Ductile Iron Pipes Market Report Scope & Overview:

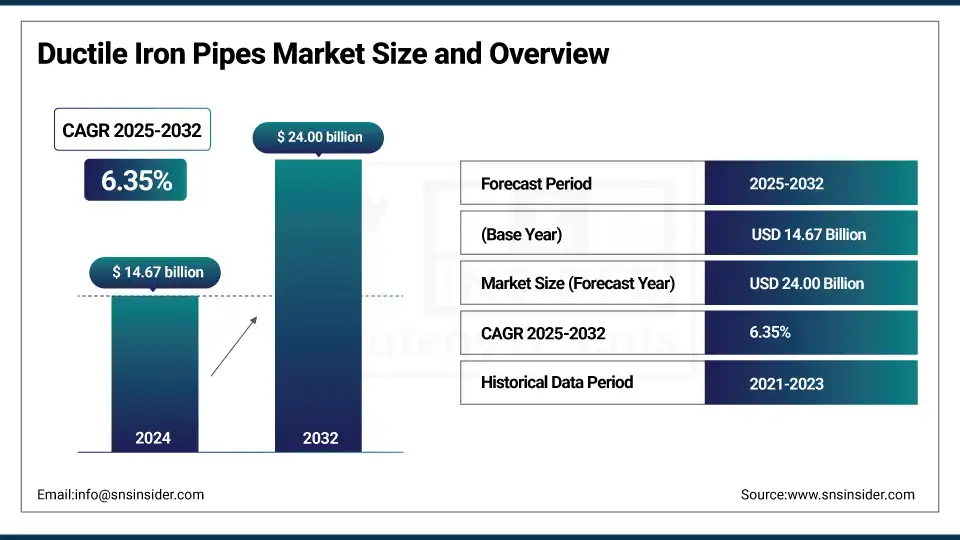

The Ductile Iron Pipes Market size was valued at USD 14.67 billion in 2024 and is expected to reach USD 24.00 billion by 2032, growing at a CAGR of 6.35% over the forecast period of 2025-2032.

The global ductile iron pipes market is witnessing steady growth, driven by increasing demand for durable and reliable piping systems in water distribution, wastewater management, and industrial applications. Ductile iron pipes are famous for high tensile strength, corrosion resistance and long service life, which makes them the most popular pipes used in municipal infrastructure projects and utility services. Ductile iron pipes industry uses them owing to their high pressure and environmental corrosive resistance, which makes them a better alternative than traditional cast iron as well as short or long-term PVC pipes.

To Get more information On Ductile Iron Pipes Market - Request Free Sample Report

Key trends shaping the market include technological advancements in protective linings and coatings, which enhance pipe longevity and performance. In addition, growing investments in urban infrastructure renewal and smart water management systems are driving the growth of the product. With growing environmental and quality standards, manufacturers are innovating products with sustainable production practices. As per the analysis, an increase in the utilization of water supply systems and a rise in infrastructure development activities for industrial fluids through pipelines are expected to foster growth in the market, required for an efficient water supply system in the industry, industry insight points out. Moreover, the incorporation of trenchless technology and digital monitoring systems into ductile iron pipelines is increasing operational efficiency as well.

In June 2025, A dispute over pipe size has delayed Kochi’s Kaloor overhead tank water supply project. The Kerala Water Authority debated between using 1,000 mm and 1,200 mm ductile iron pipes to future-proof the system. Eventually, they reverted to 1,000 mm due to feasibility issues, causing further delays as new approvals were required. The project aims to improve supply to the tail-end areas in Kochi.

