Hydrogen Pipeline Market Report Scope & Overview

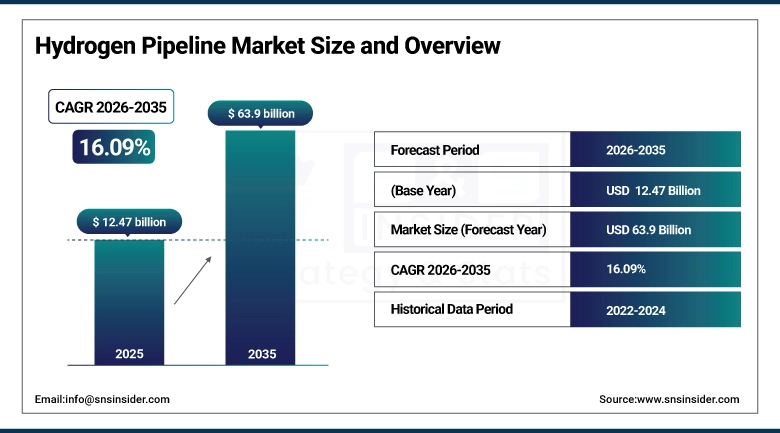

The Hydrogen Pipeline Market was valued at USD 12.47 billion in 2025 and is expected to reach USD 63.9 billion by 2035, growing at a CAGR of 16.09% from 2026–2035.

The Hydrogen Pipeline Market is expanding owing to the growing emphasis on the decarbonization process and the shift towards clean energy. Investments made by governments for producing green or blue hydrogen, and development of hydrogen-related infrastructure are contributing towards an increase in demand for efficient hydrogen transport infrastructure. Growing use of hydrogen in various industries for applications such as refining, electricity generation, and production of chemicals is propelling the market growth further. Also, creation of hydrogen clusters, international energy cooperation, and advancements in technology are aiding rapid market growth.

The blending of hydrogen into existing natural gas pipelines at 5-20% concentrations is an intermediate strategy being deployed in several countries to utilize existing infrastructure while the hydrogen economy develops. This approach is already operating in Australia, Germany, and the UK, providing practical experience with hydrogen pipeline materials and operational challenges.

Market Size and Forecast

-

Market Size in 2025: USD 12.47 Billion

-

Market Size by 2035: USD 63.9 Billion

-

CAGR: 16.09% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Hydrogen Pipeline Market - Request Free Sample Report

Hydrogen Pipeline Market Trends

-

Growing national hydrogen strategies from the EU, U.S., Japan, Korea, Australia, and China are funding massive pipeline infrastructure programs.

-

Repurposing of existing natural gas pipelines to carry hydrogen is reducing capital costs and accelerating deployment timelines.

-

AI-based leak detection and smart monitoring systems are being integrated into hydrogen pipeline operations to improve safety.

-

Green hydrogen production cost reductions driven by falling electrolyzer costs are making dedicated pipeline transport economics increasingly viable.

-

Offshore hydrogen production coupled with subsea pipeline connections is being evaluated for long-distance transport from production to demand centers.

-

Safety standards and material specifications for hydrogen service are being developed and harmonized across major markets.

-

Hydrogen blending programs in natural gas distribution networks are providing operational experience ahead of full hydrogen conversion.

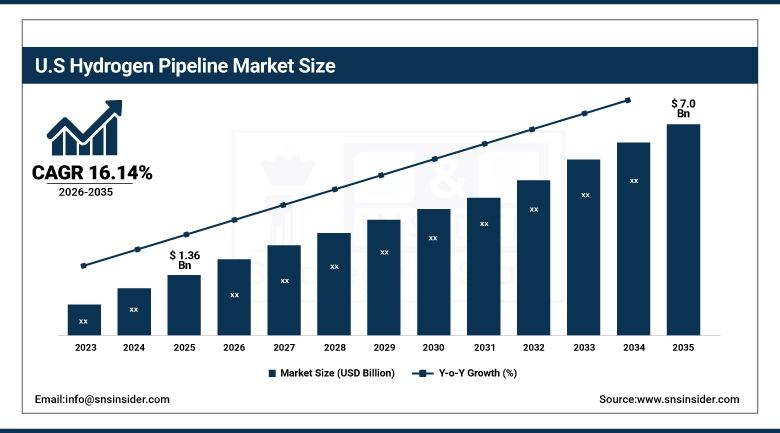

U.S. Hydrogen Pipeline Market was valued at USD 1.36 billion in 2025 and is expected to reach USD 7.0 billion by 2035, at a CAGR of 16.14% from 2026 to 2035.

