Empty Capsules Market Report Scope & Overview:

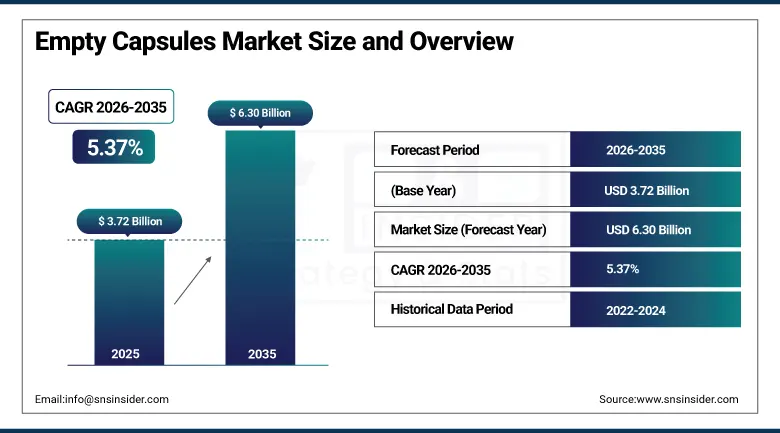

The Empty Capsules Market was valued at USD 3.72 Billion in 2025 and is expected to reach USD 6.30 Billion by 2035, growing at a CAGR of 5.37% from 2026–2035.

The global empty capsules market has been seeing constant growth due to the increased need for pharmaceutical and nutraceutical dosages that provide high bioavailability and patient compliance and also allow versatile formulations. Empty capsules are basic pharmaceutical packaging materials utilized to encapsulate powdered, granulated, liquid, or semi-liquid pharmaceutical substances in unit doses for oral consumption. The growth of the market is influenced by increased demand for pharmaceutical dosages with improved bioavailability, the increasing use of natural and clean label supplements in both nutraceutical and pharmaceutical industries, and the increased preference for vegetarian HPMC substitutes over gelatin capsules.

In September 2023, Lonza reported a significant increase in demand for its Capsugel hard gelatin capsules, driven by their use in novel drug formulations and clinical trials. These capsules are favored for their consistent performance and compatibility with a wide range of active pharmaceutical ingredients, reflecting the growing pharmaceutical industry's preference for capsule-based drug delivery systems that offer formulation flexibility, improved API stability, and enhanced patient acceptability for oral solid dosage forms across a growing therapeutic category breadth.

Market Size and Forecast

-

Market Size in 2026E: USD 3.92 Billion

-

Market Size by 2035: USD 6.30 Billion

-

CAGR: 5.37% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

Empty Capsules Market Trends

-

Growing consumer preference for vegan, vegetarian, halal, kosher, and allergen-free products is accelerating adoption of HPMC-based vegetarian capsules across pharmaceutical and nutraceutical applications

-

Increasing development of enteric-coated capsules is supporting targeted drug delivery and enhanced protection of acid-sensitive formulations, probiotics, and gastrointestinal therapies

-

Rising use of liquid-filled hard capsules is enabling improved delivery and bioavailability of poorly water-soluble active pharmaceutical ingredients (APIs)

-

Expansion of personalized medicine and compounding pharmacy services is driving demand for customized empty capsules in a variety of sizes and specialty formulations

-

Adoption of pullulan capsules is increasing due to their low moisture content, superior oxygen barrier properties, and suitability for sensitive pharmaceutical and nutraceutical ingredients

