Genome Editing Market Report Scope & Overview:

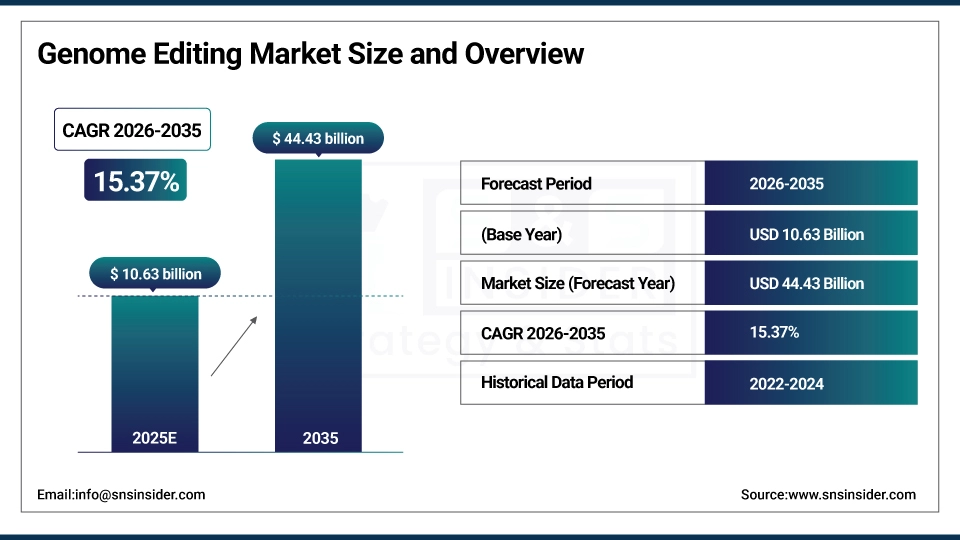

The Genome Editing Market size is estimated at USD 10.63 billion in 2025 and is expected to reach USD 44.43 billion by 2035, growing at a CAGR of 15.37% over the forecast period of 2026-2035.

The global genome editing market trend is a growing demand for precision medicine solutions such as CRISPR-based therapeutics, gene therapy development platforms, and agricultural biotechnology applications. Also driven by a growing adoption of personalized treatment approaches and the growing focus on rare disease therapy development as pharmaceutical companies become more focused on developing targeted genetic interventions and are more willing to invest in next-generation genome editing tools, resulting in growth in the domestic and international market for clinical and non-clinical genome editing applications.

Genome Editing Market Size and Forecast:

-

Market Size in 2025: USD 10.63 billion

-

Market Size by 2035: USD 44.43 billion

-

CAGR: 15.37% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Genome Editing Market - Request Free Sample Report

Genome Editing Market Trends

-

Genome editing solutions are being adopted because researchers demand precise gene modification tools, therapeutic target identification capabilities, and scalable manufacturing platforms for gene-edited products.

-

Customized gene therapy approaches based on patient genetic profiles, disease mechanisms, and target tissue specificity to improve clinical outcomes of genetic disorders.

-

The development of base editing technologies, prime editing systems, and epigenome editing tools to improve the precision of genetic modifications and expand therapeutic applications beyond DNA cutting.

-

Lipid nanoparticle delivery systems, viral vector optimization, and in vivo editing approaches are all available to ensure efficient gene delivery and sustained therapeutic effects.

-

Increased demand for automated genome editing platforms, high-throughput screening systems and artificial intelligence-guided design tools to help research efficiency and therapeutic discovery.

-

Collaboration between pharmaceutical companies, academic institutions and biotech startups to develop innovative gene editing therapeutics and improve regulatory approval pathways.

-

FDA, EMA and global regulatory bodies promoting standards for gene therapy safety, clinical trial design requirements, ethical guidelines for germline editing, and intellectual property frameworks.

