies to meet the increasing need for data processing. This trend is resulting in a strong demand for transformers, switchgear, automation systems, and utility grid integration technologies in both developed and emerging markets. Data center operators are investing heavily in resilient electrical networks to support future digital growth and continuous operation.

Restraints: Infrastructure investment requirements and grid capacity constraints.

Despite a strong growth outlook, grid congestion, lengthy utility interconnection processes and high capital expenditure requirements for large scale substation rollout challenge the market. Dedicated substations are expensive to build, needing transformers, switchgear, transmission connections, land and regulatory approvals. The increasing demand for power by hyper scale facilities could also strain existing utility infrastructure and extend project development timelines. In many geographies, operators are challenged to find enough power capacity within preferred project schedules, especially in well-established data center markets where the demand for electricity is accelerating. Such constraints can affect expansion plans, delay the start-up of facilities and raise overall infrastructure costs.

Opportunities: Smart substations and digital power infrastructure.

Data center operators are adopting AI-enabled monitoring systems, predictive maintenance platforms, and automated power management technologies to enhance efficiency and reliability. Smart substations provide large facilities with real-time visibility into operations, faster fault detection, higher asset utilization and better energy optimization. As data center environments become more complex and consume more power, intelligent electrical infrastructure is becoming a critical differentiator in operational performance. The technologies allow operators to lower the risk of downtime, improve the planning of maintenance and optimize energy consumption. The increasing demand for high reliable data-centric infrastructure management is expected to increase the adoption of digital substation solutions in hyper scale, colocation and enterprise data center environments.

Recent Developments:

-

2026: Schneider Electric and Foxconn announced a strategic partnership to develop next-generation AI data center infrastructure, including advanced power and energy management solutions.

-

2026: The U.S. Federal Energy Regulatory Commission initiated actions to modernize large-load interconnection frameworks supporting data center expansion and grid reliability.

-

2026: Texas regulators approved a new framework for managing large-scale data center electricity demand and transmission planning requirements.

-

2026: Data center developers accelerated investments in high-capacity transmission-connected infrastructure to support growing AI computing requirements.

Data Center Substation Market Key Players:

-

Siemens Energy AG

-

Hitachi Energy Ltd.

-

ABB Ltd.

-

Eaton Corporation plc

-

General Electric Company (GE Vernova)

-

S&C Electric Company

-

NR Electric Co., Ltd.

-

Toshiba Energy Systems & Solutions Corporation

-

Hyundai Electric & Energy Systems Co., Ltd.

-

CG Power & Industrial Solutions Ltd.

-

Bharat Heavy Electricals Limited (BHEL)

-

Powell Industries, Inc.

-

Schweitzer Engineering Laboratories, Inc.

-

Vertiv Holdings Co.

-

Legrand SA

-

Delta Electronics, Inc.

-

Fuji Electric Co., Ltd.

-

Larsen & Toubro Limited

Data Center Substation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 10.60 Billion |

| Market Size by 2035 | USD 22.32 Billion |

| CAGR | CAGR of 7.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Substation Type (Utility-Owned Substations, Dedicated Data Center Substations, On-Site Distribution Substations) • By Voltage Level (Below 132 kV, 132 kV–220 kV, Above 220 kV) • By Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise & Government Data Centers) • By Component (Transformers, Switchgear & Protection Systems, Control, Automation & Monitoring Systems) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Schneider Electric SE, Siemens Energy AG, Hitachi Energy Ltd., ABB Ltd., Eaton Corporation plc, General Electric Company (GE Vernova), S&C Electric Company, NR Electric Co., Ltd., Mitsubishi Electric Corporation, Toshiba Energy Systems & Solutions Corporation, Hyundai Electric & Energy Systems Co., Ltd., CG Power & Industrial Solutions Ltd., Bharat Heavy Electricals Limited (BHEL), Powell Industries, Inc., Schweitzer Engineering Laboratories, Inc., Vertiv Holdings Co., Legrand SA, Delta Electronics, Inc., Fuji Electric Co., Ltd., Larsen & Toubro Limited. |

Frequently Asked Questions

The Data Centre Substation Market was valued at USD 10.60 billion in 2025.

The market is projected to reach USD 22.32 billion by 2035.

The market is expected to expand at a CAGR of 7.73% during the forecast period.

North America dominated the global market owing to extensive hyper scale data centre investments and advanced power infrastructure.

Hyper scale Data Centers accounted for the largest revenue share of 52.00% in 2025.

Get in Touch