Hematology Analyzers Market Report Scope & Overview:

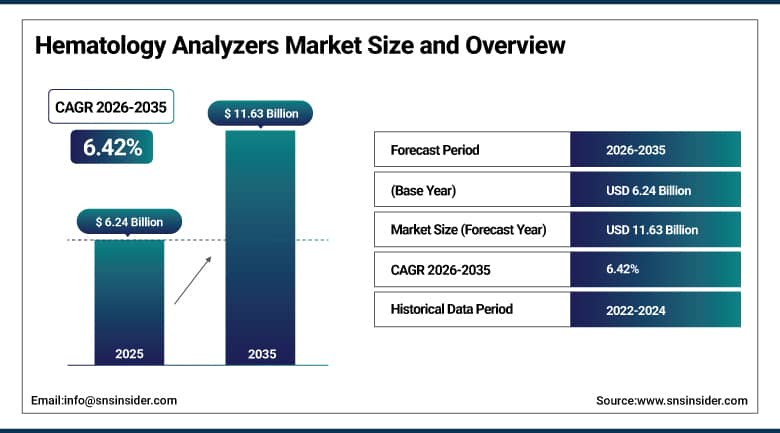

The Hematology Analyzers Market was valued at USD 6.24 Billion in 2025 and is expected to reach USD 11.63 Billion by 2035, growing at a CAGR of 6.42% from 2026–2035.

The global hematology analyzers market is growing at a sustained pace. Hematology analyzers are automated diagnostic instruments that perform complete blood counts and differentials, providing quantitative and morphological information about blood cells that guide diagnosis and monitoring of blood disorders, infections, and systemic diseases. The market is driven by the rising prevalence of blood disorders including anemia, leukemia, and other hematological malignancies, alongside the increasing aging population whose blood disorder susceptibility creates growing testing volume. More than 1.62 billion individuals globally are suffering from anemia, while leukemia constitutes 2.5% of all annual cancer diagnoses.

In August 2023, Abbott received FDA clearance for its Alinity h-series hematology system, allowing U.S. laboratories to conduct comprehensive blood count analyses as part of the Alinity integrated diagnostic product line. The clearance reflects the commercial direction of hematology analyzer development toward integrated multi-discipline analyzer platforms that share reagent handling, barcode tracking, and laboratory information system connectivity across hematology, chemistry, and immunoassay testing in a unified automated workflow that improves laboratory throughput and reduces total cost per test.

Market Size and Forecast

-

Market Size in 2026E: USD 6.64 Billion

-

Market Size by 2035: USD 11.63 Billion

-

CAGR: 6.42% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

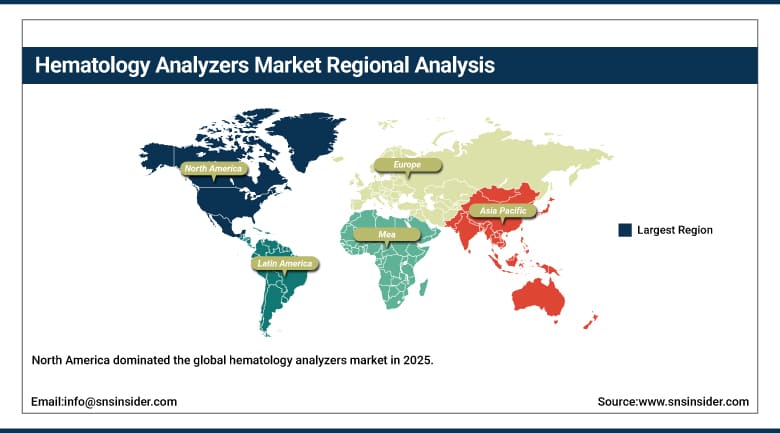

Largest Region: North America

To Get More Information On Hematology Analyzers Market - Request Free Sample Report

Hematology Analyzers Market Trends

-

Adoption of 5-part differential analyzers is increasing as healthcare facilities upgrade from 3-part systems to gain more comprehensive blood cell analysis capabilities

-

AI-powered digital morphology is improving automated blood cell classification accuracy while reducing manual slide review requirements in high-volume laboratories

-

Point-of-care hematology analyzers are gaining traction as hospitals and remote care settings require rapid complete blood count results at the patient bedside

-

Growing installation of advanced hematology analyzers is driving higher reagent consumption as newer systems require a broader range of consumables per test

-

Laboratory consolidation is increasing demand for high-throughput hematology analyzers capable of processing large sample volumes with minimal human intervention

