Drilling Fluids Market Report Scope & Overview:

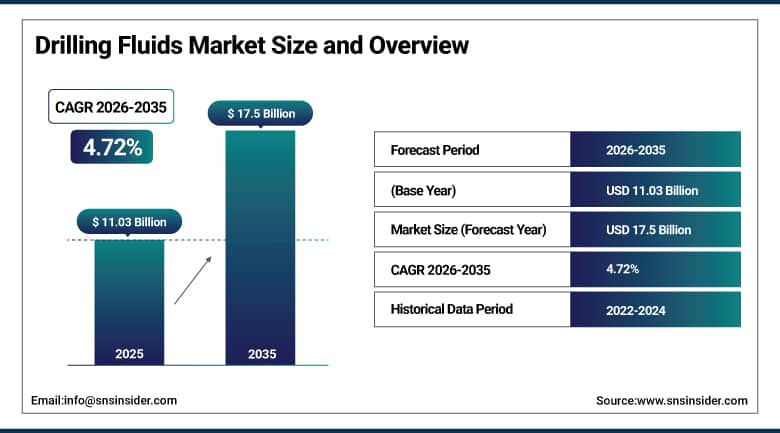

Drilling Fluids Market was valued at USD 11.03 billion in 2025 and is expected to reach USD 17.5 billion by 2035, growing at a CAGR of 4.72% from 2026-2035.

The global market for drilling fluids is mainly influenced by growing exploration efforts in the area of oil and gas, particularly in unconventional and deep-sea wells. They are important when it comes to ensuring wellbore stability and lubrication, as well as regulating pressure. The key growth drivers in this market include innovations, demand for energy, and drilling.

The U.S. Energy Information Administration reports that U.S. active rotary rig count averaged 748 rigs in 2023, with the Permian Basin alone accounting for over 330 rigs each requiring continuous drilling fluid service and chemical supply. The International Association of Drilling Contractors estimates global drilling operations consumed approximately 32 million tons of drilling fluid additives in 2023.

Drilling Fluids Market Size and Forecast

-

Market Size in 2025: USD 11.03 Billion

-

Market Size by 2035: USD 17.5 Billion

-

CAGR: 4.72% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Drilling Fluids Market - Request Free Sample Report

Drilling Fluids Market Trends

-

Nanotechnology-enhanced drilling fluid additives including nanoparticle-based fluid loss control agents and nano-clay rheology modifiers are improving performance in high-temperature, high-pressure well environments where conventional additives degrade.

-

Biodegradable and low-toxicity drilling fluid formulations are gaining regulatory and commercial preference as offshore operators face increasingly strict discharge standards from the EPA, EU, and IMO.

-

Managed pressure drilling systems require precisely engineered real-time fluid density control that is driving demand for higher-performance fluid chemistry and advanced mud monitoring technology.

-

Horizontal drilling expansion for unconventional resource development requires drilling fluids with enhanced lubricity and shale inhibition properties designed specifically for the extended horizontal sections of these wells.

-

Digital mud logging and real-time fluid monitoring using IoT sensors and AI-based anomaly detection are improving wellbore safety by enabling faster identification of gas kicks, lost circulation, and formation fluid influx events.

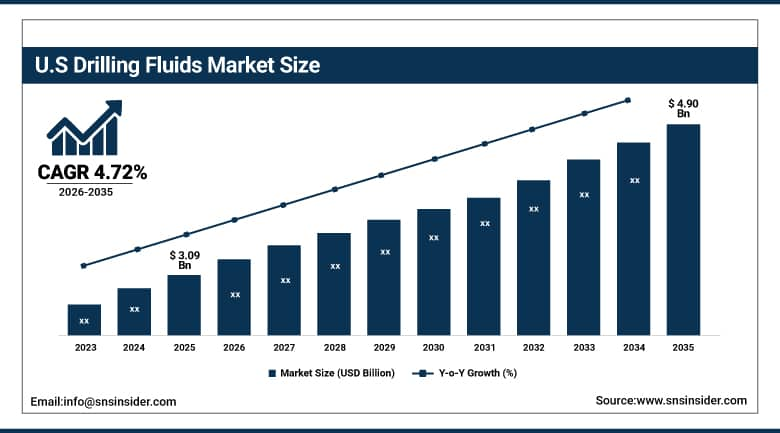

U.S. Drilling Fluids Market was valued at USD 3.09 billion in 2025 and is expected to reach USD 4.90 billion by 2035, growing at a CAGR of 4.72% from 2026-2035.

