Gasoline Direct Injection Market Report Scope & Overview:

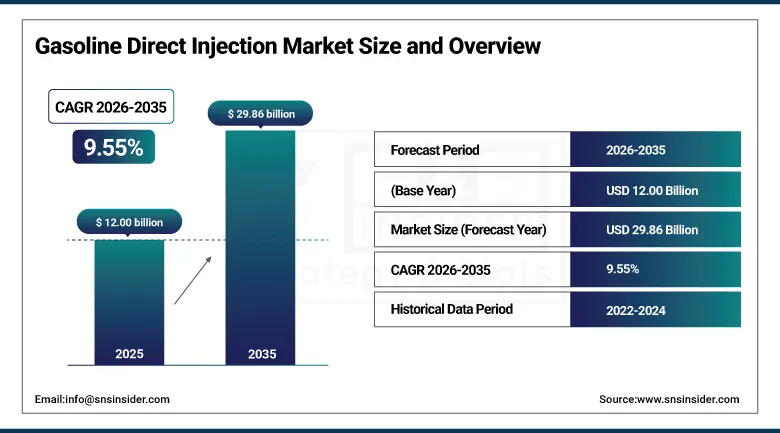

The Gasoline Direct Injection Market was valued at USD 12.00 billion in 2025 and is expected to reach USD 29.86 billion by 2035, growing at a CAGR of 9.55% from 2026-2035.

The growth of the Gasoline Direct Injection Market is driven by rising demand for fuel-efficient and high-performance cars around the world. The strict emission norms are compelling automobile companies to use sophisticated injection technologies, which will help in reducing the amount of carbon emissions and improving fuel combustion efficiency. The rising production of passenger cars and the growing trend of turbochargers in vehicles will further contribute to the growth in the market. Moreover, the developments in the field of fuel injectors, sensors, and control electronics are further boosting the performance and effectiveness of such systems.

According to the International Energy Agency (IEA), global CO₂ emissions from the transport sector account for nearly 24% of total energy-related emissions, increasing pressure on automakers to adopt advanced combustion technologies such as GDI to improve fuel efficiency and reduce emissions.

Market Size and Forecast

-

Market Size 2026E: USD 13.14 Billion

-

Market Size 2035: USD 29.86 Billion

-

CAGR (2026-2035): 9.55%

-

Fastest Growing Market: Asia Pacific

-

Largest Market: North America

To Get more information on Gasoline Direct Injection Market - Request Free Sample Report

Gasoline Direct Injection Market Trends

-

Rising demand for fuel-efficient and high-performance vehicles is driving the gasoline direct injection (GDI) market.

-

Growing adoption across passenger cars and light commercial vehicles is boosting market growth.

-

Expansion of automotive production and tightening emission regulations is fueling technology deployment.

-

Increasing focus on improved combustion efficiency, reduced fuel consumption, and lower CO₂ emissions is shaping adoption trends.

-

Advancements in high-pressure fuel injection systems, precision injectors, and engine control technologies are enhancing performance.

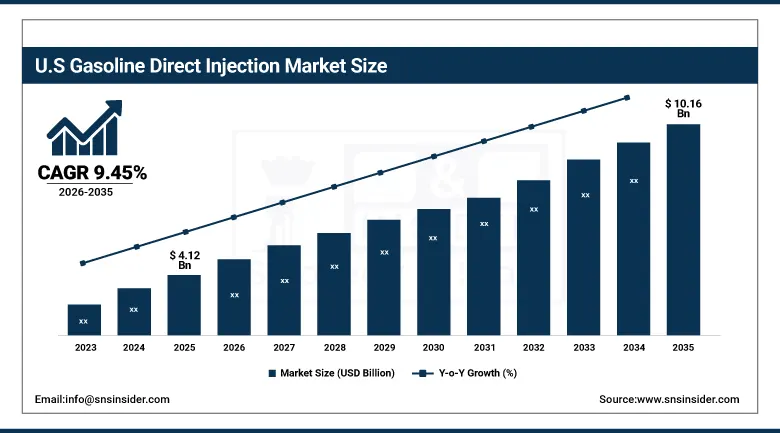

U.S. Gasoline Direct Injection Market Size Outlook

The U.S. Gasoline Direct Injection Market was valued at USD 4.12 billion in 2025 and is expected to reach USD 10.16 billion by 2035, growing at a CAGR of 9.45% from 2026-2035.

The U.S. Gasoline Direct Injection Market growth is driven by increasing demand for energy-efficient and powerful automobiles and emissions standards focused on lowering carbon emissions. The rising trend of turbocharged engines and innovations in engines contributes positively towards the growth of the market. The prominence of key automotive brands and constant improvements in fuel injection systems improve the efficiency and reliability of vehicles. Moreover, the growing customer inclination towards SUVs and luxury cars coupled with advancements in injectors and electronic control modules plays a key role in driving the growth of the market.

