Enteric Disease Testing Market Report Scope & Overview:

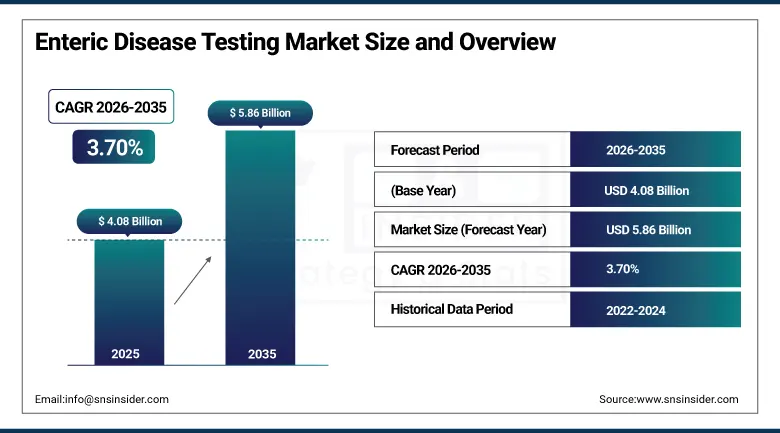

The Enteric Disease Testing Market was valued at USD 4.08 Billion in 2025 and is expected to reach USD 5.86 Billion by 2035, growing at a CAGR of 3.70% from 2026 to 2035.

The world enteric diagnostics testing market is experiencing steady growth through a combination of the persistent and significant burden of diseases of the gastro-intestinal system globally, the increasing use of rapid and molecular diagnostic techniques that allow replacement of traditional cultures for quicker and accurate results, and government led initiatives aimed at food safety and waterborne disease surveillance that led to planned procurement of diagnostic tests worldwide.

Factors driving growth in the world enteric diagnostics testing market include the increased occurrence of food borne and waterborne diseases globally with the mere 48 million cases per year in the United States alone, the improved molecular diagnostic and immunoassay tests allowing better sensitivity, specificity and quick turnaround time of results, and increased use of multiplex syndromic panel tests that can detect multiple enteric pathogens from one test sample.

In 2024, Thermo Fisher Scientific introduced an advanced TaqMan Pathogen Detection Kit that significantly strengthened real-time PCR capabilities for enteric disease testing by enabling simultaneous multi-target detection of key gastrointestinal pathogens including bacterial, viral.

Enteric Disease Testing Market Size and Forecast

-

Market Size in 2026E: USD 4.23 Billion

-

Market Size by 2035: USD 5.86 Billion

-

CAGR: 3.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Enteric Disease Testing Market - Request Free Sample Report

Enteric Disease Testing Market Trends

-

Multiplex syndromic testing panels are gaining adoption by enabling rapid detection of multiple bacterial, viral, and parasitic pathogens from a single sample.

-

Point-of-care enteric disease testing is expanding in emergency departments, urgent care centers, and primary care settings for faster diagnosis and treatment decisions.

-

AI-assisted diagnostic tools are improving test interpretation, outbreak monitoring, and antimicrobial resistance detection capabilities.

-

Next-generation sequencing (NGS) is increasingly used for pathogen identification, outbreak tracking, and antimicrobial resistance profiling.

-

Home-based and direct-to-consumer enteric disease testing kits are growing in popularity, supported by telehealth integration and rising consumer demand for convenient diagnostics.

U.S. Enteric Disease Testing Market Outlook

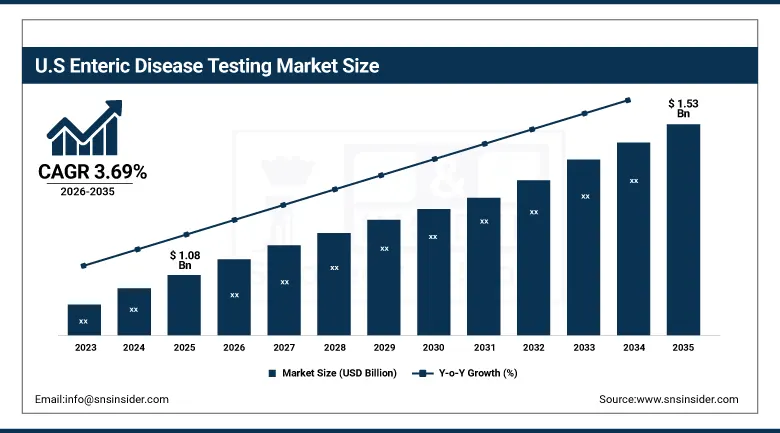

The U.S. Enteric Disease Testing Market was valued at approximately USD 1.08 Billion in 2025 and is expected to reach approximately USD 1.53 Billion by 2035, growing at a CAGR of approximately 3.69%.