Factors contributing to the growth of the U.S. Drilling Fluids Market include the presence of extensive shale oil and gas exploration in Permian Basin and other unconventional sources. Some of the key factors responsible for driving this market include technological advancements, increase in energy demand, and utilization of performance fluids.

The U.S. Permian Basin's production reached 6.3 million barrels per day in 2024 according to EIA data, sustained by approximately 330 active rigs drilling horizontal wells that collectively require hundreds of thousands of barrels of engineered drilling fluid per day in active operations.

Drilling Fluids Market Segment Analysis

-

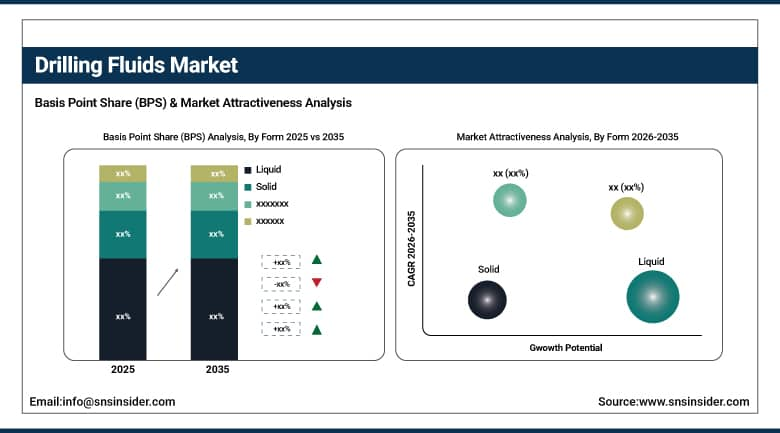

By Form, Liquid drilling fluids dominated the Drilling Fluids Market in 2025; Solid forms (lost circulation materials) growing for specialized applications.

-

By Product Type, Water-Based Fluids dominated with ~55.2% share in 2025; Synthetic-Based Fluids fastest growing (CAGR) driven by environmental performance.

-

By Application, Onshore dominated the Drilling Fluids Market in 2025; Offshore growing at a faster pace driven by deepwater investment.

-

By End-Use, Oil & Gas dominated the Drilling Fluids Market overwhelmingly in 2025; Geothermal growing fastest (CAGR).

By Form: Liquid dominates, Solid materials growing in specialized applications

Liquid drilling fluids hold the overwhelmingly dominant form position in the market which is intuitive given that drilling fluid's primary mechanical function of carrying cuttings to surface, cooling the bit, and maintaining wellbore hydrostatic pressure all require a circulating fluid medium. Water-based liquids, oil-based liquids, and synthetic-based liquids each represent a different balance of performance characteristics and environmental permissibility. The liquid form's dominance is structurally absolute for all primary drilling functions there is no solid-form alternative that can perform the fluid circulation functions that drilling requires, which means liquid drilling fluid demand grows directly with global drilling activity levels.

Solid drilling fluid materials primarily lost circulation materials (LCMs) including fibrous, granular, and flaky materials added to fluid systems when formation vugs, fractures, or permeable zones cause fluid loss into the formation represent a specialized but important product category. When a drill bit penetrates a fractured formation or a highly permeable zone, the fluid designed to flow upward around the drill pipe instead flows laterally into the formation, causing lost circulation that can range from partial returns reduction to complete fluid loss. LCM products restore fluid returns by sealing the flow paths, and their specification is tailored to the pore size distribution and fracture character of the specific lost circulation zone encountered.

By Product Type: Water-Based Fluids dominate, Synthetic-Based growing fastest

Water-Based Fluids held approximately 55.2% of the Drilling Fluids Market in 2025. Their dominance is multidimensional: water is the lowest-cost base material, water-based fluids can be discharged in many offshore environments where oil-based and synthetic fluids cannot, they are generally lower in toxicity to rig crew and environment, and they are compatible with most formation types encountered in routine drilling operations. Freshwater and seawater base fluids are modified with clay, polymers, weighting agents, and chemical additives to achieve specific rheological profiles and chemical inhibition characteristics for the formation being drilled. Inhibitive water-based fluids incorporating potassium chloride, glycol, or polyamine inhibitors provide clay stabilization in reactive shale formations that would cause wellbore instability with uninhibited water-based systems enabling water-based fluids to handle more challenging formations than was possible with earlier formulations.

