Monocyte Activation Test Market Overview

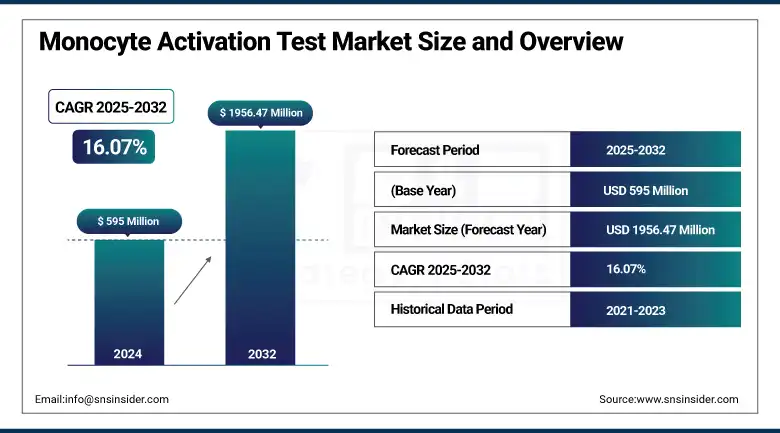

The Monocyte Activation Test (MAT) Market size was valued at USD 595 million in 2024 and is expected to reach USD 1956.47 million by 2032, growing at a CAGR of 16.07% over 2025-2032.

The Monocyte Activation Test (MAT) is becoming an important tool for the detection of pyrogens, mainly due to regulatory requirements and ethical reasons that prefer non-animal testing. The European Pharmacopeia has MAT as a validated alternative to rabbit pyrogen tests (RPT), and the EMA's Reflection Paper (2025, revised) gives further regulatory clout to the test, recommending that it be used more widely throughout the EU for biologics and parenteral drugs. Brazil’s ANVISA also adopted MAT in its national pharmacopoeia (2024), highlighting global regulatory momentum.

To Get more information On Monocyte Activation Test Market - Request Free Sample Report

For instance, in February 2025, EMA released its updated reflection paper and put MAT on the spot as the leader of the alternative to RPT in the flow of biotherapeutics testing, following the 3Rs impact and actual use cases.

Whereas demand is increasing on account of the increase in biologics and injectable drugs, which need strict compliance with pyrogen testing. Just in 2023, the global manufacturing of injectable biologics increased by more than 8.7%, intensifying MAT’s importance. For instance, Lonza has increased its PyroCell MAT system, which is much faster when conducting tests and reduces dependence on animal-originated reagents. It also revealed plans to discontinue traditional LAL and TAL assay readers in 2024. This launch was followed by the new endotoxin and pyrogen detection kit series announced by FUJIFILM Wako in June 2024, which were meant to be in accordance with MAT regulatory requirements, and propelled technology integration.

On the supply side, increased spending on R&D is evident. Validation studies for MAT are still funded by NIEHS and the OECD and more citation volume on MAT is seen in the literature that reflects academic and industrial attention. The cost-effectiveness, batch-to-batch consistency, and scalability in a high-throughput clean room environment are also some of the factors that contribute to the growing interest of pharmaceutical manufacturers in the MAT system.

In June 2024, FUJIFILM Wako unveiled pyrogen/endotoxin kits using MAT and following EP, which were developed about speed, automation, and sustainability.

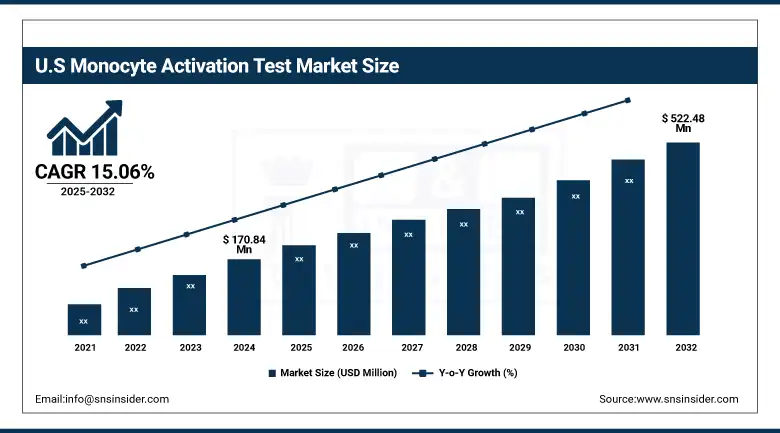

The U.S. monocyte activation test (MAT) market size was valued at USD 170.84 million in 2024 and is expected to reach USD 522.48 million by 2032, growing at a CAGR of 15.06% over 2025-2032. The U.S. holds a substantial market share in the region owing to the high acceptance of MAT over animal-based pyrogen tests in biologics and vaccine production. An FDA focus on in vitro approaches and a well-pressured finish by pharmacopeial standards has spurred rapid acceptance.

