Durable Medical Equipment Market Report Scope & Overview:

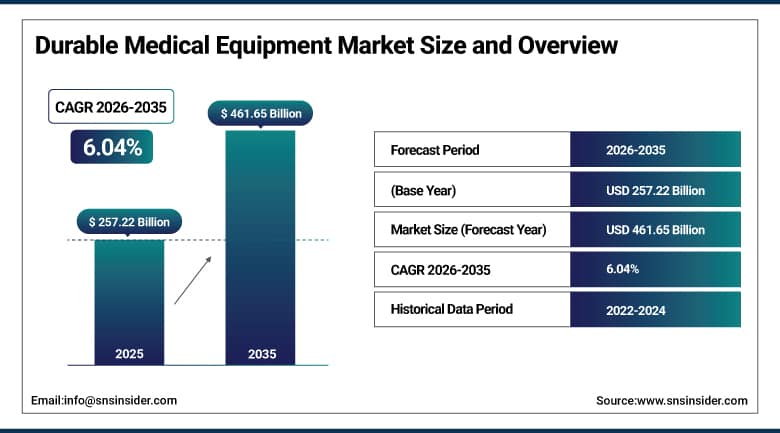

The Durable Medical Equipment (DME) Market was valued at USD 257.22 Billion in 2025 and is expected to reach USD 461.65 Billion by 2035, growing at a CAGR of 6.04% from 2026 to 2035.

Durable Medical Equipment refers to a large class of medically necessary equipment and aids which are meant to be used for prolonged periods of time for the purpose of aiding patients in dealing with their chronic medical conditions, recovery from surgical procedures, as well as the ability to perform their daily tasks independently with minimal dependence on institutional care settings. What sets the DME apart from one-time disposable medical equipment is the durability that DME possesses due to which it can be used repeatedly without losing its functionality. This makes it possible for DMEs to be used economically in various settings including the institution and home based care settings.

In early 2024, Medtronic announced a strategic partnership with BioIntelliSense to integrate remote patient monitoring peripheral devices with its chronic care management platform. The integration enables continuous physiological monitoring of DME-dependent patients including those using respiratory therapy, infusion therapy, and mobility assistance devices, automatically transmitting vital sign data to clinical teams who can intervene before acute deterioration requires expensive hospitalization. The partnership demonstrated the growing commercial importance of connected DME ecosystems whose IoT-enabled remote monitoring capability creates value for healthcare providers through reduced readmission costs, for payers through avoided acute care expenditure, and for patients through earlier clinical intervention that preserves quality of life.

Market Size and Forecast

-

Market Size in 2026E: USD 272.75 Billion

-

Market Size by 2035: USD 461.65 Billion

-

CAGR: 6.04% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Durable Medical Equipment Market - Request Free Sample Report

Durable Medical Equipment Market Trends

-

IoT-enabled durable medical equipment is enhancing remote patient monitoring and chronic disease management through real-time connectivity and data-driven care.

-

Home healthcare adoption is driving demand for portable, easy-to-use durable medical equipment that supports patient care outside traditional clinical settings.

-

Bariatric durable medical equipment is witnessing rapid growth due to increasing obesity rates and the need for high-capacity healthcare solutions.

-

Lightweight materials and advanced composites are improving the mobility, durability, and usability of wheelchairs, hospital beds, and other medical equipment.

-

Evolving reimbursement policies and value-based healthcare models are encouraging the adoption of cost-effective, outcome-oriented durable medical equipment solutions.

