Fall Protection Market Report Scope & Overview:

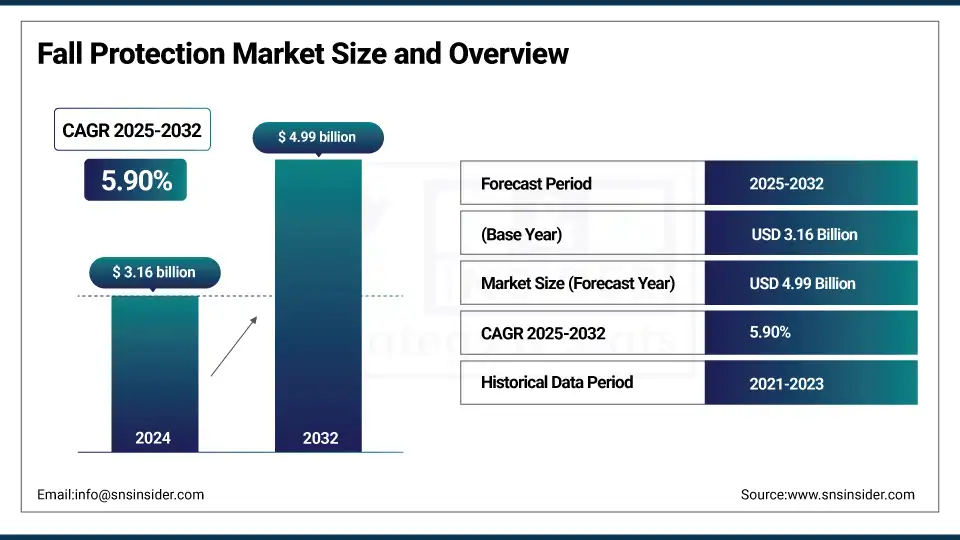

The Fall Protection Market size was valued at USD 3.16 billion in 2024 and is expected to reach USD 4.99 billion by 2032, growing at a CAGR of 5.90% over the forecast period of 2025-2032.

The global fall protection market has become a growing concern for many while maintaining worker safety and ensuring that they are not being exposed to inadequate occupational safety, which is also being strictly regulated by the respective authorities of the industries/organizations. Fall protection systems are crucial systems used for reducing one or more risks facing workers when in a high position, and they are a vital safety system in construction, manufacturing, oil & gas, mining, transportation, and utility sectors. The offerings comprise safety harnesses, lanyards, self-retracting lifelines, guardrails, and anchorage systems, to name a few. Moreover, rising penetration of technology, including the development of smart harnesses with sensors for real-time monitoring of the horse-dog relation, and automatic pedestrian fall detection systems, is changing the overall market environment.

To Get more information On Fall Protection Market - Request Free Sample Report

Growing awareness about workplace risks, along with an increase in the number of fall accidents globally, which continue to be one of the leading causes of occupational injuries and deaths, has reasserted the need for fall protection equipment. The industry is now seeking effective solutions that ensure comfort and compliance while delivering a benefit for greater safety and productivity. In addition, the setting of PPE (personal protective equipment) standards by OSHA and ANSI has stimulated new advances in fall protection products and solutions. Ongoing innovation in products, along with training services and integrated safety solutions, is a key strategy in the fall management industry.

In May 2025, OSHA organized the National Safety Stand-Down to Prevent Falls in Construction from May 5–9, urging employers to pause work for safety talks, training, and equipment checks to prevent fall-related accidents. Falls remained the leading cause of construction deaths, with 421 fatalities in 2023. The campaign, supported by NSC and CPWR, provided free resources, webinars, and safety tips.