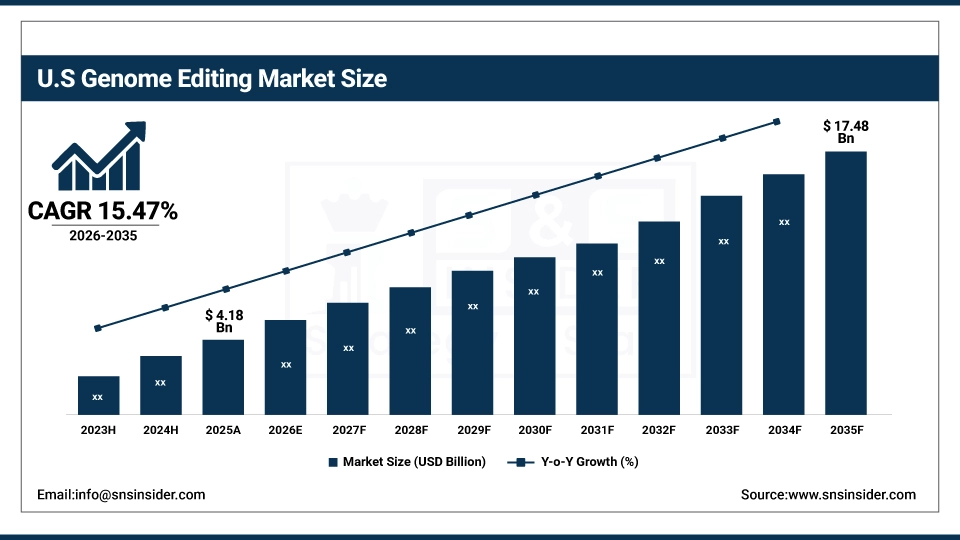

The U.S. Genome Editing Market is estimated at USD 4.18 billion in 2025 and is expected to reach USD 17.48 billion by 2035, growing at a CAGR of 15.47% from 2026-2035. The United States represents the largest market for genome editing, primarily driven by the extensive biotechnology research infrastructure, significant venture capital investment in gene therapy companies, and well-developed regulatory frameworks for advanced genetic therapies. Government funding through NIH and DARPA initiatives, high levels of academic-industry collaboration, and increased pharmaceutical company investment in precision medicine help to drive growth in the market.

Genome Editing Market Growth Drivers:

-

Rising Prevalence of Genetic Disorders and Chronic Diseases is Driving the Genome Editing Market Growth

Rising prevalence of genetic disorders and chronic diseases take the center stage as a growth driver for the genome editing market share, and are driven by the increasing incidence of inherited conditions, cancer burden, and rare disease diagnosis requiring innovative therapeutic interventions. These solutions for curative gene therapy development and disease mechanism understanding are driving the base of the market, the penetration of clinical application & genetic engineering markets, and adding to the overall market share globally.

For instance, in June 2024, gene editing-based therapies and research applications accounted for ~58% of the total global biotechnology research and development investments, reflecting growing institutional preference and expanding market share.

Genome Editing Market Restraints:

-

Ethical Concerns and Regulatory Uncertainties are Hampering the Genome Editing Market Growth

Ethical concerns & regulatory uncertainties of genome editing technologies also restrict the genome editing market growth, as a large number of stakeholders express concerns about germline editing implications, off-target effects, and long-term safety considerations in human applications. This might lead to delayed regulatory approvals, limited clinical trial advancement, and reduced public acceptance for gene therapy interventions. As a result, therapeutic development timelines are extended, and market growth is stunted in regions where ethical debates remain unresolved and regulatory frameworks for genome editing remain incomplete.

Genome Editing Market Opportunities:

-

Agricultural Biotechnology Applications Drive Future Growth Opportunities for the Genome Editing Market

The opportunity in the agricultural biotechnology applications in genome editing market is in the form of crop yield enhancement, disease resistance development, and climate-adapted plant varieties. These solutions provide for sustainable food production, reduced pesticide dependence, and improved nutritional content in agricultural products. Through enhanced global food security, environmental sustainability, and economic benefits for farming communities, particularly in areas with challenging agricultural conditions, these technologies may improve crop performance, decrease agricultural losses, and expand the market.

For instance, in April 2024, regulatory agencies in multiple countries approved 12 gene-edited crop varieties for commercial cultivation, highlighting rising acceptance of agricultural genome editing and increasing demand for sustainable biotechnology solutions.

Genome Editing Market Segment Analysis

-

By application, genetic engineering held the largest share of around 56.72% in 2025E, and the clinical applications segment is expected to register the highest growth with a CAGR of 16.24%.

