Flexible Foam Market Report Scope & Overview:

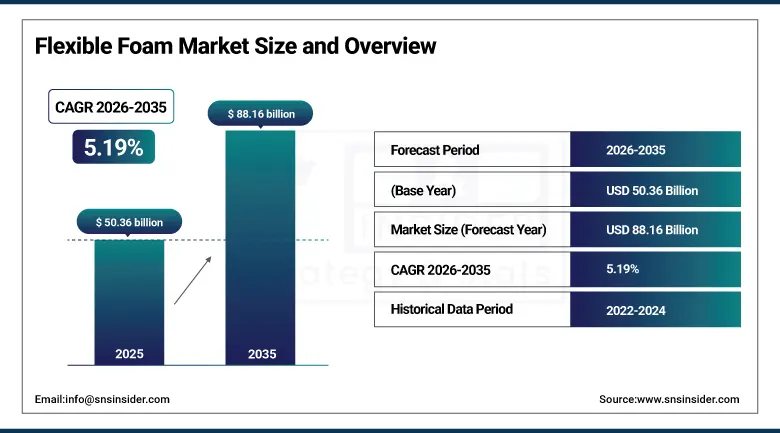

The Flexible Foam Market was valued at USD 50.36 Billion in 2025 and is expected to reach USD 88.16 Billion by 2035, growing at a CAGR of 5.19% from 2026–2035.

The global flexible foam market is progressing gradually. Flexible foam refers to a sturdy and highly adaptable cellular material obtained through the expansion of polymer matrices, where their porous structure endows them with the softness, compressibility, and rebound properties required by furniture padding, auto seat cushioning, bed comfort, packaging materials, and acoustic insulators. The market growth drivers include increased customer preference for quality sleeping beds and mattresses, demands from an expanding automotive industry for auto seats and interiors, demands from a growing furniture industry for padding, and growing soundproofing and acoustic insulation needs.

In September 2024, BASF and Future Foam announced the introduction of a new sustainable flexible foam for mattress applications using biomass-based Lupranate T 80 TDI, along with two condensers in series for CO2 emissions reductions. This innovation indicates the direction of flexible foam product development, where bio-based substitutes for the raw materials reduce the carbon emissions of polyurethane foam manufacturing without sacrificing its performance attributes.

Market Size and Forecast

-

Market Size in 2026E: USD 52.97 Billion

-

Market Size by 2035: USD 88.16 Billion

-

CAGR: 5.19% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Flexible Foam Market - Request Free Sample Report

Flexible Foam Market Trends

-

Bio-based polyurethane foam development is gaining momentum as manufacturers adopt renewable feedstocks to meet sustainability goals and environmental certification requirements

-

Advancements in memory foam technology are improving comfort, pressure relief, temperature regulation, and airflow for bedding and furniture applications

-

Growth in electric vehicle production is increasing demand for lightweight and high-performance polyurethane foams used in automotive interiors and insulation

-

Expansion of the e-commerce mattress market is driving adoption of high-resilience polyurethane foams suitable for compression packaging and direct-to-consumer delivery

-

Rising demand for acoustic insulation in residential, commercial, and professional environments is supporting increased use of polyurethane foam-based sound absorption products

