Polyurethane Sealants Market Report Scope & Overview:

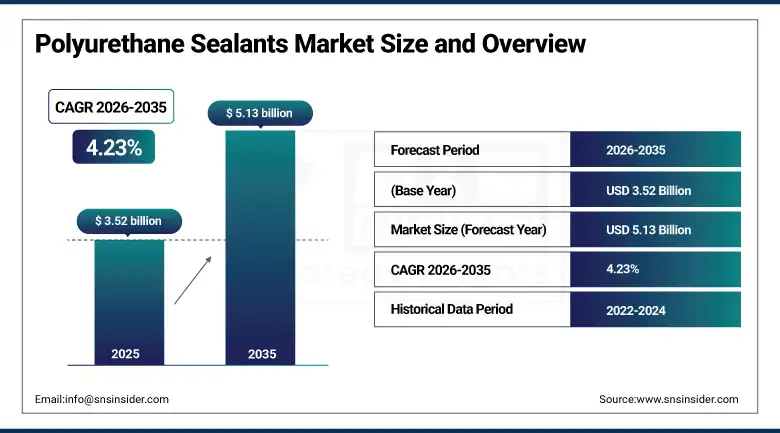

The Polyurethane Sealants Market was valued at USD 3.52 Billion in 2025 and is expected to reach USD 5.13 Billion by 2035, growing at a CAGR of 4.23% from 2026 to 2035.

Polyurethane sealants are high-end polymer-based products designed for use in joining areas in construction, automobiles, marines, and industrial manufacturing sectors. They combine features of superior adhesion, elasticity, weathering capacity, and mechanical strength, thus enabling them to be used in places where movement, vibrations, and thermal changes exist. Polyurethane sealants differ from other sealants by retaining their elasticity over time yet ensuring good bonding on different surfaces like metal, concrete, glass, wood, and plastic. The sealant composition of isocyanate-polyols makes it possible for producers to modify its properties such as modulus, hardness, elongation, and resistance to various conditions. Polyurethane sealants find application in facade glazing, flooring, automobile windscreens, marine assembly, and industries.

In 2025, Mapei announced a strategic partnership with a major global distributor to expand the availability of its polyurethane sealant products across new international markets, targeting the growing construction sector demand in Southeast Asian and Latin American countries whose building activity expansion and progressively demanding sealant specification standards create commercial growth opportunities beyond Mapei's established European and North American market positions. The partnership demonstrates the growing globalization of construction sealant specification whose adoption of international performance standards including ISO 11600 and ASTM C920 is creating uniform product performance expectations that benefit established polyurethane sealant brands with documented compliance track records over locally produced lower-performance alternatives.

Market Size and Forecast

-

Market Size in 2026E: USD 3.67 Billion

-

Market Size by 2035: USD 5.13 Billion

-

CAGR: 4.23% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Polyurethane Sealants Market - Request Free Sample Report

Polyurethane Sealants Market Trends

-

Rising demand for low-VOC and solvent-free polyurethane sealants is driven by increasingly stringent environmental regulations.

-

One-component moisture-cure polyurethane sealants are gaining popularity due to ease of application and improved consistency.

-

Growing development of bio-based polyurethane sealants is supporting sustainability initiatives in construction and automotive industries.

-

Increasing adoption of structural adhesive sealants in vehicle light weighting programs is expanding automotive applications.

-

BIM-integrated specification tools and digital product selection platforms are improving sealant selection and project efficiency in construction.

