Solid State Lighting Market Report Scope & Overview:

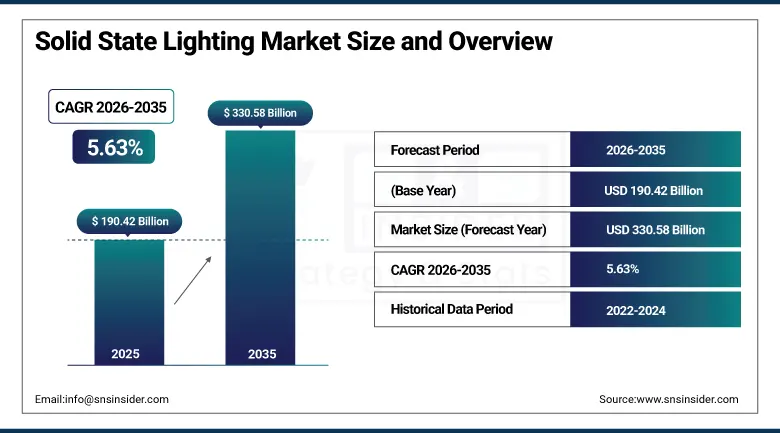

The Solid State Lighting Market was valued at USD 190.42 Billion in 2025 and is expected to reach USD 330.58 Billion by 2035, growing at a CAGR of 5.63% from 2026–2035.

The global solid state and other energy efficient lighting market is undergoing substantial transformation driven by a global regulatory shift away from energy-intensive lighting technologies toward LED and other solid-state alternatives. The market encompasses light emitting diode luminaires, organic LED panels, compact fluorescent lamps, and emerging semiconductor lighting technologies that collectively replace legacy incandescent, halogen, and fluorescent systems across residential, commercial, industrial, outdoor, and specialty lighting applications. The EU Ecodesign Directive's lamp phase-out provisions, U.S. Department of Energy efficiency standards, and fluorescent lamp phase-out commitments across 147 countries by 2027 collectively create the most commercially transformative regulatory environment in the lighting industry's history, systematically eliminating the market for inefficient lighting alternatives while expanding the addressable market for energy-efficient solutions.

In June 2024, Signify (formerly Philips Lighting) announced a significant expansion of its Interact smart lighting platform, integrating advanced AI-powered analytics for predictive maintenance, occupancy-based adaptive illumination, and building energy management system connectivity. The enhancement enables commercial facility operators to achieve measurable energy reductions beyond the LED retrofit's inherent efficiency improvement, creating a connected lighting value proposition that sustains premium specification above commodity LED alternatives in the commercial and industrial segment.

Market Size and Forecast

-

Market Size in 2026E: USD 201.14 Billion

-

Market Size by 2035: USD 330.58 Billion

-

CAGR: 5.63% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Solid State Lighting Market - Request Free Sample Report

Solid State Lighting Market Trends

-

Human-centric lighting systems are gaining adoption across commercial, healthcare, and educational facilities due to their ability to support occupant wellbeing, productivity, and circadian rhythm alignment

-

Development of micro-LED technology is advancing next-generation lighting and display applications through improved efficiency, durability, brightness, and precision control

-

Integration of Li-Fi technology with LED lighting systems is enabling simultaneous illumination and high-speed data communication, particularly in secure and RF-sensitive environments

-

Smart city initiatives are accelerating deployment of connected LED street lighting systems that offer adaptive lighting, remote monitoring, fault detection, and energy optimization capabilities

-

Growing adoption of horticultural LED lighting in controlled environment agriculture is supporting higher crop yields, improved resource efficiency, and year-round agricultural production through optimized light spectra and photoperiod management

U.S. Solid State Lighting Market Outlook

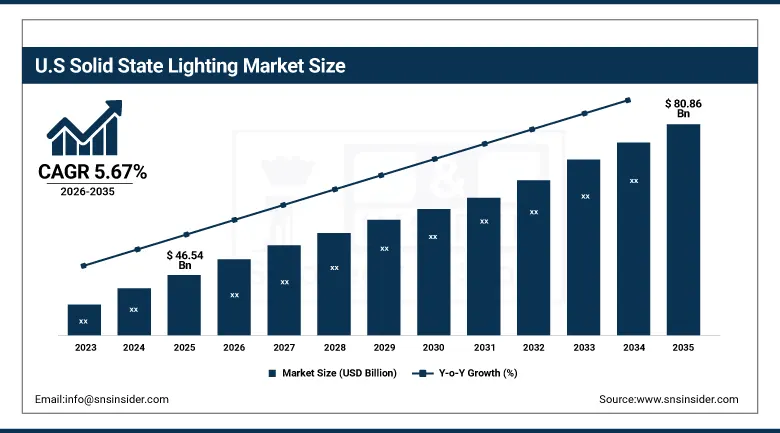

The U.S. Solid State Lighting Market was valued at approximately USD 46.54 Billion in 2025 and is expected to reach approximately USD 80.86 Billion by 2035, growing at a CAGR of approximately 5.67%.

