mRNA Synthesis Raw Materials Market Report Scope & Overview:

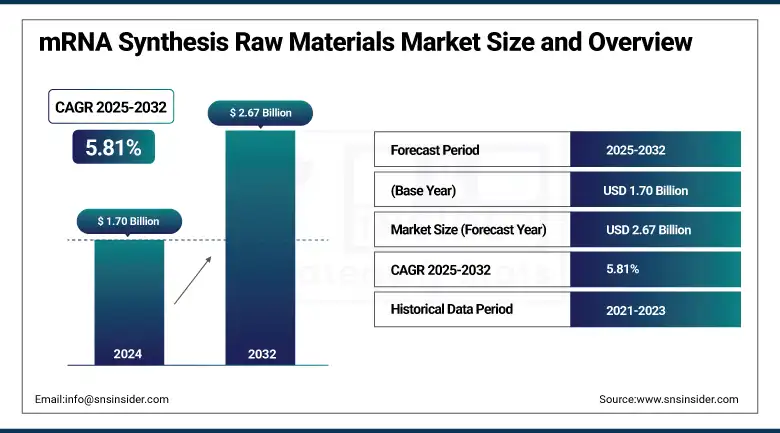

The mRNA Synthesis Raw Materials Market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 2.67 billion by 2032, growing at a CAGR of 5.81% over 2025-2032.

The mRNA synthesis raw materials market is growing fast, fueled by the explosive demand for mRNA-based treatments and vaccines, primarily in oncology, infectious diseases, and rare diseases. The success of mRNA COVID-19 vaccines has driven massive investment in mRNA platforms, so stimulating demand for high-purity raw materials, including IVT enzymes (T7 RNA polymerase and RNase inhibitors), nucleoside triphosphates (NTPs), capping reagents (CleanCap), and modified nucleotides (pseudouridine). Raw material requirements have led to a 5-to-10-fold rise above pre-pandemic levels. According to a survey conducted by BioProcess International (2024), more than 60% of mRNA developers experienced raw material supply issues in the last two years, revealing the imperative for strong sourcing strategies.

To Get more information On mRNA Synthesis Raw Materials Market - Request Free Sample Report

Apart from this, global investment in mRNA technology surpassed USD 5.5 billion in 2023, with industry giants including Moderna, BioNTech, and CureVac investing in manufacturing and R&D capacity. Moderna alone had its investment increased to USD 1.3 billion in 2023, with a significant focus on developing its pipeline of mRNA vaccines and therapies. Government support is also driving market growth. For instance, the U.S. Biomedical Advanced Research and Development Authority (BARDA) invested over USD 400 million in 2024 on advanced development of mRNA vaccines, driving upstream raw material demand.

Regulatory channels are also getting modified for the fast deployment of mRNA therapy. The U.S. FDA has also published revised CMC guidelines for mRNA treatments in 2024, particularly about low-endotoxin and GMP-compliant criteria-based approval for the suppliers of raw materials. Companies, including Thermo Fisher, have also concentrated on supply chain localization, investing in U.S. and European operations to produce locally.