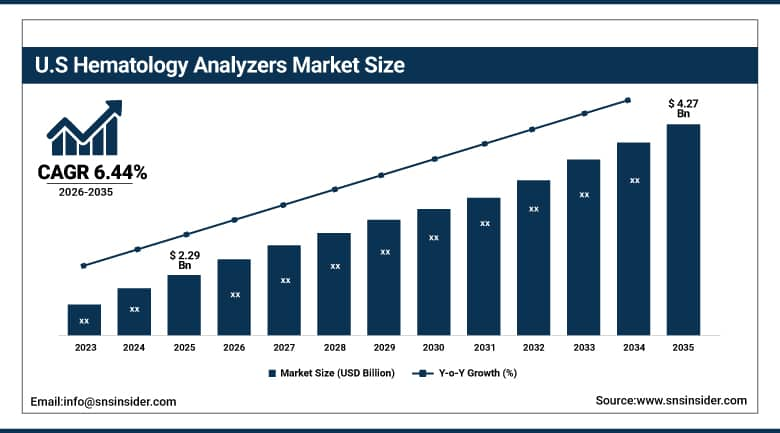

U.S. Hematology Analyzers Market Outlook

The U.S. Hematology Analyzers Market was valued at approximately USD 2.29 Billion in 2025 and is expected to reach approximately USD 4.27 Billion by 2035, growing at a CAGR of approximately 6.44%.

The U.S. is the world’s most commercially sophisticated hematology analyzers market within North America’s dominant revenue position. Sysmex, Abbott, Beckman Coulter, and Siemens Healthineers’ U.S. commercial operations define the domestic hematology analyzer market’s technology standard and commercial landscape. Abbott’s August 2023 Alinity h-series FDA clearance demonstrates the active regulatory pipeline that sustains continuous technology refresh procurement in U.S. laboratories. The Affordable Care Act’s expanded insurance coverage, the aging population’s growing blood disorder testing requirement, and oncology screening programme investment collectively sustain above-average U.S. hematology testing volume growth.

Sysmex Corporation launched its XN-10 hematology analyzer in 2024 with enhanced artificial intelligence capabilities for automated digital morphology review and reticulocyte analysis, targeting hospital laboratories seeking to reduce manual microscopy review without compromising diagnostic quality. The analyzer’s integrated AI morphology module enables laboratories to redirect haematologist review time from routine normal morphology assessments toward flagged abnormal samples whose clinical interpretation creates the highest diagnostic value.

Hematology Analyzers Market Segment Analysis

-

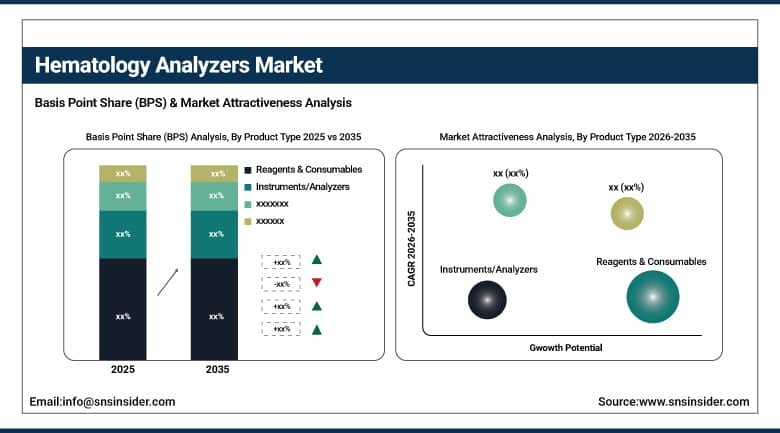

By Product Type, the Reagents & Consumables segment dominated the Hematology Analyzers Market with 48.23% share in 2025, while the Instruments/Analyzers segment is the fastest growing segment.

-

By Analyzer Type, the 5-Part Differential segment dominated the Hematology Analyzers Market with approximately 44% share in 2025, while the 6-Part Differential segment is the fastest growing segment.

-

By Technology, the Electrical Impedance segment dominated the Hematology Analyzers Market with approximately 38% share in 2025, while the Flow Cytometry/Fluorescence segment is the fastest growing segment.

-

By Application, the Anemia segment dominated the Hematology Analyzers Market with approximately 34% share in 2025, while the Blood Cancer & Hematological Malignancies segment is the fastest growing segment.

-

By End User, the Hospitals & Hospital Laboratories segment dominated the Hematology Analyzers Market with approximately 52% share in 2025, while the Clinical & Diagnostic Laboratories segment is the fastest growing segment.

