Chlor-Alkali Market Report Scope & Overview:

The Chlor-Alkali Market size was valued at USD 62.33 Billion in 2023. It is estimated to reach USD 81.33 Billion by 2032, growing at a CAGR of 3.03% during 2024-2032.

The chlor-alkali market is a critical segment of the chemical industry, focusing primarily on the production of chlorine, sodium hydroxide (commonly known as caustic soda), and soda ash. The chlor-alkali process has extensive applications across multiple industries, underscoring its importance for economic growth and daily life. Chlorine is a highly versatile chemical widely used in the production of disinfectants, water treatment solutions, and a diverse range of organic and inorganic chemicals. Data extracted from 46 intervention groups revealed significant variability in the adoption of point-of-use (POU) chlorine products, a key application of chlor-alkali technology. The studies indicated a lack of consensus on how to define household water treatment adoption, though the most common indicator was the proportion of stored water samples with free chlorine residual levels exceeding 0.1 or 0.2 mg/L. Adoption rates for chlorine POU products varied widely, ranging from 1.5% to 100%. The sample size-weighted median adoption rate was 47%, while the unweighted median was slightly higher at 58%.

Chlor-Alkali Market Size and Forecast:

-

Market Size in 2023: USD 62.33 billion

-

Market Size by 2032: USD 81.33 billion

-

CAGR: 3.03% from 2024 to 2032

-

Base Year: 2023

-

Forecast Period: 2024–2032

-

Historical Data: 2020–2022

Get More Information on Chlor-Alkali Market - Request Sample Report

The growth of the chlor-alkali market is primarily driven by the rising demand for chlorine and caustic soda across various end-use industries. The water treatment sector is a major consumer of chlorine, essential for ensuring safe drinking water by eliminating harmful pathogens. The construction and building materials industry also heavily relies on chlor-alkali products, particularly in glass manufacturing, which is experiencing increased demand due to urbanization and infrastructure development. Moreover, the pulp and paper industry utilize chlorine and sodium hydroxide for bleaching processes, improving the quality of paper products. The ongoing expansion of the chemical industry, particularly in emerging economies, further boosts the demand for chlor-alkali products. As industries continue to grow, the need for effective chemical solutions intensifies, reinforcing the significance of the chlor-alkali market.

Chlor-Alkali Market Trends

-

Growing demand for chlorine, caustic soda, and soda ash across end-use industries such as chemicals, water treatment, pulp & paper, textiles, and aluminum production is driving steady market growth globally.

-

Rising investments in water and wastewater treatment infrastructure are significantly increasing consumption of chlor-alkali products, particularly chlorine and sodium hydroxide, for disinfection and purification applications.

-

Expansion of the chemical manufacturing sector, especially in emerging economies, is boosting demand for chlor-alkali derivatives used in plastics, solvents, detergents, and specialty chemicals.

-

Technological advancements and a gradual shift toward energy-efficient membrane cell technology are improving production efficiency while reducing energy consumption and environmental impact.

-

Stringent environmental regulations and sustainability initiatives are encouraging manufacturers to adopt cleaner production processes and reduce mercury and diaphragm cell usage.

-

Growth in the aluminum, automotive, and construction industries is supporting demand for caustic soda and chlorine-based compounds used in alumina refining and PVC production.

-

Strategic capacity expansions, mergers, and long-term supply agreements among key market players are strengthening global supply chains and enhancing market competitiveness.

Market Dynamics

Drivers

-

High demand from chemical manufacturing for chlorine and caustic soda fuels the market growth.

The chemical manufacturing sector has a high demand for chlorine and caustic soda, thereby driving growth in the chlor-alkali market. Chlorine is one of the primary raw materials required in manufacturing certain chemicals and products used in most of the applications across industries, particularly polyvinyl chloride (PVC). This is a common material used in construction industries for pipes, cables, and other equipment since it is durable and cost-effective. For instance, the growing global PVC market, influenced by increased urbanization and subsequent infrastructure development, goes in parallel with growing chlorine demand. Other chlorine applications include the preparation of end-use chemicals such as solvents, disinfectants, and a wide array of intermediates for the production of other chemicals like pharmaceuticals and agrochemicals—pointing out the huge significance of chlorine in the production of these chemicals. Apart from chlorine, caustic soda itself is rather essential in alumina extraction, paper and pulp manufacturing, and textile processing. With growing alumina demand due to increasing demand in the aluminum industry, wide increases in the consumption of caustic soda have been noted. Moreover, with the increasing demand for packaging materials, the advancement of the paper industry steadily raised the use of caustic soda due to its application in paper pulping and bleaching processes. The growth prospects of the chlor-alkali market are bright at the moment, with the chemical manufacturing sector constantly broadening its base and diversifying into newer areas of application, more so in emerging economies.

-

The chlor-alkali sector embraces sustainable innovations with membrane technology and renewable energy investment.

