Erythropoietin Drugs Market Report Scope & Overview:

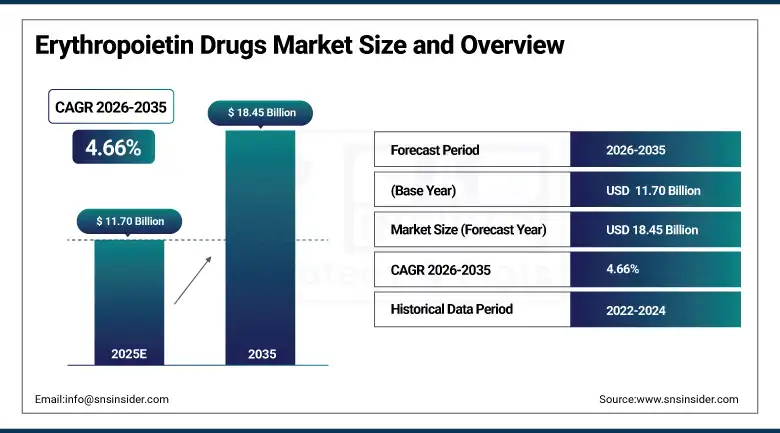

The Erythropoietin Drugs Market size is estimated at USD 11.70 Billion in 2025 and is expected to reach USD 18.45 Billion by 2035, growing at a CAGR of 4.66% over the forecast period of 2026-2035.

The global erythropoietin drugs market is experiencing stable growth owing to the increasing prevalence of chronic kidney disease (CKD), cancer-related anemia, and the rising demand for effective anemia management therapies. The growing aging population worldwide and the rising incidence of lifestyle-related diseases such as diabetes and hypertension, which frequently lead to renal complications, are further increasing the patient pool requiring erythropoietin therapy. In addition, advancements in biotechnology manufacturing and the growing adoption of biosimilar erythropoietin products are contributing to improved accessibility and affordability of treatment across developing healthcare systems.

The initiatives taken by the government to provide healthcare facilities along with reimbursement support for the treatment of anemia in various countries, especially developed countries, are also contributing to the growth of the market. Pharmaceutical companies are still investing heavily in R&D activities to develop effective formulations to treat anemia. Long-acting agents such as darbepoetin alfa have improved the rate of compliance for the treatment of anemia by reducing the frequency of the doses.

In March 2025, global dialysis networks reported a 15% increase in the adoption of long-acting erythropoiesis-stimulating agents, highlighting the growing clinical preference for therapies that reduce hospital visits and improve anemia management outcomes.

Erythropoietin Drugs Market Size and Forecast:

-

Market Size in 2025: USD 11.70 Billion

-

Market Size by 2035: USD 18.45 Billion

-

CAGR: 4.66% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Erythropoietin Drugs Market - Request Free Sample Report

Erythropoietin Drugs Market Trends:

-

Increasing adoption of biosimilar erythropoietin drugs due to their cost-effectiveness and comparable clinical efficacy to reference biologics.

-

Rising development of long-acting erythropoiesis-stimulating agents that reduce dosing frequency and improve patient adherence.

-

Growing demand for anemia treatments among chronic kidney disease patients undergoing dialysis and renal replacement therapy.

-

Technological advancements in recombinant DNA technology improving large-scale manufacturing of erythropoietin biologics.

-

Expansion of hospital-based anemia management programs integrating erythropoietin therapy with comprehensive renal care.

-

Increasing clinical studies investigating potential neuroprotective and tissue-protective roles of erythropoietin beyond hematology.

-

Rising healthcare expenditure and government reimbursement programs supporting access to anemia therapies in developed markets.