The United States is the biggest single country market for enteric disease diagnostic tests owing to the high magnitude of foodborne diseases within the country which have been estimated by the CDC at 48 million per year thus forming the biggest commercially viable gastrointestinal diagnostics market in the world. Quest Diagnostics, Labcorp, BioFire Diagnostics, Cepheid, bioMérieux, and Thermo Fisher Scientific lead the commercial market in terms of enteric diagnostics assays and services in the United States. FDA clearances for multiple gastrointestinal multiplex panels such as BioFire FilmArray GI Panel, Luminex xTAG Gastrointestinal Pathogen Panel, and Meridian MIDI kits collectively make up a structured commercial platform for the use of syndromic enteric testing.

The United States enteric disease testing market leads the commercial market owing to the United States food safety requirements under FSMA, CDC FoodNet/OutbreakNet surveillance programs, and clinical laboratory automation investments.

Cepheid and Roche broadened their PCR-based gastrointestinal pathogen panel offerings in 2023 and 2024 to incorporate detection of antimicrobial-resistant enteric pathogens, responding to the WHO's emphasis on accelerating antimicrobial-resistant enteric pathogen surveillance and the growing clinical requirement for resistance gene identification alongside pathogen detection to guide appropriate antibiotic therapy selection.

Enteric Disease Testing Market Segment Analysis

-

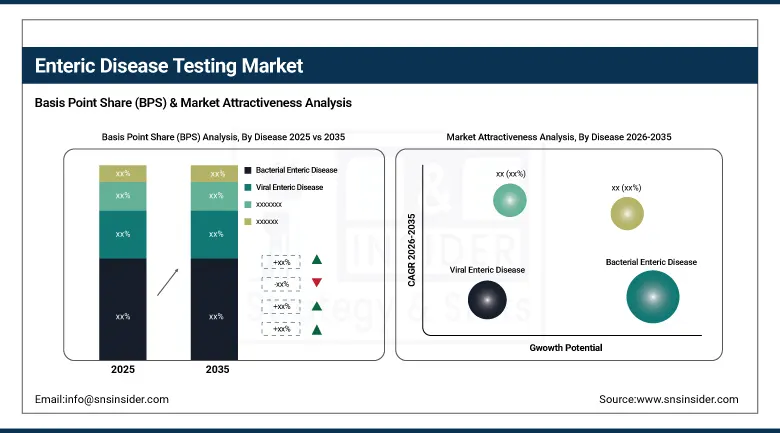

By Disease, the Bacterial Enteric Disease segment dominated the enteric disease testing market with approximately 54.31% share in 2025, while the Parasitic Enteric Disease segment is the fastest growing as expanding molecular diagnostic capability for protozoan and helminthic pathogen detection, growing clinical awareness of Giardia.

-

By Test Type, the Immunoassay segment dominated the enteric disease testing market with approximately 46.32% share in 2025, while the Molecular segment is the fastest growing as multiplex PCR panel adoption accelerates across clinical laboratories.

-

By End-Use, the Hospitals segment dominated the enteric disease testing market with approximately 42.11% share in 2025, while the Diagnostic Laboratories segment is the fastest growing as expanding private reference laboratory networks, growing ambulatory care send-out testing volume.

By Disease, bacterial dominates, parasitic grows fastest

Bacterial enteric diseases maintained their dominant position in terms of enteric disease testing in 2025, accounting for approximately 54.31% of the enteric disease testing market. The consolidation of enteric diagnostic expenditures in bacterial pathogen detection is attributable to the very high burden of enteric diseases caused by Salmonella, Clostridium difficile, Campylobacter, and E. coli infections that create the largest volumes of enteric pathogen testing in terms of commercial significance. Clostridium difficile-associated disease is a highly valuable hospital-acquired infection diagnostic testing area whose immunological and molecular testing creates a much greater diagnostic expenditure per episode than the ambulatory bacterial enteric disease testing episode.

