Frequency Converter Market Report Scope & Overview:

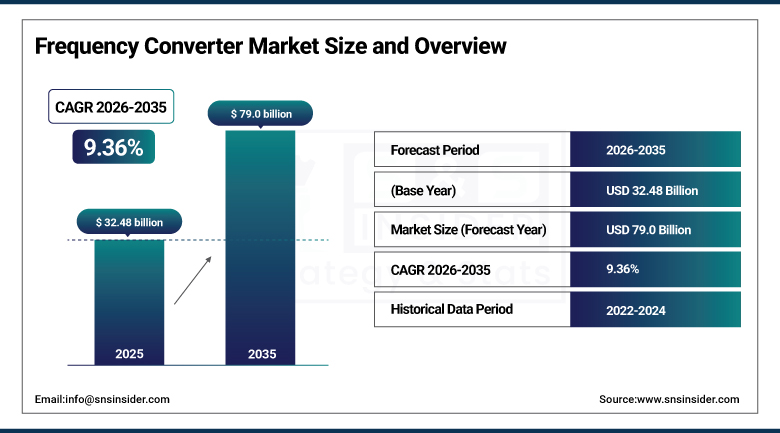

The Frequency Converter Market was valued at USD 32.48 billion in 2025 and is expected to reach USD 79.0 billion by 2035, growing at a CAGR of 9.36% from 2026-2035.

The market for frequency converters is expanding owing to the rising need for energy-efficient motor control systems in industries, HVAC systems, and renewable energy systems. Automation growth, growth in the manufacturing industry, and the use of VFDs improve efficiency. Besides, stringent energy policies and emphasis on power savings are other factors that contribute to the growth of the market.

The U.S. Department of Energy estimates that electric motors account for approximately 70% of all industrial electricity consumption. The DOE's Industrial Motor Systems Market Opportunities assessment identifies variable frequency drives and frequency converters as the highest-ROI single efficiency intervention available to industrial motor operators, with documented energy savings of 20-50% in variable-load applications.

Market Size and Growth Forecast

-

Market Size in 2025: USD 32.48 Billion

-

Market Size by 2035: USD 79.0 Billion

-

CAGR: 9.36% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Frequency Converter Market - Request Free Sample Report

Frequency Converter Market Trends

-

Digital frequency converters with IoT connectivity, AI-driven predictive maintenance, and smart monitoring capabilities are becoming the standard specification for new industrial automation projects.

-

Regenerative frequency converters that return braking energy to the power grid rather than dissipating it as heat are gaining adoption in crane, elevator, and winding applications where duty cycles involve frequent deceleration.

-

Compact, modular frequency converter designs are enabling integration into machine tools, robotics, and production line equipment at smaller footprints than previous generations required.

-

Offshore wind turbine generator systems are creating specialized large-capacity frequency converter demand for full-power converter applications that interface variable-speed generators with fixed-frequency grids.

-

Marine frequency converters enabling shore power connection (cold ironing) are growing as ports mandate that berthed ships use shore-supplied power rather than running diesel generators.

-

Medium-voltage frequency converters for high-power applications in mining, water utilities, and cement manufacturing are being specified with increasingly sophisticated power quality management features.

-

SiC (silicon carbide) power semiconductor technology adoption in frequency converters is improving switching efficiency and enabling more compact converter designs at higher power densities.

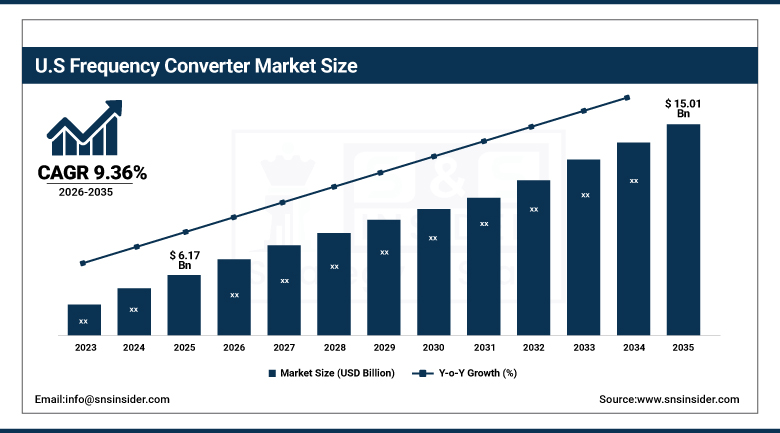

U.S. Frequency Converter Market Size Outlook:

The U.S. Frequency Converter Market was valued at USD 6.17 billion in 2025 and is expected to reach USD 15.01 billion by 2035, growing at a CAGR of 9.36% from 2026-2035. The US market for frequency converters is being propelled by robust industrial automation, stringent energy efficiency requirements, and growing HVAC and renewable energy industries. The increasing application of variable frequency drives within industry and infrastructural developments contributes to consistent demand in the field of motor control.