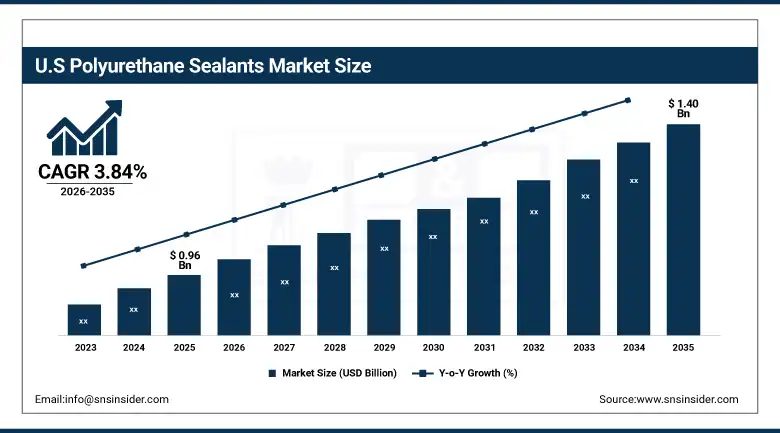

The U.S. Polyurethane Sealants Market Outlook

The U.S. Polyurethane Sealants Market was valued at approximately USD 0.96 Billion in 2025 and is expected to reach approximately USD 1.40 Billion by 2035, growing at a CAGR of approximately 3.84%. North America dominated the global Polyurethane Sealants market in 2025, driven by the large U.S. construction sector's sustained demand for high-performance joint sealants and the automotive industry's growing structural sealant consumption.

The United States market for polyurethane sealants is fueled by a growing demand for them in the construction and automotive sectors. For both commercial and residential construction projects, the demand for polyurethane sealants is due to their applications in windows, doors, expansion joints, floors, roofs, and waterproofing. With growing environmental regulations such as U.S. Environmental Protection Agency guidelines and those from California regarding volatile organic compound emissions, the adoption rate for low-volatile organic compound sealants and other environmentally friendly sealants is increasing. Other drivers include technological innovations that will make manufacturers produce superior and sustainable products. The automotive industry also plays an important role in fueling the demand for polyurethane sealants owing to their use in assembling vehicles, windshield bonding, and glass replacement for existing vehicles.

In Q3 2024, 3M debuted a new polyurethane sealant specifically engineered for marine and offshore applications, offering enhanced resistance to saltwater exposure, UV degradation, and the sustained immersion and splash zone conditions that marine vessel hull and deck sealing requires over extended service periods between dry-dock maintenance intervals. The product launch demonstrated the ongoing expansion of polyurethane sealant chemistry into demanding specialty applications whose performance requirements exceed what conventional silicone or polysulfide chemistry can sustain across the environmental exposure spectrum of marine service, creating a premium market segment where polyurethane's unique combination of flexibility, adhesion, and chemical resistance commands significant price premiums over commodity construction sealant grades.

Polyurethane Sealants Market Segment Analysis

-

By Type, one-component polyurethane sealants segment dominated the polyurethane sealants market with approximately 68% market share in 2025, while the two-component polyurethane sealants segment is projected to be the fastest growing, registering a CAGR of around 5.9% during 2026–2035.

-

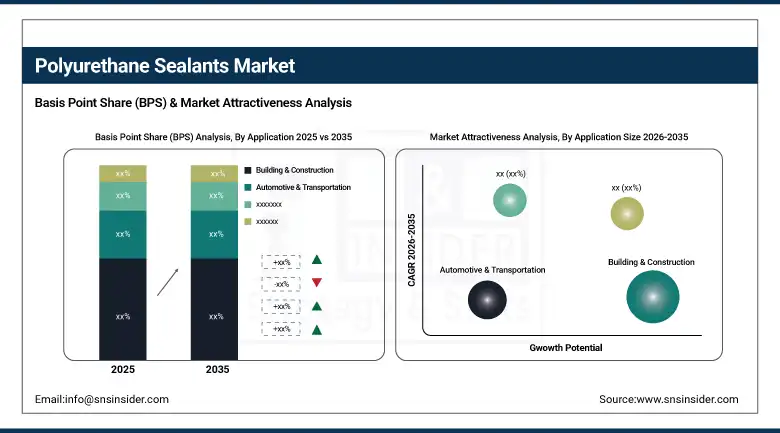

By Application, building & construction dominated the Polyurethane Sealants market with the largest share in 2025, while the flooring & joining application is among the fastest growing during 2026 to 2035.

-

By End-Use Industry, the building & construction segment dominated the Polyurethane Sealants market in 2025, while the automotive segment is the fastest growing end-use industry during the forecast period.

-

By Technology, moisture cure technology dominated the Polyurethane Sealants market in 2025, while UV cure systems are the fastest growing technology during 2026 to 2035.