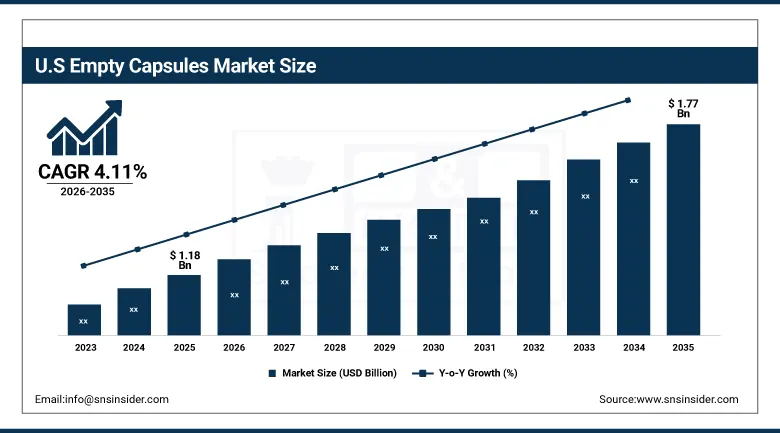

U.S. Empty Capsules Market Outlook

The U.S. Empty Capsules Market was valued at approximately USD 1.18 Billion in 2025 and is expected to reach approximately USD 1.77 Billion by 2035, growing at a CAGR of approximately 4.11%.

U.S. is an economically viable country for empty capsules due to its second largest revenue generation position from North America region due to strong activities in pharmaceutical R&D, FDA regulations for formulation of capsules and growing demand for personal medicines and nutraceutical supplements. Some of the key players in the supply chain of empty capsules in the U.S. are Lonza’s Capsugel division, ACG Worldwide, Qualicaps and US operations of Suheung Co. Progressive approval of HPMC capsules by FDA for regulated drug products, increasing API bioavailability needs by the pharmaceutical industry and unprecedented growth of nutraceutical market provide steady above average buying of empty capsules.

In January 2023, Capsugel (Lonza Group) introduced its Vcaps Plus capsules with immediate-release properties, tailored for high-speed filling processes and ensuring quick dissolution and bioavailability. The product launch addresses pharmaceutical manufacturers’ need for HPMC vegetarian capsules capable of operating at commercial-scale filling equipment speeds equivalent to gelatin capsule alternatives, removing the production efficiency barrier that previously limited HPMC specification in high-volume pharmaceutical manufacturing operations.

Empty Capsules Market Segment Analysis

-

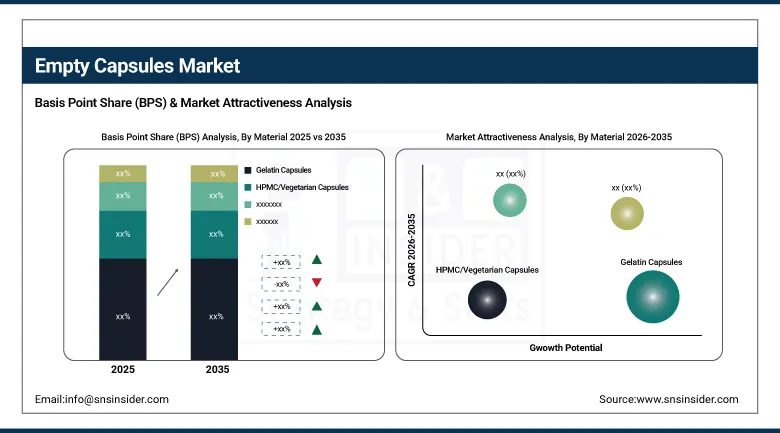

By Material, the Gelatin Capsules segment dominated the Empty Capsules Market with approximately 68% share in 2025, while the HPMC/Vegetarian Capsules segment is the fastest growing.

-

By Functionality, the Immediate Release segment dominated the Empty Capsules Market with approximately 48% share in 2025, while the Sustained Release segment is the fastest growing.

-

By Application, the Antibiotic & Antibacterial Drugs segment dominated the Empty Capsules Market with approximately 22% share in 2025, while the Nutraceuticals segment is the fastest growing.

-

By End User, the Pharmaceutical Industry segment dominated the Empty Capsules Market with approximately 58% share in 2025, while the Nutraceutical Industry segment is the fastest growing.

By Material, gelatin dominates, HPMC grows fastest

Gelatin capsules retained the dominant material position with approximately 68% of the empty capsules market in 2025. Their commercial primacy reflects decades of established pharmaceutical use whose regulatory approval track record, formulation compatibility database, and capsule filling equipment optimization create an infrastructure advantage that alternative materials must overcome to gain specification. Gelatin's natural protein structure creates a capsule shell that dissolves rapidly in gastric fluid, providing reliable immediate-release drug delivery without modified-release technology. Gelatin's compatibility with high-speed automated capsule filling at commercial production rates of up to 200,000 capsules per hour sustains pharmaceutical manufacturer preference whose capital equipment investment in gelatin-optimized filling lines creates switching cost barriers for material specification changes.