The U.S. Department of Energy's Better Plants program documents that participating industrial facilities achieve an average of 2.5% annual energy intensity reduction, with frequency converter deployment identified as a primary energy efficiency measure across manufacturing sectors. The U.S. Energy Information Administration reports that U.S. industrial sector electricity consumption exceeds 1,000 TWh annually, making motor energy optimization through frequency converters a material national energy security and climate strategy.

Frequency Converter Market Segment Analysis

-

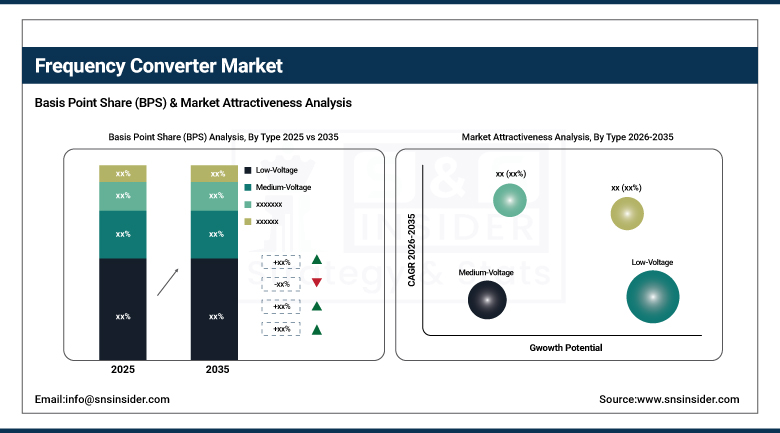

By Type, Low-Voltage Frequency Converters dominated the market with the largest share in 2025; Medium-Voltage growing fastest for heavy industrial applications.

-

By Application, Industrial Automation dominated the Frequency Converter Market in 2025; Oil & Gas and Marine segments growing steadily.

-

By End-Use, Manufacturing dominated the Frequency Converter Market in 2025; Energy & Power fastest growing.

By Type, Low-Voltage segment dominates the Frequency Converter Market, Medium-Voltage growing fastest

Low-voltage frequency converters held the dominant type position in 2025, driven by their widespread deployment in industrial automation, HVAC systems, and commercial buildings where the vast majority of motor applications operate at voltages below 1kV. Low-voltage frequency converters serve pump drives, fan drives, conveyor systems, compressors, and general-purpose motor applications that collectively represent the highest-volume motor population across manufacturing facilities and commercial buildings globally. The segment's dominance reflects both the breadth of applications and the relative cost-effectiveness of low-voltage converter technology, which has benefited from decades of development and manufacturing scale.

Medium-voltage frequency converters serving motor applications above 1kV typically in heavy industries including mining, oil and gas, power generation, water utilities, and cement manufacturing are growing at the fastest rate. High-power motor applications in these sectors involve pumps, compressors, mills, and fans where the absolute energy savings per converted unit are much larger than low-voltage applications, creating compelling individual project ROI calculations. The growing adoption of medium-voltage drives in offshore wind turbine generator converter systems is creating an additional demand driver as offshore wind capacity additions accelerate.

By Application, Industrial Automation dominates the Frequency Converter Market, Marine growing steadily

Industrial Automation maintained the dominant application position in the Frequency Converter Market in 2025, driven by manufacturing's fundamental dependence on precisely controlled motor drives for assembly lines, robotic systems, material handling, and production machinery. The global manufacturing capacity expansion particularly in automotive, electronics, food processing, and pharmaceuticals sustains consistent demand for frequency converters as the enabling technology for variable-speed industrial motor control. Industry 4.0 automation investments consistently specify frequency converters with digital communication capability as standard components in smart manufacturing equipment.

HVAC and Building Automation represents a large and growing application segment where frequency converters controlling air handling unit fans, cooling tower fans, chiller compressors, and variable-speed pumps deliver substantial energy savings in commercial buildings. Marine and Offshore applications including ship propulsion drives, winches, and thrusters represent a specialized high-value segment where frequency converter reliability under marine environmental conditions is the primary specification requirement, commanding premium pricing that sustains attractive market margins.