Synthetic-Based Fluids are projected to grow at the fastest product type CAGR, driven by the combination of their superior performance in demanding drilling conditions and their substantially improved environmental profile relative to conventional oil-based fluids. Synthetic-based fluids using ester, polyalpha-olefin, linear paraffin, or internal olefin base stocks provide lubricity, thermal stability, and shale inhibition performance approaching that of oil-based systems while meeting the offshore discharge standards that conventional oil-based fluids cannot satisfy. Their adoption has expanded significantly as deepwater and ultra-deepwater drilling has grown at water depths where wells encounter high temperatures, high pressures, and reactive shale formations that water-based fluids struggle to stabilize, synthetic-based fluids have become the default system for technically demanding applications.

By Application: Onshore dominates, Offshore growing faster

Onshore drilling operations maintained their dominant position in Drilling Fluids Market revenue in 2025, reflecting the sheer volume of onshore drilling activity globally thousands of active onshore rigs across North America, the Middle East, China, Russia, and Latin America collectively far exceed offshore rig count in absolute numbers. North American shale horizontal drilling is the world's most intensive onshore drilling activity, consuming enormous volumes of water-based and synthetic-based drilling fluids at rates driven by the short well-life, high-density pad drilling economics of shale development.

Offshore drilling is growing at a faster pace than onshore, driven by the reinvestment cycle in deepwater and ultra-deepwater development that stalled during the 2014-2020 oil price downturn and has since recovered strongly. Brazil's pre-salt discoveries in the Santos and Campos Basins are driving some of the world's most technically demanding deepwater drilling programs, where wells reaching 7,000+ meters below mudline encounter extreme pressures and temperatures that require premium synthetic-based fluid systems. West Africa's deepwater plays offshore Angola, Nigeria, and Senegal are similarly driving deepwater drilling fluid demand at operators including TotalEnergies, Shell, and ExxonMobil.

Drilling Fluids Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

45% |

|

North America |

United States |

82% |

|

Middle East & Africa |

Saudi Arabia |

55% |

|

Europe |

Norway |

38% |

|

Latin America |

Brazil |

62% |

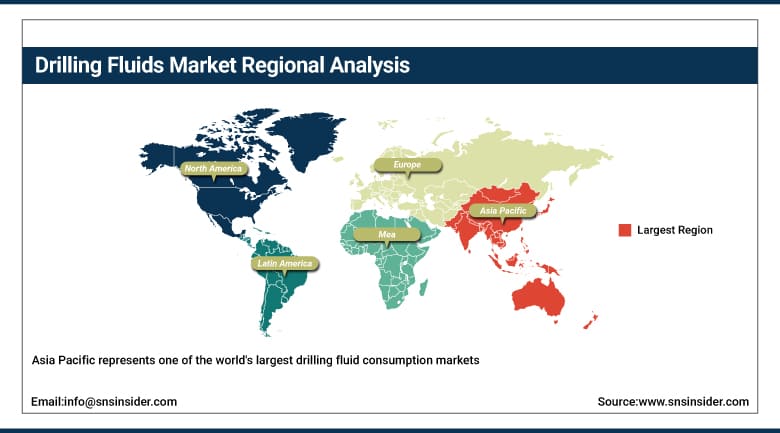

Asia Pacific Drilling Fluids Market Insights

Asia Pacific represents one of the world's largest drilling fluid consumption markets, anchored by China's extensive onshore and offshore exploration programs, India's growing oil and gas exploration investment under its HELP exploration licensing policy, and the offshore drilling activity across Southeast Asia's mature and emerging producing basins. China National Petroleum Corporation, Sinopec, and CNOOC collectively operate the world's largest national oil company drilling programs by rig count, with thousands of onshore wells drilled annually across the Tarim, Ordos, and Sichuan Basins requiring continuous drilling fluid service. India's Oil and Natural Gas Corporation has been aggressively expanding exploration drilling as the country works to reduce oil import dependency, creating growing domestic drilling fluid demand.