HPMC vegetarian capsules are the fastest-growing material because the convergence of dietary restriction awareness, religious dietary law compliance, and consumer preference for plant-derived ingredients across both pharmaceutical and nutraceutical markets is creating systematic specification migration from gelatin toward plant-based alternatives. Each nutraceutical brand that reformulates from gelatin to HPMC capsules to satisfy vegan certification or halal compliance creates HPMC procurement whose commercial growth compounds with the global nutraceutical market's extraordinary expansion. The pharmaceutical industry's progressive HPMC adoption is enabled by Lonza's Vcaps Plus and ACG's HPMC capsule production infrastructure whose manufacturing scale creates commercial pricing competitive with gelatin alternatives.

By Functionality, immediate release dominates, sustained release grows fastest

Immediate release capsules retained the dominant functionality position with approximately 48% of the empty capsules market in 2025. The immediate-release capsule's commercial dominance reflects the majority of pharmaceutical and nutraceutical formulations whose drug delivery requirement is standard rapid dissolution in gastric fluid without modified-release mechanism complexity. Each antibiotic prescription, vitamin supplement, and pain relief formulation whose therapeutic objective is rapid drug absorption after oral administration creates immediate-release capsule procurement whose aggregate across the global pharmaceutical and nutraceutical production base creates the market's largest single functionality category. The formulation simplicity, manufacturing cost advantage, and regulatory pathway clarity of immediate-release relative to modified-release alternatives sustain the category's market leadership across price-sensitive generic pharmaceutical and nutraceutical applications.

Sustained release capsules are the fastest-growing functionality because chronic disease management's patient compliance improvement through once-daily or twice-daily dosing versus multiple-daily conventional immediate-release alternatives creates pharmaceutical developer preference for controlled-release formulation investment. Each cardiovascular drug, antidiabetic medication, and neurological treatment that adopts sustained-release capsule formulation creates above-average-cost capsule procurement whose engineering complexity and regulatory documentation requirement sustain premium pricing relative to immediate-release alternatives. The chronic disease prevalence growth in ageing global populations creates structural demand for sustained-release formulations whose compliance advantage compounds with the population's growing medication burden.

By Application, antibiotic drugs dominate, nutraceuticals grow fastest

Antibiotic and antibacterial drugs retained the dominant application position with approximately 22% of the empty capsules market in 2025. Capsules provide an effective modality to administer antibiotics orally because of ease of infectibility, better taste masking, and dose consistency for a treatment category whose global prescription volume reflects the ubiquitous incidence of bacterial infection across all therapeutic areas and demographic segments. Rising infectious disease incidence, increasing antimicrobial resistance driving new antibiotic development, and the global healthcare system's continued antibiotic prescription volume collectively sustain the application's dominant commercial position across both developed and developing healthcare markets.

Nutraceuticals is the fastest-growing application because the dietary supplement market's extraordinary commercial growth, driven by consumer health awareness, preventive healthcare trends, and the supplement industry's expansion into functional food and sports nutrition categories, creates above-average empty capsule demand. Each new supplement product launch that adopts capsule form over tablet, powder, or liquid alternatives creates empty capsule procurement whose commercial aggregate grows with the nutraceutical market's new product introduction velocity. The clean-label and natural supplement movement's preference for HPMC capsule containers creates synergistic growth between the fastest-growing material and the fastest-growing application segments.

