Cranial Implants Market Report Scope & Overview:

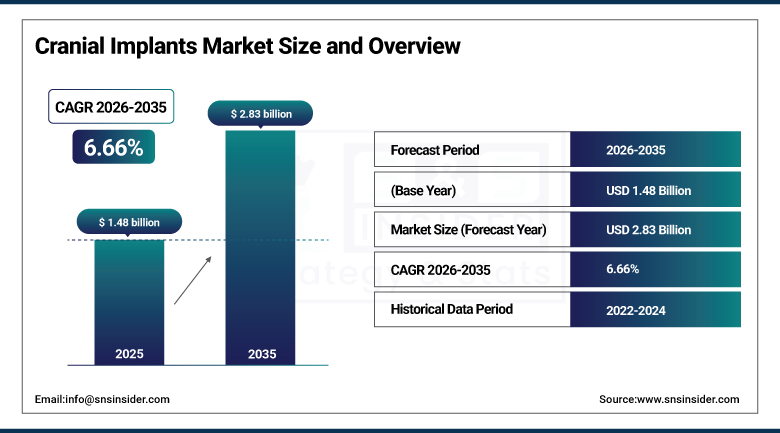

The Cranial Implants Market was estimated at USD 1.48 Billion in 2025 and is expected to reach USD 2.83 Billion by 2035, growing at a CAGR of 6.66% over the forecast period of 2026–2035.

Cranial Implants Market is described as the part of the medical devices industry sector focused on designing, producing, and clinical use of prosthetics that help restore, reconstruct or replace parts of the skull after injuries of the brain, operations involving the removal of tumors, congenital abnormalities in the skull bone structure, and cranioplasty surgeries, which help restore the normal state of the skull, protect its internal organs, and ensure their physiological functioning. Cranial implants play a significant role in clinical practice as they help restore skull structures after craniectomy and craniotomy injuries, provide mechanical protection for the brain from external shocks, establish the intracranial pressure balance necessary for cerebrospinal fluid flow, and achieve a cosmetically successful result for patients.

The structural growth dynamics of the Cranial Implants Market are anchored by the global road traffic accidents, falls, sports-related head injuries, and interpersonal violence collectively generate millions of annual TBI cases requiring neurosurgical intervention, a substantial proportion of which involve craniectomy procedures that subsequently require cranioplasty with cranial implants. The increasing global incidence of primary brain tumors, with an estimated 308,102 people diagnosed annually with primary brain or spinal cord tumors according to the World Health Organization, creates additional demand for cranial reconstruction following tumor resection surgeries that require removal of skull sections overlying the surgical site. The aging global population is also contributing to market growth through elevated incidence rates of cerebrovascular events including stroke and subdural hemorrhage that require decompressive craniectomy followed by cranioplasty.

Market Size and Forecast:

- Market Size in 2025: USD 1.48 Billion

- Market Size by 2035: USD 2.83 Billion

- CAGR: 6.66% from 2026 to 2035

- Base Year: 2025

- Forecast Period: 2026–2035

- Historical Data: 2022–2024

To Get more information on Cranial Implants Market - Request Free Sample Report

Cranial Implants Market Trends:

- Accelerating clinical adoption of patient-specific cranial implants manufactured using 3D printing technologies from CT scan-derived digital anatomical models is transforming surgical outcomes by delivering sub-millimeter anatomical precision fit, reducing intraoperative adjustment time, and achieving cosmetically superior reconstruction results compared to standardized prefabricated implant approaches, with adoption expanding beyond tertiary academic medical centers into a broader range of neurosurgical practice settings.

- Growing utilization of PEEK (polyether ether ketone) as the dominant polymer material for cranial implants reflects its unique combination of biocompatibility, chemical inertness, radiolucency enabling unobstructed post-operative CT and MRI imaging, and mechanical properties that closely approximate cortical bone, providing both clinical functionality and diagnostic imaging transparency that titanium cannot match.

- Increasing integration of digital surgical planning software, augmented reality intraoperative navigation, and virtual surgical simulation into cranial reconstruction workflows is improving the accuracy of implant positioning, reducing surgical time, and enabling less-experienced surgeons to achieve outcomes approaching those of high-volume neurosurgical specialists, expanding the addressable patient population for advanced cranial reconstruction procedures.

- Rising investment in bioactive and osteoconductive ceramic cranial implant materials including hydroxyapatite and calcium phosphate composites that promote bone cell infiltration and long-term osseointegration is creating a new generation of biologically active implants that actively participate in skeletal healing rather than functioning as purely passive mechanical substitutes, potentially offering superior long-term stability and reduced revision surgery rates.