The U.S. is a commercially sophisticated energy efficient lighting market within North America's largest regional revenue position. Acuity Brands, Signify's U.S. Philips Lighting operations, ams-OSRAM's commercial presence, Cree Lighting, GE Current, and Hubbell Lighting define the domestic commercial landscape. The DOE's 45 lm/W minimum efficacy standard for general service lamps effective August 2023 created the most commercially significant single regulatory event in the U.S. LED market's history, completing the phase-out of inefficient incandescent and halogen alternatives and ensuring LED market dominance in residential and commercial general lighting. U.S. smart city infrastructure investment and the commercial building sector's sustainability certification requirements create structured institutional LED upgrade procurement.

In March 2023, Acuity Brands launched its Atrius™ Building Intelligence platform enhancement, integrating AI-powered occupancy sensing, daylight harvesting, and building management system coordination that enables commercial facility operators to achieve 80%+ energy reduction relative to pre-LED installed base while simultaneously delivering occupancy analytics that sustain the platform's subscription revenue independent of hardware replacement cycles.

Solid State Lighting Market Segment Analysis

-

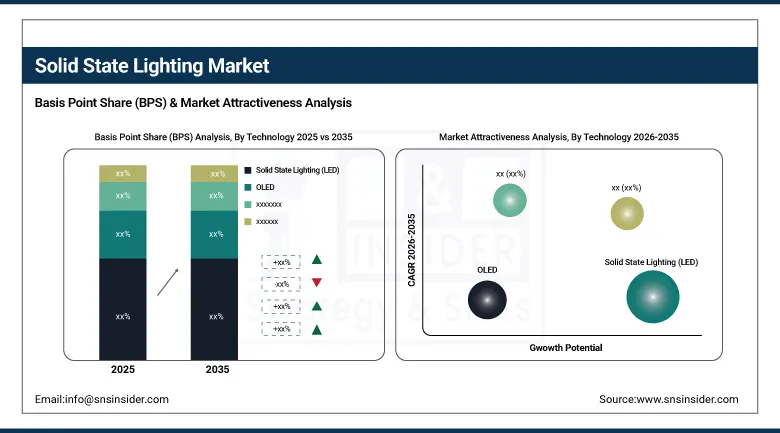

By Technology, the Solid-State Lighting (LED) segment dominated the Solid State Lighting Market with approximately 65% share in 2025, while the OLED segment is the fastest growing.

-

By Installation Type, the New Installation segment dominated the Solid State Lighting Market with approximately 58% share in 2025, while the Retrofit segment is the fastest growing.

-

By Application, the Indoor Lighting segment dominated the Solid State Lighting Market with approximately 62% share in 2025, while the Outdoor Lighting segment is the fastest growing.

-

By Vertical, the Commercial & Industrial segment dominated the Solid State Lighting Market with approximately 44% share in 2025, while the Residential segment is the fastest growing.

By Technology, SSL/LED dominates, OLED grows fastest

Solid state lighting dominated with approximately 65% of the energy efficient lighting market in 2025. LED technology's commercial dominance is the most complete technology transition in lighting history, driven by LED's extraordinary energy efficiency advantage over all legacy alternatives, its decade-long cost reduction trajectory, and the regulatory elimination of inefficient alternatives. The SSL segment held 46% of total revenue in the early forecast period and has expanded to above 65% as LED pricing continued declining and regulatory phase-outs accelerated adoption. Each government minimum efficacy standard that eliminates halogen and fluorescent alternatives creates mandatory LED adoption whose commercial impact compounds with the global installed base replacement cycle.

OLED is the fastest-growing technology because its unique physical characteristics—ultra-thin panel form, diffuse area emission eliminating hot spots and glare, flexible substrate capability for curved and shaped luminaires, and tunable color temperature—create design possibilities that LED point-source alternatives cannot replicate. Each premium automotive interior lighting specification that adopts OLED for ambient cabin illumination, each architectural installation that specifies OLED for ceiling panel integration, and each retail display lighting application whose merchandise presentation benefits from OLED's glare-free diffuse illumination creates procurement that compounds with OLED manufacturing cost reduction.