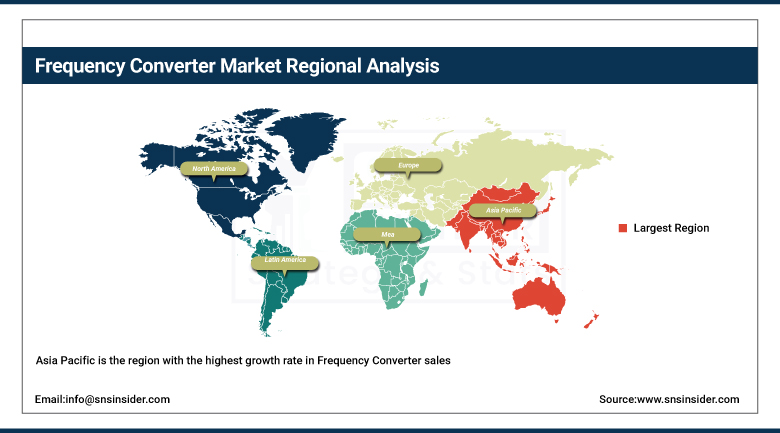

Frequency Converter Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

Asia Pacific |

China |

50% |

|

North America |

United States |

86% |

|

Europe |

Germany |

28% |

|

Middle East & Africa |

Saudi Arabia |

40% |

|

Latin America |

Brazil |

48% |

Asia Pacific Frequency Converter Market Insights

Asia Pacific is the region with the highest growth rate in Frequency Converter sales, thanks to the fast-paced industrialization in China, India, South Korea, and Southeast Asia, increased production capacity in industries such as automotive, electronics, and consumer products, and major projects in power plants and water works. China leads the global market in terms of the single country market size for frequency converters, using millions of units per year in its vast manufacturing base. The rapid growth in India's industrial capacity and large investments made in the water supply infrastructure industry, where frequency converters regulate the pump drive systems, are driving up domestic demand.

China's Ministry of Industry and Information Technology has identified energy-efficient motor systems including frequency converters as mandatory technology upgrades for industrial facilities under its Green Manufacturing Action Plan. India's Bureau of Energy Efficiency mandates frequency converter adoption in pump and fan applications above specified power thresholds under its Perform, Achieve and Trade scheme.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Frequency Converter Market Insights

The European Frequency Converter market is advanced technologically and demand is generated by government regulations on industrial energy efficiency, investments made by the automotive industry and machine tools manufacturing industry for automation purposes, and rising demands for large power converters from the offshore wind energy sector. Among the top frequency converter companies in the world are the ABB Group, Siemens AG, and Danfoss, all based in Europe. This gives Europe an advantage in terms of supply which allows the continent to maintain strong demand domestically as well as internationally through exports. Financial incentives include motor efficiency regulations as mandated by the Energy Efficiency Directive and EU ETS.

The EU Energy Efficiency Directive requires member states to achieve 11.7% reduction in energy consumption by 2030 compared to 2020 projections. The European Commission estimates that applying variable frequency drives to pump, fan, and compressor applications across European industry could deliver 20-30% energy savings in those motor systems, representing a multi-billion-euro annual energy cost reduction opportunity.

Middle East & Africa and Latin America Frequency Converter Market Insights

Market for Frequency Converters in Middle East & Africa and Latin America is expanding consistently, fueled by investments in infrastructure projects, energy efficiency campaigns, and growth in the industrial sector in nations like Brazil, South Africa, and the United Arab Emirates. Investments in water treatment plants, oil & gas sector, and power generation projects are increasing the need for frequency converters in pumps and compressors. The industrial sector in Brazil and its mining industry are generating high demand for motor controls, while the Middle East is concentrating on HVAC projects and desalination plants.

North America Frequency Converter Market Insights

The North America Frequency Converter Market is advanced and technology-intensive and consists of the United States and Canada. There is high demand for frequency converters in the areas of industrial automation, heating, ventilation, and air conditioning, and renewable energy. Energy efficiency regulations coupled with the modernization of existing infrastructures have fueled the need for frequency converters in this market, especially in manufacturing and utility industries. In the United States, there is an initiative to promote energy-efficient motor systems that use frequency converters.

Frequency Converter Market Growth Drivers:

-

Industrial automation expansion and energy efficiency mandates driving sustained global frequency converter market demand

The frequency converter industry has a solid demand structure that has existed for decades and is being bolstered today through new regulatory pressures which mean that energy efficiency expenditures are no longer voluntary choices. Any industrial operation transitioning from fixed speed motor usage to variable frequency drives can demonstrate tangible savings on their energy bills that allow for a positive return on investment on the converters themselves, usually within 1-3 years, an economic argument that was always strong but is made stronger today by carbon costs, energy price fluctuations, and ESG reporting pressures that turn energy efficiency into a corporate governance matter as well as an economic one. Industrial capacity additions fueled by the rise of nearshoring, semiconductor production, and electric vehicle manufacturing create new opportunities for frequency converter sales at industrial plants designed with variable speed motors from day one.

The International Energy Agency estimates that motor-driven systems account for 45% of global electricity consumption. IEA analysis documents that optimizing motor system performance through variable speed drives could reduce global industrial electricity consumption by 10-15%, representing one of the single largest identifiable energy efficiency opportunities available.

