Gelcoat Market Report Scope & Overview:

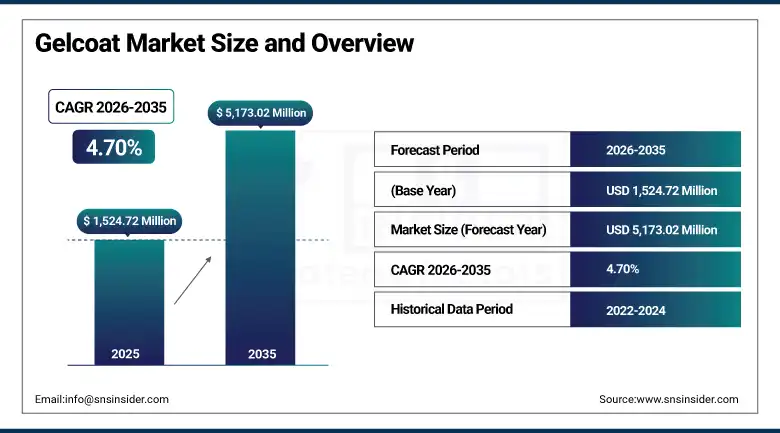

The Gelcoat Market was valued at USD 1,524.72 Million in 2025 and is expected to reach USD 5,173.02 Million by 2035, growing at a CAGR of 4.70% from 2026–2035.

The global gelcoat market is growing at a steady and commercially broad-based pace. Gelcoat is a specially formulated surface coating applied to fiber-reinforced composite materials during the molding process. Applied as the first layer in the composite fabrication process before the structural laminate, gelcoat becomes an integral part of the composite structure whose protective and aesthetic performance is critical to the final product’s commercial acceptance in marine, construction, wind energy, and transportation applications. The market is witnessing steady growth fueled by rising demand in marine, wind energy, and transportation sectors, with raw material availability and pricing trends in polyester, vinyl ester, and epoxy resins significantly impacting cost structure and market profitability.

In 2024, Ashland Inc. launched its new Derakane Momentum epoxy vinyl ester gelcoat series specifically formulated for wind turbine blade leading edge protection, addressing the erosion damage that wind turbine blades accumulate from rain, hail, and particle impact whose cumulative aerodynamic degradation reduces turbine energy output and creates costly mid-life refurbishment requirements. The leading-edge protection gelcoat’s superior toughness and erosion resistance relative to conventional polyester alternatives creates commercial differentiation in the wind energy sector’s growing blade protection market.

Gelcoat Market Size and Forecast

-

Market Size in 2026E: USD 1,596.38 Million

-

Market Size by 2035: USD 5,173.02 Million

-

CAGR: 4.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Gelcoat Market - Request Free Sample Report

Gelcoat Market Trends

-

Wind turbine blade gelcoat innovation is improving leading edge erosion resistance through enhanced toughness and flexibility compared to conventional polyester gelcoats.

-

Low-styrene and styrene-free gelcoat formulations are expanding due to REACH regulations and VOC emission restrictions in Europe.

-

Colored and pigmented gelcoat demand is increasing in marine leisure and construction sectors driven by design customization and aesthetic preferences.

-

Bio-based gelcoat resins using renewable polyester content are gaining traction as sustainable alternatives in marine and construction applications.

-

Self-cleaning and anti-fouling gelcoat technologies are emerging in marine applications to reduce fouling, maintenance costs, and improve vessel efficiency.

