Generative AI in Financial Services Market Report Scope & Overview:

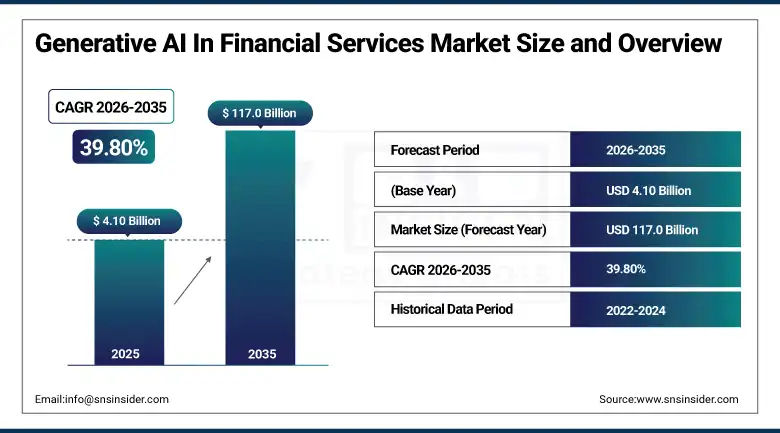

The Generative AI in Financial Services Market was valued at USD 4.10 Billion in 2025 and is expected to reach USD 117.0 Billion by 2035, growing at a CAGR of 39.80% from 2026–2035.

The global generative AI in financial services market is advancing at an extraordinary pace, reshaping financial operations as banks, insurers, asset managers, and fintech companies deploy large language models, synthetic data generators, and generative adversarial networks to automate document intelligence, personalize customer engagement, and accelerate risk assessment at scale. Generative AI’s ability to produce contextually coherent, domain-accurate content from financial data transforms the high-volume text-intensive workflows constituting the majority of financial services operational cost. AI-powered chatbots providing personalized financial advice, synthetic transaction data generation for fraud model training, automated credit decision explanation, and LLM-accelerated regulatory report drafting define the commercial applications whose rapid enterprise adoption sustains exceptional market growth.

In 2024, JPMorgan Chase deployed its LLM-powered contract intelligence tool across 3.5 million hours of annual legal document review, reducing contract analysis time from months to hours and generating USD 150 million in annual operational cost savings. The deployment demonstrated the extraordinary productivity multiplier that generative AI delivers in the document-intensive legal and compliance workflows that consume substantial human capital in global financial institutions, creating a commercially compelling reference case that accelerated peer institution investment in LLM-based automation programmes.

Market Size and Forecast

- Market Size in 2026E: USD 5.73 Billion

- Market Size by 2035: USD 117.0 Billion

- CAGR: 39.80% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information On Generative AI In Financial Services Market - Request Free Sample Report

Generative AI in Financial Services Market Trends

-

Large language model deployment for regulatory compliance document drafting is reducing compliance team workload and accelerating regulatory filing timelines.

-

Synthetic financial data generation is enabling fraud model training on balanced datasets without exposing sensitive customer transaction records.

-

AI-powered personalized financial management through conversational interfaces is enabling hyper-personalized product recommendation at mass-market scale.

-

Generative AI code generation is accelerating core banking modernization by automating COBOL-to-modern-language code translation workflows.

-

Multi-modal financial AI integrating text, tabular, and time-series data is enhancing investment research synthesis and earnings analysis automation.