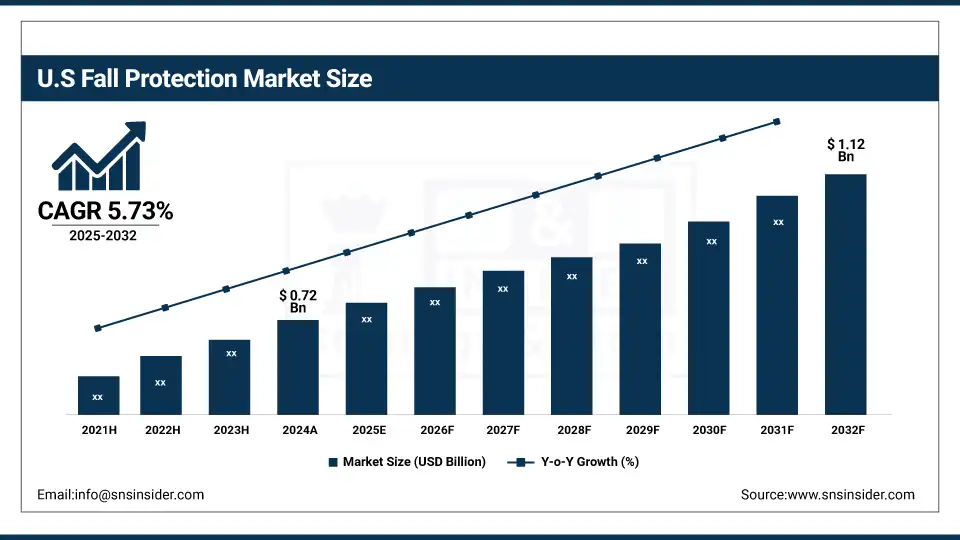

The U.S. dominates the North American fall protection market, valued at USD 0.72 billion in 2024 and projected to reach USD 1.12 billion by 2032, growing at a 5.73% CAGR. This growth is driven by strict workplace safety regulations, rising construction and industrial activities, and increasing adoption of advanced fall protection systems.

Fall Protection Market Dynamics:

Drivers

-

Stringent Safety Regulations and Compliance Mandates Fuel Growth in the Industrial Fall Protection Market.

Stringent safety regulations and compliance standards are major driving forces in the industrial fall protection market. Regulating bodies like OSHA (Occupational Safety and Health Administration) in the U.S., HSE (Health and Safety Executive) in the UK, and various similar organizations in Europe and Asia require fall protection for industry, and have similar mandates in construction, oil & gas, mining, and manufacturing. This kind of mandate, in turn, is forcing organisations into making heavy investments in advanced fall protection systems to avoid penalties and operational disruptions. Industry reports estimate that around 40% of all workplace accidents at international levels are fatalities as a result of falling from a height, and therefore, safety gear is essential. Rise in the implementation of workplace safety audits and legal inspections has indirect further commercialized safety compliance, which has prompted enterprises to adopt industrial fall protection solutions on a proactive basis. As companies worldwide recognize compliance with this new regulatory environment as a strategic imperative, the growth of the Fall Protection Industry is steadily on the rise.

In June 2025, WorkSafe Victoria reported ongoing enforcement against fall protection violations, issuing 18 criminal prosecutions, 21 notices, and fines exceeding AUD 1.65 million. Falls from heights remain a major safety concern, particularly in the construction and solar installation sectors. The agency urges employers to improve supervision, safety systems, and the proper use of fall protection equipment to prevent workplace injuries.

Restraint

-

High Upfront and Maintenance Costs Pose Challenges for SMEs In Fall Protection Adoption

High upfront costs remain a major restraint in the fall protection market, particularly for small and medium-sized enterprises (SMEs). Smart harnesses, self-retracting lifelines, and permanent anchor points make up advanced fall protection systems, which can cost between hundreds of dollars to thousands of dollars per unit, driving up the initial investment needed for many small businesses. Along with the first purchase, companies also must take on continuing costs for routine maintenance, scheduled inspections, recertification, and at times, the calibration of equipment to retain safety compliance. For example, in North America and Europe, the law mandates the annual inspection of your fall protection equipment and assesses heavy fines for failure to comply. According to various studies, inspection and maintenance expenses can make up to 20–30% of the lifecycle costs related to fall protection networks. Such financial pressure leads to what we know as SMEs not willing to move towards any kind of upgrade or to implement a complete fall protection solution, which is more likely of the case with high capital requirements witnessed especially in the cost-sensitive industries such as construction and small-scale manufacturing.