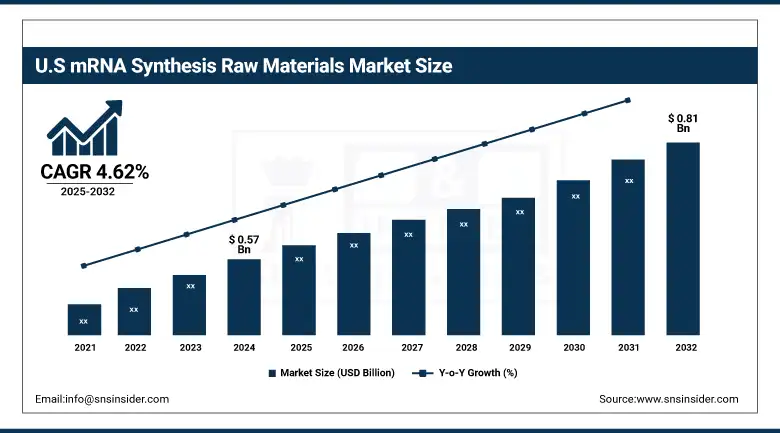

The U.S. mRNA synthesis raw materials market size was valued at USD 0.57 billion in 2024 and is expected to reach USD 0.81 billion by 2032, growing at a CAGR of 4.62% over 2025-2032. The U.S. led the region, with the highest percentage, led by its enormous vaccine manufacturing capacity, continued research in RNA therapeutics, and government-private mRNA research worth over USD 3.2 billion since 2022. The region has streamlined FDA regulations, encouraging raw material standardization and expedited approvals. Canada is also advancing in-house mRNA manufacturing, such as initiatives including the Moderna vaccine factory in Quebec, with Mexico becoming a cost-effective hub for reagent manufacturing and research outsourcing.

Market Dynamics:

Drivers:

-

Rising Therapeutic Applications, R&D Expansion, and Regulatory Acceleration Fuel Market Growth

The expanding application of mRNA technology beyond vaccines into oncology, autoimmune disorders, and orphan genetic indications is propelling record demand for high-quality raw materials. As of 2024, there are more than 190 active global clinical trials in which mRNA therapeutics, including new indications, such as protein replacement therapies and CAR-T therapies, are utilized, which further require strict IVT-grade materials.

Investments are increasing too, and Sanofi has invested USD 2.2 billion through 2025 in building an in-house mRNA center focused on therapeutic R&D. CureVac and GSK's JV has invested over USD 856 million to build mRNA flu and oncology pipelines. The rising formulation complexity is also fueling demand for highly specialized reagents, such as modified nucleotides and high-efficiency capping analogs. Regulators are keeping pace, too. In mid-2024, detailed guidance on mRNA-based drug CMC requirements was released, which facilitates the faster scale-up for the providers of raw materials to GMP standards. These efforts are generating a sustained growth driver for the mRNA synthesis raw materials market, driven by the high-volume procurement agreements that are now standard in strategic pharma partnerships.

Restraints:

-

Supply Chain Vulnerabilities, Cost Pressure, and Quality Standardization Issues Hamper Market Expansion

One of the most significant restraints in the raw materials for mRNA synthesis market is the ongoing supply chain delays, particularly in the production of enzymes, capping reagents, and clean-room grade consumables. In a 2024 BioPlan Associates survey, 68% of mRNA developers experienced delays or shortages in acquiring high-purity reagent access, which affects batch release schedules. The stringent GMP-grade requirements and the endotoxin-free purity standards further reduce the qualified raw material supplier pool.

Additionally, the IVT reagent cost has increased by 30–40% over the last three years, with strict quality requirements and restrictive manufacturing scalability. The small biotech players are hit the hardest, with high upfront procurement costs restricting early-stage development. Another restraint is the absence of global standardization of raw material specifications, inducing batch-to-batch variability, which creates regulatory and reproducibility concerns. While large companies, such as Agilent and ST Pharm, are shifting toward end-to-end raw material pipeline integration, the industry still lacks harmonized reference standards. These collective constraints challenge the market in satisfying increasing demand at scale in line with affordability.

mRNA Synthesis Raw Materials Market Segmentation Analysis:

By Type

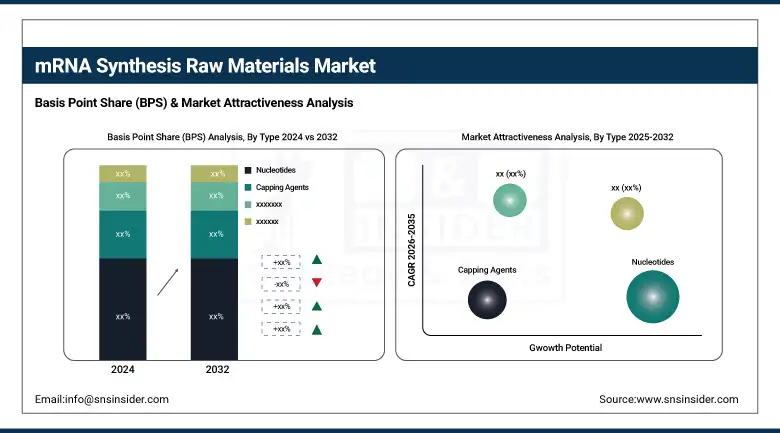

In 2024, the nucleotides segment accounted for the largest revenue share in the global mRNA synthesis raw materials market at 36.9% of total revenue. This is because nucleotides—ATP, GTP, CTP, and UTP- are essential to the in vitro transcription (IVT) process, which is the cornerstone of mRNA synthesis. Greater large-scale mRNA vaccine and therapeutic manufacturing has fueled demand for high-purity and GMP-grade nucleotides aggressively.

Alternatively, the capping agents segment is predicted to expand at the highest growth rate due to heightened emphasis on improving mRNA stability and translational efficiency. Advanced capping technologies, such as CleanCap analogs and anti-reverse cap analogs (ARCA), are increasing adoption for optimizing mRNA-based drug efficacy, especially in oncology and rare diseases.

By Application

The vaccine production segment retained the maximum revenue share of 82.3% in 2024, owing to global immunization drives and pandemic preparedness efforts. Bulk procurement of raw materials remains influenced by the high level of mRNA vaccines manufactured for COVID-19, RSV, and influenza.

The therapeutics production segment is growing at the maximum rate owing to a growing pipeline of mRNA-based therapeutics for cancer, cystic fibrosis, and genetic disease treatment. As increasing numbers of mRNA therapies move through clinical trials and into commercial development, the need for customized raw materials that are designed to therapeutic-grade specifications is growing at a fast pace.

By End Use

Pharmaceutical and biopharmaceutical companies dominated the end-use segment with a 48.5% market revenue contribution in 2024. They are attributed to their in-house large-scale production facility and investments by market leaders, such as Sanofi, BioNTech, and Moderna, in the development of the mRNA platform. They are utilizing large quantities of raw materials directly for the development of vaccines and therapies.

As biotech startups and mid-sized enterprises are outsourcing mRNA development on a significant scale to use the knowledge and infrastructure of CROs, the segment of Contract Research Organizations (CROs) and Contract Manufacturing Organizations (CMOs) is expanding at the highest rate. Increasing partnerships and technology transfer agreements are further driving raw material demand from the segment.

Regional Insights:

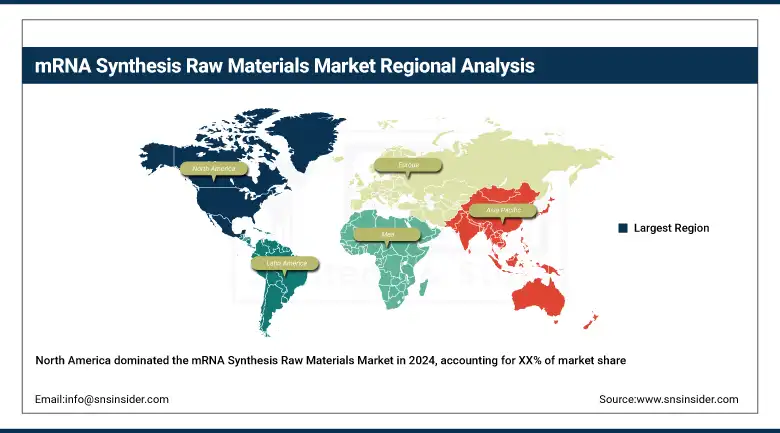

North America was the biggest mRNA synthesis raw materials market in 2024, led by its established biotechnology infrastructure, high R&D spending, and presence of industry heavyweights, such as Moderna and Thermo Fisher Scientific.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second-largest and fastest-expanding market, fueled by strong regulatory backing, world-class research institutions, and strategic collaborations. Germany dominates the regional market, spearheaded by BioNTech's high raw material usage and localization. Germany's government invested over €2 billion in biotech innovation during 2021–2024, fueling upstream demand. The U.K. is the region's fastest-expanding country, with government-backed initiatives to localize mRNA and vaccine manufacturing. The U.K. Vaccine Innovation Centre in Oxford fueled demand for cGMP-grade nucleotides and enzymes. France and Italy are expanding CDMO capacity to support regional therapeutic development.