The U.S. Department of Energy (DOE) states that advanced gasoline direct injection systems can improve fuel economy by up to ~10–15% compared to conventional port fuel injection systems, depending on engine design and driving conditions.

Gasoline Direct Injection Market Segment Analysis

-

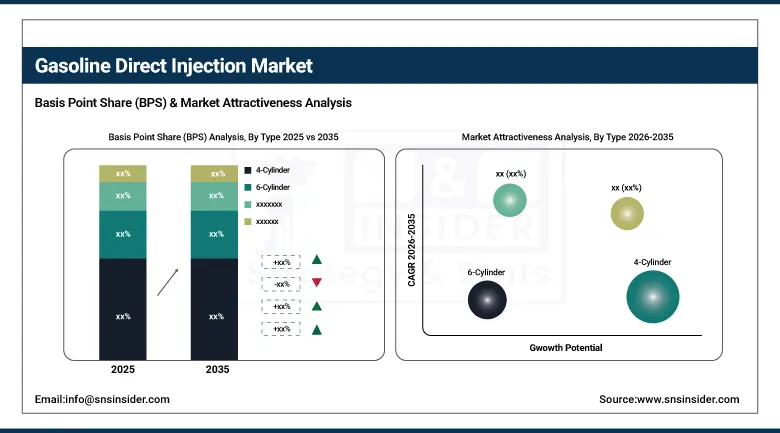

By Type, 4-cylinder segment dominated the gasoline direct injection market in 2025 with 46% share; 6-cylinder segment is the fastest growing segment.

-

By Component, fuel injectors segment dominated the market in 2025 with 41% share; electronic control units (ECUs) segment is the fastest growing segment.

-

By Vehicle Type, passenger cars segment dominated the market in 2025 with 72% share; light commercial vehicles (LCVs) segment is the fastest growing segment.

By Type, 4-cylinder segment dominates the gasoline direct injection market, 6-cylinder segment is the fastest growing

The 4-cylinder segment dominated the gasoline direct injection market owing to the ideal combination of fuel efficiency, performance, and cost effectiveness. The engines have wide applications in passenger cars as they provide better fuel efficiency than larger engine categories. Automakers opt for 4-cylinder gasoline direct injection engines owing to the ease of meeting emission norms and being economically viable for the production of affordable vehicles. Furthermore, strong consumer demand for compact and mid-sized sedans, combined with the need for fuel-efficient engines, has strengthened the position of 4-cylinder engines in the gasoline direct injection market.

The 6-cylinder segment is the fastest growing in the gasoline direct injection market owing to rising demand for power and performance in luxury cars. Engines under the category were increasingly incorporating advanced GDI technology to boost fuel efficiency while providing greater torque and acceleration. Rising preference of consumers for luxury SUVs and sports cars is expected to drive the trend. Moreover, the growing popularity of technologies such as turbo charging and innovations related to engine downsizing will enable efficient utilization of 6-cylinder engines in passenger and light commercial vehicles.

By Component, fuel injectors segment dominates the gasoline direct injection market, electronic control units (ecus) segment is the fastest growing

The fuel injectors segment dominated the gasoline direct injection market owing to its crucial role in providing accurate fuel delivery, efficient combustion, and engine performance. The fuel injector is an important element of a GDI system as it allows for fuel atomization under high pressure directly inside the combustion chamber. Furthermore, their extensive application across all engines and their requirement in terms of replacement as well as incorporation in new vehicles also contributed to their segment dominance. Lastly, there has been an increased emphasis on the use of fuel-efficient technologies that have increased their use in automotive manufacturing worldwide.

The electronic control units (ECUs) segment is the fastest growing in the gasoline direct injection market owing to rising use of advanced engine management systems in modern vehicles. Electronic control units have been gaining increasing importance because of their key function of managing the fuel injection process in terms of timing and pressure in order to achieve optimal performance and reduce emissions from engine operation. Increased adoption of vehicle electrification and tough emission regulations have driven a growing need for advanced engine controls managed via software solutions.

By Vehicle Type, passenger cars segment dominates the gasoline direct injection market, light commercial vehicles segment is the fastest growing

The passenger cars segment dominated the gasoline direct injection market owing to high vehicle manufacturing in addition to high consumer demand for energy-efficient and performance-oriented vehicles. The GDI engine system is predominantly used in passenger cars to increase power output, improve mileage and cut down emissions. Urbanization trends, rising incomes and increasing vehicle ownership have resulted in this segment dominating. Moreover, emission regulations, coupled with consumer preference for high-performance engines in compact/mid-size cars have ensured the dominance of the passenger car segment in the gasoline direct injection market.

