Discrete Semiconductor Market Report Scope & Overview:

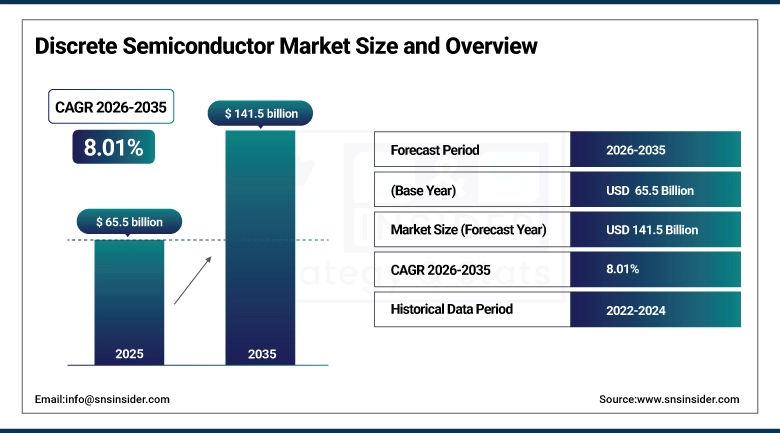

The Discrete Semiconductor Market Size was valued at USD 65.5 billion in 2025 and is expected to reach USD 141.5 billion by 2035, growing at a CAGR of 8.01% from 2026–2035.

Growth in the Discrete Semiconductor Market is fueled by extensive electrification within the automotive industry, the industrial sector, and the energy sector. Widespread acceptance of electric cars, EV charging solutions, and green energy systems leads to increased need for efficient power semiconductor components. Adoption of more automation technologies, IoT solutions, and 5G communications results in increased use of diodes, IGBTs, and rectifiers. Improvements in silicon carbide and gallium nitride semiconductors increase switching efficiencies and improve heat transfer characteristics. Digitalization, miniaturization trend, and energy-saving requirements contribute to growth.

In 2023, Nexperia launched its first silicon carbide MOSFETs at 1200V, marking its entry into the SiC power semiconductor market and signaling that SiC technology is moving from specialty producers to mainstream semiconductor companies. This broadening of the SiC supplier base will accelerate cost reduction and adoption across automotive and industrial applications.

Market Size and Forecast:

-

Market Size in 2025: USD 65.5 Billion

-

Market Size by 2035: USD 141.5 Billion

-

CAGR: 8.01% from 2026 to 2035

-

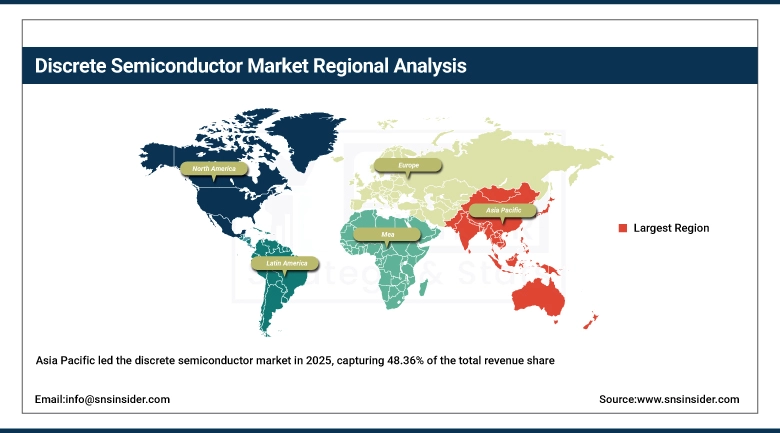

Largest Region: Asia Pacific 48.36% Revenue Share

-

Fastest Growing: North America

To Get more information on Discrete Semiconductor Market - Request Free Sample Report

Discrete Semiconductor Market Trends:

-

SiC MOSFET adoption in EV powertrains enabling 800V architecture for faster charging and extended driving range.

-

GaN power semiconductors displacing silicon in power supplies, chargers, and RF communications for superior switching performance.

-

Automotive-grade discrete semiconductor demand growing with ADAS, EV drivetrains, and software-defined vehicle architectures.

-

Industrial automation and robotics expansion driving demand for high-reliability power transistors and motor drive IGBTs.

