Forage Seed Market Report Scope & Overview:

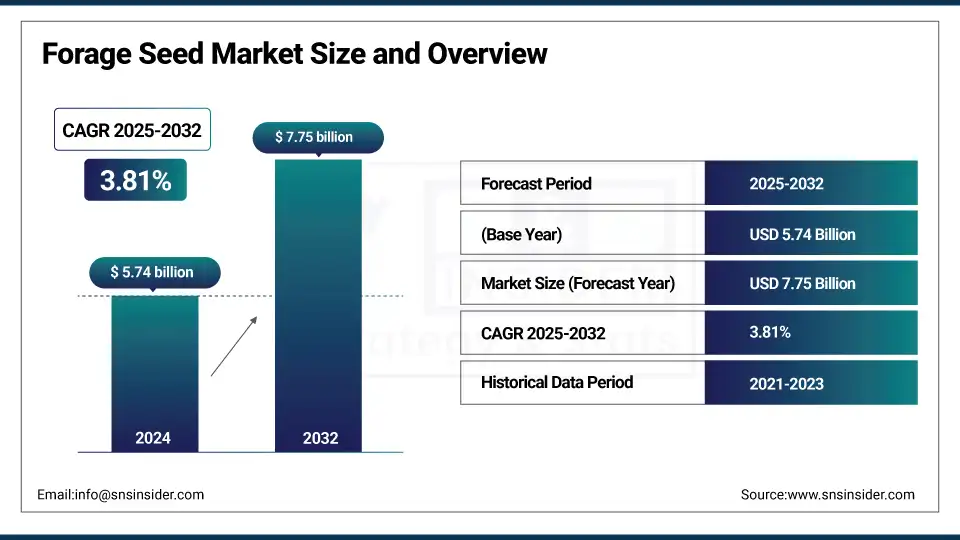

The Forage Seed Market Size was valued at USD 5.74 billion in 2024 and is expected to reach USD 7.75 billion by 2032, growing at a CAGR of 3.81% over the forecast period of 2025-2032.

The global forage seed market analysis also supports the surging demand of products based on animal protein. Growth in demand is led by an expanding global population, increasing urbanization and changing dietary habits toward more protein-rich foods, such as meat, milk and eggs. This is causing a boom in livestock production to feed this burgeoning portion of the human population. For better productivity and health of the animal, farmers are shifting towards good forage crops with improved seed variety and precision agriculture seed technology. Forage seeds ensure feed efficiency and milk yields, stimulate animal growth and they become more important members of production animal operations, which drive the forage seed market growth.

To Get more information On Forage Seed Market - Request Free Sample Report

In fact, by 2021, output of pasture, rangeland, and forage crops insured under federal crop insurance grew from neglectable in 2016 to about 40% of total insured acreage in the Federal Crop Insurance Program as estimated by the USDA Economic Research Service.