By Installation Type, new installation dominates, retrofit grows fastest

New installation retained the dominant position with approximately 58% of the energy efficient lighting market in 2025. Global construction activity's universal specification of LED as the standard new installation technology across residential, commercial, and infrastructure projects creates a structural commercial relationship that sustains new installation's market leadership. Each new residential dwelling, commercial building, and public infrastructure project creates LED luminaire procurement whose specification is the standard default rather than a premium option in virtually all markets globally. The developing world's extraordinary construction activity, particularly in Asia Pacific, Middle East, and Africa, creates above-average new installation procurement whose LED specification sustains the technology's global penetration growth.

Retrofit is the fastest-growing installation type because the regulatory phase-out of fluorescent, halogen, and high-intensity discharge alternatives is creating defined replacement timelines whose commercial procurement compresses into the period before regulatory compliance deadlines. The EU's T8 fluorescent tube phase-out, the U.S. DOE's linear fluorescent lamp efficiency standards, and equivalent national regulations across Asia and Latin America create retrofit procurement whose aggregate across the global commercial and industrial installed base represents the largest single energy efficiency investment opportunity in the lighting market's history.

By Application, indoor dominates, outdoor grows fastest

Indoor lighting retained the dominant application position with approximately 62% of the energy efficient lighting market in 2025. The extraordinary volume of indoor luminaires across residential, commercial office, retail, educational, healthcare, and industrial environments create the market's largest aggregate wattage base whose energy efficiency improvement through LED conversion creates the most commercially significant lighting investment opportunity. Each commercial office building that retrofits fluorescent office luminaires with LED alternatives, each retail store that converts spotlighting from halogen to LED, and each industrial facility that replaces high-bay HID with LED creates indoor retrofit procurement that sustains the application's commercial dominance.

Outdoor lighting is the fastest-growing application because smart city LED street lighting programme’s, transportation infrastructure investment, and the architectural facade and landscape lighting market's growth create above-average outdoor lighting procurement. Each municipality that commits to LED street lighting conversion creates a defined procurement programme whose scale ranges from thousands to hundreds of thousands of luminaire units. The smart city connectivity opportunity, where networked LED street luminaires serve as the infrastructure backbone for environmental monitoring, traffic management, and communication node deployment, sustains premium specification that conventional standalone luminaire replacement does not create.

By Vertical, commercial & industrial dominates, residential grows fastest

Commercial and industrial retained the dominant vertical position with approximately 44% of the energy efficient lighting market in 2025. The commercial and industrial sector's combination of high annual operating hours, large per-facility luminaire counts, and above-average energy cost sensitivity creates the most commercially compelling LED investment case whose energy cost savings ROI calculation typically achieves payback within 2-5 years. Each commercial building energy audit that identifies lighting as the primary energy reduction opportunity, and each industrial facility energy management programme that prioritizes lighting replacement, creates structured procurement whose investment motivation sustains commercial and industrial's dominant market position.

Residential is the fastest-growing vertical because global residential LED penetration, while advanced in developed markets, remains below saturation in the developing world whose household count growth and progressive LED adoption creates above-average unit volume procurement. Government energy efficiency incentive programme’s, utility rebate schemes for LED bulb replacement, and the declining LED bulb retail price whose competitive economics versus CFL have established LED dominance in residential purchasing collectively sustain residential segment growth. Smart home LED integration whose colour-tuneable and remote-controllable bulb adoption among tech-forward residential consumers creates above-commodity-LED commercial procurement that sustains residential vertical's commercial expansion.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Solid State Lighting Market Insights

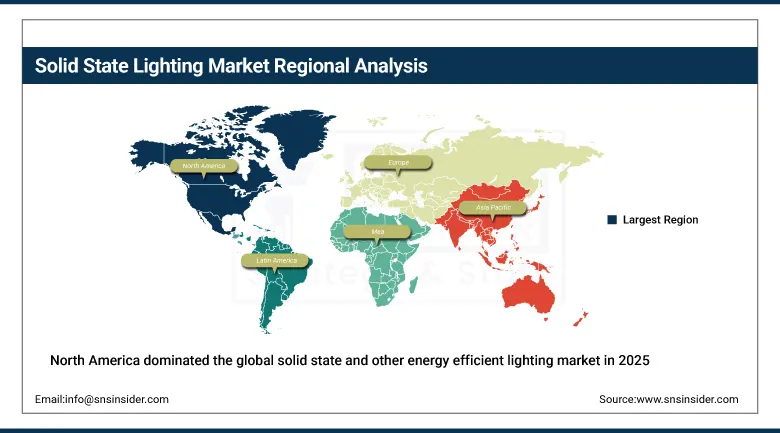

North America dominated the global solid state and other energy efficient lighting market in 2025, supported by advanced technology adoption, stringent energy efficiency mandates, and the strong commercial presence of Acuity Brands, Signify, GE Current, Cree Lighting, and ams-OSRAM. The United States accounts for approximately 87.4% of North American revenues through DOE efficiency standards, smart building LED adoption, and the commercial and industrial sector's systematic LED upgrade investment.