By End User, pharmaceutical dominates, nutraceutical grows fastest

The pharmaceutical industry retained the dominant end-user position with approximately 58% of the empty capsules market in 2025. The pharmaceutical industry's heavy reliance on prescription-filled capsules across antibiotic, cardiovascular, oncology, neurological, and metabolic disease therapeutic categories creates the most commercially concentrated and highest-quality-specification empty capsule procurement of any end-user sector. Growing chronic disease prevalence, whose expanding patient population sustains prescription volume growth, ongoing drug approvals whose new molecular entity capsule formulations create new procurement streams, and the clinical trial sector's empty capsule requirement for novel drug development collectively sustain pharmaceutical's dominant market position.

The nutraceutical industry is the fastest-growing end user because the global dietary supplement market's extraordinary growth trajectory, whose supplement sales growth compounds with health consciousness, ageing population, and sports nutrition adoption across multiple consumer segments, creates above-average empty capsule volume procurement growth. Each dietary supplement manufacturer that expands production volume, each new supplement brand launch, and each supplement market entry in an emerging economy creates nutraceutical empty capsule procurement that compounds with the sector's commercial momentum. The nutraceutical industry's lower empty capsule quality specification relative to pharmaceutical GMP requirements creates cost-optimized procurement that sustains high-volume commercial relationships with capsule manufacturers.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

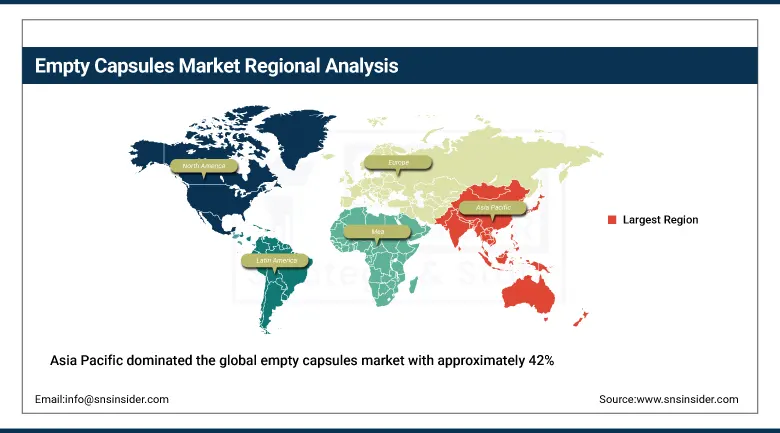

Asia Pacific Empty Capsules Market Insights

Asia Pacific dominated the global empty capsules market with approximately 42% of revenues in 2025, driven by high-capacity pharmaceutical manufacturing output, lower cost of production, and escalated government programme’s encouraging domestic drug development in China, India, and South Korea. China accounts for approximately 44.8% of Asia Pacific revenues through its position as the world's largest capsule manufacturing base, the domestic pharmaceutical industry's above-average production volume, and the growing nutraceutical market's supplement adoption.

India represents the most commercially dynamic emerging market within Asia Pacific where the generic pharmaceutical industry's extraordinary production scale creates consistent bulk gelatin capsule procurement, and the growing nutraceutical market creates new commercial demand channels beyond the established pharmaceutical procurement base.

North America Empty Capsules Market Insights

North America is the second-largest empty capsules market with approximately 28% of global revenues in 2025, benefiting from strong regulatory frameworks, high R&D investment, and a surging consumer preference for personalized medicine and premium nutraceutical supplementation. The United States accounts for approximately 87.4% of North American revenues through Lonza's Capsugel division, ACG Worldwide, and Qualicaps’ commercial operations.

Canada contributes approximately 12.6% of North American revenues through its pharmaceutical manufacturing sector's capsule procurement, the nutraceutical market's growing supplement production, and the natural health products industry's HPMC vegetarian capsule adoption.

Europe Empty Capsules Market Insights

Europe is a technically sophisticated empty capsules market where EU pharmaceutical regulation, Lonza's Swiss headquarters and Swiss-based Capsugel operations, and the pharmaceutical manufacturing sector's above-average quality specification create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its pharmaceutical industry's capsule procurement, the nutraceutical sector's supplement production, and the growing compounding pharmacy sector's patient-specific capsule dispensing.

The United Kingdom, Italy, and France are significant secondary markets where pharmaceutical manufacturing, contract manufacturing organization operations, and nutraceutical brands create consistent empty capsule demand. ACG Worldwide’s and Qualicaps’ European commercial presence sustains regional supply from established manufacturing and distribution networks.