Monocyte Activation Test Market Dynamics

Drivers:

-

Rising Regulatory Push and Biologics Pipeline Expansion Fuel MAT Adoption

The global monocyte activation test (MAT) market is being heavily driven by growing regulatory support and the rapid growth of the parenteral and biologic drug production. The U.S. FDA, through the Interagency Coordinating Committee on the Validation of Alternative Methods (ICCVAM), recommended more widespread use of non-animal tests, such as the MAT. In its 2023 report, ICCVAM reported that more than 65% of surveyed drug manufacturers intended to incorporate MAT into quality control over the next 2 years. And the rapid proliferation of biologic drugs, up to 9,000 in development around the world as of 2024, many of them requiring pyrogen testing, has further underscored the importance of non-animal approaches, such as MAT.

Growing concern about animal ethics on a global scale is also prompting a response from the pharmaceutical industry. South Korea’s MFDS, for instance, commenced the review of its biologics testing guidelines in 2024 to allow the use of MAT as an official method for pyrogen testing, following on the heels of EU harmonization. Johnson & Johnson and AstraZeneca both increased their R&D spends by 11.2% and 9.5% in 2023, some of which is earmarked for the innovation of biologics safety and QC. Regulatory and pipeline synergy continues to lead to a market trend toward MAT, especially in higher-throughput, automation-compatible lab environments.

Restraints:

-

High Cost of Validation, Technical Complexity, and Limited Awareness Slow Uptake

The cost and technical overhead of validation, particularly for small and mid-sized pharma, is a significant barrier to adoption. Standardization of MAT as an alternative to the conventional RPT would also necessitate costly reagents, standardized monocyte products, and reliable control systems. In the 2023 Frontiers in Pharmacology publication, it was found that the cost of MAT validation on a per product basis could be between USD 150,000 and USD 500,000, depending on batch complexity. The absence of standardized worldwide regulatory practices remains a source of uncertainty.

The European Pharmacopoeia has accepted the MAT; however, a range of regulatory agencies in Asia and the Middle East still demand the animal testing methods, thus global harmonization is limited. The WHO’s 2022 biologics QC report identified “limited lab readiness and training gaps” as a main obstacle, adding that just 20% of low-to-mid-income nations had the infrastructure to implement the in vitro pyrogen tests. Also, the cell-based aspect of MAT requires highly specialized lab skills and cleanroom-compatible processes, which are a concern regarding the remote lab reproducibility. These operational and knowledge constraints act as a barrier to full market roll-out, particularly in unregulated markets (outside the EU and North America).

Monocyte Activation Test Market Segmentation Analysis

By Product

Based on product, the MAT Kits segment held 65.7% of the total market share in 2024 and is expected to be the dominant segment during the forecast period on account of the rising demand for reagent kits that are ready-to-use and standardized. MAT kits are easy to use, accurate, and adaptable to automated testing systems, making them ideal for pharmaceutical and biologics manufacturing high-throughput testing facilities. With growing regulation for animal-free testing and an increase in demand for injectable drugs, the affordability and scalability of MAT kits are becoming increasingly important.

Reagents are growing at the highest CAGR on account of the increasing use of MAT technology and the growing requirement of customized and premium quality reagents for individual applications. Reagents play a crucial role in driving the success of MAT assays, and as biopharma pipelines grow, particularly in biologics and vaccines, there is an increasing need for and use of highly specialized reagents.

By Application

The drug development application segment was the largest in terms of market share in 2024. This dominance is driven by the increasing number of biologics, which have a high requirement for pyrogen testing as a safety measure, in the pipeline. While drug safety regulations become more stringent globally, the demand for a dependable and rapid method of pyrogen testing, such as the MAT method, continues to grow. Drug manufacturers are now utilizing the MAT process for sterility assurance and safety of injectable drugs before launch.

The fastest growing segment in the monocyte activation test (MAT) market is the vaccine development segment, which is driven by an increase in the global production of vaccines and growing demand for non-animal pyrogen test. With the global shift in vaccine development and the system now being more focused on vaccine research, post-pandemic, the need for MAT in the manufacturing of vaccines is growing. The necessity of replacing animal models with alternative in vitro methods, such as MAT for vaccine pyrogen testing, has been advocated by regulatory agencies, such as the European Medicines Agency (EMA).

By Source

The PBMC-based segment held the majority of the monocyte activation test (MAT) market share in 2024. Peripheral blood mononuclear cells (PBMCs) represent the most common source for MAT as they are readily accessible, economically advantageous, and are compatible with human immune responses. The predictability and relevance of the detection of pyrogens specific for human pyrogens is increased when utilizing PBMCs, and for this reason, it is an alternative that is preferred by many biopharmaceutical companies when searching for a reliable testing method.

Cell line-based source is the fastest growing segment on account of advancements in cell culture technologies and growing use of immortalized cell lines for pyrogen testing. Cell line-derived MAT platforms have several advantages, including the advantage of reproducible, scalable, and consistent immune responses over time, and are suitable for industrial testing applications. The system is becoming more widely used by companies looking to automate and standardize pyrogen testing, a key step in expediting the production of biologics and vaccines.