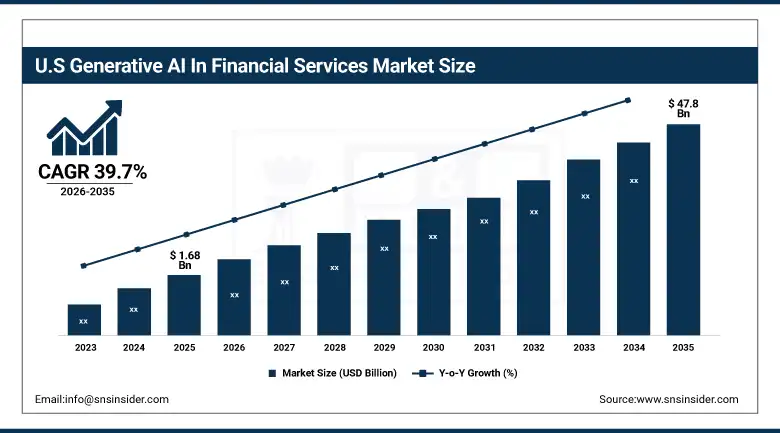

The U.S. Generative AI in Financial Services Market Outlook

The U.S. Generative AI in Financial Services Market was valued at approximately USD 1.68 Billion in 2025 and is expected to reach approximately USD 47.8 Billion by 2035, growing at a CAGR of approximately 39.7%.

The United States leads North American revenues through the world’s most commercially mature financial services AI investment culture, the largest concentration of global banking institutions deploying generative AI at enterprise scale, and the domestic fintech ecosystem’s rapid AI integration across lending, payments, and wealth management. JPMorgan Chase, Goldman Sachs, and Visa’s substantial generative AI programmes combined with SEC AI governance guidance are creating structured institutional procurement that defines the commercial direction of enterprise generative AI adoption globally.

In 2023, Mastercard launched its AI-powered Decision Intelligence Pro system using generative AI to analyse transaction patterns across one trillion data points in real time, improving fraud detection accuracy by 20% globally while simultaneously reducing false positive rates that create cardholder friction. The deployment demonstrated generative AI’s ability to improve both fraud prevention effectiveness and customer experience simultaneously by detecting complex patterns that rule-based systems cannot identify without triggering the false alerts that undermine customer trust in fraud prevention programmes.

Generative AI in Financial Services Market Segment Analysis

-

By Component, solutions segment dominated the generative AI in financial services market with the largest share in 2025, while services is the fastest growing driven by implementation complexity and ongoing model governance management demand.

-

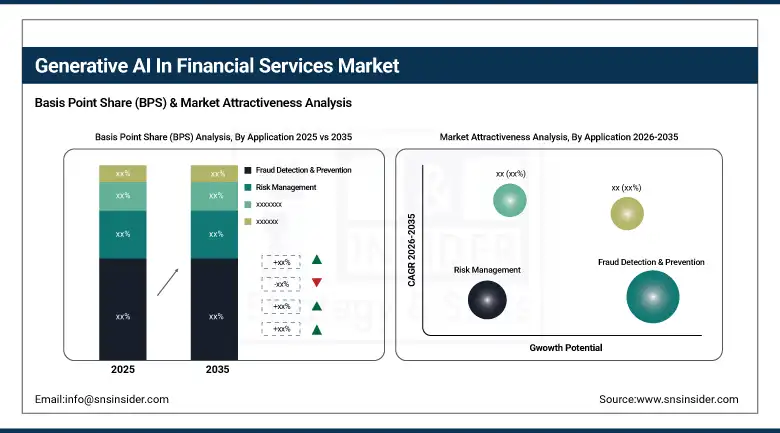

By Application, fraud detection & prevention segment dominated the generative AI in financial services market with approximately 31% market share in 2025, while risk management is expected to register the fastest CAGR of around 33.2% during 2026–2035 driven by regulatory complexity expansion.

-

By End User, retail banking segment dominated the generative AI in financial services market with the largest share in 2025 through high-volume transaction and customer service workflows, while Fintech is the fastest growing end user.

-

By Technology, large language models segment dominated the generative AI in financial services market with the largest share in 2025, while Generative Adversarial Networks are growing rapidly for synthetic financial data generation.

By Application, fraud detection dominates, risk management grows fastest

Fraud detection and prevention retained the dominant application position with the largest share of the generative AI in financial services market in 2025. The quantifiable and immediate financial return that AI-powered fraud prevention delivers, where each percentage point improvement in detection rate directly reduces chargebacks, insurance claims, and loan defaults whose aggregate impact creates measurable programme ROI, creates compelling investment motivation sustaining fraud AI as the highest-priority generative AI application. Generative AI’s ability to produce novel fraudulent transaction patterns for adversarial training, to synthesize balanced fraud datasets from imbalanced historical records, and to generate contextual fraud narrative explanations for analyst investigation creates applications that extend conventional ML fraud detection into AI-augmented fraud intelligence progressively becoming standard practice across card networks, banks, and insurers.