The fastest growing disease category is parasitic enteric diseases due to the increasing capacity of molecular diagnosis of Giardia lamblia, Cryptosporidium parvum, and Entamoeba histolytica, an increasing awareness in the clinical setting of parasitic infection as a frequent cause of diarrhoea among immunocompromised individuals and multiplex syndromic gastrointestinal panels that include parasitic pathogens.

By Test Type, immunoassay dominates, molecular grows fastest

Immunoassays remained the leading test type with 46.32% of the enteric disease testing market in 2025. The commercial success of this technology is driven by the widespread use of ELISA and lateral flow immunoassay platforms for the fast identification of enteric pathogens such as Clostridium difficile toxins, Rotavirus, Norovirus, and Salmonella. This testing method's simplicity, involving no sample preparation and result generation without any need for thermal cycling devices and molecular biology expertise required in PCR, allows the continued dominance of immunoassays as the leading enteric test in clinical laboratories lacking molecular laboratory facilities.

Molecular testing is the fast-growing test type due to multiplex PCR panels that identify 20 or more pathogens in a single specimen in four hours and provide diagnostics with accuracy that cannot be achieved by immunoassay-based tests for individual pathogens. Each FDA-cleared gastrointestinal syndromic panel that identifies at least 20 pathogens in a single specimen within four hours is worth the high price in terms of clinical outcomes improvements, contributions to antibiotic stewardship, and infection control.

By End-Use, hospitals dominate, diagnostic laboratories grow fastest

The hospitals held the leading position in the use application of the enteric diseases tests with an estimated 42.11% share in 2025. The presentation of the acute enteric disease cases that are severe enough to be admitted into the hospital creates the need for the testing which is much more expensive than ambulatory testing per episode. Each hospitalization case of patients with severe Clostridium difficile colitis, invasive Salmonella infection and haemolytic uraemic syndrome caused by Shiga toxin producing E. coli causes comprehensive diagnostic examination that consists of several tests per episode.

The diagnostic laboratories became the fastest-growing segment because the mass of investigations of ambulatory enteric diseases is processed in the relations of send out testing of the primary care physicians and urgent cares, thus causing the concentration of the high-volume stool cultures, immunoassays, and multiplex panels in the reference laboratories. Each investment in automation of the multiplex gastrointestinal panel testing reduces the cost of the test improving the economics of the syndromic testing in comparison with the traditional sequential pathogen testing, hence increasing the adoption rate of the molecular enteric diagnostics.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

86.2% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Enteric Disease Testing Market Insights

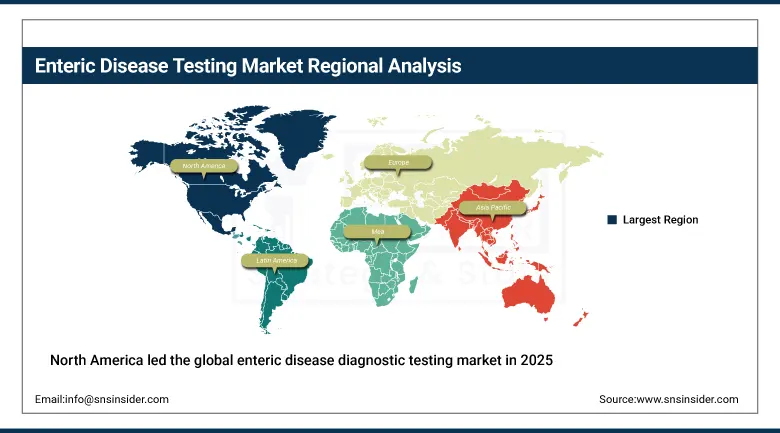

North America led the global enteric disease diagnostic testing market in 2025 owing to the exceptionally large market of the United States due to CDC-estimated 48 million annual cases of foodborne illnesses, the most advanced platform for clinical laboratory molecular testing infrastructure compared to other regions, and the commercial headquarters of BioFire Diagnostics, Cepheid, bioMérieux, and Thermo Fisher Scientific. The US market represents about 86.2% of North American market revenue due to the adoption of molecular panels in hospitals and reference laboratories, as well as investments in FoodNet surveillance program.