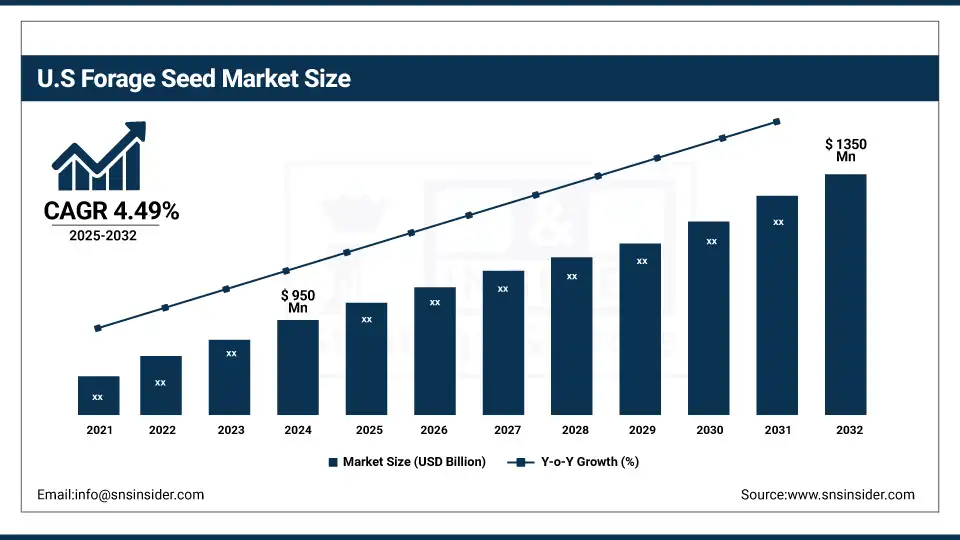

The U.S. Forage Seed market size was USD 950 million in 2024 and is expected to reach USD 1350 million by 2032 and grow at a CAGR of 4.49% over the forecast period of 2025-2032. It is due to positive use in cattle feeds used by pasture-based beef and dairy industries. Although the acreage in the U.S. committed to alfalfa hay production slipped sharply from the peak set more than a decade ago, USDA indicated that beef and dairy producers have maintained steady demand for each acre utilized for crops other than pasture. The U.S. government likewise has backed seed development through direct investment.

Market Dynamics:

Key Drivers:

-

Government Support for Sustainable Grazing and Forage Programs Drive the Market Growth

The rise of sustainable agriculture and livestock grazing practices which is supported by government backing across the globe acts as a major driver for the forage seed market. Through programs including the USDA Environmental Quality Incentives Program (EQIP) and Conservation Stewardship Program (CSP), some funds are targeted at assisting farmers in establishing improved forage resources to increase pasture productivity, reduce erosion, and promote soil health. Not only are these initiatives driving forage seed demand by adding financial incentives and technical support for producers, but the producer adoption risk has also been reduced.

For instance, EQIP was used by the USDA to provide funding of over USD 400 million in 2023 for grazing land management and forage crop establishment across a number of the U.S. states.

Restraints:

-

Climate Volatility Affecting Forage Crop Yields, which may hamper the Market Growth

Inconsistent forage seed performance is a major limitation to having proper weather patterns, which includes dry, often called "drought moisture" and wet (called "excessive moisture), and late frosts. The climate is tricky for plenty of forage species in their early growth stages, where and such erratic environmental changes can cause disturbance to your lawn-buds. Such climate risk deters farmers from buying high input cost seeds, especially in marginal or rain fed zones restricting the market growth of these varieties in vulnerable areas.

Opportunities:

-

Rising Adoption of Regenerative Livestock Systems Create an Opportunity for the Market

Advancements in regenerative livestock systems have opened new space for forage seed producers with the demand of diverse, perennial forage crops, which are a key ingredient to beefless ag as acre-by-acre land is taken out of traditional cattle ranching. Such systems increase soil carbon capture, pasture longevity and feed nutrition for the animals. Seed companies that provide regionally adapted, multi-species blends are becoming more popular within this industry, which drives the forage seed market trends.

In 2024, the USDA’s Conservation Stewardship Program funded over 5,000 contracts focused on multi-species forage planting and managed grazing, committing USD 364 million to support regenerative practices.

Segmentation Analysis:

By Product Type

Alfalfa is the most widely used forage seed and accounts for approximately 34% of the market share (2024 estimate) due to its high digestibility, protein content, and nitrogen-fixing capability make it ideal for dairy cattle, beef herds, and soil health improvement. The strong market presence is also due to its widespread adaptability to different climates and its long regrowth cycle, providing multiple harvests annually.

By Livestock

Cattle farming dominates forage seed usage with over 58% of total demand. It is due to its usage is a primary feed for both dairy and beef cattle, and the large-scale presence of cattle operations in the U.S. Midwest and West drives continuous seed demand. Dairy operations, in particular, rely on quality forage to maintain milk yield and animal health, leading to steady procurement of seeds, such as alfalfa and ryegrass.

Poultry-related forage seed demand is increasing rapidly, especially among organic and pasture-raised egg producers. Although smaller in volume, the growth is supported by rising consumer demand for free-range poultry and egg production systems that rely partly on forage for natural nutrients.

By Species

Grasses represent the largest share in species segmentation, around 53% market share in 2024 due to the varieties, such as ryegrass, timothy, and fescue are favored for their fast growth, high dry matter yield, and compatibility with different livestock types. Their low maintenance requirements and resilience also support cost-effective pasture systems.

Legumes including clover and alfalfa are gaining ground due to their protein-rich composition and soil nitrogen-fixing properties, which reduce fertilizer use. The rise of sustainable farming practices and regenerative agriculture has accelerated the adoption of legume-based forage systems across North America.

By Application

Grazing leads the application category with around 45% market share. This growth is attributed to the prevalence of pasture-based systems in beef and dairy production, especially in areas including Texas, Nebraska, and Iowa. Grazing forage crops are essential for maintaining large herds and reducing total feed costs.

Silage applications are expanding rapidly due to growing livestock density and the need for consistent feed supply throughout the year. Silage from crops including sorghum, ryegrass, and millet is increasingly used in industrial dairy farms and feedlots to manage seasonal feed gaps and ensure higher nutritional value per bale.

Regional Analysis:

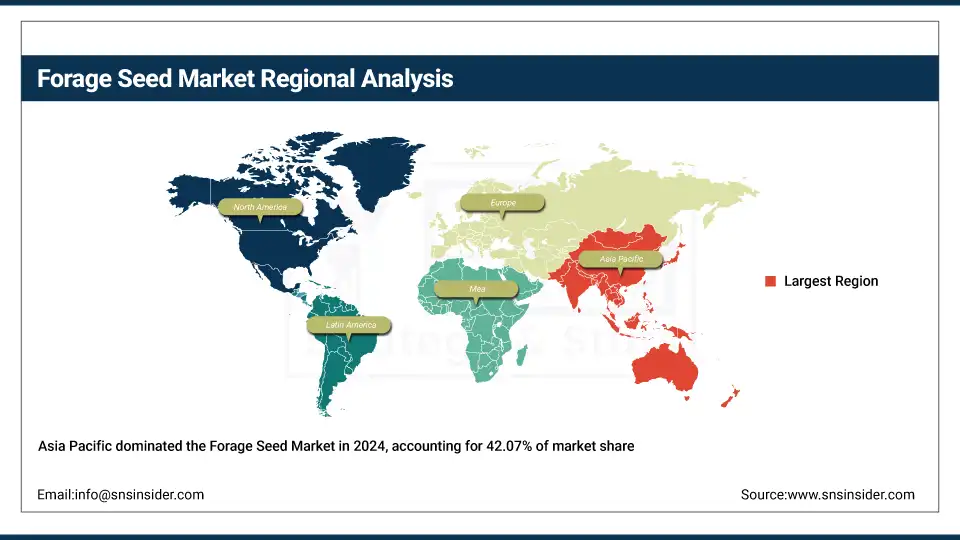

Asia Pacific held the Forage Seed market share largest market 2024, around 42.07% 2024. It is due to the huge livestock sector in this region, along with increasing demand for dairy and meat products. The article shows that conservation tillage improves life in the long term for soils within areas of India served by a specific Ministry of Agriculture and many governments push up media fodder cultivation, (new crop breakthroughs, allowing us to achieve strides while also obliging to reducing global warming). Local “hybrids” varieties particularly of sorghum, pearl millet and berseem have characteristics that make them suitable for cultivation like their inherent hardiness, high biomass yield as shown in this work.

Get Customized Report as per Your Business Requirement - Enquiry Now

In late 2023, the All India Coordinated Research Project on Forage Crops and Utilization AICRPFCU released more than 114 new forage varieties during 2017-2023, and species-specific and location-specific protocols for 1,305 field demonstrations over different agro-climatic regions. These signals institutional backing for boosting forage genetics and farmer acceptance.

The North American region is the fastest-growing market. It is due to large size cattle, dairy and livestock operations in Midwestern regions plains areas and western countries. The U.S. is home to some of the largest beef and dairy industries globally, thus, offerings demand for superior feedstuff crops, such as alfalfa, clover, ryegrass, and fescue. Stats from the USDA show that in 2024 over 50 million acres are devoted to forage crops with alfalfa covering about 15.6 million acres illustrating its importance to our livestock feed systems. It has the advantage of using higher yielding and more drought and heat tolerant seed technologies combined with water sources for irrigation and a network of extension services that provides strong education programs to farmers in the region.

in 2024, the USDA's National Institute of Food and Agriculture granted USD 3.7 million in research grants to enhance alfalfa seeds genetics on traits including drought resistance and feed quality. Among other things, this work has helped the U.S. producers to increase yields and manage climate variability without sacrificing forage as a building block in animal nutrition systems.

Europe maintains a significant share of the Forage Seed market due to the rising forage seed production that hinges on high regulatory standards, stringent demands for sustainability, and the breadth of the European livestock sector. France, Germany, the Netherlands, and such others countries have specific seeds certified to meet EU environmental goals for such things as dairy production feed, high-yield forage varieties, and beef production feed. In Europe, growers often choose ryegrass, fescue and clover because they perform well in cool weather and have soil health benefits. For instance, the Common Agricultural Policy (CAP) in the EU supports forage crop production by rewarding actions that increase biodiversity and reduce carbon emissions.

Key Players:

Major forage seeds companies are Corteva Agriscience, Barenbrug Group, DLF Seeds, Advanta Seeds, Allied Seed, RAGT Semences, S&W Seed Company, Land O’Lakes Inc., Pennington Seed, Royal Barenbrug Group, Takii & Co., Ltd., Ampac Seed Company, Germinal Holdings, La Crosse Seed, KWS SAAT SE & Co. KGaA, Limagrain, Stine Seed Company, AgReliant Genetics, Sakata Seed Corporation, and Smith Seed Services.

Recent Developments:

-

In July 2024, DLF launched “4Most”, a proprietary seed enhancement technology, developed and produced in its U.S. facility in Albany, Oregon. This formula includes slow-release nitrogen, moisture-absorbing biodegradable coatings, and beneficial microorganisms all designed to boost seedling survival, root development, and final forage stand vigor.

-

In May 2024, S&W Seed Company announced the launch of Double Team Forage Sorghum Seeds," a new, proprietary, non-GMO sorghum variety that is resistant to multiple herbicides.

| Report Attributes | Details |

| Market Size in 2024 | USD 5.74 Billion |

| Market Size by 2032 | USD 7.75 Billion |

| CAGR | CAGR of3.81% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type: (Alfalfa, Clover, Ryegrass, Chicory, Fescue, Timothy, and Others (Bromegrass, Orchardgrass, Millet, Sorghum)) • By Livestock: (Cattle, Poultry, Swine, and Others (Sheep, Goat, Horse, Rabbit) • By Species: (Legumes, Grasses, and Others (Brassicas, Herbs) • By Application: (Grazing, Hay, Silage, Green Manure, and Others (Soil Improvement, Erosion Control) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Corteva Agriscience, Barenbrug Group, DLF Seeds, Advanta Seeds, Allied Seed, RAGT Semences, S&W Seed Company, Land O’Lakes Inc., Pennington Seed, Royal Barenbrug Group, Takii & Co., Ltd., Ampac Seed Company, Germinal Holdings, La Crosse Seed, KWS SAAT SE & Co. KGaA, Limagrain, Stine Seed Company, AgReliant Genetics, Sakata Seed Corporation, Smith Seed Services |

Frequently Asked Questions

Ans Major challenges include fluctuating weather patterns, limited farmer awareness, and rising input costs for quality seed production.

Ans Key players include Corteva Agriscience, DLF Seeds, Barenbrug Group, S&W Seed Company, and PGG Wrightson Seeds.

Ans Climate change is shifting crop suitability zones and increasing demand for drought-tolerant and resilient forage seed varieties.

Ans Alfalfa and clover currently dominate the market due to their high nutritional value and widespread use in dairy and cattle feed.

Ans Rising demand for animal protein, expanding livestock farming, and advancements in seed technologies are driving global forage seed market growth.

Get in Touch