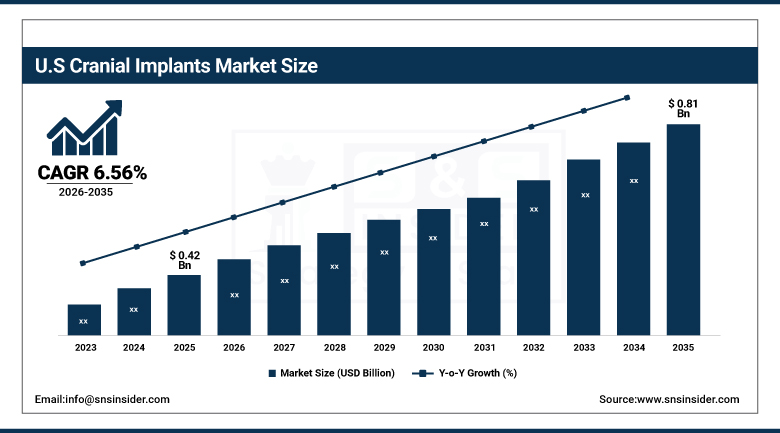

U.S. Cranial Implants Market was valued at USD 0.42 Billion in 2025 and is expected to reach USD 0.81 Billion by 2035, growing at a CAGR of 6.56%.

The United States represents the dominant national market within North America, supported by the world highest neurosurgical procedure volume, a well-established reimbursement framework for cranial reconstruction surgeries under Medicare and commercial insurance programs, and the concentrated presence of leading cranial implant manufacturers including Stryker Corporation, Integra LifeSciences, DePuy Synthes (Johnson & Johnson), and KLS Martin Group that collectively represent the global technology leaders in patient-specific and standardized cranial implant systems. The U.S. market benefits from high adoption of advanced 3D-printed patient-specific implant technologies by the country network of academic medical centers and Level I trauma centers that manage the highest-acuity cranial trauma and tumor resection cases requiring sophisticated reconstruction solutions. In April 2024, 3D Systems obtained FDA clearance for its EXT 220 MED printer using medical-grade PEEK materials for 3D-printed cranial reconstruction, and in May 2024, researchers from USC and Caltech successfully implanted a transparent cranial window in a patient for high-resolution functional ultrasound brain imaging, exemplifying the continued innovation leadership of the U.S. cranial implant market.

Cranial Implants Market Segment Insights:

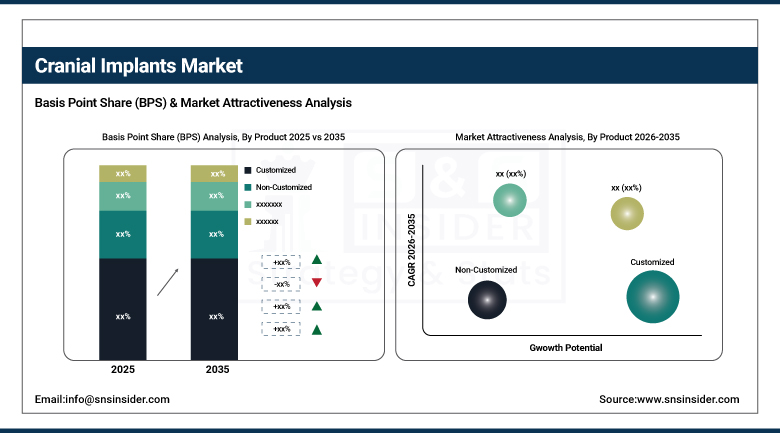

- By Product, Customized implants dominated the Cranial Implants Market in 2025; Non-Customized is expected to be the fastest-growing product segment during the forecast period.

- By Material, Polymer dominated with approximately 54.03% revenue share in 2025; Ceramic is expected to be the fastest-growing material segment during the forecast period.

- By End-User, Hospitals dominated with approximately 78.5% of Cranial Implants Market revenues in 2025; Neurosurgery Centers represent the growing secondary segment.

Cranial Implants Market Segment Analysis:

By Product: Customized dominates, Non-Customized fastest-growing

Customized cranial implants were leading the product segment in 2025 due to increasing medical understanding that personalized implants, based on individual anatomy obtained via patient CT scans, provide better surgery results across a number of indicators than pre-fabricated standard alternatives. Customized implants include fully personalized implants made using 3D printing technology from polymers, titanium, and ceramics according to individual digital anatomies as well as semi-personalized implants which are made according to standardized sizes but then individually finished or adjusted to fit the patient’s defect anatomy. Customized implants occupy a higher pricing position on the market and become more justified through health economics analysis due to a number of improvements in surgery results, including shorter surgery duration, minimal implant adjustments needed during surgery, better fitting of defects, better cosmetic results, and decreased risks of infections and need for revisions.