-

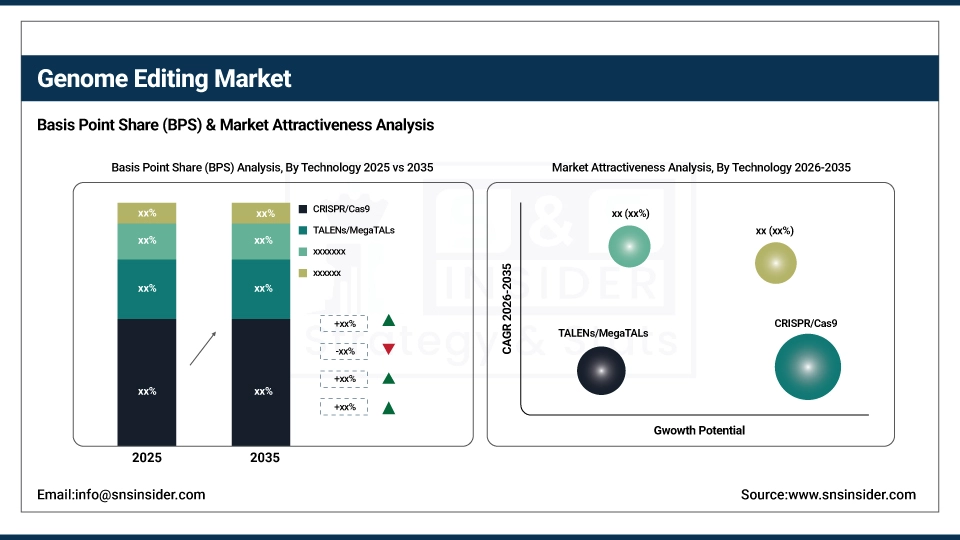

By technology, CRISPR/Cas9 segment dominated the market with approximately 64.38% share in 2025E, while the TALENs/MegaTALs is expected to register the highest growth with a CAGR of 16.12%.

-

By end-use, biotechnology and pharmaceutical companies accounted for the leading share of nearly 48.56% in 2025E, and is expected to register the highest growth with a CAGR of 15.68%.

By Technology, the CRISPR/Cas9 Segment dominates, while the TALENs/MegaTALs Segment Shows Rapid Growth

By 2025, the CRISPR/Cas9 segment contributed the largest revenue share of 64.38% due to its superior editing efficiency, ease of design and implementation, and cost-effectiveness compared to other genome editing technologies. Growing adoption of CRISPR-based research tools coupled with extensive patent licensing frameworks, researchers are increasingly utilizing CRISPR systems for diverse applications.

The TALENs/MegaTALs segment is projected to grow at the highest CAGR of about 16.12% between 2026 and 2035 due to the growing need for applications requiring higher specificity and reduced off-target effects. Some of the reasons include better performance in challenging genomic contexts, enhanced safety profiles for therapeutic applications, and biotechnology companies' preference for complementary genome editing platforms.

By Application, Genetic Engineering Leads the Market, While Clinical Applications Registers Fastest Growth

The genetic engineering segment accounted for the highest revenue share of approximately 56.72% in 2025, owing to extensive research applications in cell line development, established use in agricultural biotechnology, and widespread adoption for fundamental biological research. Emerging trends, including increasing requirements for genetically modified organisms in biopharmaceutical production and continued investment in crop improvement programs.

The clinical applications segment is anticipated to achieve the highest CAGR of nearly 16.24% during the 2026–2035 period, driven by the accelerating gene therapy clinical trials, regulatory approvals for CRISPR therapeutics, and growing investment in rare disease treatment development. Drivers include rising patient demand for curative therapies, the preference for personalized medicine approaches in oncology and inherited disorders.

By End-Use, Biotechnology and Pharmaceutical Companies Lead, and Registers Fastest Growth

The biotechnology and pharmaceutical companies segment accounted for the largest share of the genome editing market with about 48.56%, owing to their extensive therapeutic development pipelines, significant research and development budgets, and direct commercial interest in gene editing applications. Reasons driving this segment include increasing drug discovery programs utilizing genome editing and therapeutic product development requirements. Also grow at the fastest rate with a CAGR of around 15.68% throughout the forecast period of 2026–2035, as companies seek curative gene therapy platforms, cell therapy manufacturing capabilities, and target validation tools for drug development. Increased focus on precision medicine commercialization and strategic partnerships with academic institutions contribute to their adoption, while improved clinical trial success rates and expanding indication approvals drive continued investment.