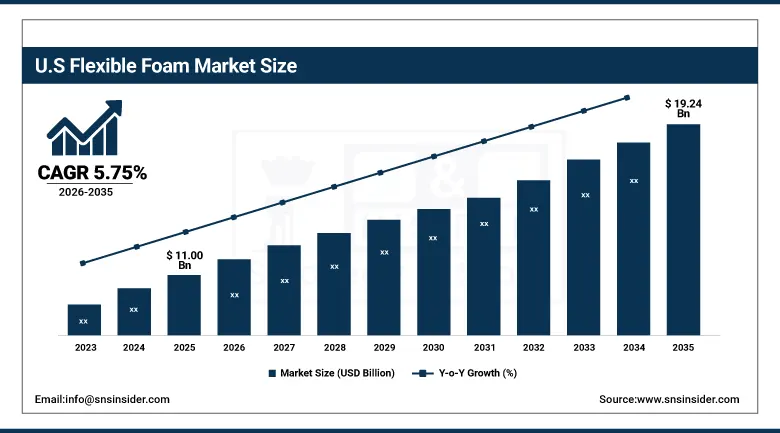

U.S. Flexible Foam Market Outlook

The U.S. Flexible Foam Market was valued at approximately USD 11.00 Billion in 2025 and is expected to reach approximately USD 19.24 Billion by 2035, growing at a CAGR of approximately 5.75%.

United States is a commercially significant market for flexible foam in North America. Companies such as Leggett & Platt, Carpenter Co., FXI, and UFP Technologies supply flexible foams to the local market for use in applications in furniture, bedding, automotive, and specialty foams. The disruption in the U.S. mattress market through direct-to-consumer sales of mattresses that specify foam formulations drive structured purchasing while the automotive industry embraces lightweight interior materials.

In January 2025, researchers at Washington State University developed a bio-based polyurethane foam from pine lignin, reducing petroleum consumption by 20%. The innovation demonstrates the commercial viability of lignin-derived polyol feedstocks whose agricultural and forestry by-product availability creates cost-competitive bio-based alternatives to petroleum-derived polyol without requiring dedicated bio-refinery investment, accelerating the commercialisation timeline for bio-based flexible foam at commercially accessible price premiums.

Flexible Foam Market Segment Analysis

-

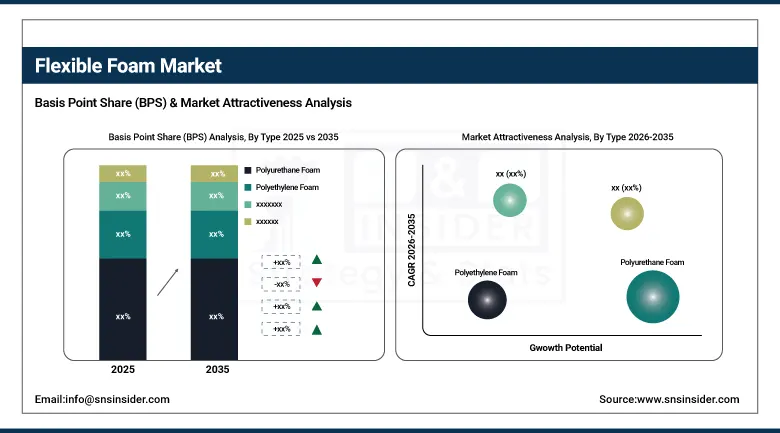

By Type, the Polyurethane Foam segment dominated the Flexible Foam Market with 45.2% share in 2025, while the Latex Foam segment is the fastest growing.

-

By Application, the Furniture & Bedding segment dominated the Flexible Foam Market with approximately 38% share in 2025, while the Automotive segment is the fastest growing.

-

By End User, the Residential segment dominated the Flexible Foam Market with approximately 42% share in 2025, while the Automotive segment is the fastest growing.

By Type, polyurethane dominates, latex grows fastest

Polyurethane foam retained the dominant type position with 45.2% of the flexible foam market in 2025. Its commercial primacy reflects the extraordinary versatility that polyurethane chemistry provides across foam density, firmness, ILD, and resilience specifications whose customisation capability enables a single material chemistry to serve applications ranging from ultra-soft pillow tops through firm industrial gaskets. Flexible PU foam's superior cushioning performance, cost effectiveness relative to latex and specialty foam alternatives, and the established manufacturing infrastructure's supply chain efficiency sustain specification preference across the broadest range of flexible foam applications globally.

Latex foam is the fastest-growing type because natural latex's combination of hypoallergenic properties, superior breathability relative to conventional PU foam, durable resiliency without synthetic polymer degradation, and natural material consumer preference creates above-average adoption in the premium mattress segment whose direct-to-consumer brands' natural positioning creates commercial motivation for latex specification. Each premium mattress brand that specifies natural latex comfort layers creates procurement whose compound growth with the premium mattress market's expansion sustains latex foam's fastest-growing type status.