The U.S. Hydrogen Pipeline Market is experiencing rapid growth due to significant government backing towards initiatives for clean hydrogen, increased investment in green and blue hydrogen generation, and increasing demands for decarbonization in industries. Growth in hydrogen hubs, energy transitions, and developments in pipeline systems are also contributing to accelerated growth in the market.

The U.S. Department of Energy's National Hydrogen Strategy targets 10 million metric tonnes of clean hydrogen production per year by 2030 and 50 million by 2050, all of which will require extensive pipeline infrastructure to move from production sites to end users. This creates a long-term structural demand for pipeline construction that extends well beyond the 2035 forecast period.

Hydrogen Pipeline Market Segment Analysis

-

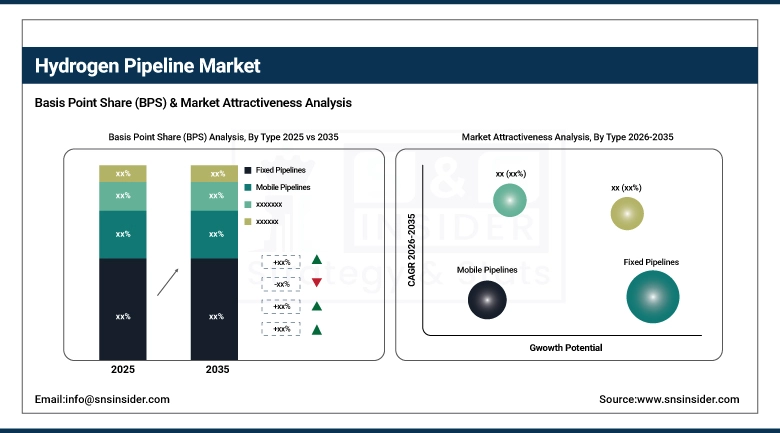

By Type, Fixed Pipelines segment dominated the Hydrogen Pipeline Market in 2025 with 72% share; Mobile Pipelines segment fastest growing (CAGR).

-

By Distance, More than 300 Km segment dominated the Hydrogen Pipeline Market in 2025 with 64% share; Upto 300 Km segment fastest growing (CAGR).

-

By Hydrogen, Gas segment dominated the Hydrogen Pipeline Market in 2025 with 81% share; Liquid segment fastest growing (CAGR).

-

By Pipeline Structure, Metal segment dominated the Hydrogen Pipeline Market in 2025 with 67% share; Plastics & Composites segment fastest growing (CAGR).

By Type, Fixed Pipelines segment dominates the Hydrogen Pipeline Market, Mobile Pipelines segment expected to grow fastest

Fixed Pipelines segment dominated the Hydrogen Pipeline Market in 2025 due to their widespread use for long-distance transportation through large hydrogen transportation systems. They have proven to be quite reliable, safe, and cost-effective for the constant transportation of hydrogen from manufacturing to distribution facilities. Heavy investments in the hydrogen economy, decarbonization plans, and well-established pipeline systems have contributed to the strong dominance of fixed pipelines globally.

Mobile Pipelines are the fastest-growing segments in the hydrogen pipeline market due to growing requirements for flexible hydrogen transportation options in areas where there are no grids or inadequate infrastructures for the delivery of hydrogen. Their use has helped facilitate the process of setting up hydrogen refueling stations and experimental projects. Growth in this segment has been fueled by growing initiatives related to green hydrogen and renewable energy.

By Distance, More than 300 Km segment dominates the Hydrogen Pipeline Market, Up to 300 Km segment expected to grow fastest

More than 300 Km segment dominated the Hydrogen Pipeline Market in 2025, owing to increasing demand for long-distance transportation of hydrogen from production sites to industrial consumption centers. Long-distance hydrogen pipelines facilitate the movement of energy over distances across regions to ensure adequate supply at refineries, chemical plants, and power generation units. Growth in export-import infrastructure for hydrogen and trans-boundary energy initiatives has played a key role in this market segment's domination.

Upto 300 Km was the fastest-growing segment, driven by an increase in the construction of hydrogen hubs and regional distribution networks. Short-distance pipelines are primarily installed for transporting hydrogen from production facilities to nearby industrial consumers and fueling stations. Increased interest in building local hydrogen economies, rising demand for hydrogen supply in industrial applications, and rapid adoption of green hydrogen initiatives have been major drivers of this segment's growth.

By Hydrogen, Gas segment dominates the Hydrogen Pipeline Market, Liquid segment expected to grow fastest

Gas segment dominated in the Hydrogen Pipeline Market in 2025 owing to their extensive use in industrial applications along with ease in transportation using pipelines. The gases have been extensively used in refining, manufacturing chemicals, and energy industries since they can be effectively handled along with having low liquefaction cost. High demands from all around the world and the existence of natural gas networks help sustain the leading position of gases in the market.