The light commercial vehicles segment is the fastest growing in the gasoline direct injection market owing to high demand for energy-efficient and emission-controlled engine systems in logistics, delivery and other similar commercial activities. The application of the gasoline direct injection system helps improve efficiency both in terms of payload and mileage. Growing e-commerce trends and logistics have led to increased usage of LCVs. In addition to that, strict emission regulations coupled with demands for more cost-effective and productive fleet operations have helped LCV segment gain traction in the market.

Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

90.1% |

|

Europe |

United Kingdom |

24.3% |

|

Asia Pacific |

China |

56.9% |

|

Middle East & Africa |

UAE |

13.8% |

|

Latin America |

Brazil |

50.7% |

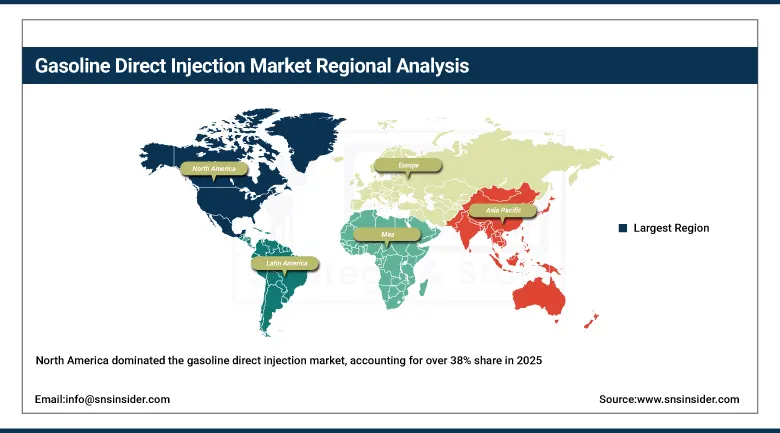

North America Gasoline Direct Injection Market Insights

North America dominated the gasoline direct injection market, accounting for over 38% share in 2025 owing to the presence of high automotive production and early adoption of latest technology engines. Stringent emission norms are among the major factors contributing towards high regional market shares, along with the growing popularity of fuel-efficient and low-emission technology. Growing demand for passenger automobiles, particularly sports utility vehicles and performance vehicles, boosts the market adoption. The presence of prominent automotive OEMs and suppliers is yet another growth factor in favor of the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Gasoline Direct Injection Market Insights

Europe gasoline direct injection market is primarily fueled by stringent emission standards and high focus on fuel efficiency by automakers. The growing preference for low emission passenger cars along with the prevalence of turbo engines contributes to the rapid uptake of the GDI technology. An extensive presence of automotive manufacturing industries coupled with consistent innovation is propelling the market forward. Another factor that is encouraging the uptake of GDI technology is the growing trend towards hybridization and electrification.

The European Environment Agency (EEA) highlights that passenger cars must meet progressively stricter CO₂ targets, including fleet-wide reductions to around 93.6 g CO₂/km (EU target framework), pushing OEMs toward high-efficiency direct injection systems and turbocharged engines.

Asia Pacific Gasoline Direct Injection Market Insights

The Asia Pacific region is witnessing rapid growth in the GDI market, with a CAGR of 10.67% anticipated throughout the forecast period. Increasing demand from the automobile sector, expanding automotive industry, and increased demand for efficient automobiles are the major drivers of this growth. Factors such as increasing urbanization and disposable income levels are helping increase the demand for passenger vehicles in emerging economies. Apart from that, the presence of automotive manufacturing bases and growing use of advanced engine technology are driving growth in the GDI market.

Middle East & Africa and Latin America Gasoline Direct Injection Market Insights

Middle East & Africa and Latin America gasoline direct injection market is witnessing steady growth due to factors such as an increase in vehicle ownership and better automotive infrastructure. Urbanization and increased populations of the middle class in these regions are leading to higher consumer demand for vehicles and more fuel-efficient products. Although there are few regulations on emissions and the technology is rather expensive, the entry of international car companies and increased awareness about fuel efficiency are aiding its growth.

Market Dynamics

Growth Drivers: Rising demand for fuel efficient and high performance engines driving gasoline direct injection adoption globally

Increasing focus on fuel economy and tightening emissions standards in major automobile-producing countries is driving the use of gasoline direct injection technology. The increasing installation of GDI systems in cars by vehicle manufacturers is being done due to its ability to improve the efficiency of the combustion process and increase power output while decreasing the amount of fuel used. An increase in the trend toward purchasing automobiles that are powerful but efficient with regard to fuel economy is further boosting growth in the sector. Furthermore, legislation focused on decreasing CO₂ emissions is forcing automobile manufacturers to replace their existing port fuel injection system with GDI systems. Improvements in technology relating to injectors, fuel pumps, and engine control systems have enhanced the capabilities of GDI systems.