By Type, one-component sealants dominate, two-component systems fastest growing

One-component polyurethane sealants generated the dominant market revenue share in 2025, reflecting their practical advantages in construction and general industrial application contexts where on-site material mixing is operationally impractical, quality-inconsistent, or prohibited by specification. One-component moisture-cure polyurethane sealants, which cross-link upon exposure to atmospheric humidity without requiring the precise metering and mixing of isocyanate and polyol components that two-component systems demand, deliver installation simplicity, consistent formulation quality, and unlimited pot life before dispensing that makes them the preferred choice for the broadest range of construction, maintenance, and manufacturing applications. Their application in window and door frame sealing, expansion joint filling, perimeter caulking, and general construction waterproofing across millions of annual construction projects creates a market volume base.

Two-component polyurethane sealants serve the premium application segments where their superior cohesive strength, chemical resistance, and mechanical performance justify their higher application cost and complexity. Structural glazing applications where glass panels are adhesively bonded to building frames through sealant joints that must carry sustained dead load require the structural integrity that only two-component high-modulus polyurethane systems can reliably provide. Industrial floor joint sealing applications where vehicle traffic loads and chemical spill exposure demand sealant performance beyond one-component products' capability represent a commercially significant two-component application whose growth tracks industrial floor construction activity.

By Application, building & construction dominates, automotive grows fastest

Building and construction generated the dominant application revenue share in 2025, underpinned by the enormous and diverse sealant requirements of the global construction industry across facade glazing, expansion joint sealing, window and door installation, roofing system sealing, flooring installation, and concrete structure waterproofing whose combined polyurethane sealant consumption spans every building type and construction method. The non-discretionary nature of building envelope sealant application, whose performance directly determines building weather tightness and energy performance whose regulatory compliance and warranty obligation create mandatory specification requirements, sustains construction sealant demand through construction market cycles with greater stability than discretionary construction material categories.

The flooring & jointing application segment is among the fastest-growing areas of the polyurethane sealants market, projected to expand steadily through 2035. Growth is being driven by rising investments in residential, commercial, and industrial construction projects that require durable, flexible, and long-lasting joint sealing solutions. Polyurethane sealants are widely used in flooring systems, expansion joints, concrete slabs, and tile installations due to their excellent adhesion, elasticity, abrasion resistance, and ability to accommodate structural movement. Increasing urbanization, infrastructure modernization, and renovation activities are further supporting demand for high-performance flooring and jointing materials. Additionally, the growing preference for seamless flooring systems in warehouses, manufacturing facilities, healthcare buildings, and commercial spaces is creating sustained demand for polyurethane sealants that ensure durability, moisture resistance, and long-term structural integrity.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

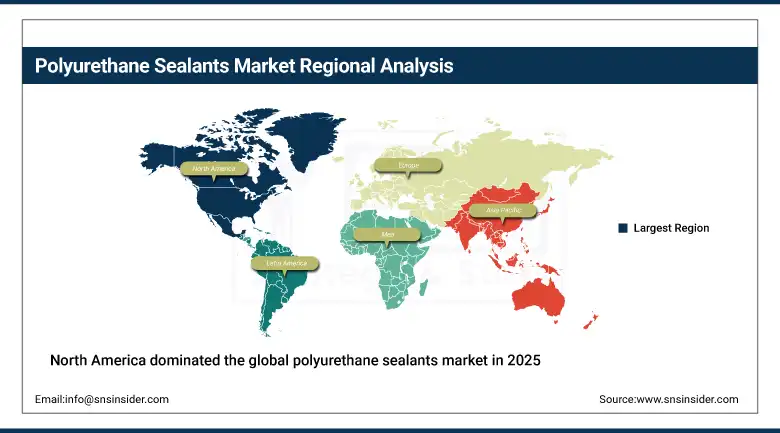

North America Polyurethane Sealants Market Insights

North America dominated the global polyurethane sealants market in 2025, holding the largest regional revenue share of around 38%. The United States accounts for approximately 82.47% of regional revenue through its large construction market's diverse sealant requirements, the domestic automotive industry's structural sealant consumption, and the commercial sophistication of its construction specification culture whose performance-based sealant selection favours proven high-performance polyurethane chemistry over lower-cost alternatives. The commercial presence of major polyurethane sealant manufacturers including Sika, Henkel, H.B. Fuller, and Dow Corning whose North American operations and distribution networks sustain broad market accessibility contributes to the region's commercial leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Polyurethane Sealants Market Insights