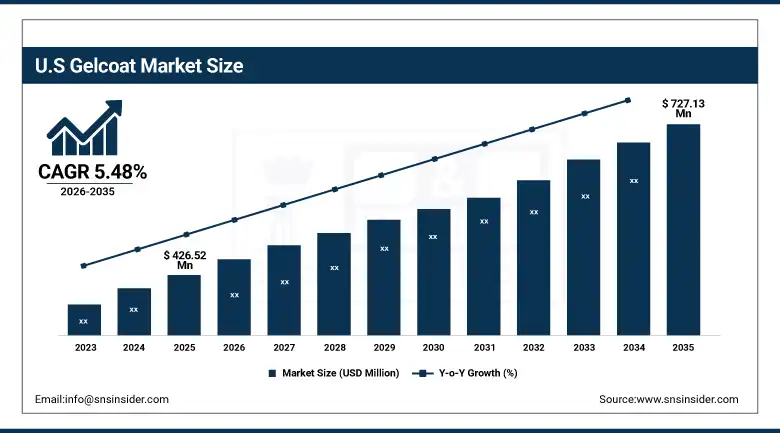

The U.S. Gelcoat Market Outlook

The U.S. gelcoat market was valued at approximately USD 426.52 Million in 2025 and is expected to reach approximately USD 727.13 Million by 2035, growing at a CAGR of approximately 5.48%.

The U.S. is the most commercially significant gelcoat market within North America’s dominant revenue position. Ashland Inc., INEOS Composites, and Polynt Reichhold’s U.S. operations serve the domestic market across marine, construction, transportation, and wind energy applications. The U.S. recreational boating market’s fiberglass boat production creates consistent marine gelcoat procurement whose volume scales with the marine leisure sector’s activity level. The wind energy sector’s extraordinary turbine installation pace creates growing blade gelcoat demand, and the construction sector’s fiberglass-reinforced plastic panel and fixture production creates consistent industrial procurement.

Scott Bader expanded its Crystic gelcoat range in 2024 with new environmentally compliant low-styrene formulations for the European and North American marine manufacturing market, achieving EU workplace exposure limits without compromising the application characteristics and surface quality that boat builders require. The reformulation investment reflects the commercial necessity of regulatory compliance whose worker health and environmental requirements create mandatory product development investment for gelcoat suppliers serving regulated markets.

Gelcoat Market Segment Analysis

-

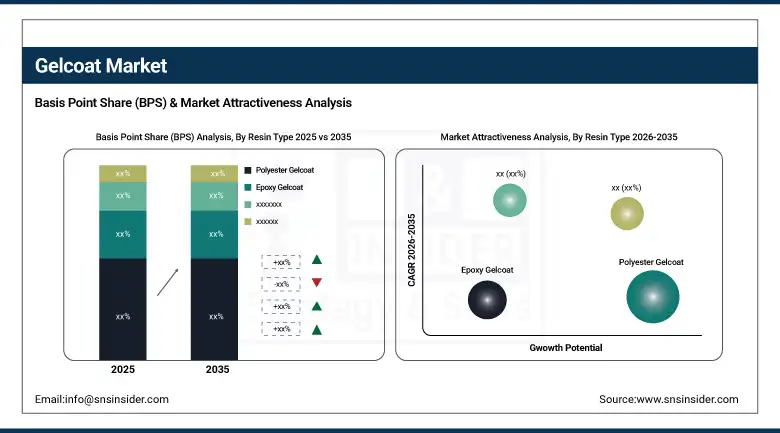

By Resin Type, the polyester gelcoat segment dominated the market with 52.8% share in 2025, while the epoxy gelcoat segment is the fastest growing as wind energy turbine blade leading edge protection, aerospace composite, and high-performance marine applications requiring superior chemical resistance and structural integrity drive above-average adoption.

-

By Application, the marine segment dominated the market with approximately 38% share in 2025, while the wind energy segment is the fastest growing as turbine blade leading edge protection, nacelle cover, and hub component composite manufacturing create above-average gelcoat demand that compounds with global wind energy installation growth.

-

By End User, the construction segment dominated the market with approximately 35% share in 2025, while the transportation segment is the fastest growing as automotive composite body panel, commercial vehicle fiberglass cab, and rail vehicle composite shell production create above-average gelcoat adoption driven by lightweighting requirements.

By Resin Type, polyester dominates, epoxy grows fastest

Polyester gelcoat retained the dominant resin type position with 52.8% of the gelcoat market in 2025. Polyester’s commercial primacy reflects its position as the most cost-effective gelcoat resin system whose unsaturated polyester chemistry creates a commercially accessible price point. The established manufacturing infrastructure, broad supplier availability, and application simplicity of polyester gelcoat whose brush, roller, and spray application at ambient temperature creates technical accessibility for composite fabricators without specialized equipment create specification continuity across the global composite manufacturing base. Pigmentation versatility and color matching capability sustain polyester’s dominance in marine leisure and construction design-sensitive applications.