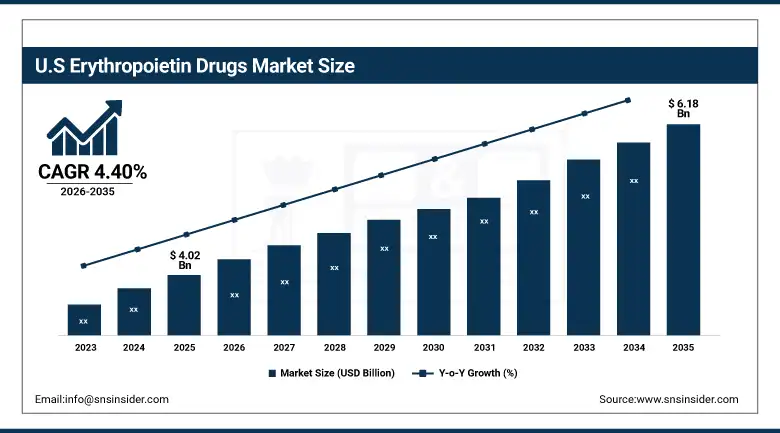

The US Erythropoietin Drugs Market is estimated to be valued at USD 4.02 billion in 2025, which is expected to grow up to USD 6.18 billion by 2035, registering a CAGR of 4.40% during the forecast period of 2026-2035. The US is a major market for Erythropoietin Drugs due to its high prevalence of chronic kidney disease, presence of major biopharma companies, and well-developed dialysis services. In addition, the availability of insurance coverage for anemia treatments under Medicare and other US health systems has helped increase patient access to these treatments. The country also has ongoing clinical research and approvals for biosimilar versions of Erythropoietin Drugs, allowing these products to be priced competitively in the market.

Erythropoietin Drugs Market Growth Drivers:

-

Rising Prevalence of Chronic Kidney Disease and Dialysis Patients Driving Market Growth

One of the major factors that is contributing to the growth of the global erythropoietin drugs market is the rise in the prevalence of chronic kidney disease (CKD) worldwide. Patients with CKD are susceptible to anemia due to the reduced level of endogenous erythropoietin. Therefore, the patients with CKD are in dire need of ESA therapy. There are millions of patients with CKD who are on dialysis. Therefore, the number of patients who are in need of erythropoietin is growing steadily. In addition to that, lifestyle disorders like diabetes and hypertension are contributing to the prevalence of CKD.

The growth in the number of dialysis centers and nephrology care facilities has also increased the adoption rate for erythropoietin injections. Hospitals and healthcare facilities have started to adopt standardized anemia management guidelines that include injections of erythropoietin for the maintenance of optimal hemoglobin levels in patients undergoing renal replacement therapy. The short- and long-acting formulations help in the administration of injections according to the requirements of the patients.

For instance, in February 2025, international nephrology associations reported that more than 70% of dialysis patients globally receive erythropoiesis-stimulating agents as part of their routine anemia management therapy.

Erythropoietin Drugs Market Restraints:

-

Safety Concerns and Strict Regulatory Monitoring Limiting Market Expansion

Despite the positive clinical acceptance of erythropoiesis-stimulating agents, some safety issues related to erythropoietin products are limiting the growth of the market. High doses of erythropoiesis-stimulating agents have been found to be associated with an increased risk of cardiovascular events like hypertension, thrombotic events, and stroke in cancer patients receiving chemotherapy. Therefore, appropriate dosing regimens are required to prevent excessively high hemoglobin levels.

Stringent safety monitoring requirements need to be fulfilled by regulatory bodies of major markets, including North America and Europe, prior to approval of erythropoietin products. Such regulatory hurdles may cause delays in approval of new therapies and biosimilars. In addition, physicians are becoming increasingly cautious in prescribing these erythropoietin agents for cancer-related anemia due to concerns over tumor progression risks observed in previous clinical studies.

Erythropoietin Drugs Market Opportunities:

-

Expansion of Biosimilars and Emerging Market Demand Creating Growth Opportunities

With the increasing use of biosimilar erythropoietin products, there are a number of opportunities for both drug makers and healthcare providers. This is because biosimilars have the same therapeutic benefits as the original biologic product, while they are cheaper for the healthcare system. With the patent expirations of major biologic erythropoietin products, biosimilar makers are increasing their product portfolios.

The emerging economies in Asia Pacific, Latin America, and the Middle East are experiencing a surge in the development of healthcare infrastructure facilities for dialysis services, thereby creating a high demand for cost-effective solutions for the treatment of anemia. Government initiatives for increasing access to chronic disease management services are boosting the market for biosimilars.

For example, in January 2025, a major biosimilar manufacturer launched a cost-efficient recombinant erythropoietin therapy across multiple Asian markets, improving treatment accessibility for thousands of dialysis patients.

Erythropoietin Drugs Market Segment Analysis:

-

By type, biologics accounted for the largest share of 63.42% in 2025, while the biosimilars segment is projected to grow at the fastest CAGR of 6.18% during the forecast period.

-

By product, erythropoietin dominated the market with a revenue share of approximately 58.36% in 2025, whereas darbepoetin-alfa is expected to grow at the highest CAGR of 5.12% due to its long-acting therapeutic properties.