Europe held a significant share of global polyurethane sealants revenues in 2025. Germany, France, the United Kingdom, Italy, and the Netherlands are the leading national markets, each hosting significant construction, automotive manufacturing, and industrial sectors whose polyurethane sealant consumption spans the full application spectrum from facade glazing through automotive seam sealing through industrial equipment assembly. Germany accounts for approximately 28.47% of European revenues through its premium automotive manufacturing sector's structural sealant consumption, its large construction market, and the commercial presence of major global sealant manufacturers whose European headquarters sustain regional market development. European VOC emission regulations under the Paints and Varnishes Directive have been a significant driver of low-VOC polyurethane sealant formulation development whose technical progress has expanded compliant product availability across the full performance range.

Asia Pacific Polyurethane Sealants Market Insights

Asia Pacific is the fastest-growing regional polyurethane sealants market, driven by the rapid expansion of construction activity across China, India, Southeast Asia, and Australia, the growing automotive manufacturing sector whose increasing vehicle output creates structural sealant demand, and the progressive adoption of international sealant performance standards that are raising specification requirements across the region's construction and industrial sectors. China accounts for approximately 38.47% of Asia Pacific revenues through its world-leading construction volume, large domestic automotive production whose sealant content per vehicle is growing with structural bonding adoption, and the expanding chemical manufacturing infrastructure that supplies domestic polyurethane sealant production.

MEA & Latin America Polyurethane Sealants Market Insights

Middle East and Latin America are growing polyurethane sealants markets where expanding construction programmes, industrial facility development, and the globalization of automotive manufacturing are creating growing demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through the extraordinary scale of its commercial and residential construction programme, whose building envelope sealing requirements for the demanding Gulf climate including extreme UV exposure, high temperature cycling, and persistent wind-driven rain create particularly stringent sealant performance requirements that premium polyurethane products address more reliably than commodity alternatives. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large construction market, growing automotive manufacturing sector, and the industrial sealant demand from its petroleum and mining sectors.

Market Dynamics

Growth Drivers: Global construction activity expansion and automotive structural bonding adoption are creating compounding structural demand

The polyurethane sealants market's growth is driven by the simultaneous expansion of its two primary end-use markets and the progressive premiumization of sealant specification within each. Global construction activity growth, particularly in Asia Pacific and the Middle East where construction investment rates substantially exceed GDP growth as infrastructure and urban development programmes are prioritized, creates growing volumes of new joint sealing requirements whose long-term weather exposure and movement accommodation demands favor polyurethane chemistry over lower-performing alternatives. The automotive industry's structural bonding adoption creates a per-vehicle sealant content growth vector that operates independently of total vehicle production volume, as each additional vehicle model generation's structural adhesive sealant application adds incremental polyurethane sealant content whose compound effect across millions of annual vehicles creates substantial market demand growth from technology adoption alone.

Restraints: Raw material cost volatility for isocyanate and polyol feedstock’s and competition from silicone sealants in high-temperature applications constrain polyurethane sealant market growth

Polyurethane sealant production depends on isocyanate and polyol feedstock’s whose pricing is closely linked to toluene di-isocyanate and MDI production economics and petroleum-derived raw material costs, creating input cost volatility that periodically compresses sealant manufacturer margins and forces price increases that reduce demand in cost-sensitive construction applications. Silicone sealants retain competitive advantage in high-temperature facade applications whose sustained exposure above 150 degrees Celsius degrades polyurethane chemistry while silicone maintains performance integrity, limiting polyurethane's penetration in curtain wall glazing applications in climates with extreme solar radiation loading. Regulatory compliance costs for low-VOC reformulation in markets with stringent emission standards add product development investment that smaller polyurethane sealant manufacturers may lack the resources to pursue simultaneously across all required product grades.