By Product Type, reagents dominate, instruments grow fastest

Reagents and consumables retained the dominant product type position with 48.23% of the hematology analyzers market in 2025. Their commercial primacy reflects the recurring revenue structure of the diagnostics industry where each installed analyzer creates a continuous reagent consumption stream whose aggregate across the global installed base sustains above-average consumable procurement volume. Hematology reagents including diluents, lysing agents, staining reagents, calibrators, and controls are proprietary to each manufacturer’s analyzer platform, creating long-term supply relationships that sustain consumable revenue through the analyzer’s 7-10 year operational lifetime.

Instruments and analyzers are the fastest-growing product type because the systematic upgrade of 3-part differential systems in middle-income countries toward 5-part platforms, combined with new laboratory establishment in emerging economies, is creating above-average instrument procurement growth. Each new hospital or diagnostic centre that establishes hematology testing capability creates an instrument procurement event whose consumable revenue stream then sustains multi-year commercial relationships. AI-powered analyzer launches including the Sysmex XN-10 and Abbott Alinity h-series create upgrade procurement from existing laboratories seeking AI morphology capability that legacy systems cannot provide.

By Application, anemia dominates, blood cancer grows fastest

Anemia retained the dominant application position with approximately 34% of the hematology analyzers market in 2025. The WHO’s estimate that over 1.62 billion people globally suffer from anemia creates the most commercially substantial single blood disorder testing volume of any hematology application. Iron deficiency, vitamin B12 and folate deficiency, haemoglobinopathies, and chronic disease anemia collectively create the most geographically distributed and highest-volume hematology testing requirement. In developing markets where anemia’s nutritional cause creates population-scale prevalence, the primary healthcare system’s anemia screening requirement creates consistent hematology analyzer testing volume that sustains market demand across all economic development levels.

Blood cancer and hematological malignancies is the fastest-growing application because the global oncology diagnostics market’s expansion, the progressive adoption of comprehensive haematological profiling in cancer diagnosis, and the treatment monitoring requirements of blood cancer therapies are creating above-average hematology testing volume growth. Each new leukemia, lymphoma, or myeloma diagnosis creates a treatment monitoring testing programme whose longitudinal CBC and differential testing sustains per-patient testing volume across the treatment course. Immunotherapy and targeted therapy’s haematological side effect monitoring requirements create additional test volume that conventional chemotherapy regimens did not generate at equivalent frequency.

By Analyzer Type, 5-part differential dominates, 6-part grows fastest

5-part differential hematology analyzers retained the dominant analyzer type position with approximately 44% of the hematology analyzers market in 2025. The 5-part differential’s commercial dominance reflects its position as the current global standard for comprehensive blood count analysis whose five-population differential provides the neutrophil, lymphocyte, monocyte, eosinophil, and basophil counts that clinical guideline-based blood disorder diagnosis and monitoring requires. Each hospital laboratory and diagnostic centre that establishes comprehensive hematology testing capability specifies 5-part differential as the minimum clinical standard, creating systematic procurement that sustains the segment’s market leadership.

6-part differential is the fastest-growing analyzer type because the addition of immature granulocyte quantification to the standard 5-part differential creates clinical diagnostic value in sepsis detection, bone marrow recovery monitoring, and systemic inflammatory condition assessment that 5-part systems cannot provide without manual slide review. Each clinical laboratory that adopts 6-part differential eliminates the reflex manual review requirement for immature granulocyte flag resolution, improving workflow efficiency and diagnostic timeliness in high-volume critical care settings.

By End User, hospitals dominate, clinical labs grow fastest

Hospitals and hospital laboratories retained the dominant end-user position with approximately 52% of the hematology analyzers market in 2025. Hospital laboratories’ comprehensive testing menu, high daily sample volume from inpatient, emergency, and outpatient services, and the requirement for 24/7 hematology testing availability create the most commercially intensive hematology analyzer deployment environment. Each hospital laboratory’s multiple analyzer installation, redundancy requirement for critical testing continuity, and reagent consumption at multi-hundred sample per day volumes create per-hospital commercial relationships whose aggregate sustains the hospital segment’s market leadership.

Clinical and diagnostic laboratories are the fastest-growing end-user because the consolidation of community laboratory testing into centralised diagnostic laboratory networks creates high-throughput hematology analyzer demand whose volume and efficiency requirements drive premium automated analyzer specification. Commercial laboratory operators’ focus on cost per test economics and instrument uptime creates above-average investment in high-throughput 5-part and 6-part differential systems with robotic sample handling whose combined capability creates superior economics relative to multiple lower-throughput instruments.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Hematology Analyzers Market Insights

North America dominated the global hematology analyzers market in 2025 as the most commercially advanced diagnostic equipment market. The United States accounts for approximately 87.4% of North American revenues through its combination of the world’s highest per-capita healthcare spending, advanced diagnostic infrastructure, and the commercial presence of Sysmex, Abbott, Beckman Coulter, and Siemens Healthineers whose U.S. operations define the commercial and technology standard.