-

Renewable energy inverter installations creating large-scale demand for high-voltage SiC and silicon power devices.

-

Wide-bandgap semiconductor cost reductions through larger wafer sizes (150mm to 200mm SiC) making advanced devices cost-competitive.

-

5G infrastructure deployment driving demand for GaN RF transistors and high-frequency switching components.

U.S. Discrete Semiconductor Market Size Outlook:

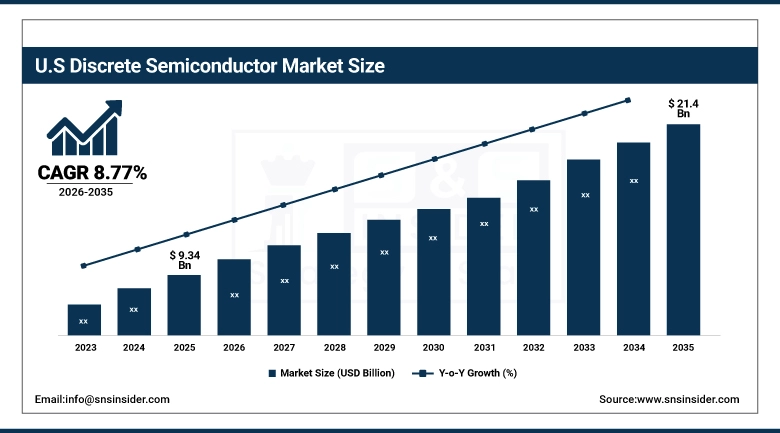

The U.S. Discrete Semiconductor Market was valued at USD 9.34 billion in 2025 and is expected to reach USD 21.4 billion by 2035, at a CAGR of 8.77% from 2026 to 2035. Drivers behind U.S. Discrete Semiconductor Industry include growing usage of electric vehicles, renewable energy systems, and advanced automation solutions. High efficiency power electronic devices' usage in data centers, 5G technology, and military equipment is also aiding the market growth. Investments in research and development in SiC and GaN contribute to market growth.

The CHIPS and Science Act's USD 52 billion semiconductor incentive program is funding new U.S. discrete semiconductor manufacturing capacity, particularly for power semiconductors supporting automotive and defense applications. SiC and GaN power device manufacturing is specifically cited as a strategic domestic manufacturing priority, supporting investment decisions by companies including onsemi, Wolfspeed, and Navitas Semiconductor.

Discrete Semiconductor Market Segment Insights:

-

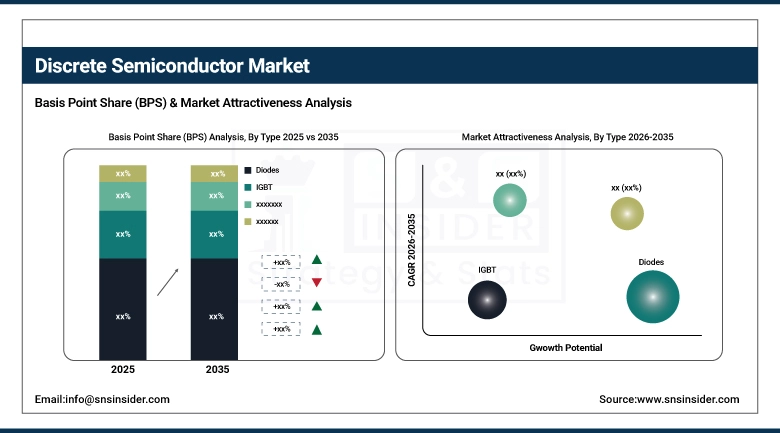

By Type, Diodes segment dominated the Discrete Semiconductor Market in 2025 with ~38% share; IGBT segment fastest growing with highest CAGR during 2026–2035.

-

By End User, Industrial segment dominated the Discrete Semiconductor Market in 2025 with ~34% share; Automotive segment fastest growing with highest CAGR during 2026–2035.

By Type, Diodes segment dominates the Discrete Semiconductor Market, IGBTs segment expected to grow fastest

Diodes segment led the discrete semiconductor industry owing to their extensive application in power management, signal processing, and protective functions. The devices play an important role in virtually all electronics products in the market, ranging from consumer goods to industrial systems and telecommunications devices. Their affordability, reliability, and ease of use make the devices critical in large-scale production. Demand from sectors like power supplies, rectifiers, and voltage regulators is another major driver for the dominance of diodes in semiconductors.