Canada contributes approximately 12.6% of North American revenues through its building energy efficiency programme, the commercial sector's LED adoption, and the outdoor LED street lighting investment in major Canadian municipalities.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Solid State Lighting Market Insights

Europe is the world's most regulatory-advanced energy efficient lighting market where the EU Ecodesign Directive's systematic elimination of inefficient lighting technologies creates the most commercially comprehensive LED adoption framework globally. Germany accounts for approximately 22.3% of European revenues through ams-OSRAM's domestic headquarters, Zumtobel's Austrian-headquartered European commercial presence, the industrial sector's smart lighting investment, and the commercial building sector's sustainability certification LED specification.

The United Kingdom, France, and the Netherlands are significant secondary markets where national energy efficiency programme’s, sustainable building regulations, and the retail sector's LED display lighting investment create consistent commercial demand. Signify's Dutch headquarters and LEDVANCE's European operations sustain regional market supply.

Asia Pacific Solid State Lighting Market Insights

Asia Pacific is the fastest-growing regional energy efficient lighting market, driven by China's position as the world's largest LED manufacturing and domestic consumption market, India's UJALA LED lamp programme, Japan and South Korea's smart lighting adoption, and Southeast Asia's urban infrastructure investment. China accounts for approximately 44.8% of Asia Pacific revenues through its domestic LED production scale, the government's smart city street lighting programme, and the residential and commercial construction market's LED specification.

India represents the most commercially dynamic emerging market within Asia Pacific where the UJALA programme has distributed over 367 million LED bulbs, creating the world's largest government-led LED adoption programme whose commercial impact has transformed the domestic residential and commercial lighting market.

MEA & Latin America Solid State Lighting Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its Vision 2030 smart city investment, government LED building efficiency programmes, and mega-development construction projects creating above-average Gulf LED procurement. The UAE's Expo City, NEOM, and major commercial real estate expansion add substantial complementary demand. Brazil leads Latin American revenues at approximately 44.2% through its national urban LED street lighting programme, the commercial and industrial sector's energy efficiency investment, and the growing retail sector's premium LED display lighting. Mexico's manufacturing base LED adoption and Colombia's municipal smart city programmes collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Regulatory fluorescent and halogen phase-out and smart lighting integration creating premium LED specification

The global regulatory phase-out of inefficient lighting technologies is the most commercially certain structural demand driver in the energy efficient lighting market. The EU's linear fluorescent lamp phase-out, the U.S. DOE's 45 lm/W minimum efficacy standard effective August 2023, and 147 countries' commitment to fluorescent phase-out by 2027 collectively eliminate the addressable market for inefficient alternatives while mandating LED adoption across the global lighting installation base. Each regulatory compliance deadline creates defined commercial procurement timelines whose aggregate across residential, commercial, and industrial sectors creates the most commercially predictable lighting market demand environment in history.

Smart lighting integration is simultaneously creating premium specification above commodity LED replacement by adding connected lighting platform value that justifies investment beyond energy cost savings alone. Each smart lighting system that delivers occupancy analytics, predictive maintenance, and building energy management integration creates subscription revenue streams and service relationships that sustain above-hardware pricing. Signify's Interact platform, Acuity Brands’ Atrius Building Intelligence, and OSRAM's ENCELIUM system collectively demonstrate the commercial value proposition that sustains premium lighting specification.

Restraints: High upfront cost for smart lighting systems and quality variance among lower-cost LED manufacturers

High upfront investment for connected smart lighting systems creates adoption barriers in cost-sensitive commercial segments whose ROI calculation must demonstrate energy savings and operational efficiency improvement that justifies above-commodity-LED system investment. Each commercial facility whose budget constraints priorities commodity LED replacement over smart lighting system investment creates procurement that sustains the lower-value commodity LED market segment at the expense of premium connected system adoption.

Quality variance among lower-cost LED manufacturers, particularly in Asian export markets, creates specification risk for procurement programme’s whose minimum efficacy, color rendering, and lifespan performance requirements are not met by lowest-cost alternatives. Each below-specification LED installation that underperforms promised efficacy or lifetime creates customer experience damage that moderates LED adoption confidence in cost-sensitive markets where performance guarantee mechanisms are commercially underdeveloped.