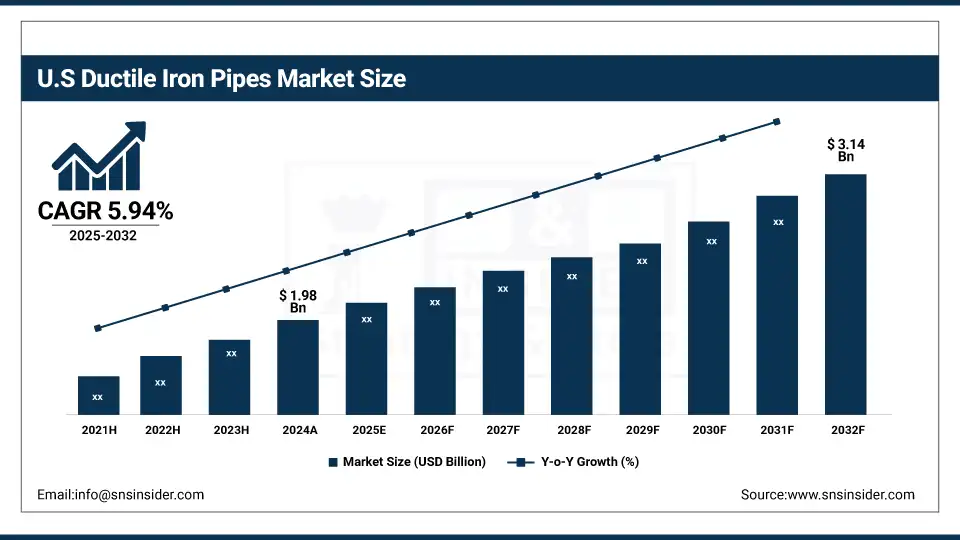

The U.S. ductile iron pipes market was valued at USD 1.98 billion in 2024 and is projected to reach USD 3.14 billion by 2032, growing at a CAGR of 5.94%. Growth is fueled by infrastructure upgrades, urban expansion, and replacement of aging water pipelines. Government funding and demand for durable, corrosion-resistant materials support sustained market expansion.

Ductile Iron Pipes Market Dynamics:

Drivers

-

Superior Mechanical Strength and Eco-Friendly Attributes Propel Sustainable Growth in The Ductile Iron Pipes Market

Superior mechanical and environmental benefits are significantly driving the ductile iron pipes market growth. These pipes are characterized by their tensile strength and high impact resistance, along with a lifespan of over 100 years, making them suitable for heavy infrastructure. The advantages of metal, such as having inherent recyclability and advanced corrosion protection coatings, also improve durability while minimizing environmental impact. These features make ductile iron pipes a better sustainable option than PVC and HDPE in the water and wastewater systems, as per the changing global ductile iron pipes market trends. Moreover, rising regulatory pressure for green construction materials, particularly in Europe and North America, is further driving their adoption. The increased preference of governments and utilities toward materials consistent with long-term sustainability objectives is bolstering demand for ductile iron pipes. This adherence to increasingly more exacting performance and sustainability demands drives marketplace decisions, and is sustained growth within developed and developing countries.

Restraint

-

High Performance Drives Growth in Ductile Iron Pipes Market, But High Costs and Logistics Remain Key Barriers

In the Ductile Iron Pipes Market, one of the key growth factors is their superior mechanical and environmental benefits. These pipes are strong, impact-resistant, and can last over 100 years, making them perfect for municipal water and wastewater systems. Their corrosion resistance and recyclability promote the development of sustainable infrastructure, in accordance with the leading trends in the Ductile Iron Pipes Market, supporting sustainability in infrastructure, namely durability and eco-friendliness. But, high costs and logistical challenges are stunting that growth. Ductile iron has higher manufacturing, transportation, and installation costs due to its greater weight, making PVC or HDPE a more attractive alternative in remote or price-sensitive market segments. Also, installation often needs an extra set of instruments along with skilled workers, which adds to the initial cost. Such factors can create hurdles for adoption, with developing geographies being under tighter budget pressures. However, infrastructure investments are a continuous effort that helps to compensate for the overall Ductile Iron pipes market growth.

Ductile Iron Pipes Market Segmentation Analysis:

By Joint Type

Socket and spigot segments dominated the market and accounted for 52% of the ductile iron pipes market share. These joints are highly favored due to their ease of installation, flexibility, and excellent sealing capabilities. They are designed to allow a slight angular deflection that makes them perfect for underground applications since the ground may shift from time to time. Globally, they are used in water supply and sewage pipelines in municipal and utility applications. The fact that they are leak-proof and can handle internal pressure even without bolts or welding continues to make them the material of choice. Socket and spigot joints are the conventional option for buried infrastructure systems that need to last for decades. They can be cost-effective and efficient for new projects and can also be used for pipeline rehabilitation.