-

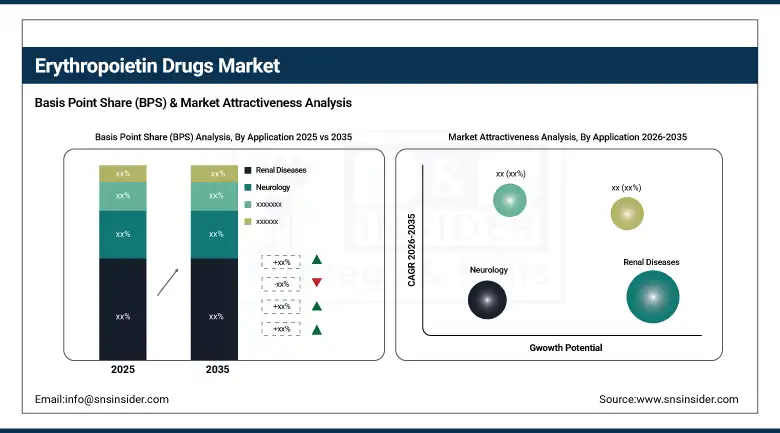

By application, renal diseases held the largest share of around 52.18% in 2025, followed by cancer-related anemia treatment.

By Application, Renal Diseases Segment Dominates the Market

The renal diseases segment accounted for the largest revenue in the market. This segment accounted for a significant 52.18% of the overall revenue generated in the market during 2025. This is due to the high prevalence rate of anemia among patients suffering from chronic kidney disease. The kidney is responsible for the production of the hormone erythropoietin. This hormone is naturally produced in the body. However, when the kidney fails to function properly, the production of this hormone is not adequate.

Another segment of the market, which is covered by the cancer segment, is the significant portion of the market share, as erythropoietin products are used to treat anemia, which is caused by chemotherapy. This can help alleviate the need for transfusions as well as improve the quality of life for cancer patients who are subjected to aggressive treatment. However, there is clinical research underway to determine the potential use of erythropoietin for the treatment of neurological disorders as well.

By Type, Biologics Lead the Market, While Biosimilars Gain Rapid Adoption

The dominant class of drug in the market is biologic erythropoietin agents, which have a market revenue share of over 63.42% in 2025. The established biologic agents are trusted by physicians, well validated clinically, and have gained approvals under various healthcare systems worldwide. These agents are still popular in developed markets where reimbursement is favorable for premium biologic agents.

However, biosimilars are witnessing rapid adoption due to the increased need to reduce healthcare costs. There is a gradual shift towards biosimilar erythropoietin therapy in hospitals and dialysis centers. As the regulatory environment for biosimilars becomes standardized globally, the rate of adoption for biosimilars is expected to rise rapidly.

By Product, Erythropoietin Segment Holds the Largest Market Share

The erythropoietin product segment had the largest market share of about 58.36% in 2025, as it is an established treatment for anemia in patients with chronic kidney diseases and chemotherapy, which are widely used in hospitals and dialysis centers for their well-proven clinical efficacy.

On the other hand, darbepoetin-alfa is expected to experience strong growth during the forecast period. The half-life of darbepoetin-alfa is long enough to require less frequent injections compared to conventional injections of erythropoietin.

Erythropoietin Drugs Market Regional Highlights:

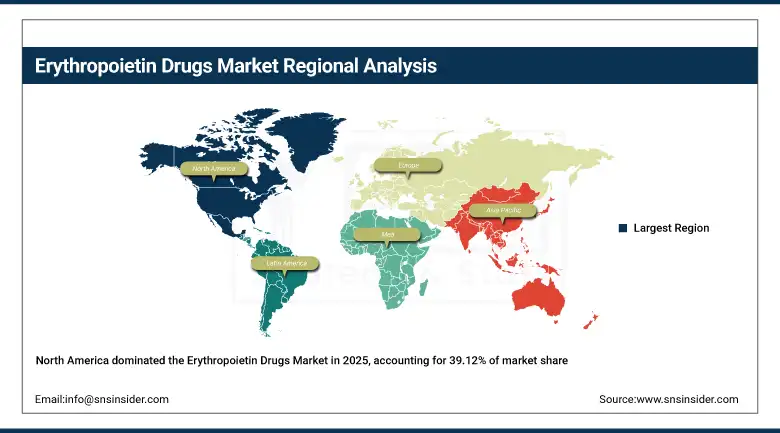

Asia Pacific Erythropoietin Drugs Market Insights:

The Asia Pacific region is expected to grow faster in terms of market size, registering a CAGR of 5.34% during the forecast period. This is due to the increasing patient pool of people suffering from chronic kidney disease and anemia, particularly in China and India. The investments in the healthcare sector, expansion of dialysis services, and increasing presence of biosimilar drug manufacturers are also boosting the market in this region.