Canada represents about 13.8% of North American market revenue due to multiplex panels in clinical laboratories and the investments of the Public Health Agency of Canada in enteric disease surveillance program.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Enteric Disease Testing Market Insights

The Europe enteric diseases test market is a compliance-based market, driven by the stringent diagnostic product registration processes of the EU In Vitro Diagnostic Regulation (IVDR), the ECDC enteric disease surveillance system and the enteric pathogens testing program of national public health laboratories. Germany comprises 22.3% of European revenues due to its reference lab network, hospital clinical microbiology network and European business of bioMérieux and Roche Diagnostics.

The United Kingdom, France and the Netherlands are the other prominent secondary markets where NHS enteric tests conducted and the national food safety surveillance program keep the procurement constant. The transition to IVDR is creating a compliance opportunity for diagnostic vendors with registered products.

Asia Pacific Enteric Disease Testing Market Insights

The Asia Pacific region is considered to be the fasted growing regional enteric disease testing market on account of the high burden of enteric diseases in the region, advanced clinical laboratory technology, and government expenditure for food safety and enteric disease monitoring. The major revenue generator in the region is China, which contributes about 44.8% of the total revenue generated from enteric disease testing owing to increasing investment in clinical laboratory automation, food safety test infrastructure, and enteric disease testing in tertiary care hospitals using advanced platforms.

The emerging markets of India, Indonesia, and Vietnam are highly profitable in the Asia Pacific region because of the increasing enteric disease burden due to pathogen exposure and rising investments in private hospitals.

MEA & Latin America Enteric Disease Testing Market Insights

South Africa dominates MEA revenues with around 31.2%, which includes its private hospital laboratory, the enteric pathogen surveillance program of National Institute for Communicable Diseases, and molecular diagnostics of the reference laboratory in the Johannesburg and Cape Town metropolitan regions. Brazil leads Latin American revenues with around 44.2% through the country's clinical laboratories, the food safety testing regulation by ANVISA, and the adoption of hospital multiplex panels in São Paulo and Rio de Janeiro. México and Argentina provide complementary testing demands within the region up to 2035 through their respective clinical microbiology laboratories.

Market Dynamics

Growth Drivers: Rising global enteric disease burden and molecular multiplex panel adoption improving diagnostic comprehensiveness

The consistent and considerable burden of enteric diseases, in which the aggregate effect per annum of millions of instances of enteric diseases, mortality especially among paediatric patients and immunocompromised subjects, and food safety outbreaks create continuous demand for diagnostics that propels market growth at every level of healthcare system development. This is supported by the CDC report on the 48 million cases per year of foodborne illnesses in the U.S., and the data from the WHO on diarrhoeal diseases being the second leading cause of mortality among children younger than five years worldwide, and the rising burden of antimicrobial-resistant enteric pathogens which increases the significance of clinical consequences of the absence of proper diagnosis to motivate enteric disease diagnostics testing market procurement.

Multiplex molecular panel adoption's enhancement of diagnostic comprehensiveness creates a structural market growth engine that drives both the volume and price of testing. Every lab that changes from serial pathogen-specific culture and immunoassays testing to multiplex molecular panel testing produces revenues per test instance which exceed the value of the old testing protocol significantly while providing more sensitive pathogen detection and coverage.

Restraints: High molecular diagnostic test cost and regulatory variability across markets

The expense of the enteric diagnostic test kits with multiplex PCR costing between USD 50 to USD 300 makes it difficult to access such kits in health systems of low and middle-income countries where traditional culture-based tests are being used because they have poor diagnostic sensitivity and a long turnaround time. In each case where the expensive nature of these tests keeps manufacturers from using the more sensitive molecular panels, the less sensitive testing paradigm remains prevalent due to its low cost per test.

Different regulatory standards of different markets make it difficult for manufactures to bring their enteric diagnostic kits into the global market. The transitioning criteria under the IVDR in Europe, the complex FDA clearance process for molecular tests, and the lack of any standardized regulatory structure in developing countries create diverse routes, timeframes, and costs of entering the global market which leads to global market access inequality and developing regional markets differently.