The U.S. Durable Medical Equipment Market Outlook

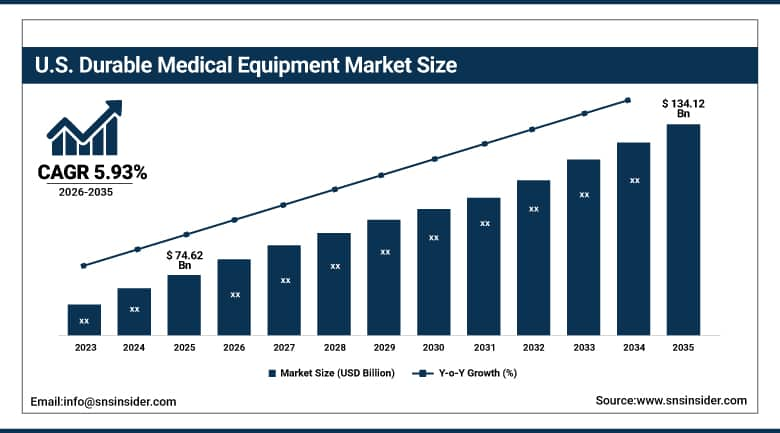

The U.S. Durable Medical Equipment Market was valued at approximately USD 74.62 Billion in 2025 and is expected to reach approximately USD 134.12 Billion by 2035, growing at a CAGR of approximately 5.93%.

The United States DME market is anchored by the Medicare and Medicaid reimbursement infrastructure whose coverage of prescribed DME products across mobility aids, respiratory devices, and monitoring equipment creates a clinical procurement pathway that makes DME economically accessible to the large elderly and disabled patient population whose out-of-pocket payment capacity is limited. The U.S. Centers for Medicare & Medicaid Services projects national healthcare spending growth at an average of 5.1% annually through 2032, sustaining the DME reimbursement funding base whose accessibility directly drives adoption rates. The growing preference for home healthcare delivery, whose cost per episode of care is substantially lower than equivalent skilled nursing facility or hospitalization costs, creates strong incentive for DME investment in home settings across both commercially insured and Medicare/Medicaid beneficiary populations.

In 2023, Invacare Corporation introduced the TDX SP2 power wheelchair incorporating advanced positioning technology and enhanced manoeuvrability for users with complex seating and positioning requirements including ALS, spinal cord injury, and multiple sclerosis whose severe mobility limitations require sophisticated power wheelchair capability beyond standard products. The TDX SP2's cloud-connected performance monitoring and remote programming capability demonstrated the growing commercial importance of connected DME technology whose data-driven maintenance scheduling, remote clinical adjustment, and usage pattern analytics provide value-added services that strengthen provider-patient relationships and support premium pricing above commodity DME alternatives.

Durable Medical Equipment Market Segment Analysis

-

By Product Type, monitoring & therapeutic devices dominated the durable medical equipment market with approximately 38% of the revenue share in 2025, while respiratory equipment segment is projected to register the fastest CAGR of approximately 7.9% during 2026–2035.

-

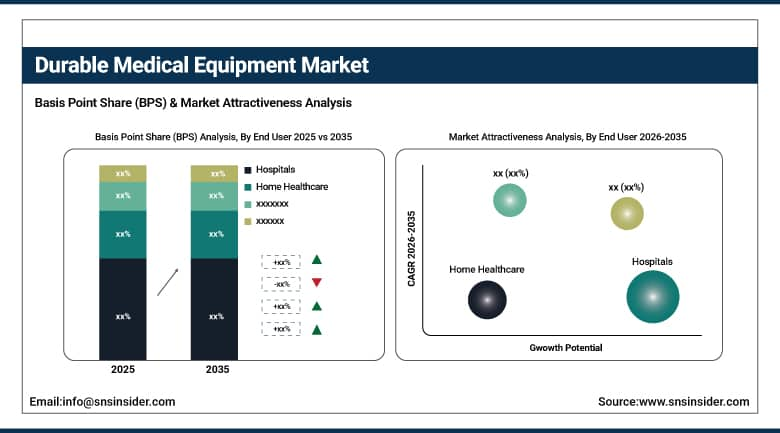

By End User, hospitals dominated the durable medical equipment market in 2025, while home healthcare is the fastest growing end user segment during 2026 to 2035.