The IGBT segment is the fastest-growing product segment due to growing demand for efficient high-voltage switches in electric cars, alternative energy technologies, and automated industries. These semiconductors are energy-efficient, have faster switching speeds, and can handle high voltages, making them perfect for modern applications in power electronics. The surge in the use of electric vehicles, solar inverters, and smart grids is the primary growth driver.

By End User, Industrial segment dominates the Discrete Semiconductor Market, Automotive segment expected to grow fastest

Industrial segment leads the discrete semiconductors market owing to their usage in automation, motor controls, robotic applications, and power controls. Discrete semiconductors play an important role in increasing efficiency, reliability, and operational control in industries. With increasing demand for efficient industrial systems along with the adoption of Industry 4.0 technology, this segment will be able to retain its dominance. Owing to developments in infrastructure and automation, the demand remains high.

Automotive segment is the fastest growing segment driven by increasing use of electronic devices in hybrid, electric, and advanced driver assistance system applications. Semiconductors find wide application in vehicle battery management systems, powertrain control systems, and safety systems in vehicles. Increasing electrification of transport along with demand for smart mobility solutions will drive the demand. Increasing production of electric vehicles is further driving the growth of this segment.

Discrete Semiconductor Market Regional Analysis:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

76% |

|

Europe |

Germany |

33% |

|

Asia Pacific |

China |

52% |

|

Middle East & Africa |

Israel |

31% |

|

Latin America |

Brazil |

48% |

Asia Pacific Discrete Semiconductor Market Insights

Asia Pacific led the discrete semiconductor market in 2025, capturing 48.36% of the total revenue share, backed by robust manufacturing setups for electronics and efficient manufacturing capabilities. This dominance is fueled by the availability of prominent semiconductor fabs, burgeoning growth of automotive electrification, and rising demands for consumer electronic devices. Moreover, increased spending on industrial automation and renewable energy, together with the development of 5G networks, boosts market penetration. Furthermore, favorable government policies and supply chains add to the efficiency of production in Asia Pacific and boost its global standing in the discrete semiconductor industry.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Discrete Semiconductor Market Insights

The North American region is projected to show the highest CAGR within the discrete semiconductor market due to significant improvements made in electric vehicles, incorporation of renewable energy, and industrial automation. There have been substantial developments in the wide bandgap semiconductors market with investments being made in silicon carbide (SiC) and gallium nitride (GaN). In addition, there is also increased research and development activity in the North American region, the establishment of new data centers, and high demand for power electronic solutions.

Europe Discrete Semiconductor Market Insights

Europe’s discrete semiconductor market is propelled by the increasing trend of electric mobility, automation in industry, and utilization of renewable energy sources. The growth is supported by the rise in the need for energy-saving power semiconductors in EVs, chargers, and intelligent manufacturing. Moreover, the region is also characterized by strict energy-saving policies as well as robust research and development activities in SiC and GaN technologies.

Middle East & Africa and Latin America Discrete Semiconductor Market Insights

Discrete semiconductor demand is showing a slow but sure increase in the Middle East & Africa and Latin American markets, as a result of developing telecommunications infrastructure, renewable energy installations, and industry development. The increase in urbanization along with the proliferation of consumer electronic devices is also adding impetus to this demand. Growing investment in solar power and smart grids is helping increase demand in power semiconductors. While the manufacturing footprint remains small, import dependence is creating solid growth prospects nonetheless.

Market Growth Drivers: Rising adoption of electric vehicles, renewable energy systems, and industrial automation accelerating demand for discrete power semiconductor devices globally rapidly

The growth in electrification within the transportation, energy, and industry segments is boosting the requirement for effective switching, rectifying, and power management devices. Diodes, transistors, and thyristors are discrete semiconductor devices that play an important role in managing and manipulating electrical power in the electric vehicle powertrain, charger units, and renewable energy converters. The rising deployment of solar and wind power plants is driving the demand for efficient power devices. Moreover, industrial automation and intelligent manufacturing systems necessitate dependable power controllers for reliable performance. Advances in energy-saving electronic devices and trends toward miniaturization are contributing to their market growth.