Risk management is growing fastest because expanding regulation across Basel IV capital requirements, DORA operational resilience obligations, and ESG disclosure mandates creates growing demand for generative AI’s ability to automate regulatory document analysis, synthesize risk scenario narratives, and generate stress test documentation. Each new regulatory framework requiring extensive scenario analysis, documentation drafting, and multi-jurisdiction reporting creates structured generative AI procurement whose per-institution value scales with regulatory complexity.

By End User, retail banking dominates, fintech grows fastest

Retail banking retained the dominant end-user position with the largest share of the generative AI in financial services market in 2025. Retail banks’ extraordinary data richness from billions of daily customer transactions, the high-volume nature of customer service and compliance workflows whose automation creates measurable cost reduction, and competitive pressure from digital-native challengers create the most commercially significant generative AI deployment context. Each major retail bank deploying generative AI for customer inquiry response, mortgage document processing, and credit decision explanation creates multi-million-dollar platform investment whose ROI documentation sustains expansion commitment.

Fintech is growing fastest because AI-native architecture, built for data-driven automation from inception rather than requiring legacy integration, creates dramatically lower implementation friction for generative AI adoption than incumbent bank deployment contexts. Each new fintech product incorporating generative AI for personalized financial coaching, automated portfolio rebalancing explanation, and real-time lending decision rationale creates commercial deployment at lower cost and faster timeline than equivalent bank transformation programmes.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

United Kingdom |

28.4% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

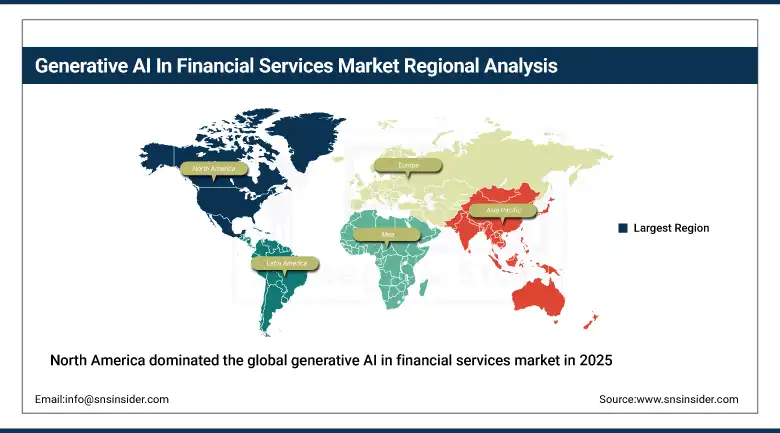

North America Generative AI in Financial Services Market Insights

North America dominated the global generative AI in financial services market in 2025 with the largest revenue share through its concentration of global banking and asset management institutions, the most extensive fintech ecosystem, and highest enterprise generative AI investment budgets. The United States accounts for approximately 82.5% of North American revenues through JPMorgan Chase’s, Goldman Sachs’, and Visa’s large-scale programmes whose outcomes create industry reference deployments.

Canada contributes supplementary revenues through its large financial services sector’s progressive generative AI adoption in customer service, risk management, and regulatory compliance. The Canadian banking sector’s technology investment culture and the growing AI research sector’s commercial activity sustain domestic generative AI financial services development above purely commercial market demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Generative AI in Financial Services Market Insights

Europe is a significant generative AI in financial services market where GDPR, the EU AI Act’s high-risk AI classification for credit decisioning, and DORA’s operational resilience regulation create compliance-driven investment. The United Kingdom accounts for approximately 28.4% of European revenues through its world-leading financial services cluster’s early adoption and the FCA’s progressive AI governance framework creating structured procurement.

Germany’s banking and insurance sector, France’s BNP Paribas and Société Générale’s AI investment programmes, and the Netherlands’ ING Bank’s AI deployment sustain European market development. European institutions’ DORA compliance investment is creating structured generative AI procurement for operational resilience testing and incident response automation above voluntary digital transformation investment.

