Catalyst Regeneration Market Report Scope & Overview:

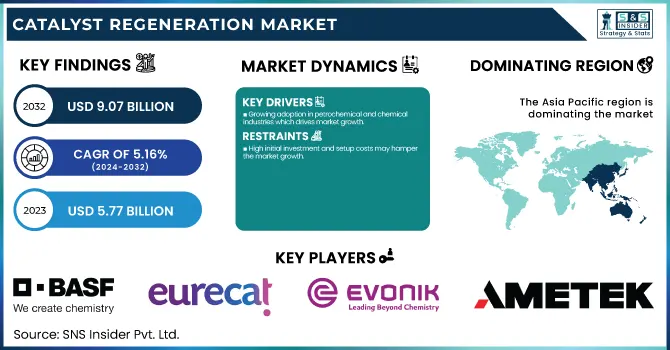

The Catalyst Regeneration Market size was USD 5.77 Billion in 2023 and is expected to reach USD 9.07 Billion by 2032 and grow at a CAGR of 5.16 % over the forecast period of 2024-2032. This report provides comprehensive statistical insights and trends in the catalyst regeneration market, covering key aspects such as production capacity and utilization rates by country and type, along with feedstock and regeneration costs across major regions. It examines the regulatory impact and environmental compliance, highlighting sustainability initiatives and waste reduction efforts. The report also explores innovation and R&D investments, focusing on advancements in regeneration technologies. Additionally, it analyzes market adoption trends by industry and region, providing a clear picture of demand across the refining, petrochemical, and chemical sectors. These insights help stakeholders understand market dynamics, cost structures, and growth opportunities in catalyst regeneration.

Catalyst Regeneration Market Size and Forecast

-

Market Size in 2023: USD 5.77 Billion

-

Market Size by 2032: USD 9.07 Billion

-

CAGR: 5.16% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2023

To Get more information on Catalyst Regeneration Market - Request Free Sample Report

Catalyst Regeneration Market Trends

-

Increasing demand from refining and petrochemical industries is driving catalyst regeneration adoption, with over 60% of spent catalysts being regenerated to reduce replacement costs.

-

Rising focus on cost optimization is encouraging reuse, as regeneration can lower catalyst expenses by 30–50% compared to fresh catalyst procurement.

-

Stringent environmental regulations are boosting demand, with regeneration reducing hazardous waste generation by up to 70%.

-

Growth in residue upgrading and hydroprocessing units is supporting market expansion, contributing to over 40% of regeneration demand globally.

-

Advancements in on-site and off-site regeneration technologies are improving recovery efficiency, achieving up to 90–95% catalyst activity restoration.

Catalyst Regeneration Market Dynamics

Drivers

-

Growing adoption in petrochemical and chemical industries which drives market growth.

Catalyst regeneration has become a common practice in the petrochemical and chemical industries, where the process relies heavily on catalyst efficiency, thereby driving market growth. The growing need for specialty chemicals, polymers, and refined products is forcing industries to look for effective replacement solutions for their downstream units, while keeping their catalyst performance intact without incurring high replacement costs. Catalysts that can be regenerated are a sustainable solution because they prolong the life of the catalyst, reduce waste, and lower operating costs. Moreover, stringent environmental regulations on waste disposal and emissions are also pushing chemical producers to adopt regeneration activities.

Restraint

-

High initial investment and setup costs may hamper the market growth.

The high capital & operational expenditures and installation costs represent one of the major restraints for catalyst regeneration market growth, owing to catalyst regeneration facilities requiring new infrastructure, refrigeration, and specialized personnel, as well as extensive capital & operational expenditures. There are also financial burdens for companies that need to invest in processing units, emission control devices, and quality testing systems to meet industry standards, particularly for Small and Medium-Sized Enterprises (SMEs). Compliance with regulations also adds to the costs, since environmental and safety standards are often stringent, necessitating a lot of monitoring and upgrades. Such capital expenditure makes it difficult for new players to enter the market and even slows the expansion of current market players restricting the overall growth of the market.

Opportunity

-

Technological advancements in regeneration techniques create an opportunity in the market.