Opportunities: Bio-based polyurethane sealant development and emerging market construction growth represent significant commercial expansion opportunities

The development of commercially viable bio-based polyurethane sealants incorporating plant-derived polyol content from castor oil, soybean oil, and sugarcane-derived succinic acid represents a product innovation direction whose commercial momentum is building as both regulatory pressure on petroleum-derived raw materials and corporate procurement sustainability commitments create market pull for verified bio-content documentation. Each bio-content percentage point incorporated into polyurethane sealant formulations without performance compromise creates a differentiation argument for sustainability-conscious specification that commands price premiums in green building construction markets. Emerging market construction growth in India, Southeast Asia, Africa, and Latin America represents a progressive market development opportunity as construction quality standards rise, building codes incorporate sealant performance requirements, and distributor networks improve product accessibility beyond current major urban market concentration.

Recent Developments:

-

2025: Mapei entered a strategic partnership with a major global distributor to expand its polyurethane sealant product availability across Southeast Asian and Latin American markets, targeting the growing construction sector demand in rapidly developing economies whose building quality standards are progressively adopting international polyurethane sealant performance specifications.

-

2024: 3M launched a new polyurethane sealant specifically engineered for marine and offshore applications with enhanced saltwater resistance, UV stability, and sustained immersion performance, targeting the premium marine vessel hull and deck sealing segment where conventional sealant chemistry cannot maintain adhesion integrity across the harsh environmental exposure of marine service.

-

2023: Sika AG expanded its polyurethane structural sealant and adhesive portfolio for automotive lightweight body construction, introducing new low-density structural sealant formulations compatible with the increasing use of aluminium, carbon fibre, and multi-material body assembly techniques in next-generation premium and electric vehicle platforms.

Polyurethane Sealants Market Key Players are:

-

Sika AG

-

Henkel AG & Co. KGaA

-

H.B. Fuller Company

-

BASF SE

-

3M Company

-

Bostik SA (Arkema)

-

Mapei SpA

-

Dow Inc. (Dow Corning)

-

Wacker Chemie AG

-

Momentive Performance Materials Inc.

-

Tremco Inc. (RPM International)

-

GCP Applied Technologies Inc.

-

Bondo Corporation (3M)

-

Den Braven Group

-

Würth Group

-

Illbruck (Tremco)

-

Permabond LLC

-

Sikaflex (Sika AG)

-

Master Bond Inc.

-

Hernon Manufacturing Inc.

Polyurethane Sealants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.52 Billion |

| Market Size by 2035 | USD 5.13 Billion |

| CAGR | CAGR of 4.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (One-Component Polyurethane Sealants, Two-Component Polyurethane Sealants) • By Application (Building & Construction, Automotive & Transportation, Aerospace & Marine, Flooring & Joining, Electrical & Electronics, Others) • By End-Use Industry (Building & Construction, Automotive, Industrial, Consumer) • By Technology (Moisture Cure, Heat Cure, UV Cure, Solvent Cure) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sika AG, Henkel AG & Co. KGaA, H.B. Fuller Company, BASF SE, 3M Company, Bostik SA (Arkema), Mapei SpA, Dow Inc. (Dow Corning), Wacker Chemie AG, Momentive Performance Materials Inc., Tremco Inc. (RPM International), GCP Applied Technologies Inc., Bondo Corporation (3M), Den Braven Group, Würth Group, Illbruck (Tremco), Permabond LLC, Sikaflex (Sika AG), Master Bond Inc., and Hernon Manufacturing Inc. |

Frequently Asked Questions

The polyurethane sealants market is expected to grow at a CAGR of 4.23% from 2026 to 2035.

The polyurethane sealants market was valued at USD 3.52 Billion in 2025.

Expanding global construction activity, increasing automotive structural bonding applications, growing adoption of building performance standards, and rising demand for low-VOC sealant formulations.

The building & construction segment dominated the polyurethane sealants market in 2025 as the largest application category.

North America dominated the polyurethane sealants market in 2025, holding the largest regional revenue share.

Get in Touch