By End-use

The pharmaceutical industry segment dominated the monocyte activation test (MAT) market, with a share of 58.3%, in 2024. This dominance can be attributed to the high demand for injectable drugs, biologics, and vaccines, which are tested for pyrogen before being released to the market. Pharmaceutical companies are being pressed by regulations and the growing need for safe, sterile drug products to move away from animal testing and toward alternatives, such as MAT.

The biotechnology industry is witnessing the highest growth in the monocyte activation test (MAT) market, which is attributed to the growing biopharma innovations including gene therapies, cell therapies, and new biologics. Biotech companies are spending billions and billions on R&D, which is why MAT is very important to protect these new products. The capability to apply MAT for pyrogen testing of new biological products is also important due to the preference in the U.S., EU, and Japan of regulatory agencies to propose the utilization of in vitro tests.

Monocyte Activation Test Market Regional Outlook:

In 2024, North America held the largest share of the monocyte activation test (MAT) market, owing to its strong pharmaceutical industry, favorable regulatory scenario, and rising government R&D investments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Furthermore, rapidly increasing demand for endotoxin detection methods that are safe and swift is propelling the incorporation of MAT as part of day-to-day quality control procedures in the pharmaceutical industry. Canada and Mexico are beginning to implement MAT as they become more integral to global biopharma supply chains.

Europe is the second-largest and second fastest growing region of the monocyte activation test (MAT) market, driven mainly by stringent regulations. Ethical guidelines adhere to the 3Rs (Replacement, Reduction, and Refinement). In most cases, the region has switched away from legacy Rabbit Pyrogen Tests, and the European Pharmacopoeia has recognized MAT as a validated alternative. Dominated by Germany, which has a strong pharmaceutical industry, and has been an early adopter of in vitro testing technologies and investing in R&D. Other major players, including the U.K. and France, are also moving towards MAT adoption driven by stringent regulatory mandates and industry sustainability targets. With the increasing knowledge about animal-free testing, the expansion of MAT for use in academic, contract research, and industrial settings in Europe is anticipated.

Asia Pacific is the fastest-growing region in the monocyte activation test (MAT) market, due to growth in pharmaceutical manufacturing, vaccine production, and growing acceptance of alternative testing methods by regulatory bodies. The regional market is dominated by China on account of high investments in biotechnology infrastructure and increasing requirements for non-animal testing options. The presence of government support and domestic production of MAT kits has also boosted the growth. Another rapidly growing market is India, where increasing R&D of biologics, along with a move toward international quality standards, is driving demand. In light of a large number of patients and the growth in the incidence of infectious diseases, the demand for high-throughput and expandable pyrogen-detection approaches has increased. There are also countries, including Japan, South Korea, and Singapore, where usage is growing rapidly, led by factors such as technological progress and better medical regulatory conditions.

Monocyte Activation Test Market Key Players

Leading Monocyte Activation Test (MAT) companies operating in the market are Lonza Group, Charles River Laboratories, Bio-Rad Laboratories, Merck KGaA, Seikagaku Corporation, Hyglos GmbH, Wako Chemicals USA, Thermo Fisher Scientific, MAT BioTech, and Eurofins Scientific.

Recent Developments in the Monocyte Activation Test Market

In June 2024, FUJIFILM Wako released LumiMAT, a next-generation MAT kit based on the NOMO‑1 human cell line and luciferase reporter technology. The system delivers highly sensitive pyrogen detection within approximately 5 hours, offering improved reproducibility and stability over traditional PBMC-based MAT assays.

In October 2023, Lonza launched its PyroCell MAT Rapid System and Human Serum (HS) Rapid System, featuring the new PeliKine Human IL‑6 Rapid ELISA Kit. This innovation slashes testing time from up to two days down to just two hours, streamlining workflows and replacing reliance on rabbit testing.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 595 million |

| Market Size by 2032 | USD 1956.47 million |

| CAGR | CAGR of 16.07% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (MAT Kits, Reagents) • By Application (Drug Development, Vaccine Development, Medical Device Testing, and Others) • By Source (PBMC Based, Cell Line Based) • By End Use (Pharmaceutical Industry, Biotechnology Industry, Medical Device Industry, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Lonza Group, Charles River Laboratories, Bio-Rad Laboratories, Merck KGaA, Seikagaku Corporation, Hyglos GmbH, Wako Chemicals USA, Thermo Fisher Scientific, MAT BioTech, and Eurofins Scientific. |

Frequently Asked Questions

North America is the dominant region in the Monocyte Activation Test market.

High cost of validation, technical complexity, and limited awareness slow uptake.

The global monocyte activation test (MAT) market is being heavily driven by growing regulatory support and the rapid growth of the parenteral and biologic drug production.

By 2032, the Monocyte Activation Test Market is expected to reach USD 1956.47 million, up from USD 595 million in 2024.

The Monocyte Activation Test Market is projected to grow at a CAGR of 16.07% during the forecast period.

Get in Touch