Canada contributes approximately 12.6% of North American revenues through its universal healthcare system’s consistent diagnostic laboratory investment, the growing oncology screening programme’s hematology testing requirement, and the research institute sector’s advanced hematology analyzer procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Hematology Analyzers Market Insights

Europe is a technically sophisticated hematology analyzers market where universal healthcare systems, national cancer screening programmes, and the EU’s medical device regulatory framework create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced hospital laboratory infrastructure, the healthcare system’s above-average hematology analyzer deployment density, and the medical device industry’s procurement sophistication.

The United Kingdom, France, and Italy are significant secondary markets where NHS, Santé Publique, and Servizio Sanitario Nazionale’s laboratory service networks create institutional-scale hematology analyzer procurement whose centralised purchasing creates commercially predictable large-contract opportunities for major analyzer manufacturers.

Asia Pacific Hematology Analyzers Market Insights

Asia Pacific is the fastest-growing regional hematology analyzers market, driven by expanding healthcare infrastructure in China, India, and Southeast Asia, the systematic upgrade of diagnostic laboratory capability, and the high prevalence of anemia, thalassaemia, and haematological malignancies in regional populations. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary hospital network expansion, the government’s healthcare infrastructure investment, and the domestic hematology analyzer manufacturer Mindray’s market presence whose competitive pricing creates broad adoption across tier-2 and tier-3 hospital facilities.

India’s Ayushman Bharat programme’s rural diagnostic infrastructure investment and ASEAN’s growing middle-class healthcare demand collectively create above-average first-time hematology analyzer installation procurement that compounds with ongoing reagent consumption growth.

MEA & Latin America Hematology Analyzers Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital network, Vision 2030’s healthcare investment programme, and the Ministry of Health’s diagnostic laboratory standardisation that creates structured hematology analyzer procurement. Brazil leads Latin American revenues at approximately 44.2% through its large SUS public health laboratory network, the growing private diagnostic laboratory sector, and the oncology centre’s hematological malignancy monitoring requirements.

UAE’s advanced hospital infrastructure, South Africa’s private laboratory sector, and Egypt’s expanding diagnostic network collectively represent significant MEA secondary markets whose growth sustains regional market development.

Market Dynamics:

Growth Drivers: Rising blood disorder prevalence and AI-powered analyzer technology creating diagnostic upgrade demand

Rising global blood disorder prevalence is the hematology analyzers market’s most structurally certain growth driver. Anemia’s 1.62 billion global sufferer count, leukemia’s 2.5% cancer incidence share, and the aging population’s growing hematological disease susceptibility create a continuously expanding testing volume whose aggregate across global laboratory infrastructure creates consistent hematology analyzer procurement. Each percentage point increase in blood disorder prevalence creates proportional testing volume growth whose commercial impact on reagent and instrument procurement sustains market expansion.

AI-powered analyzer technology is creating diagnostic upgrade demand that sustains instrument replacement investment beyond normal lifecycle replacement timing. Each analyzer generation that integrates AI morphology classification, improved differential accuracy, or expanded parameter reporting creates clinical motivation for laboratory upgrade investment whose economic justification is measured in improved diagnostic quality, reduced manual review time, and enhanced workflow efficiency. The Abbott Alinity h-series’ FDA clearance and Sysmex XN-10’s AI morphology capability represent the commercial precedents whose adoption creates peer laboratory upgrade motivation.

Restraints: High equipment cost limiting adoption in low-income markets and skilled operator shortage in emerging economies

High hematology analyzer instrument cost, ranging from USD 15,000-100,000 for high-end 5-part differential systems, creates adoption barriers in low-income country healthcare settings whose diagnostic laboratory budget constraints prevent premium instrument specification. Each developing country health ministry procurement decision that must choose between higher-performance 5-part systems and lower-cost 3-part alternatives creates market fragmentation whose lower-tier adoption limits the average selling price contribution per installation in the fastest-growing regional markets.

Skilled operator shortage in emerging economies creates a technical capability gap whose impact on advanced analyzer adoption is commercial. High-performance 5-part and 6-part differential hematology systems require trained laboratory scientists whose interpretation of flagged results, instrument troubleshooting capability, and quality control management create staffing requirements that rural and lower-tier facility laboratories in developing markets frequently cannot satisfy.