The Liquid segment is the fastest growing segment due to rising demand for dense hydrogen and better ways of transporting it over large distances. The liquid form of hydrogen provides greater density and therefore is applicable in aerospace, logistics, and energy industries. The rising investments in liquefaction technologies, the development of hydrogen export terminals, and increased focus on renewable energy logistics drive the market towards higher growth rates.

By Pipeline Structure, Metal segment dominates the Hydrogen Pipeline Market, Plastics & Composites segment expected to grow fastest

Metal segment led the Hydrogen Pipeline market in 2025 owing to its greater strength, longevity, and capability to sustain high-pressure hydrogen transportation. The steel pipelines are widely employed in existing hydrogen pipelines and natural gas pipeline infrastructure, making them reliable and long-lasting. The widespread usage, network, and suitability of metals to facilitate large-scale hydrogen transport have contributed to their dominance in hydrogen pipelines.

Plastics & Composites segment is the fastest-growing owing to increased demand for corrosion-resistant, lightweight, and pliant pipelines. These products minimize hydrogen leakage problems and are ideal for low-to-moderate hydrogen transport pressure in new hydrogen infrastructure. Innovations in composites technology, rise in green hydrogen projects, and requirement for cost-effective pipeline installation have fueled the growth of the plastics & composites segment in hydrogen pipelines.

Hydrogen Pipeline Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

79% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

Japan |

32% |

|

Middle East & Africa |

Saudi Arabia |

45% |

|

Latin America |

Chile |

52% |

Europe Hydrogen Pipeline Market Insights

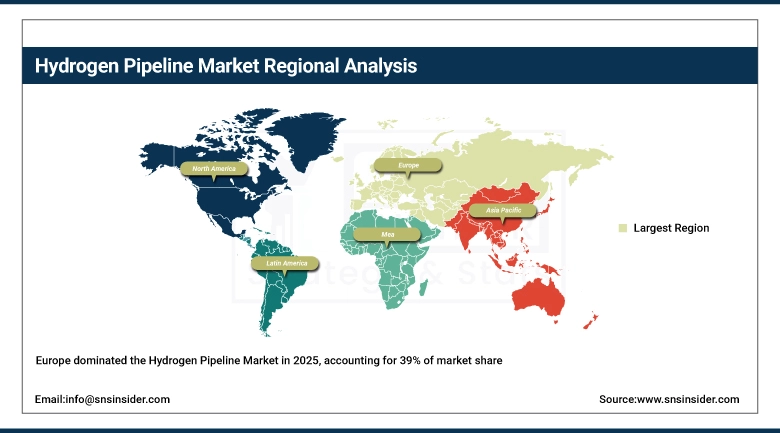

In 2025, Europe accounted for around 39% of the worldwide Hydrogen Pipeline Market share owing to favorable government policies and stringent goals on decarbonization. The European market is focusing significantly on hydrogen pipeline construction, cross-border pipelines, and hydrogen corridor development in industries. Germany, Netherlands, and France are among those countries that are involved in large-scale hydrogen corridor development projects. The presence of major engineering firms, advanced energy infrastructure, and higher renewable energy penetration are contributing toward the dominance of Europe in the hydrogen pipeline market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Hydrogen Pipeline Market Insights

The Asia Pacific region will witness robust growth in the Hydrogen Pipeline Market owing to growing investment in energy transition and industrialization. Growing government activities to support the manufacture of green hydrogen in nations such as China, Japan, South Korea, and India are contributing to infrastructure development. The growing installation of renewable energy sources and demand for eco-friendly fuels are propelling the installation of pipelines. Moreover, the emphasis on energy security and cross-border hydrogen transport and the development of industrial hydrogen clusters is further fostering the growth of the market in the region.

North America Hydrogen Pipeline Market Insights

The North America Hydrogen Pipeline Market is witnessing significant growth because of rising investment in hydrogen-related infrastructure, along with growing governmental initiatives in favor of decarbonization strategies. Growing attention towards reduction in carbon footprint within industries like oil & gas, electricity, and transportation sector is adding to the growth of the pipeline market. Increasing number of hydrogen projects, especially the adoption of green & blue hydrogen production technology, and building up of hydrogen hubs is adding fuel to the fire.

Middle East & Africa and Latin America Hydrogen Pipeline Market Insights

The Hydrogen Pipeline Market in the Middle East & Africa and Latin America is expanding at a steady pace because of the rising investments in the development of green hydrogen plants and renewable energy installations. The abundant presence of solar and wind power sources is enabling the establishment of hydrogen generation facilities on a massive scale in these regions. The authorities have prioritized diversification of their energy sources along with reducing their reliance on traditional fossil fuels, which has encouraged infrastructural development.