Opportunities: Horticultural LED and micro-LED next-generation display lighting

Horticultural LED represents the fastest-growing specialty application who’s photosynthetically optimized spectral output creates agricultural productivity improvements that justify premium LED specification investment. Each new vertical farming facility, greenhouse LED conversion, and cannabis cultivation facility creates horticultural LED procurement whose per-square-meter lighting intensity and spectral precision requirements create above-commodity commercial relationships.

Micro-LED technology's progression toward commercial viability creates the most commercially premium next-generation solid state lighting opportunity. Its pixel-level control, superior efficiency exceeding current LED performance, and unlimited lifespan relative to organic-degradation-limited OLED create a technology platform whose commercial adoption timeline is extending from display applications toward specialty architectural and automotive lighting where performance premium sustains above-OLED pricing.

Recent Developments:

-

2024: Signify announced a significant expansion of its Interact smart lighting platform in June 2024, integrating AI-powered analytics for predictive maintenance, occupancy-based adaptive illumination, and BEMS connectivity enabling commercial facilities to achieve energy reductions beyond LED replacement alone.

-

2024: ams-OSRAM launched its next-generation OSLON Pure 1515 LED chip family in 2024 with enhanced luminous efficacy exceeding 220 lm/W, targeting high-bay industrial luminaire and outdoor street lighting applications where energy cost reduction economics justify premium LED component specification.

-

2023: Acuity Brands launched the Atrius Building Intelligence platform enhancement in March 2023, integrating AI-powered occupancy sensing, daylight harvesting, and building management system coordination enabling commercial facilities to achieve over 80% energy reduction relative to pre-LED installed base.

-

2023: The U.S. Department of Energy's 45 lm/W minimum efficacy standard took effect in August 2023, completing the phase-out of incandescent and halogen general service lamps and establishing LED as the mandatory standard for U.S. residential and commercial general lighting.

-

2023: LEDVANCE launched its new SUN@HOME WiFi tunable LED series in 2023 for residential human-centric lighting applications, enabling smartphone-controlled color temperature adjustment that supports circadian rhythm alignment and personalized residential lighting environments without dedicated smart home hub infrastructure.

Solid State Lighting Market Key Players

-

Signify N.V. (Philips Lighting)

-

ams-OSRAM AG

-

Acuity Brands Inc.

-

Cree Lighting (IDEAL Industries)

-

GE Current (Daintree Networks)

-

Hubbell Lighting Inc.

-

LEDVANCE GmbH

-

Zumtobel Group AG

-

Nichia Corporation

-

Seoul Semiconductor Co. Ltd.

-

Everlight Electronics Co. Ltd.

-

Eaton Corporation

-

Lutron Electronics Co. Inc.

-

Legrand SA

-

Fagerhult AB

-

TRILUX GmbH & Co. KG

-

General Electric Company

-

Toshiba Corporation

-

Savant Systems LLC

-

Helvar Oy Ab

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 190.42 Billion |

| Market Size by 2035 | USD 330.58 Billion |

| CAGR | CAGR of 5.63% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Technology (Solid State Lighting/LED, OLED, Compact Fluorescent Lamp/CFL, Other Energy-Efficient Technologies) • by Installation Type (New Installation, Retrofit) • by Application (Indoor Lighting, Outdoor Lighting, Specialty Lighting) • by Vertical (Residential, Commercial & Industrial, Healthcare, Transportation, Hospitality, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Signify N.V., ams-OSRAM AG, Acuity Brands Inc., Cree Lighting, GE Current, Hubbell Lighting Inc., LEDVANCE GmbH, Zumtobel Group AG, Nichia Corporation, Seoul Semiconductor Co. Ltd., Everlight Electronics Co. Ltd., Eaton Corporation, Lutron Electronics Co. Inc., Legrand SA, Fagerhult AB, TRILUX GmbH & Co. KG, General Electric Company, Toshiba Corporation, Savant Systems LLC, Helvar Oy Ab |

Frequently Asked Questions

The Solid State Lighting Market is expected to grow at a CAGR of 5.63% from 2026 to 2035.

The regulatory phase-out of inefficient lighting technologies including fluorescent and halogen across 147+ countries by 2027 creating mandatory LED adoption, and smart lighting system integration creating connected lighting value that sustains premium specification above commodity LED replacement.

Solid State Lighting (LED) dominated with approximately 65% share in 2025, while OLED is the fastest growing segment.

North America dominated the Solid State Lighting Market in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch