Forensic Equipment And Supplies Market Size & Trends:

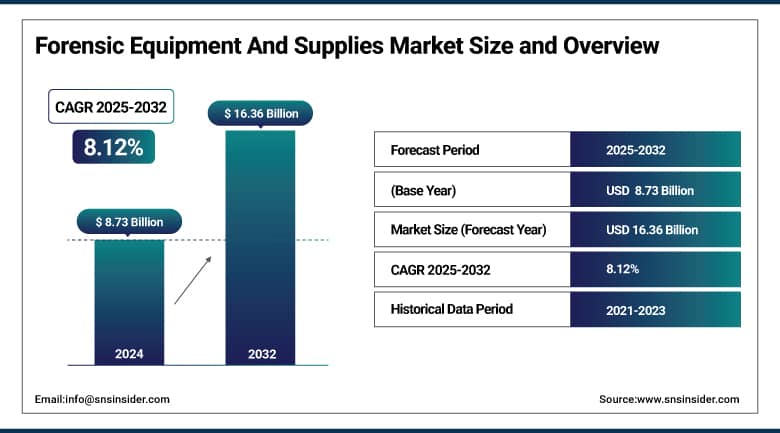

The Forensic Equipment And Supplies Market size was valued at USD 8.73 billion in 2024 and is expected to reach USD 16.36 billion by 2032, growing at a CAGR of 8.12% over 2025-2032.

The global forensic equipment and supplies market is gaining momentum on account of various factors, primarily including the rising crime rates, technological advancements, and the growing demand for accurate and swift forensic analysis. The forensic equipment and supplies market in the U.S. has experienced an increasing demand, as per the FBI's 2023 Uniform Crime Reporting (UCR) estimates that violent crimes exceeded 1.3 million cases, triggering an increase in the need for forensic analysis instruments and services. A full assessment by the NIJ reveals, it has escalating needs for DNA sequencers, toxicology kits, digital forensics tools, and rapid DNA systems.

To Get More Information On Forensic Equipment And Supplies Market - Request Free Sample Report

Increasing public safety investments, such as from the U.S. Department of Justice (DOJ) through the DNA Capacity Enhancement and Backlog Reduction (CEBR) Program, are driving the global forensic equipment and supplies market. Furthermore, countries such as India have also shown rising government spending, and for instance, the PIB press release (2024) has alluded to allocating significant budgets to modernize forensic labs in different states. The ISO 18385 standard now establishes explicit quality specifications for the production of forensic products, also affecting the development and purchasing of products globally.

In May 2025, the Guardian Nigeria reported NDLEA’s inauguration of a refurnished forensic laboratory, one of many investment-led stories indicative of the overall direction of the global forensic equipment and supplies market toward modernization and increased efficiencies.

Rising crime, expanding caseloads at forensic labs, and contamination, such as that at Hennepin County's crime lab, highlight the need for secure, non-contaminated forensic instruments of the highest quality. The supply-side rise of leading forensic equipment and supplies suppliers is accelerating R&D investment to address a burgeoning market, demonstrated in the development of expert-handheld rapid DNA processing tools promoted by the IACP and NIJ-funded digital forensics platforms. In the U.S., for instance, publicly funded forensics crime labs processed more than 5.5 million requests in 2022, up from 4.3 million three years earlier, which highlights market lift and the pressure on lab capacity, according to data from the Bureau of Justice Statistics (BJS).

Regulatory influence, such as the advent of ISO/IEC 17025 accreditation, is also shaping purchasing and operational strategies in laboratories throughout the world. Rising investments in R&D in sectors such as forensic toxicology and ballistics, and to authenticate digital evidence, also strengthen the forensic equipment market trends. Globally, the global forensic equipment and supplies market is expanding with increasing demand for cross-border forensic collaboration, disaster victim identification, and narcotics detection, as demonstrated by the efforts by the NDLEA and the U.K.’s FFLM on sample collection protocols.

In May 2024, Colorado and Connecticut lab capacity and integration of rapid DNA technology resulted in a decrease in DNA evidence backlog, representing a big leap forward in the U.S. forensic equipment and supplies market.

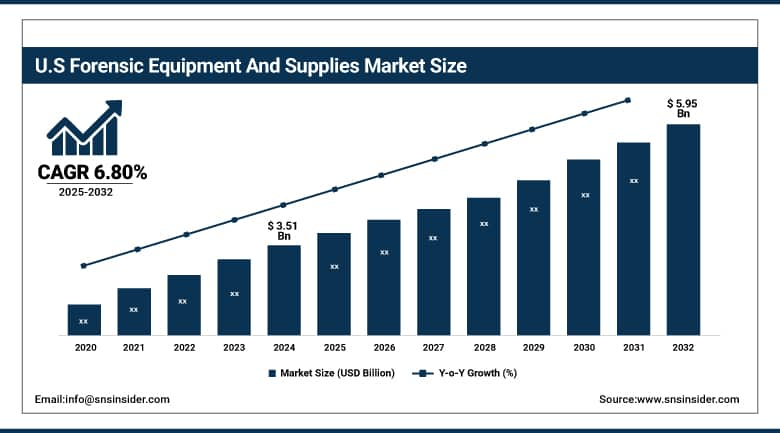

The U.S. Forensic Equipment And Supplies Market size was valued at USD 3.51 billion in 2024 and is expected to reach USD 5.95 billion by 2032, growing at a CAGR of 6.80% over 2025-2032. The U.S. remained the paramount region owing to the presence of strong government and independent forensic lab systems, an enriched judicial structure, and prominent federal funding facilities, such as Coverdell and CEBR, and has dominated over 65% market share in the region. In addition, the leading forensic equipment and supplies companies are located in the U.S., where innovation and deployment thrive. Canada is experiencing a gradual uptake, especially in digital and toxicological forensics, and Mexico is enhancing narcotics and organized crime activities through lab modernization initiatives. The U.S. leads with its focus on rapid DNA testing, mobile forensic units, and its rollout of ISO 17025 accreditation at state labs.

Forensic Equipment And Supplies Market Dynamics:

Drivers:

-

Rising Crime Complexity, Technological Integration, and Government Investment Fuel Growth

The growing complexity of crimes, technological advancements in the forensic space, and the global transition toward digitization in forensic investigation are the major factors driving the demand for forensic equipment and supply products. Recently developed DNA phenotyping, forensic toxicology, and digital forensic technologies are driving law enforcement departments to improve equipment and forensics protocols. More than 65% of the U.S. forensic labs were planning significant technology upgrades to accommodate new requirements, such as mobile device forensics and synthetic drug detection, according to the NIJ (2023). Moreover, higher funding and grants have led to endless procurement.

For instance, in 2024, the DOJ’s Paul Coverdell Forensic Science Improvement Grants Program received a 22% funding increase.

R&D in forensic science has spiked, and NIST pumped money into AI-enabled forensic imaging systems. The innovations, enabled by ISO 21043 and ISO 18385 guidelines, are streamlining the processing of evidence and the manufacturing of material, while increasing market confidence in and facilitating the adoption of the technology. The private sector is getting involved as well, leading to next-gen tools, such as crime scene lasers and portable gene analyzers , being developed by companies. Increasing need for accurate, fast, and standardized forensic testing, along with government and private financial support, is solidifying the momentum of forensic equipment and supplies market growth, especially in technologically advanced regions.

Restraints:

-

Operational Backlogs, Funding Gaps, and Shortage of Skilled Forensic Professionals Hinder the Market Expansion

The forensic equipment and supplies market is restricted by a lack of operational efficiency, a dearth of funding, and a shortage of trained professionals. Case backlogs plague crime laboratories globally. In 2022, more than 40% of the U.S. crime labs were taking longer than 30 days to process toxicology and DNA evidence, the Bureau of Justice Statistics (BJS) found. Much of this backlog can be traced to a lack of resources, outdated technology and infrastructure, and obsolete forensic techniques. Although there are funding programs, they tend to focus on particular stripes, including DNA processing, leaving holes in others, such as trace evidence, or forensic anthropology.

According to a 2024 OJP study, the inability to retain trained forensics scientists was the biggest operational bottleneck for more than 30% of labs. Moreover, strict regulatory requirements and procurement lead time prevent the rapid use of innovative tools, particularly in areas without the existence of standardized certification mechanisms. These issues are preventing the market from scaling along with demand. As a result, the forensic equipment and supplies market share is still concentrated amongst well-financed state institutions and favors the interest of these over that of other ordinary global forensic equipment and supplies markets yet to access.

Forensic Equipment And Supplies Market Segmentation Analysis:

By Application

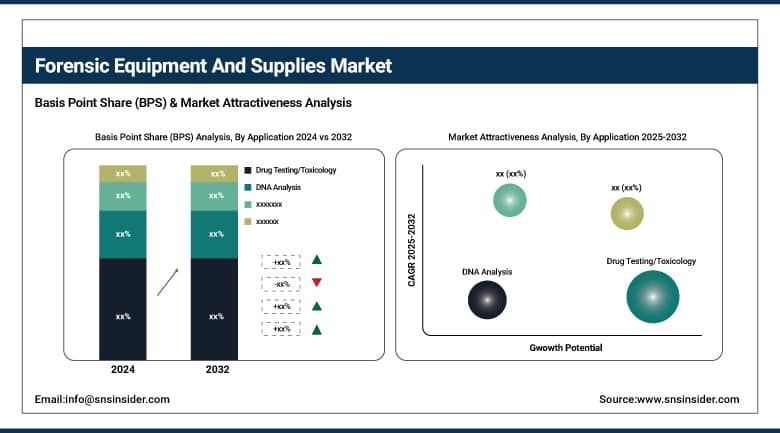

In 2024, drug testing/toxicology was the leading application, which accounted for almost 37% of the forensic equipment and supplies market share. The growth is driven by the ascending trend of substance abuse on a global basis and the demand for sensitive detection of opioids, synthetic cannabinoids, and designer drugs. Toxicology tests have become routine for both autopsies and crime scene investigations.

At the same time, DNA analysis is expected to be the fastest growing of all testing applications, as it continues to be used in more and more cold cases, disaster victim identification, and through familial matching. The rapid DNA testing systems and national DNA databases are also encouraging an investment drive in this category.

By Product

Instruments were the largest segment of the forensic equipment and supplies market in 2024 and contributed a revenue share of around 48.9%. The growth is driven by the extensive utilization of modern forensic technologies, such as spectrometry, chromatography, and computer forensics tools currently being operated in crime laboratories to further support detailed and multivariate evidence examination.

The reagents and consumables segment, on the other hand, is expected to grow at the highest CAGR during the forecast period. This is fueled by repeated purchases of purity reagents, chemical kits, swabs, and collection products that are necessary for evidence processing. Also, the demand for disposable ready-to-use consumables is growing with the trend toward forensic automation and high-throughput workflows, notably in toxicology and DNA analysis.

By End-User

The government forensic laboratories segment held the largest share in the global forensic equipment and supplies market, with a 52% share of the total market in 2024, as they receive a steady stream of government funding, enforcement of established forensic methodologies, and the fact that they are pivotal in police investigations. These laboratories are generally early adopters of cutting-edge forensic technology and have priority donor-funded investment in national forensic infrastructure.

The private forensic laboratories segment is expected to become one of the fastest-growing segments through the outsourcing of forensic testing services, notably in overwhelmed public forensics labs. The flexibility, lack of delay, and specialization of private labs should make them an attractive escape hatch, especially for law firms and private investigations.

Forensic Equipment And Supplies Market Regional Insights:

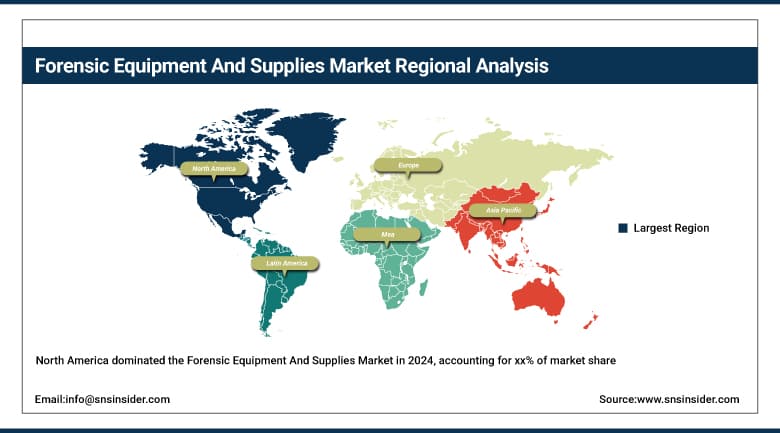

North America led the global forensic equipment and supplies market in 2024, on account of the high incidence of crime reporting, robust forensic infrastructure, and continuous public spending.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe was the second fastest growing forensic equipment and supplies market, driven by cross-border crime detection initiatives, development of regulatory frameworks across the EU, and national forensics modernization programs. Key countries are the U.K., which contributes close to 30% of the European market share in 2024 due to its extensive forensic science, digital forensics investment, and strong partnership with law enforcement. Biometrics and toxicology are both being developed at breakneck speed in the forensic institutions of Germany and France. Research projects funded by the EU as ENFSI (European Network of Forensic Science Institutes), facilitate technological development and regional standardization. Turkey and Poland are building up forensic capabilities at the local level to serve national security and civil and criminal resolution.

The Asia Pacific forensic equipment and supplies market is expected to be the fastest-growing region globally, owing to increasing urbanization, crime, and government support for forensic reforms. China remains the largest country in the area, accounting for more than 40% of the regional market in 2024, driven by massive government investments to boost crime lab expansion, AI-integrated forensic systems, and digital surveillance. India is growing fast as the government has instituted modern state-of-the-art regional forensic labs, including ones to alleviate the DNA and toxicology backlog.

Forensic Equipment And Supplies Market Key Players:

-

Mettler Toledo

-

HORIBA

-

Olympus Corporation

-

Agilent Technologies

-

Bio-Rad Laboratories

-

Waters Corporation

-

Bruker

-

Thermo Fisher Scientific

-

Danaher Corporation

-

Nikon Corporation

-

Leica Microsystems

-

PerkinElmer

-

Illumina, Inc.

Recent Developments in the Forensic Equipment And Supplies Market:

-

In April 2025, 26 care sites in Ohio received new forensic equipment to improve support services and evidence collection for survivors of sexual violence.

-

In March 2025, the U.S. Department of Justice awarded USD 2 million in grants to support cold case investigations, digital forensics enhancements, and forensic training programs across multiple agencies.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 8.73 billion |

| Market Size by 2032 | USD 16.36 billion |

| CAGR | CAGR of 8.12% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Instruments (Spectroscopy Equipment (Fluorescence Spectrometers, Atomic Absorption Spectrometers, Infrared Spectrometers, UV-visible Spectrometers, and Mass Spectrometers), DNA Analyzers (PCR Instruments, NGS Instruments, Electrophoresis Instruments, and Sanger Sequencers), Liquid Chromatography Systems, Gas Chromatography Systems, Blood Chemistry Analyzers, Fingerprint Analyzers, Microscopes, Forensic Cameras, Laboratory Centrifuges, and Other Forensic Instruments), Reagents and Consumables, Evidence Drying Cabinets, and Low-Temperature Storage Devices) • By Application (Drug Testing/Toxicology, DNA Analysis, Blood Analysis, Biometrics, and Other Applications) • By End User (Government Forensic Laboratories, Independent Forensic Laboratories, and Research Laboratories & Academic Institutes) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Shimadzu Corporation, Mettler Toledo, HORIBA, Olympus Corporation, Sartorius AG, Agilent Technologies, Bio-Rad Laboratories, Waters Corporation, Bruker, Thermo Fisher Scientific, Danaher Corporation, Nikon Corporation, Leica Microsystems, PerkinElmer, and Illumina, Inc. |

Frequently Asked Questions

The growing complexity of crimes, technological advancements in the forensic space, and the global transition towards digitization in forensic investigation are the major factors driving the demand for forensic equipment and supply products.

The forensic equipment and supplies market is restricted by a lack of operational efficiency, a dearth of funding, and a shortage of trained professionals.

North America dominated the Forensic Equipment and Supplies market.

The market is expected to reach USD 16.36 billion by 2032, increasing from USD 8.73 billion in 2024.

The Forensic Equipment and Supplies market is anticipated to grow at a CAGR of 8.12% from 2025 to 2032.

Get in Touch