By Application, furniture & bedding dominates, automotive grows fastest

Furniture and bedding retained the dominant application position with approximately 38% of the flexible foam market in 2025. The global furniture and mattress industry's combined scale, encompassing seating cushions, back rests, mattress comfort layers, pillows, and toppers across residential, hospitality, and healthcare settings, creates the most commercially certain and highest-volume flexible foam procurement category. The mattress-in-a-box market's extraordinary growth in the direct-to-consumer segment created above-average high-resiliency foam demand from online mattress brands whose compression packaging requirement necessitates foam chemistry that recovers after sustained compression shipping.

Automotive is the fastest-growing application because EV interior design's systematic weight reduction program, the progressive adoption of moulded flexible foam for dashboard, door panel, and headliner acoustic management, and the premium automotive segment's comfort specification upgrade are collectively creating above-average per-vehicle flexible foam content growth. Each new EV platform that replaces heavy felt acoustic insulation with lightweight flexible foam acoustic composite creates material substitution procurement that compounds with EV production volume growth. The autonomous vehicle interior's passenger comfort focus creates additional premium flexible foam specification motivation beyond conventional transportation automotive design.

By End User, residential dominates, automotive grows fastest

Residential end users retained the dominant position with approximately 42% of the flexible foam market in 2025. The residential sector's diverse flexible foam consumption across mattresses, sofas, chairs, pillows, and acoustic products creates aggregate demand that substantially exceeds any other single end-user category. Each new residential unit constructed or furnished creates flexible foam procurement whose combined global scale across new construction and furniture replacement cycles creates consistent commercial demand. The growing global middle-class population's increasing investment in home comfort creates above-average demand for premium flexible foam specifications in both developed and emerging markets.

The automotive end user is the fastest-growing segment because vehicle electrification is creating a material substitution opportunity for flexible foam in acoustic management, thermal insulation, and weight reduction whose commercial motivation compounds with EV production growth. Each EV's battery cooling system's thermal management requirement creates foam encapsulation and thermal interface opportunities that ICE vehicles did not generate. The automotive industry's systematic lightweight material programme whose weight reduction targets sustain continued foam content per vehicle growth creates procurement that expands proportionally with automotive production.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

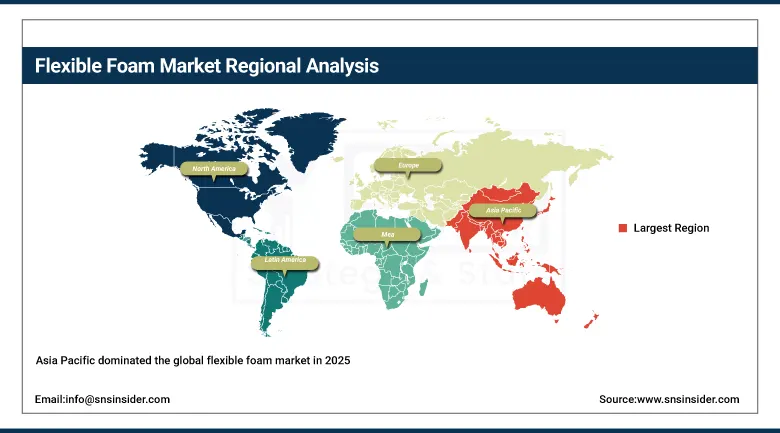

Asia Pacific Flexible Foam Market Insights

Asia Pacific dominated the global flexible foam market in 2025 as the world's largest production and consumption region. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary furniture manufacturing scale, the growing domestic mattress market, and the automotive sector's foam procurement. The region's rapid urbanisation, rising middle-class household formation, and expanding automotive production collectively sustain the most commercially significant flexible foam demand globally.