Asia Pacific Generative AI in Financial Services Market Insights

Asia Pacific is the fastest-growing regional generative AI in financial services market, driven by China’s world-leading mobile payment infrastructure creating vast transaction data, India’s expanding digital banking ecosystem, and the progressive AI adoption across Japan, South Korea, and Singapore’s mature financial centres. China accounts for approximately 44.8% of Asia Pacific revenues through Ant Group and WeBank’s AI deployment leadership.

India represents the most commercially dynamic emerging market, where the UPI platform’s transaction data, rapidly growing digital lending sector’s credit scoring investment, and the fintech start-up ecosystem create above-regional-average growth momentum. Singapore’s MAS Project Guardian and South Korea’s financial AI investment create premium secondary regional demand above commercial enterprise adoption.

MEA & Latin America Generative AI in Financial Services Market Insights

The UAE leads MEA revenues through its advanced digital banking infrastructure, DIFC’s progressive AI financial regulation framework, and Emirates NBD and First Abu Dhabi Bank’s substantial generative AI investment. Saudi Arabia’s Vision 2030 financial sector digital transformation creates growing institutional generative AI procurement across banking and insurance sectors.

Brazil leads Latin American revenues through its Pix instant payment infrastructure’s AI fraud monitoring, the large fintech sector’s generative AI credit scoring adoption, and Banco Central do Brasil’s open banking regulation creating data-rich AI training environments. Mexico and Colombia contribute growing secondary demand through financial sector digitalization and fintech regulatory development.

Market Dynamics

Growth Drivers: Document-intensive workflow automation delivering measurable cost reduction and fraud prevention ROI compelling above-average enterprise AI investment

Generative AI in financial services is uniquely positioned because the industry’s foundational operating model is document-intensive, data-rich, and operationally costly in ways that align precisely with generative AI’s core capabilities. Each global bank whose compliance team processes thousands of annual regulatory updates and each insurer whose claims review processes millions of documents creates workflow automation opportunity whose LLM productivity multiplier generates quantifiable savings. JPMorgan’s documented USD 150 million annual savings from contract intelligence AI validates board-level financial services generative AI investment commitment that sustains accelerating procurement.

Fraud prevention’s quantifiable ROI creates the most commercially certain generative AI investment justification, where each basis point improvement in detection rate directly reduces charge-off losses whose annual scale at major banks measures in hundreds of millions. Generative AI’s ability to create synthetic fraud scenarios for adversarial model training, identify novel patterns in real-time transaction streams, and generate investigator-readable fraud narratives collectively creates applications whose financial return documentation is straightforward and whose AML compliance value creates regulatory motivation above pure loss reduction economics.

Restraints: Model hallucination risk in high-stakes decisions and regulatory uncertainty about AI liability creating caution in credit and advisory applications

Generative AI’s propensity for hallucination, producing confident but factually incorrect outputs documented across all current LLM architectures, creates a fundamental adoption barrier in high-stakes financial decisions where liability for erroneous credit refusals, incorrect investment advice, or fraudulent transaction false positives creates institutional risk constraining deployment without robust human review. Each documented AI hallucination in financial context creates institutional caution that slows deployment timelines and increases oversight infrastructure investment above what the AI platform cost alone requires.

Regulatory uncertainty about liability assignment for AI-generated financial advice, the permissibility of AI credit decision explanations under fair lending law, and accountability for AI-driven trading decisions creates legal risk requiring compliance and legal team assessment before approving deployment in regulated categories. The SEC’s AI governance guidance, UK FCA’s regulation consultation, and EU AI Act’s high-risk classification create complex multi-jurisdictional compliance whose navigation adds cost and timeline to enterprise generative AI financial services programmes.

Opportunities: Real-time personalized financial advisory and legacy core banking modernization representing transformative commercial frontiers

Real-time personalized financial advisory through conversational AI, whose LLM-generated planning recommendations and market commentary calibrate to individual risk profiles, goals, and life stage, represents the most commercially valuable near-term opportunity whose addressable market spans every retail banking customer globally. Each bank deploying a generative AI financial advisor providing wealth management quality guidance to mass-market retail customers creates a service whose improved product penetration and retention substantially exceed the platform investment.