By End User, hospitals dominate, home healthcare grows fastest

Hospitals generated the dominant end user revenue share in 2025 through their procurement of the full spectrum of DME product categories for inpatient, ICU, rehabilitation, and outpatient clinical use whose combined institutional volume creates the largest single-channel DME procurement market. Hospital investments in bariatric-appropriate DME, ICU monitoring systems, infusion therapy infrastructure, and post-surgical rehabilitation equipment span the highest-value DME categories whose clinical specification and institutional procurement processes create durable supplier relationships whose switching costs support stable market positions for established DME providers. The growing number of hospital facilities, particularly in rapidly developing Asian and Middle Eastern healthcare markets, creates greenfield DME procurement opportunities whose aggregate volume across newly commissioned healthcare facilities represents substantial incremental DME market demand.

Home healthcare is the fastest growing end user segment as the convergence of cost containment pressure on institutional care, patient preference for home-based treatment, caregiver support technology improvement, and telehealth-enabled remote clinical supervision creates a powerful commercial incentive to shift DME-supported care from institutional to home settings. Each patient transitioned from skilled nursing facility to home care with DME support generates institutional cost savings of USD 5,000 to USD 15,000 per month that create payer incentives for DME investment in home settings, while simultaneously creating a home care DME market that prioritizes portability, user-friendliness, and connectivity features that institutional DME designs need not address.

By Product Type, monitoring & therapeutic devices dominate, respiratory equipment grows fastest

Monitoring and therapeutic devices generated the dominant product type revenue share in 2025, encompassing the commercially diverse category of blood glucose monitors, CPAP and BiPAP respiratory therapy devices, infusion pumps, electrotherapy devices, and patient monitoring systems whose combined revenue exceeds that of mobility aids and medical furniture through the value intensity of complex therapeutic devices whose per-unit pricing reflects their clinical sophistication, regulatory approval investment, and clinical efficacy documentation. Blood glucose monitoring systems alone represent a multi-billion-dollar global market within DME whose consumable test strip requirement per patient creates a recurring revenue model that sustains aftermarket revenue streams substantially in excess of the initial device sales value.

Respiratory equipment is among the fastest growing product categories, driven by the global burden of COPD affecting over 380 million individuals, the post-COVID respiratory complication prevalence creating new long-term oxygen therapy and pulmonary rehabilitation device demand, and the sleep apnea epidemic whose estimated 1 billion affected individuals globally create enormous untapped CPAP and oral appliance therapy demand whose diagnosis rate in developing markets remains well below its true clinical prevalence. Portable oxygen concentrator technology advances enabling lighter, quieter, and longer-lasting devices are expanding respiratory DME adoption into ambulatory patients whose activity level requirements previously precluded conventional oxygen delivery system use.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.47% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