Epoxy gelcoat is the fastest-growing resin type because wind energy’s turbine blade leading edge erosion protection requirement creates structured demand for epoxy’s superior toughness, elongation at failure, and chemical resistance that polyester alternatives cannot provide under the cumulative erosion impact of rain, hail, and airborne particle impact at blade tip speeds exceeding 80 m/s. Ashland’s Derakane Momentum launch demonstrates the commercial investment in wind energy-specific epoxy gelcoat formulation whose performance advantage creates premium pricing that sustains above-average segment revenue growth.

By Application, marine dominates, wind energy grows fastest

Marine retained the dominant application position with approximately 38% of the gelcoat market in 2025. The global recreational and commercial boating industry’s fiberglass composite construction dependence creates consistent gelcoat procurement whose aggregate across millions of boats and vessels in production and maintenance creates the largest single application category. Each fiberglass boat hull requires gelcoat for the outer surface protection and aesthetic finish whose replacement during refurbishment and repair creates aftermarket procurement that sustains marine application’s commercial leadership beyond new vessel production.

Wind energy is the fastest-growing application because the extraordinary global wind turbine installation pace, combined with the growing recognition of blade leading edge erosion’s operational impact on turbine energy output, is creating structured gelcoat procurement from both new blade manufacturing and erosion repair programmes. Each new wind turbine’s three blades create blade leading edge protection gelcoat procurement whose aggregate across tens of gigawatts of annual new wind capacity creates commercial scale.

By End User, construction dominates, transportation grows fastest

Construction retained the dominant end-user position with approximately 35% of the gelcoat market in 2025. The building and construction sector’s broad gelcoat application encompassing fiberglass bathroom fixtures, bathtubs and shower trays, architectural facade panels, swimming pool shells, water tanks, and structural composite elements creates diverse procurement channels whose combined volume sustains construction’s aggregate commercial dominance. Each new residential and commercial building project creates construction gelcoat procurement across multiple application categories whose combined per-project volume sustains the end-user category’s market leadership.

Transportation is the fastest-growing end user because the automotive and commercial vehicle sector’s systematic adoption of fiberglass composite body panels and structural components creates above-average gelcoat procurement growth from a previously smaller application base. Each commercial vehicle that replaces steel cab components with fiberglass composite alternatives creates gelcoat procurement whose per-vehicle content compounds with commercial vehicle fleet electrification’s weight reduction motivation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

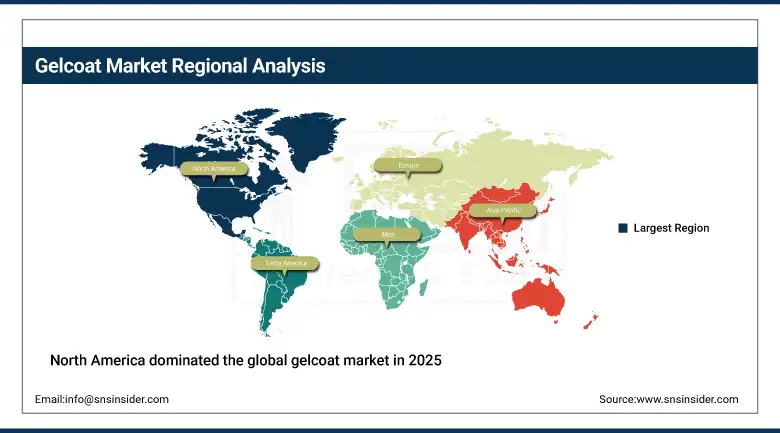

North America Gelcoat Market Insights

North America dominated the global gelcoat market in 2025 as the most commercially sophisticated fiberglass composite manufacturing region. The United States accounts for approximately 87.4% of North American revenues through Ashland Inc., INEOS Composites, and Polynt Reichhold’s commercial operations whose combined portfolio serves the domestic marine, construction, wind energy, and transportation gelcoat markets. The U.S. recreational boating industry’s annual production of hundreds of thousands of fiberglass vessels creates consistent marine gelcoat procurement, while the construction sector’s fiberglass fixture and panel production creates stable industrial demand.