China's National Energy Administration reports that domestic oil and gas drilling activity reached a record 180 million meters of footage in 2023, representing the world's largest single-country drilling program by footage drilled. China's domestic drilling fluid manufacturers including Shengli Oil Field Chemical and CNOOC Drilling Service supply a substantial portion of domestic demand, creating competition with international suppliers in the world's most important drilling fluid growth market.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Middle East & Africa Drilling Fluids Market Insights

The Middle East is the world's highest-revenue single-region Drilling Fluids Market when adjusted for the density and scale of drilling programs relative to geographic area, with Saudi Arabia, UAE, Iraq, Kuwait, and Qatar all maintaining active exploration and development drilling programs of significant scale. Saudi Aramco operates the world's most productive oil fields and sustains a large program of horizontal development well drilling in Ghawar, Shaybah, and offshore fields that represents consistent, long-term demand for high-performance drilling fluid services. National Drilling Company in the UAE and Kuwait Oil Company both maintain large drilling programs using SLB, Halliburton, and Baker Hughes fluid services under long-term service contracts. The Middle East's conventional reservoir geology generally favors water-based fluid use for formation compatibility reasons, though horizontal well drilling and high-pressure high-temperature wells are driving synthetic fluid adoption in technically demanding applications.

North America Drilling Fluids Market Insights

North America holds a significant and highly active drilling fluids market dominated by the U.S. shale basins primarily the Permian Basin in West Texas and New Mexico, the Haynesville Shale in Louisiana, and the Marcellus and Utica in Appalachia. The horizontal drilling economics of shale development create distinctive drilling fluid service requirements: high-volume, fast-moving, logistics-intensive supply chains that must deliver the right fluid composition to multiple wells on a drilling pad simultaneously. Fluid service companies compete on logistics reliability, local inventory positioning, and proprietary fluid formulations that provide drilling performance advantages. Canada's WCSB conventional and oil sands development adds additional drilling fluid demand, with cold-climate SAGD operations requiring specialized high-temperature stable fluid systems.

Europe and Latin America Drilling Fluids Market Insights

Europe's drilling fluids market is concentrated in Norway's North Sea offshore operations where Equinor, Shell, and TotalEnergies maintain some of the world's most technically demanding deepwater drilling programs and in the UK North Sea's mature field infill drilling activity. Norway's offshore environmental regulations are among the world's most stringent, creating a market that preferentially selects environmentally certified synthetic-based fluids and mandates drill cuttings treatment before discharge in most offshore operations. Latin America is the most dynamic regional drilling fluid growth market, driven by Brazil's extraordinary deepwater pre-salt development program. Petrobras's pre-salt well drilling at 7,000+ meters total depth requires specialized ultra-high-pressure synthetic fluid systems that represent the technical frontier of deepwater fluid engineering, sustaining premium revenue and technical development investment from leading fluid service companies.

Drilling Fluids Market Growth Drivers:

-

Growing global energy demand and unconventional resource development driving sustained drilling fluids market growth worldwide

Despite the energy transition narrative, global oil and gas demand has not peaked it grew in 2023 and 2024, and the IEA projects demand growth continuing at least through the early 2030s driven by aviation, shipping, and petrochemicals rather than personal transportation. That demand growth requires continued investment in oil and gas production, which means drilling new wells, which means sustained drilling fluid consumption. The shift toward horizontal drilling for both unconventional resources (shale) and extended-reach wells in conventional fields is systematically increasing the technical complexity of drilling fluid requirements horizontal wells require substantially more lubrication, shale inhibition, and torque-and-drag reduction capability than vertical wells, pulling demand toward premium specialty fluid systems. Deepwater and ultra-deepwater frontier exploration which remains necessary to discover the large reserve additions required for long-term supply security requires the most technically sophisticated and expensive fluid systems in the market, sustaining premium revenue density per-well.

BP's Energy Outlook projects that global oil demand will remain above 80 million barrels per day through 2035 even in accelerated energy transition scenarios, requiring sustained upstream investment in new well drilling that directly sustains drilling fluid market demand. The IEA's upstream investment tracking documents that global oil and gas exploration and development spending reached USD 570 billion in 2023, a four-year high.

Drilling Fluids Market Restraints:

-

Crude oil price volatility and environmental regulations creating investment uncertainty in the drilling fluids market

The drilling fluids market's single most significant structural vulnerability is its dependence on oil price as the primary determinant of drilling investment levels. When crude oil prices fall below operators' breakeven thresholds which vary by basin, well design, and company cost structure drilling programs are cut, rig contracts are cancelled, and drilling fluid demand drops in direct proportion. The 2020 pandemic-driven oil price collapse demonstrated how rapidly drilling activity can contract U.S. rig counts fell from 800+ to under 300 in a matter of months, devastating drilling fluid service revenues. Environmental regulatory pressure creates a different kind of challenge: each new restriction on drilling fluid discharge or disposal requirements adds operational complexity and cost that can slow drilling program pace and increase the per-well fluid cost that operators must absorb.