With a growing focus on sustainability, significant funds are being allocated to eco-friendly production methods in the Chlor-Alkali sector. As environmental laws become stricter globally, chlor-alkali companies are starting to implement sustainable measures to reduce their environmental impact and meet international standards. A significant advancement has been the substitution of mercury cell technology with membrane cell technology in chlorine production. These membrane cells provide an eco-friendlier and energy-saving option. It decreases mercury emissions by roughly 99% and energy consumption by 25-30%. This action is aligned with worldwide efforts to protect human health and the environment from mercury pollution as defined in the Minamata Convention. Moreover, companies are investing in renewable energy sources for their electrolysis operations, reducing both carbon footprints and operational expenses. For instance, European chlor-alkali producers are exploring the possibility of using sustainable electricity to reduce greenhouse gas emissions and comply with the environmental policy regulations of the European Union. The sector is working on green chemistry solutions to utilize saltwater instead of mined salt in producing chlor-alkali products, preserving resources and lessening environmental harm.

Restraints

-

Stringent environmental regulations, requiring costly technology upgrades.

One of the main limitations on the Chlor-Alkali Market is the strict environmental regulations, which require costly technology upgrades and adherence to rules. Efforts such as the Minamata Convention are pushing for a worldwide elimination of mercury cell technology, requiring expensive upgrades to more eco-friendly options like membrane cells. Legislation on water pollution and greenhouse gas emissions mandates manufacturers to adopt sophisticated emission control and wastewater treatment procedures. Although necessary for meeting regulations and environmental standards, enhancements in these specific areas can lead to higher operational expenses and create a financial burden, particularly for smaller businesses with restricted funding. As a result, this will affect the company's profits and present various obstacles for market competitors in maintaining competitive prices due to ongoing investments in compliance technologies.

Market Segmentation

By Product

Caustic Soda, also known as sodium hydroxide, held a major market share of over 48% in 2023. Its wide application in chemical manufacturing, pulp and paper processing, and water treatment makes it integral to various industries. Its important role in the production of detergents, soaps, and rayon is due to its high alkaline nature. Big corporations such as Olin Corporation and Occidental Chemical Corporation depend on caustic soda for their chemical processing requirements in large-scale operations. Caustic Soda continues to be dominant due to its strong demand in various industries such as textiles and aluminum, supported by widespread industrial dependence and diverse uses.

Chlorine segment is expected to the fastest-growing during 2024-2032 due to the increasing demand in pharmaceuticals, water disinfection, and PVC production. The disinfectant qualities are crucial in water treatment plants, and its application in PVC manufacturing aids in the expansion of the construction and automotive industries. Westlake Chemical Corporation and Formosa Plastics Corporation utilize chlorine to manufacture polyvinyl chloride (PVC) for long-lasting and eco-friendly construction materials. Chlorine's market is growing rapidly due to its expanding use in pharmaceuticals and public health, boosted by global advancements in health and infrastructure.

By Technology

Membrane cell dominated in 2023 with a 56% market share in the chlor-alkali market due to its energy efficiency and lower environmental impact. In contrast to the diaphragm and mercury techniques, membrane cells utilize ion-exchange membranes that only permit sodium ions to move across, successfully dividing chlorine and sodium hydroxide. This technology provides excellent purity in the final products and minimizes contamination, making it perfect for applications with strict quality requirements. Industries such as Dow Chemical and Olin Corporation utilize membrane cell technology for producing chlorine and caustic soda used in PVC manufacturing, water treatment, and chemical processing.

Diaphragm cell is anticipated to become the fastest-growing segment in the chlor-alkali market during 2024-2032. It utilizes a permeable membrane to divide the anode and cathode sections, allowing the creation of chlorine gas and caustic soda without requiring mercury. This technique requires less energy compared to methods using mercury, but usually results in less pure caustic soda because of the mixture of brine. Occidental Chemical Corporation and Tata Chemicals utilize diaphragm cell technology to fulfill needs in industries such as textiles, soap, and paper production, where caustic soda and chlorine are vital.

Regional Analysis

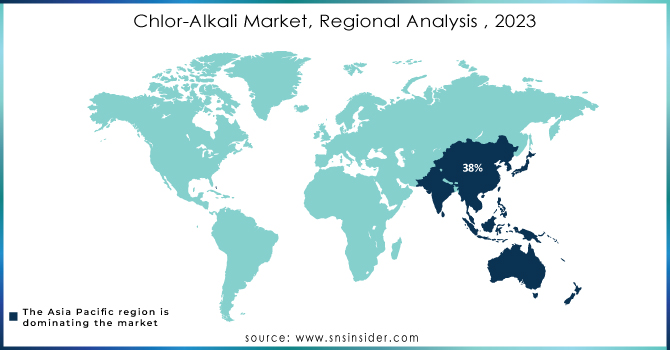

In 2023, the Asia-Pacific region dominated the market with a share of 55% in the, owing to the rapidly growing consumer base, the rising middle class, and high demand for new innovative flavors and fragrances. High population growth, coupled with economic development in this region, results in increased disposable income and thereby fuels higher consumption of processed foods and beverages, personal care, and other FMCG products. For instance, countries like China and India have consumed large volumes of flavored beverages and snacks, thus largely contributing to regional dominance. Growing demand for premium and customized fragrance products in emerging markets has also underpinned growth.