Fall Protection Market Segmentation Analysis:

By Type

The individual protection segment dominated the market and accounted for 59% of the fall protection market share. This growth is primarily attributed to the rising demand for personal fall protective equipment like full-body harnesses, lanyards, and self-retracting lifelines in a range of industries. They provide increased safety for workers, greater adaptability, and are required by some of the most stringent occupational safety regulations in the world. Those systems are particularly critical for higher-risk work at heights for industries that do a lot of work there, like construction, oil & gas, and utilities. The rising awareness among workers about personal safety and also stringent adherence to compliance standards by regulatory bodies is expected to uplift the demand globally for individual fall protection equipment as well.

The collective protection segment is expected to witness the fastest growth in the fall protection market during the forecast period. This section comprises devices, for example, guardrails, safety nets, and barricades, which protect multiple workers simultaneously. The increasing adoption of fall mitigation measures (especially in mini-industrial and commercial construction projects) has sped up the requirements for these systems. Prino also noted, however, that collective protection solutions are becoming preferred as they help reduce human error detected in personal fall protection equipment. This, coupled with rising government initiatives promoting safe workplaces, particularly in developing economies, and innovations in modular and easy-to-install systems, is further accelerating the growth of the segment.

By End-Use

The construction sector remains the dominant end-use segment in the fall protection market, contributing to 32% of the total share in 2024. Falls remain one of the highest risks for construction workers, meaning fall protection systems are not optional. Construction site safety measures are heavily mandated by regulatory authorities and governments across the globe, driving high demand for fall protection equipment in this sector. In addition, the continued boom in home, commercial, and infrastructure work in developing and developed nations boosts the requirement for strong safety systems. Growth in urbanization, rising investments in infrastructure, and construction worker safety training programs continue to play a key role in sustaining fall protection equipment demand in the construction sector.

The manufacturing segment is anticipated to be the fastest-growing in the fall protection market over the coming years. The reason for this growth mainly relates to the automation of manufacturing plants, which includes elevated platforms, machines, and other high structures, highlighting the added risk of falls. Automotive, aerospace, chemicals, food processing, and many other industry sectors that have high investment in safety systems so as to avoid accidents and rightfully meet the advanced occupational health and safety regulations. Also, the integration with Internet of Things (IoT) and sensor-based smart fall protection systems in manufacturing environments is increasingly being adopted to provide a better safety solution, which may eventually accelerate the growth of the fall protection solution market.

Fall Protection Market Regional Outlook:

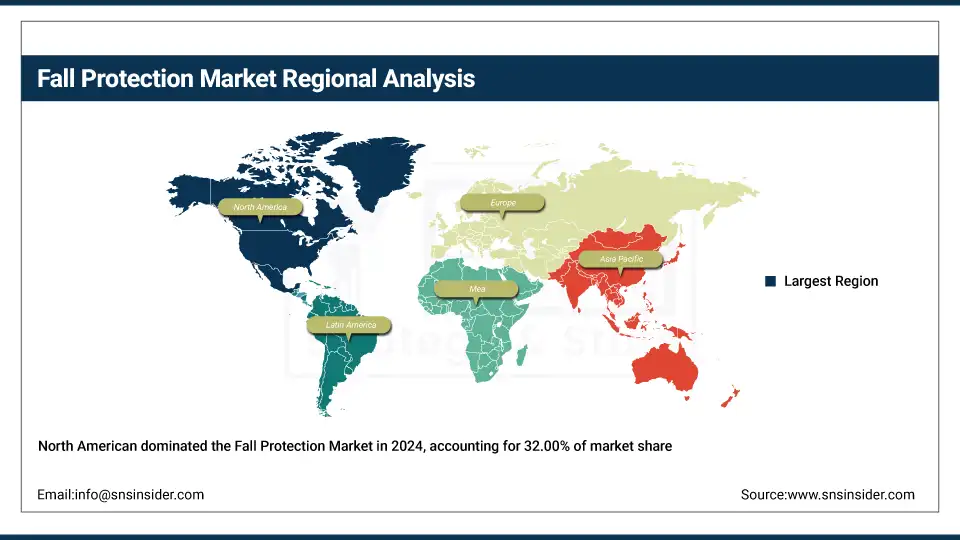

North America dominated the fall protection market, accounting for a 32.00% share in 2024. This is largely due to the stringent workplace safety regulations by agencies like OSHA (Occupational Safety and Health Administration) in the U.S. and CCOHS in Canada, which make this region a leader in safety. As the construction, oil & gas, and utilities sectors continue to grow, the need for superior fall protection systems, such as harnesses, lifelines, and guardrails, is also on the rise. Furthermore, a rise in the use of sophisticated personal protective equipment (PPEs) in industries such as manufacturing, telecommunications, etc., is expected to bolster the regional market. North America has the largest share in the fall protection market due to the presence of key market players and continuous advancements and innovations in technology.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe holds a significant share of the global fall protection market due to its strong regulatory framework and robust industrial base. Various organizations, including the European Agency for Safety and Health at Work (EU-OSHA), have also developed stringent safety regulations across industries, including construction, utilities, and mining. Strengthening demand for fall protection systems, including safety nets, guardrails, and personal protective equipment across the region is attributed to the emphasis on worker safety and expanding investments in infrastructure modernization projects. Moreover, increasing awareness of workplace safety and advancements in technologies of fall protection products are further contributing to the market growth. Germany, France, and the UK are particularly responsible for upholding Europe’s significant share of the market.

Germany is the dominant country in the European fall protection market. Its leadership is driven by strict occupational safety laws, a strong industrial base, and significant construction activities. Germany’s focus on worker safety, coupled with the widespread adoption of advanced fall protection systems in sectors like manufacturing, automotive, and infrastructure, positions it as the leading market within Europe.

Asia-Pacific is emerging as the fastest-growing region in the fall protection market, driven by rapid industrialization and infrastructure development. Since construction, manufacturing, and energy projects are rising in nations like China, India, Japan, and Australia, the need for safety systems for workers increases. Moreover, rising government initiatives for increasing the safety standards at the workplace and increasing foreign investment in industrial projects are further propelling the growth of the market for fall protection equipment. Escalating awareness about worker safety and the requirement to comply with international safety standards are some other factors driving market growth in the region. This, along with the rising penetration of global safety equipment players in the Asia-Pacific region, is fueling the market growth.

Key Players in the Fall Protection Market:

Fall protection companies are Honeywell International Inc., 3M, MSA, Guardian Fall, Petzl, WernerCo, FallTech, SKYLOTEC, Kee Safety Inc., Gravitec Systems, Inc.

Recent Development:

-

In January 2024, WernerCo launched a new fall protection utility lifeline designed for utility workers and linemen. The system features an anchor strap fall arrest mechanism to enhance climbing safety on utility poles. This product highlights WernerCo’s focus on specialized safety solutions for high-risk industries.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 3.16 Billion |

| Market Size by 2032 | USD 4.92 Billion |

| CAGR | CAGR of 5.90% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Individual Protection, Collective Protection, Access Equipment) • By End-use (Construction, Manufacturing, Oil & Gas, Chemicals, Food, Pharmaceuticals, Healthcare, Transportation, Mining, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Honeywell International Inc., 3M, MSA, Guardian Fall, Petzl, WernerCo, FallTech, SKYLOTEC, Kee Safety Inc, Gravitec Systems, Inc. |

Frequently Asked Questions

The North America region dominated the Fall Protection Market in 2024.

The “individual protection” segment dominated the Fall Protection Market.

Stringent Safety Regulations and Compliance Mandates Fuel Growth in the Industrial Fall Protection Market.

The Fall Protection Market was USD 3.16 billion in 2024 and is expected to reach USD 4.99 billion by 2032.

The Fall Protection Market is expected to grow at a CAGR of 5.90% from 2025-2032.

Get in Touch