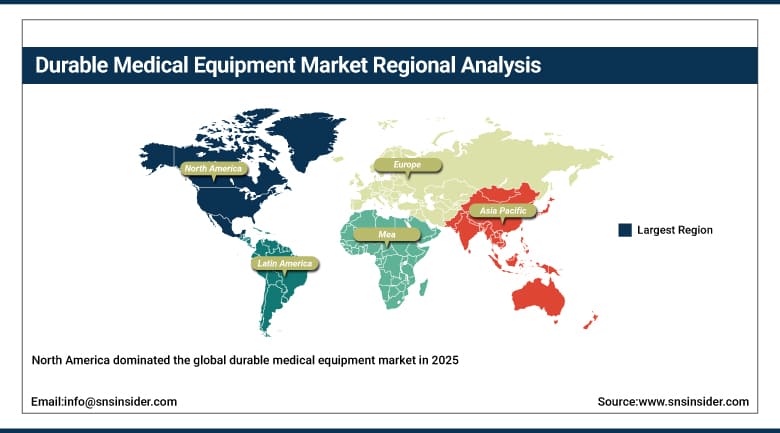

North America Durable Medical Equipment Market Insights

North America dominated the global durable medical equipment market in 2025, accounting for approximately 35% of total global revenue. The United States accounts for approximately 82.47% of regional revenue through its extensive Medicare and Medicaid reimbursement infrastructure, high chronic disease prevalence, large elderly population, and the commercial concentration of major DME manufacturers and distributors whose domestic market development sustains regional leadership. Canada contributes supplementary demand through its provincial public health insurance coverage of medically necessary DME, growing home care investment, and aging demographics whose trajectory mirrors the U.S. market's structural growth drivers with a lag of approximately five to seven years.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Durable Medical Equipment Market Insights

Europe held a significant share of global durable medical equipment revenues in 2025. Germany, France, the United Kingdom, and the Netherlands are the leading national markets whose universal healthcare systems, comprehensive DME reimbursement coverage, and large aging populations sustain consistent commercial demand. Germany accounts for approximately 28.47% of European revenues through its statutory health insurance system's DME coverage, large elderly patient population, and advanced healthcare infrastructure that supports early adoption of connected and technologically sophisticated DME products. European DME market growth is supported by the EU's active aging policy framework and the Member States' progressive investment in community-based care infrastructure that substitutes for institutional long-term care.

Asia Pacific Durable Medical Equipment Market Insights

Asia Pacific is the fastest-growing regional durable medical equipment market, with growth driven by ageing demographics across Japan, China, South Korea, and Australia, rapidly expanding healthcare infrastructure investment across India and Southeast Asian developing markets, and government initiatives promoting home healthcare adoption as a cost-effective alternative to institutional elderly care. China accounts for approximately 38.47% of Asia Pacific revenues through its large elderly population, expanding hospital network, and domestic DME manufacturing industry whose scale and cost competitiveness create a dual commercial opportunity in both domestic market supply and global export. India's growing healthcare infrastructure investment, expanding middle-class health insurance coverage, and government home care promotion initiatives create an accelerating DME adoption trajectory from a relatively low base.

MEA & Latin America Durable Medical Equipment Market Insights

Middle East and Latin America are growing durable medical equipment markets where improving healthcare access, expanding hospital infrastructure, and rising chronic disease burden are creating growing DME procurement demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its world-class hospital network, comprehensive national health insurance coverage that includes DME reimbursement, and growing elderly care infrastructure investment. Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large public hospital network under the SUS system, growing private health insurance sector, and expanding home healthcare services whose DME procurement requirements are increasing with care model evolution.

Market Dynamics

Growth Driver: Global demographic ageing creating compounding chronic disease burden and the shift to home-based care models are the primary structural growth drivers of the durable medical equipment market.

The durable medical equipment market's growth is driven by the convergence of demographic ageing creating a structurally growing patient population and healthcare system economics incentivizing substitution of expensive institutional care with DME-supported home care. The global population aged 65 and over is projected to grow from approximately 760 million in 2023 to 1.6 billion by 2050, each year adding tens of millions of new individuals to the age cohort whose chronic disease prevalence, mobility limitation rates, and care dependency create direct DME demand. Healthcare systems facing unsustainable institutional care costs are simultaneously creating financial incentives through reimbursement structures that reward home healthcare DME investment whose per-episode cost is a fraction of equivalent institutional care.

Restraint: Reimbursement policy complexity, competitive bidding programme pricing pressure, and counterfeit product concerns create market challenges that constrain revenue growth in certain DME categories.

DME reimbursement policy complexity across different national healthcare systems creates market access and pricing challenges for manufacturers whose product commercialization requires separate regulatory approval, reimbursement code assignment, and coverage documentation in each national market. The U.S. Medicare competitive bidding programme for durable medical equipment, which has reduced reimbursement rates for commodity DME categories including standard wheelchairs, walkers, and CPAP devices by 40 to 70% since its implementation, has compressed supplier margins in affected categories and driven consolidation among DME providers whose economies of scale are required to sustain commercially viable operations at lower reimbursement levels. Counterfeit and substandard DME products, particularly in developing market channels, create patient safety risks and competitive pricing distortion that legitimate manufacturers cannot match without compromising product quality.