Legacy core banking modernization represents a structurally large opportunity for generative AI code translation, where the global installed base of COBOL mainframe banking systems whose estimated 800 billion lines of legacy code require modernization creates decades of translation automation work. Each bank deploying generative AI for automated COBOL-to-modern-language translation reduces modernization cost and timeline that previously made comprehensive replacement economically infeasible for mid-size institutions whose transformation budgets cannot support multi-decade manual migration programmes.

Recent Developments:

-

2024: JPMorgan Chase deployed its LLM-powered contract intelligence tool replacing 3.5 million annual legal document review hours, generating USD 150 million in documented annual operational cost savings from automated contract analysis and due diligence workflow acceleration.

-

2023: Mastercard launched AI-powered Decision Intelligence Pro using generative AI to analyse one trillion transaction data points in real time, improving fraud detection accuracy by 20% globally while reducing false positive rates that create friction for legitimate cardholders.

-

2023: Goldman Sachs deployed a generative AI developer productivity platform across its 10,000-engineer software team, using LLM code generation and review assistance to accelerate financial software development and reduce code review cycle times for trading and risk systems.

Generative AI in Financial Services Market Key Players are:

-

IBM Corporation (Watson Financial Services)

-

Microsoft Corporation (Azure OpenAI for Financial Services)

-

Google LLC (Vertex AI for Financial Services)

-

Amazon Web Services Inc. (SageMaker, Bedrock)

-

Salesforce Inc. (Einstein for Financial Services)

-

Palantir Technologies Inc.

-

Bloomberg LP (BloombergGPT)

-

Temenos AG

-

Finastra Holdings Ltd.

-

Provenir Inc.

-

Kasisto Inc.

-

Socure Inc.

-

Kensho Technologies (S&P Global)

-

Zest AI Inc.

-

Wolters Kluwer NV

-

Experian PLC

-

Moody’s Analytics Inc.

-

SAS Institute Inc.

-

Symphony AyasdiAI

-

Quantexa Ltd.

Generative AI in Financial Services Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.10 Billion |

| Market Size by 2035 | USD 117.0 Billion |

| CAGR | CAGR of 39.80% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Technology (Large Language Models, Generative Adversarial Networks, Variational Autoencoders, Others) • By Application (Fraud Detection & Prevention, Risk Management, Customer Service & Personalization, Regulatory Compliance, Investment & Portfolio Management, Others) • By End User (Retail Banking, Investment Banking, Insurance, Wealth Management, Fintech, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | IBM Corporation (Watson Financial Services), Microsoft Corporation (Azure OpenAI for Financial Services), Google LLC (Vertex AI for Financial Services), Amazon Web Services Inc. (SageMaker, Bedrock), Salesforce Inc. (Einstein for Financial Services), Palantir Technologies Inc., Bloomberg LP (BloombergGPT), Temenos AG, Finastra Holdings Ltd., Provenir Inc., Kasisto Inc., Socure Inc., Kensho Technologies (S&P Global), Zest AI Inc., Wolters Kluwer NV, Experian PLC, Moody’s Analytics Inc., SAS Institute Inc., Symphony AyasdiAI, and Quantexa Ltd. |

Frequently Asked Questions

The Generative AI in Financial Services Market is expected to grow at a CAGR of 39.80% from 2026 to 2035.

The Generative AI in Financial Services Market was valued at USD 4.10 Billion in 2025.

Document-intensive workflow automation delivering measurable cost savings, fraud prevention ROI compelling enterprise investment, regulatory compliance automation demand, and personalized customer engagement through conversational AI are the primary growth factors.

The Fraud Detection & Prevention segment dominated with the largest share in 2025, while Risk Management is the fastest growing application driven by expanding regulatory complexity.

North America dominated in 2025 with the largest revenue share through its world-leading concentration of global banking institutions, fintech ecosystem, and highest enterprise generative AI investment budgets.

Get in Touch