North America Erythropoietin Drugs Market Insights:

The North American region held the highest market share of 39.12% in 2025 due to well-developed dialysis services, high healthcare expenditure, and robust regulatory support for biologic agents. The presence of key pharmaceutical players, well-developed biotechnology infrastructure, and early adoption of cutting-edge anemia therapy are key contributors to the dominance of the North American market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Erythropoietin Drugs Market Insights:

Europe represents the second largest market due to the robust government healthcare systems, dialysis services, and the early adoption of biosimilar erythropoietin products. Several European countries have been encouraging biosimilar substitution policies, which have enabled the higher adoption of biosimilars within their hospital systems.

Latin America (LATAM) and Middle East & Africa (MEA) Erythropoietin Drugs Market Insights:

The Latin America & MEA erythropoietin drugs market is expanding steadily. This can be attributed to the increasing investments in the healthcare industry, diagnostic capabilities, and awareness of the importance of anemia treatment. Governments are investing heavily in the improvement of the dialysis facilities of patients suffering from chronic diseases. This will have a positive impact on the erythropoietin market.

Erythropoietin Drugs Market Competitive Landscape:

Amgen Inc. is one of the pioneers in erythropoiesis-stimulating agent development and continues to maintain a strong presence in the market through its established biologic therapies used for anemia management among chronic kidney disease and cancer patients.

-

In April 2025, the company expanded global distribution of its anemia therapy portfolio through partnerships with dialysis service providers in emerging markets.

Roche Holding AG is another major market participant focusing on biotechnology-driven therapies and advanced biologic manufacturing platforms to improve treatment accessibility for anemia patients worldwide.

-

In December 2024, the company strengthened its biologics production capacity to support increasing global demand for erythropoietin therapies.

Johnson & Johnson continues to invest in hematology research and biosimilar development to expand its presence in the anemia treatment market.

-

In January 2025, the company collaborated with multiple hospital networks to evaluate long-term clinical outcomes of erythropoiesis-stimulating therapies in oncology patients.

Erythropoietin Drugs Market Key Players:

-

Amgen Inc.

-

Roche Holding AG

-

Johnson & Johnson

-

Pfizer Inc.

-

Novartis AG

-

Teva Pharmaceutical Industries Ltd.

-

Biocon Ltd.

-

Dr. Reddy’s Laboratories

-

Intas Pharmaceuticals

-

LG Chem Life Sciences

-

Celltrion Healthcare

-

Samsung Bioepis

-

Kyowa Kirin Co., Ltd.

-

3SBio Inc.

-

Reliance Life Sciences

-

Zydus Lifesciences

-

Sun Pharmaceutical Industries

-

Hetero Biopharma

-

Glenmark Pharmaceuticals

-

Stada Arzneimittel AG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.70 Billion |

| Market Size by 2035 | USD 18.45 Billion |

| CAGR | CAGR of 4.66% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Biologics, Biosimilars) • By Application (Cancer, Renal Diseases, Neurology, Others) • By Product (Erythropoietin, Darbepoetin-alfa) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Amgen Inc., Roche Holding AG, Johnson & Johnson, Pfizer Inc., Novartis AG, Teva Pharmaceutical Industries Ltd., Biocon Ltd., Dr. Reddy’s Laboratories, Intas Pharmaceuticals, LG Chem Life Sciences, Celltrion Healthcare, Samsung Bioepis, Kyowa Kirin Co. Ltd., 3SBio Inc., Reliance Life Sciences, Zydus Lifesciences, Sun Pharmaceutical Industries, Hetero Biopharma, Glenmark Pharmaceuticals, Stada Arzneimittel AG |

Frequently Asked Questions

The Erythropoietin Drugs Market is estimated to be valued at USD 11.70 billion in 2025 and is projected to reach USD 18.45 billion by 2035, growing at a CAGR of 4.66% during 2026–2035.

Erythropoietin drugs are primarily used to treat anemia, especially in patients with chronic kidney disease (CKD), cancer-related anemia caused by chemotherapy, and other conditions that reduce red blood cell production.

The market growth is driven by the increasing prevalence of chronic kidney disease, rising dialysis patient population, growing demand for anemia treatment, and advancements in biotechnology manufacturing.

The renal diseases segment dominates the market, accounting for around 52.18% of the total market share in 2025, due to the high prevalence of anemia among CKD patients.

Biosimilar erythropoietin drugs are gaining popularity because they offer similar therapeutic benefits to original biologics while being more cost-effective, improving treatment accessibility.

Get in Touch