Genome Editing Market Regional Highlights:

North America Genome Editing Market Insights:

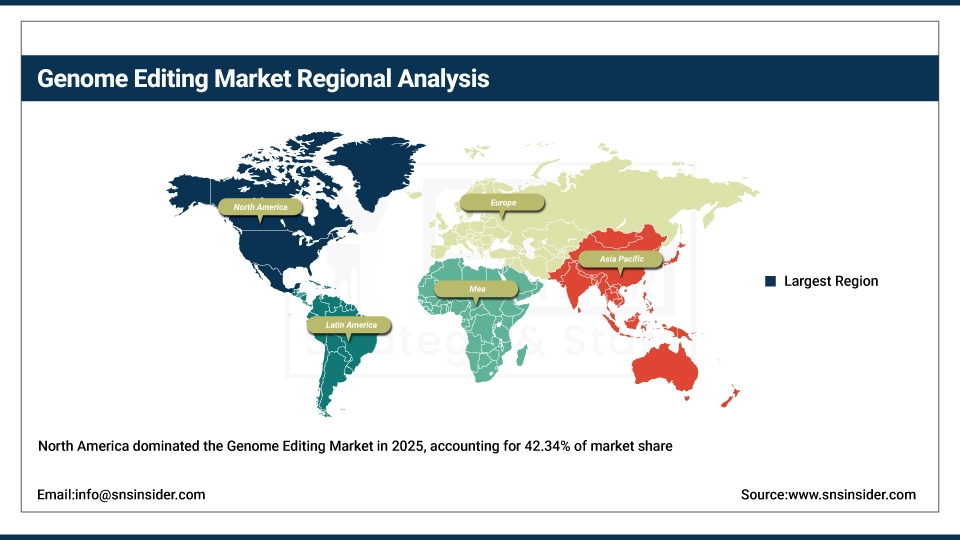

North America held the largest revenue share of over 42.34% in 2025 of the genome editing market due to an established biotechnology industry infrastructure, leading academic research institutions, and increased venture capital funding for gene therapy companies. Drivers include ubiquitous use of CRISPR technologies in research settings, an advanced clinical trial network, growing pharmaceutical company investment in genetic medicine and greater acceptance of innovative therapeutic modalities stemming from regulatory clarity. At the same time, various government funding programs, NIH genomic research initiatives and enormous investments in precision medicine from healthcare systems are anchoring genome editing technologies and services in the market, and ensuring multibillion dollar revenues around the world.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Genome Editing Market Insights:

Asia Pacific is the fastest-growing segment in the genome editing market with a CAGR of 17.26%, as the awareness about genetic disease treatment options, government biotechnology development programs, and research infrastructure investment in developing nations is growing. Factors including rapid pharmaceutical industry expansion, rising clinical trial activity with cost advantages, and growing adoption of agricultural genome editing for food security are stimulating the market growth. Academic research institution establishment and biotech startup ecosystem development have been instrumental in improving genome editing research capabilities, especially in countries with emerging biotechnology sectors. Public health initiatives and regulatory framework modernization also help in advancing gene therapy research and therapeutic development activities. Increase in demand in Asia Pacific region owing to rising healthcare expenditure against historical spending levels and growing accessibility of genome editing technologies and contract research services.

Europe Genome Editing Market Insights:

The genome editing market in Europe is the second-dominating region after North America on account of an increase in the adoption of gene therapy research programs, robust intellectual property protection frameworks including patent systems, and increasing collaborative research initiatives across healthcare institutions. Rising implementation of European biotechnology funding programs, advanced genomic medicine centers, favorable government support for translational research, and cross-border scientific collaboration networks are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Genome Editing Market Insights:

In Latin America, and Middle East & Africa, the growing biotechnology sector development and increase in research infrastructure investment with international collaboration expansion support the genome editing market growth. The rising popularity of agricultural genome editing applications and clinical research participation, along with technology transfer from developed markets, will aid genetic research accessibility and therapeutic development. The increasing medical tourism for advanced therapies and improving regulatory frameworks in these regions are continuing to encourage market growth.