Frequency Converter Market Restraints:

-

High upfront capital cost and harmonic distortion challenges limiting frequency converter adoption in cost-sensitive markets

Even though there is clear evidence about energy savings ROI for frequency converters, their application is hindered by high costs especially in smaller industries and emerging economies, where financial considerations are stricter and payback period analyses have a shorter timeline compared to other industrial practices. The investment cost for frequency converters consisting of the cost of the drive unit itself, installation charges, cabling, and in some instances, harmonic filtration system can reach several times the cost of a conventional motor starter system, posing capital budget challenges for SME manufacturers, which do not have easy access to the financing of energy-saving measures as seen among larger industrial corporations. The creation of distorted voltages and currents through harmonic distortions created by frequency converters needs to be resolved through filtering techniques.

Frequency Converter Market Opportunities:

-

Offshore wind energy and smart manufacturing digitalization creating new high-value frequency converter growth opportunities globally

There are two factors that will ensure the market's growth rate exceeds its current path from now on. The first one is the development of offshore wind energy. Full-scale converter systems used to connect variable-speed permanent magnet generators to fixed-frequency offshore grid infrastructure have to employ high-capacity power converter systems, which can be considered an expensive component of each turbine's bill of material. Considering the increasing numbers of installations of offshore wind farms in North Sea, US Atlantic coast, and Asia-Pacific regions, the aggregate demand for power converters will create a lucrative segment for already existing frequency converter vendors equipped with electrical engineering skills capable of serving megawatt-scale power conversion needs. Smart manufacturing digitalization is another factor that will ensure sustainable growth of the market. With more factories implementing Industry 4.0 solutions, the use of frequency converters connected to IoT and controlled by artificial intelligence to serve as an interface between digital control systems and electric motors is inevitable.

Recent Developments:

-

2026: ABB launched its ACS880 Series II industrial drive with integrated IIoT connectivity and edge AI predictive maintenance capability, providing real-time motor health analysis that predicts bearing failures, winding degradation, and cooling system issues up to 6 weeks before failure based on vibration, temperature, and electrical signature monitoring embedded within the drive.

-

2025: Siemens introduced its SINAMICS G120X frequency converter with native PROFINET and OPC UA connectivity and an integrated cybersecurity module meeting IEC 62443 Level 2 requirements, targeting manufacturing facilities deploying converters in IIoT-connected production environments where operational technology cybersecurity is a procurement requirement.

-

2025: Danfoss released its VLT AutomationDrive FC 302 with SiC power module technology, achieving 98.5% power conversion efficiency a 1.5 percentage point improvement over the previous generation reducing heat dissipation in drive panels and enabling 30% smaller enclosure designs for space-constrained machine tool and packaging machinery applications.

Frequency Converter Companies are:

-

ABB Ltd

-

Siemens AG

-

Schneider Electric SE

-

Rockwell Automation Inc

-

Eaton Corporation plc

-

Mitsubishi Electric Corporation

-

Yaskawa Electric Corporation

-

Nidec Corporation

-

WEG S.A.

-

Hitachi Ltd

-

Parker Hannifin Corporation

-

Emerson Electric Co

-

GE Vernova

-

Honeywell International Inc

-

Beckhoff Automation GmbH & Co. KG

-

Bosch Rexroth AG

-

Invertek Drives Ltd

-

Control Techniques (Nidec)

Frequency Converter Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 32.48 Billion |

| Market Size by 2035 | USD 79.0 Billion |

| CAGR | CAGR of 9.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Low-Voltage Frequency Converters, Medium-Voltage Frequency Converters, High-Voltage Frequency Converters) • By Application (Industrial Automation, HVAC & Building Automation, Oil & Gas, Marine & Offshore, Power Generation, Others) • By End-Use (Manufacturing, Energy & Power, Oil & Gas, Marine, Construction, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd.; Siemens AG; Danfoss A/S; Schneider Electric SE; Rockwell Automation Inc.; Eaton Corporation plc; Mitsubishi Electric Corporation; Fuji Electric Co., Ltd.; Yaskawa Electric Corporation; Nidec Corporation; WEG S.A.; Hitachi Ltd.; Parker Hannifin Corporation; Emerson Electric Co.; GE Vernova; Honeywell International Inc.; Beckhoff Automation GmbH & Co. KG; Bosch Rexroth AG; Invertek Drives Ltd.; Control Techniques |

Frequently Asked Questions

Asia Pacific dominated the Frequency Converter Market in 2023.

The Aerospace & Defense segment dominated the Frequency Converter Market in 2023.

The major growth factor of the frequency converter market is the increasing demand for energy-efficient systems and automation across various industries.

Frequency Converter Market size was USD 27.15 billion in 2023 and is expected to Reach USD 60.60 billion by 2032.

The Frequency Converter Market is expected to grow at a CAGR of 9.36% during 2024-2032.

Get in Touch