India and Southeast Asia are the most commercially dynamic emerging markets within Asia Pacific where furniture manufacturing growth, rising consumer spending on home furnishings, and automotive production expansion are creating above-average flexible foam demand growth that compounds with industrial development.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Flexible Foam Market Insights

North America is a commercially significant flexible foam market anchored by the U.S. mattress and furniture industry, the automotive OEM sector's foam interior, and the packaging industry's protective foam procurement. The United States accounts for approximately 87.4% of North American revenues through Leggett & Platt, Carpenter Co., FXI, and UFP Technologies' operations whose combined portfolio serves the domestic market across all major application categories.

Canada contributes approximately 12.6% of North American revenues through its furniture manufacturing sector, the automotive assembly industry's foam procurement, and the construction sector's acoustic and thermal foam insulation investment.

Europe Flexible Foam Market Insights

Europe is a technically sophisticated flexible foam market where sustainability regulation is creating the most commercially transformative product innovation cycle in the market's history. BASF, Covestro, Dow, and Huntsman's European operations create the chemical raw material supply chain whose TDI and polyol innovation sustains European flexible foam manufacturers' product development. Germany accounts for approximately 22.3% of European revenues through its automotive manufacturing sector's foam interior procurement, the furniture industry cushioning demand, and the construction sector's acoustic foam adoption.

Vita Group and Covestro's collaborative work on sustainable foam solutions demonstrates Europe's commercial momentum in bio-based flexible foam development. BASF and Future Foam's September 2024 sustainable bedding foam launch using biomass-based TDI reflects the European market's sustainability-driven innovation investment whose commercial differentiation sustains premium pricing in the bedding and furniture segments.

MEA & Latin America Flexible Foam Market Insights

Saudi Arabia is the leader in MEA's sales at around 31.2%, which comes from furniture and mattress needs in the country's residential construction sector, foam demand from the country's growing automotive manufacturing sector, and Vision 2030's industry development resulting in more channels for foam utilization. Brazil leads in Latin America in sales at around 44.2%, which comes from its huge furniture manufacturing industry, foam purchase by its automotive sector, and middle class' household formation in the country.

UAE's premium furniture and hospitality sector creates above-average per-unit flexible foam specification, and South Africa's automotive manufacturing creates consistent foam interior procurement across the regional market.

Market Dynamics

Growth Drivers: Mattress market DTC disruption and EV automotive foam content growth creating dual market drivers

The direct-to-consumer mattress market's extraordinary growth is the flexible foam market most commercially dynamic near-term driver. Each online mattress brand whose bed-in-a-box delivery model requires high-resiliency flexible foam formulations creates procurement that compounds with DTC mattress market penetration growth. The global mattress market's progressive transition from traditional retail to online creates new product formulation requirements whose foam chemistry innovation sustains premium product development investment. The global wellness trend's elevation of sleep quality as a health priority creates consumer willingness to pay for premium foam specifications that sustains above-average mattress foam quality upgrade investment.

EV automotive interior foam content growth is simultaneously creating the most structurally transformative demand shift in automotive flexible foam procurement. Each BEV platform's systematic reduction of heavy acoustic materials through lightweight foam composite replacement, combined with the passenger comfort focus of vehicles whose driving task reduction creates more time for in-cabin comfort appreciation, creates per-vehicle foam content growth that compounds with EV market penetration globally.

Restraints: Volatile TDI and polyol raw material pricing and environmental regulation creating reformulation investment

TDI and MDI isocyanate raw material pricing volatility creates foam production cost uncertainty whose impact on margin predictability limits foam manufacturer investment confidence in capacity expansion at marginal economics. Each toluene and benzene price cycle creates TDI cost variation whose downstream impact on flexible foam production economics creates margin compression during high-feedstock-cost periods that affects manufacturer pricing competitiveness.

Environmental regulation of flame retardants, specifically PBDE and HBCD phase-outs under the Stockholm Convention, and California's TB 117-2013 flame retardancy standard's evolution creates product reformulation investment whose cost and timeline create operational burden for foam manufacturers. Each new flame retardant regulatory restriction creates chemistry substitution investment whose commercial impact adds cost relative to markets with less stringent regulations.