Regeneration techniques are being modernized through technology, and they are becoming the backbone of the catalyst regeneration market by providing efficient, economical turnaround, and a wider range of catalyst types that can be regenerated. Innovations in thermal, chemical, and wet regeneration processes are increasing catalyst contact times, leading to improved activity and selectivity retention of the regenerated catalysts. Moreover, the adoption of artificial intelligence (AI) and automation in regeneration plants are improving process control, and lowering energy consumption and waste. The growing ability to regenerate even high-performance catalysts used in the petrochemical, refining, and chemical industries also fosters the market adoption of advanced regeneration techniques. It is driven by sustainability and cost reduction trends in many industries, these technological advances not only reinforce the environmentally friendly and economically attractive nature of catalyst regeneration but also enhance its sustainability profile relative to fresh catalyst replacement.

Challenges

-

Technological barriers in purification and refining may create a challenge for the market.

Technological barriers can be a major challenge to the Catalyst Regeneration market especially in industries that require high-purity grades for application in pharmaceuticals, specialty chemicals, and high-performance polymers. Common purification techniques are distillation and crystallization; however, they tend to be ineffective at achieving the ultra-high purities required for higher-end applications. Impurities like sulfur compounds and other polycyclic aromatic hydrocarbons (PAHs) are present in the product, affecting product quality and its use in stringent industries. Furthermore, implementing new refining technologies requires very high capital investments against which small and mid-sized manufacturers cannot compete. Stringent quality standards imposed by regulatory authorities require firms to develop advanced purification technologies, leading to higher operating costs and increasing entry barriers for new players entering this market.

Catalyst Regeneration Market Segmentation Analysis

By Type

The off-site regeneration segment held the largest market share around 68% in 2023. It has the ability to provide high-quality regeneration with advanced processing techniques for optimal catalyst performance. The facility located away from manufacturers is outfitted with sophisticated technology, high-level quality control, and specific tools, that improve the durability and performance of recycled catalysts. Industries such as oil refining, petrochemicals, and chemicals, where the catalyst is key to smooth operation, prefer this method. It also does not require any investments in on-site infrastructure as the rare elements are separated in a dedicated facility thus offering companies a competitive advantage in the design of their catalysts towards longer life regimes without on-site compromises in quality. The off-site regeneration segment is projected to further dominate the market due to advantages such as high-scale regeneration capacity, low downtime, & meeting harsh environmental regulations.

By Application

Refineries held the largest market share around 42% in 2023. The catalysts are extensively used in the refining processes including fluid catalytic cracking (FCC), hydrocracking, and hydrotreating. Refineries need continuous catalyst regeneration to achieve processing efficiency, lower operational cost, and comply with stricter economic regulations focused on decreasing emissions and waste generation. The growing global demand for clean fuels and low-sulfur petroleum products has led refiners to use regenerated catalysts to maximize process efficiency and sustainability. As the implementation of circular economy practices worldwide increases, as well as the need to reduce fresh catalyst production, refineries have sought to achieve high performance while saving costs by expanding the use of off-site catalyst regeneration services.

Catalyst Regeneration Market Regional Outlook

Asia Pacific held the largest market share around 42% in 2023. It is owing to the swift development of refining, petrochemical, and chemical industries in this region. The industrial growth in China, India, Japan, and South Korea is likely to contribute to the growth of the market where the market offers countries in the region an increased need to use restored drivers to become more efficient and cost-effective. Stringent emission and waste disposal regulations in the region have further propelled the concept of catalyst regeneration as a sustainable alternative to newly manufactured catalysts. Moreover, the increase in demand for energy, the expansion of refineries on a large scale, and investments in petrochemicals also drive market growth. Asia Pacific is again the market leader due to the presence of the leading catalyst regeneration service provider and the development of regeneration technology. In addition, its cost-effective regeneration services coupled with the availability of skilled manpower and advanced infrastructure act as a hub of catalyst regeneration services.

North America held a significant market share in 2023. It is a highly developed refining, petrochemical, and chemical industry in the region, specifically in the U.S. and Canada. Over the coming years, the demand for regenerated catalysts is expected to rise with a growing emphasis on lowering operational costs, improving sustainability, and complying with stringent environmental regulations in various industries. The market growth is further supported by the presence of various leading refinery operators and petrochemical companies, along with several advanced R&D initiatives related to catalyst regeneration technologies. Finally, government regulation from such agencies as the U.S. Environmental Protection Agency (EPA) and the Canadian Environmental Protection Act (CEPA) has been urging industries to practice some form of regeneration for waste and emission control. Despite continued development in refinery upgrades investments in clean energy projects and the growth of principles walks on the circular economy, North America has remained the leading player in the catalyst regeneration market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key Players