Flanged joints are the fastest-growing segment in the ductile iron pipes market due to increasing demand in above-ground and industrial applications. These joints form stiff and robust connected elements and allow for easy disassembly and reassembly, as needed in systems that often get inspected or modified. This has led to increased adoption in sites such as water treatment plants, pumping stations, and other industrial applications where flexibility and maintenance access are valued. In case of valves, meters, and specialty fittings, where accuracy and rigidity are important, it is also ideal to use flanged joints. The increasing complexity of infrastructure and an industry shift toward systems that reduce maintenance requirements are driving the adoption of flanged joints, particularly in the public and private environments where durability, flexibility, and a long service life are crucial performance factors.

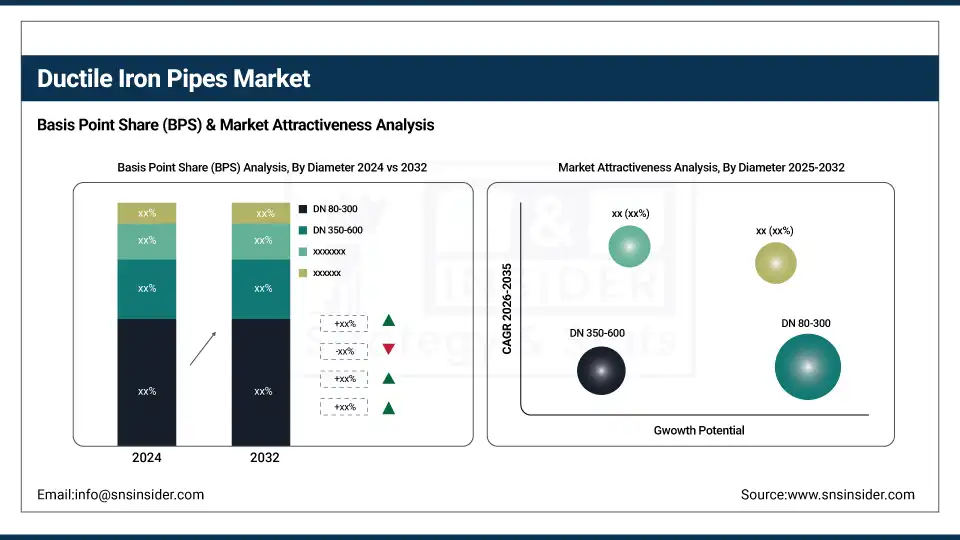

By Diameter

The DN 80–300 diameter range dominated with a market share of over 42% in 2024, primarily due to its widespread application in urban water distribution and municipal supply systems. They provide the best combination of hydraulic efficiency and lightweight for low-cost, flexible construction, making them suitable for easier handling in new projects and rehabilitation tasks. This medium size offers flexibility in layout but is big enough to provide adequate flow capacity for residential and commercial use. Furthermore, they are more manageable, transportable, and simple to install, thereby driving down total venture costs. Due to their high applicability in city infrastructure projects as well as utility networks, volumes are expected to be consistent in these diameter ranges, making this diameter segment the most favored option in standard pipelines in markets all over the world.

The DN 2000 & above categories are the fastest-growing segments in the ductile iron pipes market, driven by large-scale infrastructure investments. These Large-Diameter Pipes as commonly used for high-capacity applications such as intercity water transmission, desalination plant pipelines, and large-scale sewage and drainage systems. With drinking water scarcity seriously threatening hundreds of millions of people each year in most regions of the world, governments and sectors of private water management are becoming ever more receptive to the idea of long-distance water transfer projects and the industrial water supply solution. Large-diameter ductile iron pipes have strength and durability and are thus suitable for transporting massive volumes of water or wastewater with limited loss and a long service life.

By Application

Water distribution remained the dominant application in the Ductile Iron Pipes Market in 2024. This type of pipe is often used in municipal water supply systems because of its high strength, corrosion resistance, and long service life. Best in the urban and suburban infrastructure that can sustain high-pressure flow and resist the stress of the environment. Replacing old pipeline networks in developed nations and new installations due to rapid urbanization in emerging economies further cements the dominance of this segment. These pipes are used primarily by local governments and utilities for transporting substantial amounts of water over long distances, thereby providing steady demand for ductile iron pipes from the core application segment.

The desalination and marine outfalls segment is the fastest-growing application area for ductile iron pipes. In the case of desalination infrastructure, these pipes are crucial because they resist corrosion from saline environments and can withstand high-flow pressures, and investment in such infrastructure grows as more arid or coastal regions experience increasing water scarcity. In addition, systems for marine discharge are spreading over the world, and they need a durable, long-lasting piping solution for treated effluents, too. The abrasive conditions are also why ductile iron is the ideal material for integrity and durability.