The Non-Customized segment is anticipated to register the fastest CAGR during the forecast period, driven by expanding utilization in emergency trauma settings and emerging market healthcare systems where the rapid availability, lower cost, and simplified surgical workflow of standardized prefabricated titanium mesh, plates, and PEEK sheet products make them the practical first-line option for cranial reconstruction in resource-constrained environments. Non-customized implants remain the standard of care in many developing healthcare markets where advanced digital design and 3D printing services are not readily accessible, and they continue to serve important clinical roles in urgent cranioplasty procedures where patient-specific manufacturing turnaround time is not compatible with clinical timelines.

By Material: Polymer dominates, Ceramic fastest-growing

Polymer-based implants, mainly comprising PEEK-based materials, have led the market for Cranial Implants with 54.03% of market share by 2025, owing to the long-time proven clinical superiority of PEEK as a material for both customized and prefabricated cranial implants in cranioplasty as well as anterior skull base reconstruction surgery. The popularity of PEEK can be attributed to its exceptional characteristics of biocompatibility backed up by decades of use in clinical application, radiolucency that allows for clear imaging after the operation without any disturbance caused by metal artifacts, mechanical properties close to cortical bones in terms of Young modulus, which prevents stress shielding of the surrounding bone tissue, and low density resulting in comfort for the patient. PEEK offers flexibility regarding production methods from CNC machining of customized implants made of porous PEEK to injection molding of standardized implants.

The Metal implants category consists of metallic components mainly based on titanium and its alloys and constitutes a substantial share in the secondary materials market owing to their proven biocompatibility history, high tensile strength, and predictable clinical outcomes through years of neurosurgical applications. The category of titanium mesh-based implants holds significance in the non-customizable category because of their high formability and availability. In terms of CAGR, the Ceramic segment would show the maximum growth rate due to rising research activities on active bone formation ceramics such as hydroxyapatite, tricalcium phosphate, and ceramic composites.

By End-User: Hospitals dominate, Neurosurgery Centers growing

Hospitals dominated the Cranial Implants Market with approximately 78.5% revenue share in 2025, reflecting the concentration of cranial implant procedures in hospital settings that provide the full spectrum of neurosurgical infrastructure including operating suites with intraoperative neuroimaging and navigation systems, intensive care unit support for post-operative management of brain-injured patients, interdisciplinary care teams encompassing neurosurgeons, neurologists, anesthesiologists, and rehabilitation specialists, and the emergency department capabilities required to triage and manage acute traumatic brain injury cases requiring urgent craniectomy. The hospital segment dominance is also reinforced by reimbursement structures that bundle cranial implant costs within inpatient surgical episode payments.

Neurosurgery Centers, encompassing standalone outpatient neurosurgical facilities and ambulatory surgical centers with neurosurgical specialization, represent the growing secondary end-user segment as improvements in minimally invasive surgical techniques, advanced anesthesia, and enhanced recovery protocols enable an increasing proportion of elective cranioplasty procedures to be performed in outpatient or short-stay settings outside traditional inpatient hospital environments. The shift toward ambulatory neurosurgery reduces healthcare system costs while maintaining clinical outcomes for carefully selected patients, creating growth opportunities for cranial implant utilization in the Neurosurgery Centers segment.

Regional Insights:

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~79% |

|

Europe |

Germany |

~28% |

|

Asia Pacific |

China |

~42% |

|

Middle East & Africa |

UAE |

~24% |

|

Latin America |

Brazil |

~39% |

North America Cranial Implants Market Insights

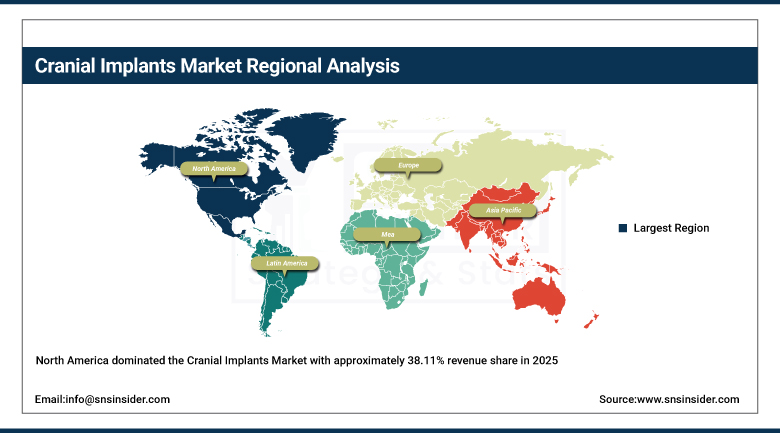

North America dominated the Cranial Implants Market with approximately 38.11% revenue share in 2025, anchored by the United States; leading position in neurosurgical procedure volumes, advanced healthcare infrastructure, favorable reimbursement policies that cover both standardized and patient-specific cranial reconstruction procedures, and the concentrated presence of market-leading cranial implant manufacturers including Stryker, Integra LifeSciences, DePuy Synthes, and KLS Martin. The U.S. market high adoption of 3D-printed patient-specific implants reflects both the technical capabilities of leading neurosurgical centers and the favorable reimbursement environment that supports premium implant utilization in complex reconstructive cases. The CDC documented high burden of TBI in the United States, with approximately 200,000 hospitalizations and nearly 70,000 TBI-related deaths annually, provides a substantial and sustained volume base for cranial implant utilization. Canada contributes a growing secondary market supported by universal healthcare coverage for cranial reconstruction procedures and expanding neurosurgical capabilities across academic medical centers in major urban centers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cranial Implants Market Insights

Europe represents a technically advanced and innovation-driven Cranial Implants Market, characterized by the presence of several leading cranial implant technology companies including OssDsign AB in Sweden, Renishaw plc in the United Kingdom, and Xilloc Medical in the Netherlands that specialize in patient-specific 3D-printed cranial implant design and manufacturing. Germany leads the European market through its sophisticated neurosurgical infrastructure, high adoption of digital surgical planning technologies, the presence of major medical device companies including B. Braun SE with comprehensive neurosurgical product portfolios, and the strong clinical research culture that drives evaluation and adoption of innovative implant materials and designs. Europe aging population is contributing to growing cranial implant market volumes through elevated rates of cerebrovascular disease, brain tumor incidence, and age-related falls causing head injuries that require neurosurgical intervention. The EU Medical Device Regulation (MDR) framework that became fully effective in 2021 has strengthened quality and clinical evidence requirements for cranial implants while creating compliance burden particularly for smaller specialized manufacturers.

Latin America & Middle East and Africa Cranial Implants Market Insights

Latin America and the Middle East & Africa represent developing Cranial Implants Markets where improving healthcare infrastructure, growing private hospital investment, and increasing access to neurosurgical care are generating expanding market opportunities. Brazil leads Latin American market development through its public healthcare system (SUS) coverage of neurological surgical procedures, the presence of ANVISA-regulated domestic medical device manufacturers, and academic medical centers in South Paulo and Rio de Janeiro with advanced neurosurgical programs that deploy international-standard cranial implant technologies. Mexico and Colombia represent secondary growth markets with growing private hospital networks offering neurosurgical services. In the Middle East & Africa, the UAE and Saudi Arabia lead market development through their world-class hospital infrastructure, high government healthcare investment, and adoption of advanced neurosurgical technologies including patient-specific implant capabilities at major tertiary medical centers. South Africa leads Sub-Saharan African cranial implant market development through its academic hospital system neurosurgical programs.

Market Dynamics:

Cranial Implants Market Growth Drivers: Rising global traumatic brain injury burden, increasing neurosurgical procedure volumes, and clinical adoption of 3D-printed patient-specific implant technologies driving market growth

The primary structural growth drivers for the Cranial Implants Market are the sustained global burden of traumatic brain injury, the growing incidence of brain tumors requiring cranial resection and reconstruction, and the progressive aging of global populations that is elevating rates of cerebrovascular events and age-related falls causing head injuries requiring neurosurgical intervention. Rising cases of road traffic accidents, sports-related head injuries, occupational injuries, and physical violence globally are driving consistent annual TBI volumes that require neurosurgical management including craniectomy and subsequent cranioplasty with cranial implants. The accelerating clinical validation and adoption of patient-specific 3D-printed cranial implants is simultaneously expanding the market total addressable revenue pool by enabling premium-priced implant solutions that deliver demonstrably superior clinical outcomes compared to legacy standardized alternatives, driving average selling price growth that complements the procedure volume growth generated by demographic and epidemiological factors.

Restraints: High patient-specific implant costs, lengthy design and manufacturing timelines, regulatory complexity for custom medical devices, and healthcare reimbursement limitations constraining market expansion

The Cranial Implants Market faces several structural constraints on growth rate and market penetration. The high cost of patient-specific cranial implants manufactured through 3D printing processes, typically ranging from USD 5,000 to USD 30,000 or more depending on complexity, material, and manufacturer, limits access to advanced customized solutions in healthcare systems with constrained budgets, public healthcare reimbursement caps, or limited health insurance coverage for medical devices. The design, manufacturing, quality testing, and sterilization cycle for patient-specific implants typically requires 2-4 weeks from CT scan receipt to implant delivery, which is incompatible with urgent trauma reconstruction timelines and constrains patient-specific implant utilization to elective or semi-elective cranioplasty procedures.