Opportunities: Point-of-care testing expansion and AI-enhanced outbreak surveillance

PoC enteric diagnostics represents the closest market expansion opportunity in terms of commercial availability with its same-day results, which gives it significantly more clinical utility than send-out lab testing for the clinically critical areas of antibiotic prescription and infection isolation. Each emergency department, urgent care center, and primary care practice adopting PoC enteric pathogen identification produces testing volume which would have otherwise yielded no commercial benefit for the manufacturer, since it could not be tested by sending out samples to labs where timely results are not available.

Enteric disease testing integrated with AI-powered outbreak detection and cluster analysis provides commercial opportunity for the development of data analytics value-added service rather than just selling commodity test kits. Each laboratory network which integrates enteric disease tests with AI-powered outbreak identification, geographic clustering and AMR trend analysis generates additional motivation for institutional purchases beyond single-use test purchase motivation that keeps the price of an integrated test-surveillance solution above the level of simple commodity test kit.

Recent Developments:

-

2024: Cepheid expanded its Xpert Gastrointestinal Panel portfolio in 2024 with enhanced pathogen coverage incorporating additional bacterial and parasitic targets, enabling clinical laboratories to achieve comprehensive enteric syndromic testing on the widely deployed GeneXpert platform with expanded pathogen identification capability.

-

2024: bioMérieux enhanced its BIOFIRE GI Panel workflow capabilities in 2024 with faster time-to-result features and improved sample compatibility that extends the panel's clinical utility across a broader range of specimen types and collection conditions encountered in diverse clinical settings.

Enteric Disease Testing Market Key Players

-

bioMérieux SA

-

Cepheid (Danaher Corporation)

-

Thermo Fisher Scientific Inc.

-

Abbott Laboratories

-

Roche Diagnostics GmbH

-

Meridian Bioscience Inc.

-

Luminex Corporation (DiaSorin)

-

BD (Becton, Dickinson and Company)

-

Quidel Corporation (QuidelOrtho)

-

Hologic Inc.

-

Seegene Inc.

-

Qiagen NV

-

Siemens Healthineers AG

-

Bio-Rad Laboratories Inc.

-

Danaher Corporation

-

Chembio Diagnostics Inc.

-

Coris BioConcept SPRL

-

BÜHLMANN Laboratories AG

-

Savyon Diagnostics Ltd.

-

CorisBioConcept SA

Enteric Disease Testing Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.08 Billion |

| Market Size by 2035 | USD 5.86 Billion |

| CAGR | CAGR of 3.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Disease (Bacterial Enteric Disease, Viral Enteric Disease, Parasitic Enteric Disease) • By Test Type (Immunoassay, Molecular, Conventional, Chromatography & Spectrometry, Other Test Types) • By End-Use (Hospitals, Diagnostic Laboratories, Research & Academic Institutes, Other End-Users) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | bioMérieux SA, Cepheid (Danaher Corporation), Thermo Fisher Scientific Inc., Abbott Laboratories, Roche Diagnostics GmbH, Meridian Bioscience Inc., Luminex Corporation (DiaSorin), BD (Becton, Dickinson and Company), Quidel Corporation (QuidelOrtho), Hologic Inc., Seegene Inc., Qiagen NV, Siemens Healthineers AG, Bio-Rad Laboratories Inc., Danaher Corporation, Chembio Diagnostics Inc., Coris BioConcept SPRL, BÜHLMANN Laboratories AG, Savyon Diagnostics Ltd., and CorisBioConcept SA. |

Frequently Asked Questions

The Enteric Disease Testing Market is expected to grow at a CAGR of 3.70% from 2026 to 2035.

The Enteric Disease Testing Market was valued at USD 4.08 Billion in 2025.

Rising global enteric disease incidence creating consistent diagnostic procurement motivation, and molecular multiplex panel adoption that improves diagnostic comprehensiveness and per-episode testing revenue simultaneously while delivering antibiotic stewardship and infection control benefits that create institutional procurement justification beyond individual test cost.

Bacterial Enteric Disease dominated the Enteric Disease Testing Market with approximately 54.31% share in 2025.

North America dominated the Enteric Disease Testing Market in 2025.

Get in Touch