Genome Editing Market Competitive Landscape:

Thermo Fisher Scientific Inc. (est. 1956) is a leading life sciences and laboratory equipment provider that focuses on integrated research solutions for scientific discovery and therapeutic development. It uses its comprehensive product portfolio and global distribution network to produce cutting-edge genome editing tools with seamless research workflow integration.

-

In February 2025, it expanded its genome editing portfolio with next-generation CRISPR delivery systems and automated gene editing platforms, aiming to improve research efficiency and therapeutic development capabilities across its global customer base.

CRISPR Therapeutics AG (est. 2013) is a well-known gene editing company focused on developing transformative gene-based medicines for serious diseases. It invests in innovative CRISPR/Cas9 therapeutic platforms and ex vivo cell therapy approaches with the hopes of revolutionizing genetic disease treatment with safe, effective, and durable curative therapies.

-

In May 2024, received FDA approval for its first CRISPR-based therapy for sickle cell disease and beta-thalassemia, marking a historic milestone in gene editing therapeutics and expanding commercial market opportunities for genetic medicine.

Editas Medicine, Inc. (est. 2013) is a leading clinical-stage genome editing company in the fields of CRISPR-based therapeutics, ocular disease treatment, and immuno-oncology applications. The company's therapeutic development portfolio focuses on in vivo editing approaches and tissue-specific delivery systems, and features a strong commitment to scientific innovation and continuous clinical advancement to complement the strong market presence in both rare disease and cancer treatment settings.

-

In September 2024, advanced its lead ocular gene editing program into Phase II clinical trials with positive safety and efficacy data, strengthening its therapeutic pipeline and expanding clinical development in inherited retinal diseases.

Genome Editing Market Key Players:

-

Thermo Fisher Scientific Inc.

-

CRISPR Therapeutics AG

-

Editas Medicine, Inc.

-

Intellia Therapeutics, Inc.

-

Beam Therapeutics Inc.

-

Sangamo Therapeutics, Inc.

-

Horizon Discovery Group (Revvity)

-

GenScript Biotech Corporation

-

Merck KGaA

-

Lonza Group AG

-

Precision BioSciences, Inc.

-

Bluebird Bio, Inc.

-

Caribou Biosciences, Inc.

-

Cellectis S.A.

-

Integrated DNA Technologies (IDT)

-

New England Biolabs, Inc.

-

OriGene Technologies, Inc.

-

Synthego Corporation

-

Regeneron Pharmaceuticals, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | US$ 10.63 Billion |

| Market Size by 2035 | US$ 44.43 Billion |

| CAGR | CAGR of 15.37% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application [Genetic Engineering (Cell Line Engineering, Animal Genetic Engineering, Plant Genetic Engineering, Others), Clinical Applications (Diagnostics, Therapy Development)] • By Technology ((CRISPR)/Cas9, TALENs/MegaTALs, ZFN, Meganuclease, Others) • By Delivery Method (Ex-vivo, In-vivo) • By End-use (Biotechnology and Pharmaceutical Companies, Academic and Government Research Institutes, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles |

Thermo Fisher Scientific Inc., CRISPR Therapeutics AG, Editas Medicine, Inc., Intellia Therapeutics, Inc., Beam Therapeutics Inc., Sangamo Therapeutics, Inc., Horizon Discovery Group (Revvity), GenScript Biotech Corporation, Merck KGaA, Lonza Group AG, Precision BioSciences, Inc., Bluebird Bio, Inc., Caribou Biosciences, Inc., Cellectis S.A., Integrated DNA Technologies (IDT), New England Biolabs, Inc., OriGene Technologies, Inc., Synthego Corporation, Regeneron Pharmaceuticals, Inc. |

Frequently Asked Questions

North America dominated the Genome Editing Market in 2025.

By application, the Genetic Engineering segment dominated the Genome Editing Market in 2025.

Rising Prevalence of Genetic Disorders and Chronic Diseases is Driving the Genome Editing Market Growth.

The Genome Editing Market size was USD 10.63 billion in 2025 and is expected to reach USD 44.43 billion by 2035.

The Genome Editing Market is expected to grow at a CAGR of 15.37% over the forecast period.

Get in Touch