Hydrogen Pipeline Market Insights Growth Drivers

-

Expanding industrial adoption of hydrogen in refining, ammonia production, and heavy manufacturing sectors boosting long-distance pipeline transportation demand

Increased consumption of hydrogen by industries in refining crude oil, producing ammonia, producing steel, and chemicals are important factors responsible for the establishment of pipelines for hydrogen. The trend within industries today has been towards switching to low-carbon hydrogen in order to cut down on emission levels, among others. Huge quantities of hydrogen need to be transported from the point of its production to end-user industries through effective methods. Pipelines present the most cost-effective means of transporting large volumes of hydrogen over long distances than road and rail routes.

Hydrogen Pipeline Market Insights Restraints

-

High infrastructure development costs and technical challenges in hydrogen storage and transportation limiting large-scale pipeline deployment

The need for high initial investment in the creation of the hydrogen pipeline network is one of the significant impediments to the growth of the market. Hydrogen needs special equipment as well as advanced engineering solutions owing to its small molecule size and ability to make metals brittle. The existing natural gas pipelines may require substantial changes or even replacement to enable hydrogen transportation, thus raising costs. Moreover, difficulties with hydrogen storage and compression lead to increased costs. Lack of standard technologies in hydrogen pipeline construction and immaturity of infrastructure in various countries hinder the development of hydrogen pipelines.

Hydrogen Pipeline Market Insights Opportunities

-

Increasing investments in green hydrogen projects and government-backed energy transition programs creating strong opportunities for pipeline infrastructure expansion

The fast growth of green hydrogen production initiatives backed by government subsidies is leading to many business opportunities for hydrogen pipelines. Nations are making huge investments in developing hydrogen corridors, hydrogen terminals for export/import of hydrogen energy, and energy transmission systems that cross international borders for distribution purposes. In fact, hydrogen pipelines are becoming necessary for the connection between production centers and industrial centers where hydrogen will be used. With more hydrogen production from renewable energy sources, there is also the need for more energy infrastructure development. All these are presenting business opportunities for investment in hydrogen pipelines.

Recent Developments

-

2025: The European Hydrogen Backbone consortium announced a detailed technical assessment confirming the feasibility of converting over 10,000 km of existing natural gas pipelines to hydrogen service in Germany, France, and the Netherlands, significantly reducing the capital cost of the European hydrogen grid.

-

2024: Air Liquide and TotalEnergies announced the construction of a new 200 km dedicated hydrogen pipeline in France connecting industrial hydrogen producers in the Seine Valley to major industrial consumers, representing one of the largest new hydrogen pipeline projects in Western Europe.

-

2023: The U.S. Department of Energy announced 7 Regional Clean Hydrogen Hubs receiving a combined USD 7 billion in funding, including pipeline infrastructure connecting hydrogen production and distribution across diverse U.S. regions.

Hydrogen Pipeline Market Key Players

-

Cenergy Holdings

-

Salzgitter AG

-

Gruppo Sarplast S.r.l

-

Tenaris

-

Hexagon Purus

-

Pipelife International GmbH

-

Europe Technologies

-

H2 Clipper, Inc.

-

NPROXX

-

GF Piping Systems

-

ArcelorMittal

-

Jindal Saw Limited

-

Tata Steel

-

Liberty Steel Group

-

ILJIN Steel

-

Butting Group

-

Welspun Corp

-

Tubacex Group

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.47 Billion |

| Market Size by 2035 | USD 63.9 Billion |

| CAGR | CAGR of 16.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Mobile Pipelines, Fixed Pipelines) • By Distance (Upto 300 Km, More than 300 Km) • By Hydrogen (Gas, Liquid) • By Pipeline Structure (Metal, Plastics & Composites) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cenergy Holdings, SoluForce B.V., Salzgitter AG, Gruppo Sarplast S.r.l, Tenaris, Hexagon Purus, Pipelife International GmbH, Europe Technologies, H2 Clipper, Inc., NPROXX, GF Piping Systems, ArcelorMittal, Jindal Saw Limited, Vallourec, Tata Steel, Liberty Steel Group, ILJIN Steel, Butting Group, Welspun Corp, Tubacex Group. |

Frequently Asked Questions

Global decarbonization targets requiring clean hydrogen for hard-to-abate industrial sectors, supported by substantial government funding programs.

Europe leads due to the EU's ambitious hydrogen strategy and the European Hydrogen Backbone initiative planning 53,000 km of hydrogen pipelines.

Fixed Pipelines dominate as the primary dedicated infrastructure for transporting hydrogen from production to industrial end-users.

The Hydrogen Pipeline Market was valued at USD 12.47 billion in 2025.

The Hydrogen Pipeline Market is expected to grow at a CAGR of 16.09% from 2026 to 2035.

Get in Touch