By External Protection Coating

Zinc-coated ductile iron pipes hold a dominant position in the market due to their cost-effectiveness and dependable corrosion resistance. The zinc layer is sacrificial and protects the iron below it from corrosion across even the most varied and severe soil conditions. These are extensively used in underground water and sewage networks, particularly in Europe & North America, where durability over a longer term & regulatory compliance are a priority. With their ease of application, long track record of performance, and compatibility with other protective layers like bitumen, galvanized zinc coatings are a popular choice for municipalities.

Polyurethane-coated ductile iron pipes are emerging as the fastest-growing segment due to their advanced protective capabilities. Due to their excellent chemical, abrasion, and corrosion resistance, these coatings are great for harsh environments, including coastal, industrial, and aggressive soil regions. Seamless finish provides lower permeability and higher durability than similar coatings (traditional coatings) in full-term performance. The growing demand for high durability and low maintenance from global infrastructure projects, along with the need for low-maintenance coatings in high-risk applications, especially in marine outfalls and desalination plants, is fueling the adoption of polyurethane coatings.

Ductile Iron Pipes Market Regional Outlook:

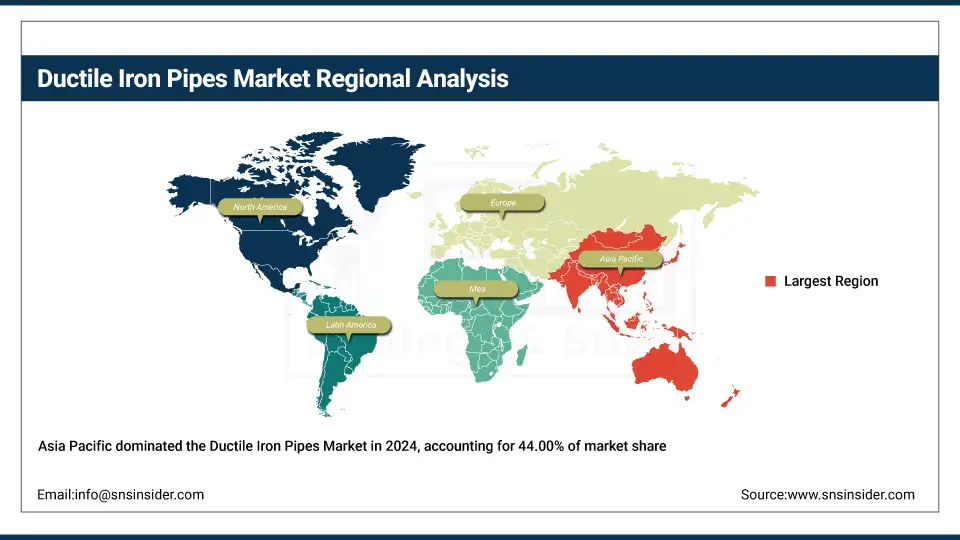

Asia-Pacific dominated the ductile iron pipes market, holding a substantial 44.00% share in 2024. It is a leadership fueled by the tremendous urbanization, massive infrastructure networks, and megastructures in water supply and sewage that are being constructed in China and India. With rising investments in smart city projects, water management systems, and industrial development, governments are focusing on durable and high-capacity piping solutions such as ductile iron pipes. In addition, the increase in population and the need for better sanitation and access to water in the region will continue to drive the demand. This regional dominance is backed up with local production capabilities and supporting regulatory environments, with some domestic manufacturers serving regional and international markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

China dominates the ductile iron pipes market in the Asia-Pacific region, driven by massive infrastructure development and rapid urbanization. The demand continues from large investments in water supply, sewage systems, and industrial pipelines. While China, with robust domestic manufacturing capacities and government-backed projects, continues to be the leading force for regional market expansion.

Europe is the fastest-growing region in the Ductile Iron Pipes Market, propelled by stringent environmental regulations, aging pipeline infrastructure, and a strong push for sustainable water management solutions. In countries like Germany, France, the UK, and other countries, the outdated systems have been replaced by modern ductile iron piping based on its corrosion resistance, long service life, and environmental sustainability. Growing demand for longer-lasting materials is driven by EU policies aimed at accelerating circular economy practices and sustainable urban development. In addition, development in technology and rising use of trenchless pipe-laying techniques cut down future installation time and, consequently, expenses, which continue to drive the attraction of ductile iron pipes.