Opportunity: Connected DME ecosystems integrating IoT monitoring, AI-driven clinical decision support, and telehealth infrastructure represent transformative growth opportunities

The integration of IoT connectivity, real-time physiological monitoring, and AI-powered predictive analytics into DME platforms is creating a connected care ecosystem whose commercial value extends far beyond the underlying device market into recurring data services, remote monitoring programmes, and chronic disease management platforms whose subscription revenue models generate durable aftermarket revenue streams. Each connected DME device whose physiological monitoring data feeds into an AI clinical decision support algorithm creates actionable health insights that prevent costly acute events, improve medication adherence, and enable earlier clinical intervention whose documented health economic value justifies both premium device pricing and sustained service subscription revenue.

Recent Developments:

-

2024: Medtronic partnered with BioIntelliSense to integrate continuous remote patient monitoring devices with its chronic care platform, enabling automated physiological data transmission for DME-dependent patients that allows earlier clinical intervention and reduces hospitalization rates for high-risk chronic disease populations.

-

2023: Invacare Corporation launched the TDX SP2 power wheelchair with advanced positioning technology, cloud-connected performance monitoring, and remote programming capability, demonstrating the growing commercial value of connected DME platforms for users with complex mobility requirements.

-

2023: Sunrise Medical completed the acquisition of Ride Designs, a customized wheelchair seating specialist, expanding its personalized seating solution portfolio and strengthening its clinical expertise in complex rehabilitation seating for wheelchair users with specialized positioning requirements.

Durable Medical Equipment Market Key Players are:

-

Medtronic PLC

-

Stryker Corporation

-

Invacare Corporation

-

Koninklijke Philips NV

-

ResMed Inc.

-

Hill-Rom Holdings Inc. (Baxter)

-

Drive DeVilbiss Healthcare

-

GF Health Products Inc.

-

Sunrise Medical LLC

-

Ottobock SE & Co. KGaA

-

Getinge AB

-

Compass Health Brands

-

Permobil AB

-

Joerns Healthcare LLC

-

ArjoHuntleigh AB

-

Medline Industries LP

-

Cardinal Health Inc.

-

B. Braun Melsungen AG

-

Omron Corporation

-

Natus Medical Inc.

Durable Medical Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 257.22 Billion |

| Market Size by 2035 | USD 461.65 Billion |

| CAGR | CAGR of 6.04% from 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Personal Mobility Devices, Monitoring and Therapeutic Devices, Bathroom Safety Devices and Medical Furniture) • By End Use (Hospitals, Nursing Homes, Home Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Medtronic PLC, Stryker Corporation, Invacare Corporation, Koninklijke Philips NV, ResMed Inc., Hill-Rom Holdings Inc. (Baxter), Drive DeVilbiss Healthcare, GF Health Products Inc., Sunrise Medical LLC, Ottobock SE & Co. KGaA, Getinge AB, Compass Health Brands, Permobil AB, Joerns Healthcare LLC, ArjoHuntleigh AB, Medline Industries LP, Cardinal Health Inc., B. Braun Melsungen AG, Omron Corporation, Natus Medical Inc. |

Frequently Asked Questions

The monitoring and therapeutic devices segment dominated the Durable Medical Equipment Market in 2025.

North America dominated the Durable Medical Equipment Market in 2025, holding approximately 35% of global revenues.

The Durable Medical Equipment Market was valued at USD 257.22 Billion in 2025.

Global demographic ageing creating an expanding chronic disease patient population requiring long-term DME support, healthcare system cost containment incentivizing home healthcare DME adoption over institutional care.

The Durable Medical Equipment Market is expected to grow at a CAGR of 6.04% from 2026 to 2035.

Get in Touch