MEA & Latin America Empty Capsules Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through Vision 2030's healthcare localization investment, import-substitution pharmaceutical policies, and growing domestic capsule manufacturing capacity serving both pharmaceutical and nutraceutical procurement. The UAE's specialty pharmaceutical sector and Egypt's expanding generic drug manufacturing industry add complementary regional demand across all capsule material categories. Brazil leads Latin American revenues at approximately 44.2% through its large pharmaceutical manufacturing base, ANVISA's regulatory dosage form framework, and the growing nutraceutical supplement market. Mexico's pharmaceutical manufacturing and Argentina's healthcare sector collectively sustain regional expansion through 2035.

Market Dynamics

Growth Drivers: Rising pharmaceutical drug approvals and nutraceutical market growth creating systematic empty capsule demand

Rising pharmaceutical drug approvals creating new molecular entity capsule formulations is the empty capsules market's most commercially certain structural growth driver. Each FDA, EMA, and equivalent regulatory approval of a capsule-formulated pharmaceutical creates a new empty capsule procurement stream whose volume scales with the drug's prescription market penetration. The growing global pharmaceutical pipeline, particularly in oncology, rare disease, and biologics-adjacent small molecule categories, creates systematic new drug launch capsule procurement that compounds with the existing drug product's ongoing commercial manufacturing volume.

The global nutraceutical market's extraordinary growth, compounding at above-average rates with consumer health awareness, ageing population supplement adoption, and sports nutrition market expansion, creates above-average empty capsule demand growth that sustains the market's overall growth trajectory above the pharmaceutical segment's more stable base. Each new supplement product launch, each entry into new international supplement markets, and each brand's production volume expansion creates nutraceutical empty capsule procurement whose commercial aggregate compounds with the sector's exceptional growth momentum.

Restraints: Gelatin supply constraints from animal source and regulatory complexity for novel capsule materials

Gelatin supply constraints from bovine and porcine processing by-products create raw material availability sensitivity for capsule manufacturers whose gelatin sourcing is dependent on the meat processing industry's production scale. Each disease event, regulatory restriction, or supply disruption in the bovine or porcine processing industry creates potential gelatin supply constraint that motivates capsule manufacturers’ HPMC alternative development investment. BSE-related restrictions on bovine gelatin use in certain pharmaceutical applications create structural motivation for HPMC alternative adoption that sustains plant-based capsule material growth.

Regulatory complexity for novel capsule material approvals, including pullulan, modified starch, and synthetic polymer alternatives, creates commercialization timeline challenges whose safety assessment, compatibility testing, and regulatory submission investment extends product launch timelines by 2-5 years from material development through regulatory approval and pharmaceutical customer validation.

Opportunities: HPMC capsule pharmaceutical specification and enteric-coated capsule advanced drug delivery

HPMC vegetarian capsule pharmaceutical specification growth represents the most commercially transformative near-term market opportunity. Each pharmaceutical company that specifies HPMC as the capsule material for a new drug product creates a long-duration procurement relationship whose commercial lifecycle spans the drug's patent protection and generic entry period. Lonza's Vcaps Plus demonstrated that HPMC capsules can operate at commercial-scale high-speed filling, removing the manufacturing efficiency barrier that previously limited pharmaceutical specification.

Enteric-coated capsule development for targeted intestinal delivery represents the most commercially premium capsule functionality growth opportunity. Each acid-sensitive API, probiotic requiring gastric protection, and colon-targeted therapeutic creates enteric capsule procurement whose above-immediate-release cost economics sustain premium commercial relationships for capsule manufacturers capable of providing validated delayed-release shell construction.

Recent Developments:

-

2023: Lonza reported a significant increase in demand for its Capsugel hard gelatin capsules in September 2023, driven by their use in novel drug formulations and clinical trials, reflecting growing pharmaceutical industry preference for capsule-based drug delivery.