North America holds a significant share in the ductile iron pipes market due to a well-established infrastructure, growing investments employed in water and wastewater projects, and rising focus on the replacement of aging pipeline networks. Particularly, the United States is zeroing in on upgrading water delivery systems through programs like the Bipartisan Infrastructure Law, which earmarks billions for clean water and more modern pipes. Offering a combination of strength, durability, and pressure-carrying capacity, ductile iron pipes have become a common choice for municipal and industrial applications in water infrastructure. Moreover, increasing focus on water pollution and leakage is pushing utilities to switch to reliable piping systems.

Key Players in the Ductile Iron Pipes Market are:

Ductile iron pipes companies are Aliaxis SA, American Cast Iron Pipe Company (ACIPCO), CNBM INTERNATIONAL CORPORATION, Electrotherm (India) Ltd., Jindal SAW Limited, KUBOTA Corporation, Saint-Gobain PAM Canalisation, Supra Group, Tata Metaliks Limited, U.S. Pipe, McWane, Inc., Xinxing Ductile Iron Pipes Co., Ltd., Angang Group Yongtong Ductile Cast Iron, Benxi Beitai Ductile Iron Pipes Co., Ltd., Electrosteel Castings Ltd., United Gulf Pipe Manufacturing Co. LLC, Kalahasthi Pipes Limited, Rajwadi Pipes, Atlantic States Cast Iron Pipe Company

Recent Development:

-

In January 2025, American Cast Iron Pipe Company announced a $285 million investment to install electric-powered induction furnaces, replacing its traditional coke-fueled system. The upgrade aims to increase ductile iron pipe production capacity by 25% and cut CO₂ emissions by up to 95%.

-

In June 2025, Jindal SAW Ltd. announced a USD 118 million investment to expand its pipe manufacturing operations in the Middle East. The plan includes a seamless pipe plant in Abu Dhabi and two joint ventures in Saudi Arabia—one for HSAW pipes and another for ductile iron pipes. The expansion will be executed through its subsidiary, Jindal Saw Holdings FZE. Following the announcement, the company’s shares surged nearly 11%.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 14.67 Billion |

| Market Size by 2032 | USD 24.00 Billion |

| CAGR | CAGR of 6.35% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Joint Type (Socket and spigot, Flanged, Others) • By Diameter (DN 80-300, DN 350-600, DN 700-1000, DN 1200-2000, DN2000 & above) • By Application (Water Distribution, Sewage & Wastewater Systems, Irrigation Systems, Fire Protection Networks, Industrial Utilities, Desalination & Marine Outfalls, Hydropower & Dams) • By External Protection Coating (Zinc Coated, Bitumen Coated, Polyethylene Sleeve, Polyurethane Coated, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Aliaxis SA, American Cast Iron Pipe Company (ACIPCO), CNBM INTERNATIONAL CORPORATION, Electrotherm (India) Ltd., Jindal SAW Limited, KUBOTA Corporation, Saint-Gobain PAM Canalisation, Supra Group, Tata Metaliks Limited, U.S. Pipe, McWane, Inc., Xinxing Ductile Iron Pipes Co., Ltd., Angang Group Yongtong Ductile Cast Iron, Benxi Beitai Ductile Iron Pipes Co., Ltd., Electrosteel Castings Ltd., United Gulf Pipe Manufacturing Co. LLC, Kalahasthi Pipes Limited, Rajwadi Pipes, Atlantic States Cast Iron Pipe Company, AMERICAN SpiralWeld Pipe Company, LLC. |

Frequently Asked Questions

The Asia-Pacific region dominated the Ductile Iron Pipes Market in 2024.

The “Socket and spigot” segment dominated the Ductile Iron Pipes Market.

Superior Mechanical Strength and Eco-Friendly Attributes Propel Sustainable Growth in The Ductile Iron Pipes Market

The Ductile Iron Pipes Market was USD 14.67 billion in 2024 and is expected to reach USD 24.00 billion by 2032.

The Ductile Iron Pipes Market is expected to grow at a CAGR of 6.35% from 2025-2032.

Get in Touch