Drilling Fluids Market Opportunities:

-

Deepwater exploration expansion and geothermal drilling growth creating significant new drilling fluids market opportunities

Deepwater and ultra-deepwater exploration represents the drilling fluids market's highest-value growth opportunity both in terms of per-well revenue and in the technical differentiation that premium fluid chemistry provides. As operators push into 3,000-4,000 meter water depths and encounter bottomhole temperatures above 200°C and pressures above 20,000 psi, the fluid requirements become technically extreme in ways that commodity products cannot address and that justify significant investment in proprietary formulation expertise. Geothermal drilling is emerging as a genuinely new demand category that did not materially contribute to drilling fluid market revenue a decade ago: governments in Iceland, Kenya, Indonesia, the Philippines, and increasingly across Europe and the U.S. are expanding geothermal power development programs that require specialized high-temperature drilling fluid systems distinct from both conventional oil and gas fluid technology and standard water well drilling practices.

Recent Developments:

-

2025: SLB (Schlumberger) launched its NOVATEK High-Performance Synthetic Base Fluid System designed specifically for ultra-high-pressure, ultra-high-temperature (HPHT) deepwater applications, demonstrating stable rheological performance at 220°C bottomhole temperature and 30,000 psi wellbore pressure in qualification testing for a Gulf of Mexico deepwater operator.

-

2025: Halliburton introduced its Baroid OptiDrill AI-powered drilling fluid monitoring platform that continuously analyzes real-time drilling data including flowline temperature, gas readings, and pump pressures to predict and recommend fluid adjustments before wellbore instability events occur reporting a 40% reduction in non-productive time related to fluid-related wellbore instability issues across 150 deployed wells.

Drilling Fluids Market Key Players

Some of the Drilling Fluids Market Companies

-

SLB (Schlumberger)

-

Halliburton Company

-

Baker Hughes Company

-

Newpark Resources Inc.

-

Tetra Technologies Inc.

-

Scomi Group Bhd

-

Secure Energy Services Inc.

-

National Oilwell Varco Inc.

-

Weatherford International plc

-

Anchor Drilling Fluids USA LLC

-

CESI Chemical

-

Drilling Fluids Technology (DFT)

-

Chevron Phillips Chemical Company

-

Aramco Products

-

Calfrac Well Services Ltd.

-

Safecore Ltd.

-

Global Drilling Support International

-

M-I SWACO (SLB subsidiary)

-

Henkel AG & Co. KGaA

-

Huvis Water Solutions

Drilling Fluids Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.03 Billion |

| Market Size by 2035 | USD 17.5 Billion |

| CAGR | CAGR of 4.72% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form (Solid, Liquid) • By Product Type (Water-Based Fluids, Oil-Based Fluids, Synthetic-Based Fluids, Others) • By Application (Onshore, Offshore) • By End-Use (Oil & Gas, Geothermal, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | SLB (Schlumberger), Halliburton Company, Baker Hughes Company, Newpark Resources Inc., Tetra Technologies Inc., Scomi Group Bhd, Secure Energy Services Inc., National Oilwell Varco Inc., Weatherford International plc, Anchor Drilling Fluids USA LLC, CESI Chemical, Drilling Fluids Technology (DFT), Chevron Phillips Chemical Company, Aramco Products, Calfrac Well Services Ltd., Safecore Ltd., Global Drilling Support International, M-I SWACO (SLB subsidiary), Henkel AG & Co. KGaA, Huvis Water Solutions. |

Frequently Asked Questions

Ans: Asia Pacific dominated the Drilling Fluids Market in 2025.

Ans: The Onshore segment dominated the Drilling Fluids Market in 2025.

Ans: Water-Based Fluids dominated with approximately 55.2% share in 2025; Synthetic-Based Fluids are the fastest growing.

Ans: The Drilling Fluids Market was valued at USD 11.03 billion in 2025.

Ans: The Drilling Fluids Market is expected to grow at a CAGR of 4.72% from 2026 to 2035.

Get in Touch