Canada contributes approximately 12.6% of North American revenues through its recreational marine sector, the construction industry’s fiberglass fixture production, and the wind energy sector’s growing turbine blade procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Gelcoat Market Insights

Europe is a technically sophisticated gelcoat market where EU REACH’s styrene exposure limits are driving the most commercially significant gelcoat reformulation investment in the market’s history. Germany accounts for approximately 22.3% of European revenues through its advanced wind energy turbine manufacturing, the chemical industry’s gelcoat resin supply, and the boat building industry’s established fiberglass composite production. Ashland, Scott Bader, and Allnex’s European commercial operations define the regional supply landscape.

France, the Netherlands, and Italy are significant secondary markets where boat building tradition, wind energy installation, and construction composite production create consistent gelcoat procurement. Scott Bader’s UK headquarters and Allnex’s European network sustain domestic supply capability that reduces Asian import dependence for European composite manufacturers.

Asia Pacific Gelcoat Market Insights

Asia Pacific is the fastest-growing regional gelcoat market, driven by rapid expansion in construction, marine, and wind energy sectors across China, India, South Korea, and Southeast Asia. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary wind turbine blade production scale, the shipbuilding industry’s fiberglass composite adoption, and the construction sector’s fiberglass fixture manufacturing. China’s position as the world’s largest wind turbine manufacturer creates the most commercially significant wind energy gelcoat procurement globally.

India and South Korea are significant secondary markets where boat building, wind energy installation, and construction composite production create consistent gelcoat procurement. India’s government’s wind energy expansion target creates growing turbine blade gelcoat demand, and the rapidly expanding construction sector’s fiberglass panel adoption creates above-average first-time procurement growth.

MEA & Latin America Gelcoat Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its boat building sector, construction composite production for the extraordinary infrastructure development programme, and the growing wind energy sector’s turbine blade procurement. Brazil leads Latin American revenues at approximately 44.2% through its established boat building industry, construction sector’s fiberglass fixture production, and the growing wind energy sector whose onshore wind expansion creates turbine blade gelcoat demand.

UAE’s luxury yacht market and South Africa’s boat building and construction sectors create significant MEA secondary markets whose gelcoat procurement reflects the respective national composite manufacturing capabilities.

Market Dynamics

Growth Drivers: Wind energy blade production creating premium epoxy gelcoat demand and marine sector sustained procurement

Wind energy’s extraordinary global installation pace is the gelcoat market’s most commercially dynamic growth driver. The IEA’s projection of over 2,000 GW cumulative wind capacity by 2030 creates turbine blade manufacturing procurement whose gelcoat component grows proportionally with each new blade set’s leading edge protection requirement. Beyond new blade production, the operational wind fleet’s leading edge erosion repair programme creates growing aftermarket gelcoat procurement whose commercial scale reflects the cumulative global fleet’s multi-decade blade service life requiring periodic protective surface restoration. Each offshore wind turbine’s above-average erosion rate from marine environment airborne particle density creates premium leading edge protection specification that sustains above-commodity gelcoat pricing in the wind energy application.

The marine sector’s sustained gelcoat procurement reflects recreational boating’s above-average consumer engagement in leisure activities and the commercial marine industry’s consistent vessel construction and refurbishment investment. The global recreational marine market’s post-pandemic growth trajectory, whose leisure time and outdoor recreation investment sustained above-average boat purchase activity, creates consistent fiberglass vessel production procurement.

Restraints: Styrene regulation constraining conventional formulation and raw material price volatility

EU REACH Regulation’s occupational exposure limit for styrene at 50 ppm, combined with proposals for further reduction, creates reformulation investment requirements for conventional polyester and vinyl ester gelcoat formulations whose styrene monomer content substantially exceeds regulatory thresholds in standard open-mould application processes. Each gelcoat manufacturer that invests in low-styrene or styrene-free formulation development creates R&D cost whose commercial recovery requires premium pricing that creates adoption resistance in cost-sensitive construction and sanitary ware applications.