-

Eurecat (RAISE Hydrogenation Catalyst Regeneration, Catalyst Pretreatment Services)

-

CORMETECH (SCR Catalyst Regeneration, Catalyst Management Services)

-

BASF SE (FCC Catalyst Regeneration, Environmental Catalyst Services)

-

Zibo Hengji Chemical Co., Ltd. (Hydroprocessing Catalyst Regeneration, Petrochemical Catalyst Services)

-

Evonik Industries AG (Porocel) (actiCAT Presulfurization Treatment, Activated Alumina Regeneration)

-

Advanced Catalyst Systems LLC (Catalyst Rejuvenation Services, Custom Catalyst Solutions)

-

Al Bilad Catalyst Company (Catalyst Recycling Services, Hydrocracking Catalyst Regeneration)

-

AMETEK, Inc. (Catalyst Regeneration Systems, Process Instrumentation for Catalysts)

-

Axens (Catalyst Regeneration Solutions, Process Licensing Services)

-

EBINGER Katalysatorservice GmbH & Co. KG (Industrial Catalyst Regeneration, Catalyst Handling Services)

-

NIPPON KETJEN Co., Ltd. (Hydroprocessing Catalyst Services, Catalyst Performance Optimization)

-

Yokogawa Corporation of America (Catalyst Performance Monitoring, Process Automation Solutions)

-

Johnson Matthey (Hydroprocessing Catalyst Regeneration, Emission Control Catalyst Services)

-

Haldor Topsoe (AR-401 Activated Nickel Catalyst, Catalyst Management Services)

-

Honeywell UOP (CCR Platforming Catalyst Regeneration, Catalyst Support Services)

-

GlobeCore (Oil Regeneration Units, Transformer Maintenance Equipment)

-

Albemarle Corporation (FCC Catalyst Regeneration, Hydroprocessing Catalyst Services)

-

Porocel (actiCAT Presulfurization Treatment, Activated Alumina Regeneration)

-

Axens (Octanizing Catalyst Regeneration, Process Licensing Services)

-

Engelhard Corporation (BASF) (Magnaforming Catalyst Regeneration, Environmental Catalyst Services)

Recent Development:

-

In March 2024, Evonik introduced Octamax, an advanced sustainable catalyst solution designed to enhance sulfur removal efficiency while preserving octane levels. This cost-effective innovation applies proven hydroprocessing catalyst reuse technology to cracked gasoline hydrodesulfurization units, providing a more sustainable alternative to conventional fresh catalysts.

-

In November 2024, Clariant launched its Plus series syngas catalysts, featuring ReforMax LDP Plus, ShiftMax 217 Plus, and AmoMax 10 Plus. These advanced catalysts are engineered to improve plant efficiency and lower carbon emissions, playing a crucial role in the production of blue hydrogen and green ammonia.

| Report Attributes | Details |

| Market Size in 2023 | USD 5.77 Billion |

| Market Size by 2032 | USD 9.07 Billion |

| CAGR | CAGR of 5.16% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Source (Coal Tar, Petroleum) •By Application (Phthalic Anhydride, Catalyst Regeneration Sulfonates, Low-Volatility Solvents, Moth Repellent, Pesticides, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Eurecat, CORMETECH, BASF SE, Zibo Hengji Chemical Co., Ltd., Evonik Industries AG (Porocel), Advanced Catalyst Systems LLC, Al Bilad Catalyst Company, AMETEK, Inc., Axens, EBINGER Katalysatorservice GmbH & Co. KG, NIPPON KETJEN Co., Ltd., Yokogawa Corporation of America, Johnson Matthey, Haldor Topsoe, Honeywell UOP, GlobeCore, Albemarle Corporation, Porocel, Engelhard Corporation (BASF) |

Frequently Asked Questions

Asia Pacific led the Catalyst Regeneration Market in the region with the highest revenue share in 2023.

Growing adoption in petrochemical and chemical industries which drives market growth.

The Off-site regeneration will grow rapidly in the Catalyst Regeneration Market from 2024-2032.

The expected CAGR of the global Catalyst Regeneration Market during the forecast period is 5.16%

The Catalyst Regeneration Market was valued at USD 5.77 Billion in 2023.

Get in Touch