Opportunities: Emerging market neurosurgical infrastructure development, bioactive osseointegrating materials, digital workflow integration, and transparent implant technologies creating long-term growth opportunities

The Cranial Implants Market presents substantial growth opportunities across multiple strategic dimensions. The continued expansion of neurosurgical infrastructure across developing healthcare systems in Asia Pacific, Latin America, and Sub-Saharan Africa represents a multi-year volume growth opportunity as populations with historically unmet needs for cranial reconstruction gain access to neurosurgical services. The development and clinical validation of bioactive osseointegrating ceramic and composite cranial implant materials that promote bone integration and deliver long-term biological fixation represent a meaningful clinical advancement opportunity that could generate substantial implant replacement cycles as legacy passive implants are upgraded to biologically active alternatives.

Recent Developments:

- February 2024: OssDsign AB launched a next-generation 3D-printed cranial implant with improved osteointegration capabilities incorporating a calcium phosphate mineral coating that enhances bone cell attachment and long-term skeletal integration, representing a meaningful advancement in the biological performance of synthetic cranial reconstruction materials.

- April 2024: 3D Systems received FDA clearance for the EXT 220 MED 3D printer using medical-grade PEEK materials for cranial reconstruction applications, enabling hospital and CDMO facilities to produce patient-specific PEEK cranial implants in-house with an FDA-cleared manufacturing system, reducing turnaround times and logistics complexity.

Cranial Implants Market Key Players:

- Stryker Corporation

- Integra LifeSciences Holdings Corporation

- DePuy Synthes (Johnson & Johnson MedTech)

- KLS Martin Group

- OssDsign AB

- B. Braun SE

- Zimmer Biomet Holdings Inc.

- Medtronic plc

- Renishaw plc

- Brainlab AG

- Xilloc Medical B.V.

- Evonos GmbH

- Bioplate Inc.

- Anatomics Pty Ltd

- 3D Systems Corporation

- Materialise NV

- Synimed Synergie

- Biomet (Zimmer Biomet)

- Natus Medical Incorporated

- Acumed LLC

Cranial Implants Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.48 Billion |

| Market Size by 2035 | USD 2.83 Billion |

| CAGR | CAGR of 6.66% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Customized, Non-Customized) • By Material (Polymer, Ceramic, Metal) • By End-User (Hospitals, Neurosurgery Centers) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Stryker Corporation, Integra LifeSciences Holdings Corporation, DePuy Synthes (Johnson & Johnson MedTech), KLS Martin Group, OssDsign AB, B. Braun SE, Zimmer Biomet Holdings Inc., Medtronic plc, Renishaw plc, Brainlab AG, Xilloc Medical B.V., Evonos GmbH, Bioplate Inc., Anatomics Pty Ltd, 3D Systems Corporation, Materialise NV, Synimed Synergie, Biomet (Zimmer Biomet), Natus Medical Incorporated, and Acumed LLC |

Frequently Asked Questions

Ans: Asia Pacific is expected to register the fastest CAGR of 7.28% during the forecast period, driven by expanding healthcare infrastructure across China and India, growing awareness of cranial reconstruction procedures, rising traumatic brain injury incidence in rapidly urbanizing populations, and accelerating adoption of modern implant technologies.

Ans: Hospitals dominated with approximately 78.5% of Cranial Implants Market revenues in 2025, reflecting the concentration of cranial implant procedures in hospital settings that provide the full neurosurgical infrastructure, intensive care capabilities, and emergency department access required for both acute trauma cases and complex elective cranioplasty procedures.

Ans: Polymer materials, primarily PEEK-based implants, dominated with approximately 54.03% market share in 2025, driven by PEEK unique combination of biocompatibility, radiolucency enabling unobstructed post-operative neuroimaging, bone-like mechanical properties, and versatile manufacturability across both 3D printing and traditional machining processes.

Ans: The Customized segment dominated the Cranial Implants Market in 2025, reflecting growing clinical adoption of patient-specific 3D-printed cranial implants that deliver superior anatomical precision, improved cosmetic outcomes, and reduced surgical time compared to standardized prefabricated alternatives.

Ans: The Cranial Implants Market was valued at USD 1.48 billion in 2025.

Ans: The Cranial Implants Market is expected to grow at a CAGR of 6.66% from 2026 to 2035.

Get in Touch