Market Restraints: Volatility in raw material supply chains and fluctuating prices of silicon, metals, and specialty substrates affecting production stability globally persistently

The unpredictable nature of sourcing essential raw materials like silicon wafers, rare earth elements, and special gases imposes considerable production limitations for discrete semiconductor manufacturers. The price instability of these raw materials translates into higher costs of manufacturing and thus lower profits, which limits growth potential. Issues in the global logistics of raw material delivery and geopolitical risks add to these difficulties. Moreover, reliance on a few sources for obtaining highly pure raw materials makes such companies vulnerable to shortages. All of these problems lead to long production periods and delay the delivery of semiconductors to the relevant industries like the automotive industry.

Market Opportunities: Rising penetration of 5G networks, IoT ecosystems, industrial automation, and AI-driven smart devices boosting semiconductor integration demand rapidly globally expanding

The growing number of connected devices and smart systems has led to a rise in the demand for discrete semiconductors that will serve the purposes of power control, signal processing, and switching. The expansion of 5G technologies and edge computing makes it imperative to have efficient and reliable components in use within base stations, data centers, and other networking hardware. Industrial automation and smart manufacturing are increasingly leveraging advanced electronics in an effort to boost productivity and cut down on energy use. Digital transformation continues to drive increased semiconductor adoption in industries.

Recent Developments:

-

2025: Infineon Technologies completed commissioning of its new SiC MOSFET manufacturing facility in Villach, Austria the world's largest SiC power device fab adding significant capacity to serve European and global automotive customers transitioning to 400V and 800V EV architectures.

-

2024: onsemi announced a 10-year SiC supply agreement with a major European automotive OEM valued at over USD 2 billion, reflecting the long-term strategic nature of SiC supply relationships in the automotive discrete semiconductor market.

-

2023 (November): Nexperia launched its first silicon carbide (SiC) MOSFETs at 1200V in two initial product configurations, entering the SiC market and signaling the broadening of the SiC supplier base beyond specialist producers to mainstream discrete semiconductor companies.

Discrete Semiconductor Companies are:

-

Infineon Technologies AG

-

STMicroelectronics N.V.

-

NXP Semiconductors N.V.

-

Diodes Incorporated

-

ROHM Co., Ltd.

-

Littelfuse Inc.

-

Toshiba Electronic Devices & Storage Corporation

-

Mitsubishi Electric Corporation

-

Fuji Electric Co., Ltd.

-

Nexperia B.V.

-

Renesas Electronics Corporation

-

Texas Instruments Inc.

-

Wolfspeed Inc.

-

Microsemi Corporation (Microchip)

-

Semikron Danfoss

-

GeneSiC Semiconductor Inc.

-

ABB Ltd.

Discrete Semiconductor Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 65.5 Billion |

| Market Size by 2035 | USD 141.5 Billion |

| CAGR | CAGR of 8.01% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By End User (Automotive, Consumer Electronics, Communication, Industrial, Other End-use Verticals) • By Type (Diodes, IGBT, Bipolar Transistor, Thyristor, Rectifier, Other) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Infineon Technologies AG, ON Semiconductor Corporation, STMicroelectronics N.V., NXP Semiconductors N.V., Vishay Intertechnology Inc., Diodes Incorporated, ROHM Co., Ltd., Littelfuse Inc., Microchip Technology Inc., Toshiba Electronic Devices & Storage Corporation, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Nexperia B.V., Renesas Electronics Corporation, Texas Instruments Inc., Wolfspeed Inc., Microsemi Corporation (Microchip), Semikron Danfoss, ABB Ltd, GeneSiC Semiconductor Inc. |

Frequently Asked Questions

The Discrete Semiconductor Market is expected to grow at a CAGR of 8.01% from 2026 to 2035.

The Discrete Semiconductor Market was valued at USD 65.5 billion in 2025.

The major growth factor of the Discrete Semiconductor Market is the increasing adoption of electric vehicles and renewable energy systems requiring efficient power management components.

IGBT segment is fastest growing due to EVs, renewables, and efficient industrial power switching demand.

Automotive is fastest growing due to EV adoption, ADAS growth, and higher semiconductor content per vehicle.

Get in Touch