Opportunities: Bio-based foam commercialisation and EV acoustic foam lightweighting

Bio-based flexible foam commercialisation represents the most commercially transformative product development direction whose successful market adoption creates sustainable product categories that premium pricing sustains. Washington State University's pine lignin bio-foam demonstrating 20% petroleum reduction and BASF and Future Foam's biomass-based TDI launch collectively demonstrate the commercial progress whose acceleration creates bio-based foam market development opportunity for producers who invest early in sustainable chemistry capability.

EV acoustic and thermal management foam represents a premium commercial opportunity whose per-vehicle value substantially exceeds conventional automotive seating foam economics. Each new EV platform's acoustic management requirement creates specialised foam composite specification whose thermal stability, vibration damping, and lightweight combine to create material performance beyond commodity flexible foam capability, creating premium procurement that sustains above-market margin contribution for technically qualified suppliers.

Recent Developments:

-

2024: BASF and Future Foam launched sustainable flexible foam for bedding in September 2024, based on biomass-based Lupranate T 80 TDI with two condensers in series for CO₂ reduction, targeting mattress manufacturers seeking commercially viable sustainable foam alternatives.

-

2025: Researchers at Washington State University developed a bio-based polyurethane foam from pine lignin in January 2025, reducing petroleum consumption by 20%, demonstrating the commercial viability of lignin-derived polyol feedstocks for sustainable flexible foam production.

-

2024: Covestro expanded its Desmodur and Baytherm polyurethane portfolio in 2024 with new sustainable flexible foam grades targeting automotive lightweighting and thermal management applications, supporting EV manufacturers seeking weight reduction in interior and battery thermal insulation systems.

Flexible Foam Market Key Players

-

BASF SE

-

Covestro AG

-

Dow Chemical Company

-

Huntsman Corporation

-

Armacell International S.A.

-

Sealed Air Corporation

-

Leggett & Platt Inc.

-

Carpenter Co.

-

FXI (Foamex)

-

UFP Technologies Inc.

-

Recticel NV

-

Vita Group Ltd.

-

Colfax Corporation

-

Woodbridge Group

-

Foam Supplies Inc.

-

Future Foam Inc.

-

Rogers Corporation

-

Latexco NV

-

Greiner Foam International

-

Eurofoam GmbH

Flexible Foam Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 50.36 Billion |

| Market Size by 2035 | USD 88.16 Billion |

| CAGR | CAGR of 5.19% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Polyurethane Foam, Latex Foam, Polyethylene Foam, Polypropylene Foam, Others) • by Application (Furniture & Bedding, Automotive, Packaging, Construction, Healthcare, Others) • by End User (Residential, Automotive, Industrial, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | BASF SE, Covestro AG, Dow Chemical Company, Huntsman Corporation, Armacell International S.A., Sealed Air Corporation, Leggett & Platt Inc., Carpenter Co., FXI (Foamex), UFP Technologies Inc., Recticel NV, Vita Group Ltd., Colfax Corporation, Woodbridge Group, Foam Supplies Inc., Future Foam Inc., Rogers Corporation, Latexco NV, Greiner Foam International, Eurofoam GmbH |

Frequently Asked Questions

The Flexible Foam Market is expected to grow at a CAGR of 5.19% from 2026 to 2035.

The Flexible Foam Market was valued at USD 50.36 Billion in 2025.

Increasing demand for comfortable and supportive bedding products driving DTC mattress market growth requiring high-resiliency flexible foam formulations, and growing automotive industry.

Polyurethane Foam dominated the Flexible Foam Market with 45.2% share in 2025, while Latex Foam is the fastest growing segment.

Asia Pacific dominated the Flexible Foam Market in 2025 as the world's largest production and consumption region, with China accounting for approximately 44.8% of Asia Pacific revenues.

Get in Touch