North America is anticipated to become the fastest-growing market during 2024-2032 because of its increasing use in water treatment, pulp and paper, and textiles industries. Heightened regulations for water quality and environmental control have increased the need for chlorine-based products. Occidental Petroleum Corporation and Olin Corporation have established a significant presence in this area, propelling growth through their emphasis on sustainable production methods. The increasing focus on environmentally friendly production technologies and advancements in chlor-alkali derivatives in North America is contributing to its role as a significant growth area, particularly due to the growing use of chlor-alkali products in energy storage applications.

Key Players

The key players in the Chlor-Alkali Market are:

-

Tata Chemicals Ltd (Sodium Carbonate, Caustic Soda)

-

Olin Corporation (Chlorine, Sodium Hydroxide)

-

Axiall Corporation (Chlorine, Caustic Soda)

-

Tronox Limited (Sodium Chloride, Sodium Hydroxide)

-

Solvay SA (Soda Ash, Caustic Soda)

-

Akzo Nobel NV (Chlorine, Sodium Bicarbonate)

-

Covestro AG (Chlorine, Polycarbonate)

-

Bayer AG (Chlorine, Sodium Hydroxide)

-

Xinjiang Zhongtai Chemical Co. Ltd (Caustic Soda, Chlorine)

-

Tosoh Corporation (Sodium Chloride, Caustic Soda)

-

Dow Chemical Company (Chlorine, Sodium Hydroxide)

-

Westlake Chemical Corporation (Caustic Soda, Chlorine)

-

Formosa Plastics Corporation (Chlorine, Sodium Hydroxide)

-

INOVYN (INEOS Group) (Chlorine, Sodium Hydroxide)

-

Chemical Company of Canada (Sodium Bicarbonate, Calcium Chloride)

-

KEM ONE (Chlorine, Caustic Soda)

-

SABIC (Chlorine, Sodium Hydroxide)

-

Shandong Jinling Chemical (Chlorine, Sodium Bicarbonate)

-

Koch Industries (Caustic Soda, Chlorine)

-

Nippon Soda Co., Ltd. (Sodium Hydroxide, Chlorine)

Recent Development

-

February 2024: INEOS Inovyn has developed a set of Ultra Low Carbon products, ULC Chlor-Alkali with emissions reductions up to 70%, setting new standards in sustainability powered by renewable energy.

-

April 2024: Nuberg EPC has commissioned largest Chlor-Alkali project of India for Mundra Petrochemical Ltd.(Adani Enterprises), fully NaOH based having149017230 TPD capacity.

-

Feb 2024: Launch of Ultra Low Carbon Chlor-Alkali range by INEOS Inovyn – 70% lower CO2 footprint.

-

November 2023: Brenntag has purchased Old World Specialty Chemicals and Old-World Logistics, adding distribution network access in North America along with additional terminal capabilities.

-

December 2023: Asahi Kasei announced that it will launch a demonstration trial in Europe for a rental service of chloralkali electrolysis cells with Nobian GmbH and LOGISTEED Europe B.V. With its headquarters located in the State of North Rhine-Westphalia, Germany, Nobian is one of the top chloralkali companies in Europe.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 62.33 Billion |

| Market Size by 2032 | US$ 81.33 Billion |

| CAGR | CAGR of 3.03% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Caustic soda, Soda ash, Chlorine) •By Production Process (Membrane cell process, Diaphragm cell process, Mercury cell process) •By Application (Organic chemicals, Food processing, Paper & pulp, Water treatment, Textiles, Soaps & detergents, Alumina, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Tata Chemicals Ltd, Olin Corporation, Axiall Corporation, Tronox Limited, Solvay SA, Akzo Nobel NV, Covestro AG, Bayer AG, Xinjiang Zhongtai Chemical Co. Ltd, Tosoh Corporation, and other players. |

| Key Drivers | •High demand from chemical manufacturing for chlorine and caustic soda •Focus on sustainability, driving investments in eco-friendly production processes. |

| RESTRAINTS | •Stringent environmental regulations, requiring costly technology upgrades. |

Frequently Asked Questions

Ans. The Compound Annual Growth rate for the Chlor-Alkali Marketover the forecast period is 6.5%

Ans: Chlor-Alkali Market size was USD 54.9 billion in 2023 and is expected to reach USD 96.8 billion by 2032.

Ans: Expansion projects like India's largest chlor-alkali facility by Nuberg EPC and increased focus on sustainable practices, creating demand for greener technologies are the driving factors that fuel the demand for the Chlor-Alkali market

Ans: Stringent environmental regulations, requiring costly technology upgrades hamper the demand for the Chlor-Alkali market

Ans: The Asia Pacific region dominated the Chlor-Alkali Market holding the largest market share of about 38% during the forecast period.

Get in Touch