Restraints: High carbon buildup and maintenance complexity limiting gasoline direct injection system reliability and adoption growth

There are various obstacles that exist in GDI systems due to the buildup of carbon deposits in the intake valves, causing inefficiencies in the engine's functioning. This increases maintenance needs and incurs extra costs for maintenance. Besides, due to their complexities relative to other fuel injection systems, repairs of GDI require extra expenses and even sophisticated diagnostic equipment. All these contribute to their unpopularity in markets where cost is an important consideration when buying a car. Inconsistent quality of gasoline in different areas adds to the engine deposit problems as well. Car manufacturers need to include some advanced technology in their designs, including dual injection systems or cleaning methods, which increase their cost.

Opportunities: Increasing integration of gasoline direct injection in hybrid and turbocharged engine platforms creating strong growth opportunities

There are great opportunities in the increased use of hybrid cars and turbocharged engines which are boosting the growth of the GDI technology market. GDI systems are highly useful in ensuring the effective combustion of gasoline and fuel efficiency in hybrid powertrains and hence become one of the main parts of the future cars. Combining GDI with the use of turbocharging has been becoming common among automobile manufacturers for getting more power while still maintaining fuel efficiency and adhering to emission levels. This trend has been more dominant in the regions that are concentrating on electric vehicles and fuel economy. Increasing research into new automotive technologies is another factor behind the advancements in GDI systems. Also, the growing popularity of high-performance cars is contributing greatly to the growth of the market.

Recent Developments:

-

2026: Bosch continued scaling its next-generation gasoline direct injection portfolio, focusing on high-pressure injector systems designed for turbocharged ICE engines. Bosch emphasized improved spray precision and emissions reduction supporting EU7-ready combustion systems and hybrid ICE optimization platforms.

-

2025: Continental expanded its engine management and fuel injection system portfolio, integrating advanced GDI control units with ECU optimization for improved fuel efficiency and lower particulate emissions in gasoline turbo engines used by global automakers.

-

2025: BorgWarner expanded its fuel system and air management technologies, supporting gasoline direct injection platforms with improved turbocharging compatibility and combustion efficiency enhancements for downsized ICE engines.

-

2024: Marelli developed high-pressure fuel injector systems reaching advanced pressure levels, supporting next-generation GDI engines with improved combustion efficiency and emissions reduction capability for ICE platforms.

-

2024: Stanadyne advanced its GDI fuel pump and injector systems, focusing on high-pressure gasoline injection components designed to improve durability and precision fuel delivery in turbocharged gasoline engines.

-

2023: Continental announced development of advanced gasoline direct injection systems for hybrid platforms, integrating fuel injection with engine control software to improve efficiency and reduce emissions in electrified ICE vehicles.

Gasoline Direct Injection Market Key Players are:

-

Robert Bosch GmbH

-

Denso Corporation

-

BorgWarner Inc.

-

Continental AG

-

Hitachi Astemo Ltd.

-

Marelli Corporation

-

Aisin Corporation

-

TI Automotive Inc.

-

Stanadyne LLC

-

Vitesco Technologies Group

-

MAHLE GmbH

-

Rheinmetall Automotive AG

-

Mikuni Corporation

-

Keihin Corporation

-

Cummins Inc.

-

Eaton Corporation

-

Woodward Inc.

-

Siemens VDO

-

Hitachi Ltd.

-

Johnson Matthey

Gasoline Direct Injection Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 12.00 Billion |

| Market Size by 2035 | USD 29.86 Billion |

| CAGR | CAGR of 9.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (4-Cylinder, 6-Cylinder, 8-Cylinder, Others) • By Component (Fuel Injectors, Fuel Pumps, Electronic Control Units (ECUs), Sensors, Others) • By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Robert Bosch GmbH, Denso Corporation, BorgWarner Inc., Continental AG, Hitachi Astemo Ltd., Marelli Corporation, Aisin Corporation, TI Automotive Inc., Stanadyne LLC, Vitesco Technologies Group, MAHLE GmbH, Rheinmetall Automotive AG, Mikuni Corporation, Keihin Corporation, Cummins Inc., Eaton Corporation, Woodward Inc., Siemens VDO, Hitachi Ltd., Johnson Matthey |

Frequently Asked Questions

North America dominated the Gasoline Direct Injection Market in 2025.

The 4-Cylinder segment dominated the Gasoline Direct Injection Market in 2025.

The Gasoline Direct Injection Market was valued at USD 12.00 billion in 2025.

The Gasoline Direct Injection Market is expected to grow at a CAGR of 9.55% from 2026 to 2035.

Get in Touch