Asia Pacific is the region's fastest-growing market, fueled by rising vaccine manufacturing capacity, expanding clinical trials, and encouraging government patronage for biotech localization. China leads the region by market share, with robust state backing for mRNA platforms and raw material self-sufficiency. Industry leaders, including Stemirna Therapeutics and Walvax Biotechnology, are scaling up local manufacturing with Chinese-made reagents. India is expanding most rapidly in Asia Pacific, with players including Biological E. and Gennova Biopharmaceuticals manufacturing mRNA vaccines and investing in local reagent production. Japan and South Korea are focusing on high-purity enzyme development and cleanroom reagent supply for precision therapeutics.

mRNA Synthesis Raw Materials Market Key Players:

Leading mRNA synthesis raw materials companies in the market are Thermo Fisher Scientific, Merck KGaA, Cytiva, TriLink BioTechnologies, New England Biolabs, BioNTech, Moderna, CureVac, GenScript, and ST Pharm.

Recent Developments:

In January 2025, Thermo Fisher Scientific launched a new GMP-compliant IVT kit featuring ultra-pure nucleotide sets and RNase-free reagents designed to reduce purification time in mRNA manufacturing, enhancing scalability.

In April 2025, BioNTech announced a USD 1.07 billion expansion of its Marburg facility to include an in-house raw material production unit focused on high-volume synthesis of capping reagents and modified nucleotides, aiming to reduce reliance on third-party suppliers.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.70 billion |

| Market Size by 2032 | USD 2.67 billion |

| CAGR | CAGR of 5.81% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Capping Agents (CleanCap Reagents, ARCA (Anti-Reverse Cap Analog), and Others), Nucleotides (Modified Nucleic Acids, (N1-methylpseudouridine-triphosphate, 5-Methylcytidine triphosphate (5mCTP), and Others), Natural Nucleic Acids (Adenine, Guanine, Cytosine, and Uracil), Plasmid DNA, Enzymes (Polymerase, RNase Inhibitor, DNase, and Others), Others) • By Application (Vaccine Production, Therapeutics Production, and Others) • By End Use (Biopharmaceutical & Pharmaceutical Companies, CROs & CMOs, and Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Thermo Fisher Scientific, Merck KGaA, Cytiva, TriLink BioTechnologies, New England Biolabs, BioNTech, Moderna, CureVac, GenScript, and ST Pharm |

Frequently Asked Questions

Future trends include the increased adoption of personalized mRNA therapies, a rise in self-amplifying and circular RNA research, and the development of next-gen capping technologies to improve mRNA stability and translation.

North America, led by the U.S., dominates the market due to strong biotechnology infrastructure, government support, and major players headquartered in the region.

Key players include Thermo Fisher Scientific, Merck KGaA (MilliporeSigma), TriLink BioTechnologies, New England Biolabs, Cytiva (Danaher), BioNTech, Moderna, GenScript, CureVac, and ST Pharm.

Growth is driven by the expanding application of mRNA technology in infectious disease vaccines, cancer therapeutics, and rare genetic disorders, along with heavy R&D investments, government funding, and the need for GMP-compliant raw materials such as nucleotides, capping agents, and enzymes.

The global mRNA synthesis raw materials market was valued at USD 1.70 billion in 2024 and is projected to reach USD 2.67 billion by 2032, growing at a CAGR of 5.81% from 2025 to 2032.

Get in Touch