-

2023: Capsugel (Lonza Group) introduced Vcaps Plus capsules with immediate-release properties in January 2023, tailored for high-speed filling processes and ensuring quick dissolution, enabling commercial-scale pharmaceutical manufacturing of HPMC vegetarian capsules.

-

2024: ACG Worldwide expanded its HPMC vegetarian capsule production capacity in 2024 with a new manufacturing line at its Pondicherry, India facility, targeting the growing global demand for plant-based pharmaceutical and nutraceutical capsule alternatives driven by vegan and halal consumer segments.

-

2024: Qualicaps launched a new line of pharmaceutical-grade pullulan capsules in 2024 with enhanced oxygen barrier properties and low moisture content, targeting sensitive APIs including omega-3 fatty acids, probiotics, and botanical extracts whose oxidative stability requirements create specification motivation beyond standard gelatin and HPMC alternatives.

-

2025: Suheung Co. expanded its production capacity for size 0 and size 00 HPMC vegetarian capsules in 2025 to meet growing demand from European and North American nutraceutical customers seeking plant-based dosage form alternatives compliant with vegan certification and clean-label supplement standards.

Empty Capsules Market Key Players

-

Lonza Group AG (Capsugel)

-

ACG Worldwide

-

Qualicaps Co. Ltd.

-

Suheung Co. Ltd.

-

Medi-Caps Ltd.

-

Sunil Healthcare Ltd.

-

Farmacapsulas SA de CV

-

Natural Capsules Limited

-

CapsCanada Corporation

-

Roxlor LLC

-

Lefan Capsule Co. Ltd.

-

Snail Pharma Industry Co. Ltd.

-

Zhejiang Huangyan Dawang Capsule Co.

-

Erawat Pharma Ltd.

-

Bright Pharma Caps Inc.

-

Capsugel Japan

-

GreenCaps Ltd.

-

Jilin Province Tuoze Biology Technology Co. Ltd.

-

BioCaps Enterprise

-

Healthcaps India Ltd.

Empty Capsules Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.72 Billion |

| Market Size by 2035 | USD 6.30 Billion |

| CAGR | CAGR of 5.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Material (Gelatin Capsules, HPMC/Vegetarian Capsules, Pullulan Capsules, Others) • by Functionality (Immediate Release, Sustained Release, Delayed Release, Enteric Coated, Others) • by Application (Antibiotic & Antibacterial Drugs, Cardiovascular Drugs, Antacids & Anti-flatulent, Nutritional Supplements, Pain Relief Drugs, Nutraceuticals, Others) • by End User (Pharmaceutical Industry, Nutraceutical Industry, Cosmetics & Personal Care, Contract Manufacturing Organizations) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Lonza Group AG (Capsugel), ACG Worldwide, Qualicaps Co. Ltd., Suheung Co. Ltd., Medi-Caps Ltd., Sunil Healthcare Ltd., Farmacapsulas SA de CV, Natural Capsules Limited, CapsCanada Corporation, Roxlor LLC, Lefan Capsule Co. Ltd., Snail Pharma Industry Co. Ltd., Zhejiang Huangyan Dawang Capsule Co., Erawat Pharma Ltd., Bright Pharma Caps Inc., Capsugel Japan, GreenCaps Ltd., Jilin Province Tuoze Biology Technology Co. Ltd., BioCaps Enterprise, Healthcaps India Ltd. |

Frequently Asked Questions

The Empty Capsules Market is expected to grow at a CAGR of 5.37% from 2026 to 2035.

The Empty Capsules Market was valued at USD 3.72 Billion in 2025.

Rising pharmaceutical drug approvals and chronic disease prevalence creating systematic capsule-based dosage form procurement, and the nutraceutical market's extraordinary growth creating above-average empty capsule demand from supplement manufacturers serving consumer health, wellness, and sports nutrition sectors.

Gelatin Capsules dominated the Empty Capsules Market with approximately 68% share in 2025, while HPMC/Vegetarian Capsules is the fastest growing segment.

Asia Pacific dominated the Empty Capsules Market with approximately 42% of revenues in 2025, with North America as the second-largest region at approximately 28%.

Get in Touch