Polyester, vinyl ester, and epoxy resin raw material price volatility, driven by crude oil and naphtha price cycles and global chemical supply chain dynamics, creates gelcoat production cost uncertainty that limits manufacturer pricing predictability.

Opportunities: Wind blade leading edge erosion protection specialist gelcoat and bio-based sustainable formulation

Wind turbine blade leading edge erosion protection specialist gelcoat represents the most commercially premium new product development category in the gelcoat market. Each wind farm operator whose turbine fleet requires leading edge restoration creates high-value repair gelcoat procurement whose per-blade commercial value substantially exceeds conventional marine and construction gelcoat economics. The growing sophistication of leading-edge protection system specification, from basic gelcoat application through multilayer tape and coating systems, creates premium product development opportunity for technically qualified gelcoat suppliers.

Bio-based and sustainable gelcoat formulation development using partially renewable resin content creates commercial differentiation for manufacturers targeting the growing segment of marine and construction customers whose sustainability procurement criteria create specification motivation beyond minimum performance requirements.

Recent Developments:

-

2026: Polynt-Reichhold Group enhanced its marine gelcoat range with improved UV-resistant and high-durability formulations for wind turbine blades and boat manufacturing.

-

2026: INEOS Composites developed low-VOC gelcoat solutions aligned with EU environmental regulations for reduced styrene emissions.

-

2026: Hexion Inc. advanced bio-based resin integration into gelcoat formulations to support sustainable composite material demand.

-

2025: Gurit Holding AG expanded its high-performance gelcoat systems for wind energy blade protection and structural composite applications.

Gelcoat Market Key Players are:

-

Ashland Inc.

-

Allnex GmbH

-

Scott Bader Company Ltd.

-

INEOS Composites

-

Polynt Reichhold Group

-

Bufa Composite Systems GmbH

-

AOC Resins (Advanced Composites Inc.)

-

HK Research Corporation

-

Interplastic Corporation

-

Reichhold LLC

-

BASF SE

-

Hexion Inc.

-

Momentive Performance Materials

-

Lonza Group AG

-

Gurit Holding AG

-

Olin Epoxy (Blue Cube)

-

Aditya Birla Chemicals

-

SIR Industrial (Sirtek)

-

Cray Valley (Total Energies)

-

Zhongshan Jinhao Plastics Co., Ltd

Gelcoat Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1,524.72 Million |

| Market Size by 2035 | USD 5,173.02 Million |

| CAGR | CAGR of 4.70% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Polyester Gelcoat, Epoxy Gelcoat, Vinyl Ester Gelcoat, Others) • By Application (Marine/Boat Building, Wind Energy/Turbine Blades, Transportation/Automotive, Construction/Building & Infrastructure, Sanitary Ware & Tubs, Others) • By End User (Construction, Marine, Wind Energy, Transportation & Automotive, Sanitary Ware, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Ashland Inc., Allnex GmbH, Scott Bader Company Ltd., INEOS Composites, Polynt Reichhold Group, Bufa Composite Systems GmbH, AOC Resins (Advanced Composites Inc.), HK Research Corporation, Interplastic Corporation, Reichhold LLC, BASF SE, Hexion Inc., Momentive Performance Materials, Lonza Group AG, Gurit Holding AG, Olin Epoxy (Blue Cube), Aditya Birla Chemicals, SIR Industrial (Sirtek), Cray Valley (Total Energies), Zhongshan Jinhao Plastics Co., Ltd. |

Frequently Asked Questions

The market is expected to grow at a CAGR of 4.70% from 2026 to 2035.

The market was valued at USD 1,524.72 Million in 2025.

Rising demand in marine vessel construction and maintenance, wind energy turbine blade manufacturing and leading edge erosion protection.

Polyester gelcoat dominated the market with 52.8% share in 2025 due to its cost-effectiveness and durability, while Epoxy Gelcoat is the fastest growing segment.

Asia Pacific is the fastest-growing region in the Gelcoat Market.

Get in Touch