Opportunities: Point-of-care hematology expansion and AI-integrated morphology platform development

Point-of-care hematology analyzer expansion represents one of the most commercially dynamic near-term market development opportunities. Emergency department bedside complete blood count testing, intensive care unit real-time patient monitoring, and remote clinical setting diagnostic capability each require hematology analyzer systems whose portability, ease of operation, and rapid result delivery create specifications that traditional centralised laboratory analysers cannot satisfy. Each new POC hematology platform approval and clinical validation creates an adoption channel beyond the traditional laboratory setting.

AI-integrated morphology platform development represents the most commercially premium technology direction in hematology analyzers whose diagnostic quality improvement creates clinical value that sustains premium pricing. Each platform that demonstrates AI morphology classification accuracy equivalent to trained haematologist review at fraction of the manual time creates health system cost savings whose measurement validates premium instrument specification investment.

Recent Developments:

-

2023: Abbott received FDA clearance for its Alinity h-series hematology system in August 2023, enabling U.S. laboratories to conduct comprehensive blood count analyses as part of the Alinity integrated diagnostic platform creating unified workflow across hematology, chemistry, and immunoassay testing.

-

2024: Sysmex Corporation launched its XN-10 hematology analyzer in 2024 with enhanced AI capabilities for automated digital morphology review and reticulocyte analysis, enabling hospital laboratories to reduce manual microscopy review time while sustaining diagnostic quality.

-

2024: Mindray Medical launched its BC-7500 CRP hematology analyzer with integrated C-reactive protein measurement in 2024, enabling simultaneous CBC with 5-part differential and CRP testing from a single blood tube draw for fever workup and infection assessment in hospital emergency settings.

Hematology Analyzers Market Key Players:

-

Sysmex Corporation

-

Abbott Laboratories

-

Beckman Coulter Inc. (Danaher)

-

Siemens Healthineers

-

Mindray Medical International

-

HORIBA Ltd.

-

Bio-Rad Laboratories

-

F. Hoffmann-La Roche Ltd.

-

Nihon Kohden Corporation

-

EKF Diagnostics

-

Boule Diagnostics AB

-

Diatron (Stratec SE)

-

Ortho Clinical Diagnostics

-

Transasia Bio-Medicals

-

Trivitron Healthcare

-

Shenzhen Mindray Bio-Medical Electronics

-

Norma Instruments Zrt.

-

Agappe Diagnostics

-

Drew Scientific

-

Erba Mannheim

Hematology Analyzers Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.24 Billion |

| Market Size by 2035 | USD 11.63 Billion |

| CAGR | CAGR of 6.42% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Product Type (Reagents & Consumables, Instruments/Analyzers, Software & Services) • by Analyzer Type (3-Part Differential, 5-Part Differential, 6-Part Differential, Point-of-Care, Semi-Automated) • by Technology (Electrical Impedance, Flow Cytometry, Fluorescence Flow Cytometry, Light Scattering) • by Application (Anemia, Blood Cancer & Hematological Malignancies, Hemorrhagic Conditions, Infectious Diseases, Immune Disorders, Others) • by End User (Hospitals & Hospital Laboratories, Clinical & Diagnostic Laboratories, Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Sysmex Corporation, Abbott Laboratories, Beckman Coulter Inc. (Danaher), Siemens Healthineers, Mindray Medical International, HORIBA Ltd., Bio-Rad Laboratories, F. Hoffmann-La Roche Ltd., Nihon Kohden Corporation, EKF Diagnostics, Boule Diagnostics AB, Diatron (Stratec SE), Ortho Clinical Diagnostics, Transasia Bio-Medicals, Trivitron, Healthcare, Shenzhen Mindray Bio-Medical Electronics, Norma Instruments Zrt. Agappe Diagnostics, Drew Scientific, Erba Mannheim |

Frequently Asked Questions

The Hematology Analyzers Market is expected to grow at a CAGR of 6.42% from 2026 to 2035.

The Hematology Analyzers Market was valued at USD 6.24 Billion in 2025.

Rising prevalence of blood disorders including anemia affecting 1.62 billion people globally and leukemia comprising 2.5% of all cancer diagnoses, and AI-powered analyzer technology creating diagnostic upgrade demand beyond normal lifecycle replacement cycles.

Reagents & Consumables dominated the Hematology Analyzers Market with 48.23% share in 2025, while the Instruments/Analyzers segment is the fastest growing.

North America dominated the Hematology Analyzers Market in 2025, with the United States accounting for approximately 87.4% of North American revenues.

Get in Touch