Geotextile Market Report Scope & Overview:

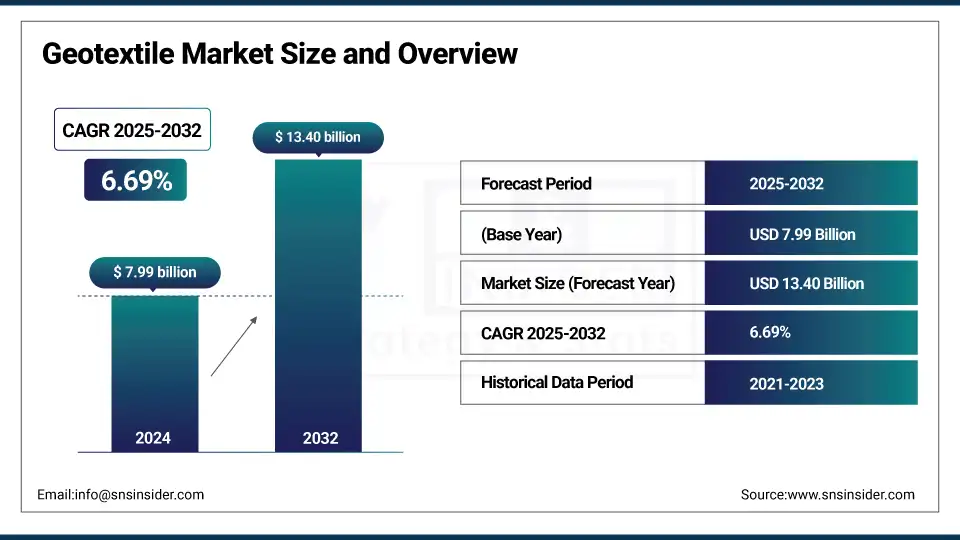

The Geotextile Market size was valued at USD 7.99 billion in 2024 and is expected to reach USD 13.40 billion by 2032, growing at a CAGR of 6.69% over the forecast period of 2025-2032.

Increasing environmental legislation and infrastructure development are influencing the growth of the geotextile market. Over time, the utilization of non-woven geotextiles has been seen in road construction and erosion control. The geotextile market is witnessing a surge in geotextile fabric applications for eco-friendly projects such as green pavements and smart geotextiles incorporated with sensors. Portfolio consolidation within the geotextile market is signaled by Solmax’s acquisition of GSE, TenCate Geosynthetics, and Propex. FHWA’s FP-24 specifications require class 1-type A non-woven geotextile for drainage and separation applications after June 2024.

Geotextile Market Size and Forecast

-

Market Size in 2024: USD 7.99 Billion

-

Market Size by 2032: USD 13.40 Billion

-

CAGR: 6.69% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get more information On Geotextile Market - Request Free Sample Report

Geotextile Market Trends:

-

Growing infrastructure development and road construction is driving geotextile demand, accounting for over 45% of total consumption, particularly in emerging economies.

-

Rising focus on soil stabilization and erosion control is boosting adoption, with geotextiles improving soil strength by 30–50% in civil engineering applications.

-

Increasing use in waste management and landfill applications is expanding the market, contributing to over 20% of demand due to lining and filtration requirements.

-

Shift toward sustainable and biodegradable geotextiles is gaining traction, with eco-friendly products witnessing over 10% annual growth.

-

Advancements in nonwoven geotextiles are enhancing filtration and drainage efficiency, capturing more than 60% market share globally.

Moreover, the AASHTO-NTPEP Approved List currently boasts a list of more than 550 geotextile products, which would set explicit quality guidelines for geotextile market research by January 2023. Such upgrades are already improving the share of the geotextile market in civil and environmental applications, supporting product standardization. Considering the need for regulatory compliance, innovation, and durability, the geotextile market is expected to expand in overall market size.

Market Dynamics:

Drivers:

-

Federal infrastructure investments under the Infrastructure Investment and Jobs Act prioritize geotextile usage in highway projects

Large investment from the U.S. federal government, with over $350 billion invested in highways and bridges in the Infrastructure Investment and Jobs Act, has propelled the geotextile market growth as state departments of transportation continue to specify non-woven geotextile fabrics for separation, filtration, and reinforcement in major projects. The Federal Highway Administration has recently issued the FP-24 standard in September 2024, which compels the use of class 1-type A non-woven geotextile fabric in drainage and stabilization applications in driving the geotextile market size since it is a standardized requirement, raising the geotextile market share in federally funded work.

-

Industry consolidation and technological innovation fuel advanced geotextile fabric composites

Key players in the geotextile market are pooling their resources to develop high-quality geotextile fabric composites. Solmax’s TenCate Geosynthetics and GSE Environmental purchases from 2020 highlight consolidation in the field and establish the platform for launching smart geotextile lines with sensor capabilities. These portfolio expansions not only enable more advanced geotextile market analysis but also prepare the geotextile industry to address increasing demands for next-generation performance-based solutions within infrastructure monitoring and maintenance.

Restraints:

-

Ultraviolet degradation vulnerability of non-woven geotextile constrains long-term performance in exposed environments

When exposed to UV light, non-woven polyester and polypropylene geotextiles lose their tensile strength. High-throughput aging tests reveal severe fiber damage after 500–1,000 h exposure to UV light. Thus, Washington State Department of Transportation guidelines suggest that stored geotextiles should be protected from direct UV exposure and that stored geotextiles should be covered or protected from exposure until installation. This vulnerability limits the geotextiles market from growth in exposed drainage applications requiring prolonged UV exposure, which also constitutes a major geotextiles market restraint in long-term environmental solutions.

Segmentation Analysis:

By Material

Synthetic geotextile dominated and held a 77.4% share in 2024. High tensile strength, resistance to UV, and cost effectiveness are the key drivers of the polypropylene subsegment. FHWA FP-24 requires non-woven, polypropylene geotextile to be used for road base stabilization, and good reason. It is the most commonly used material in projects financed by the DOT in highway and infrastructure projects. It's strong enough to withstand your chemical and the test of time! Rigorous regulation and consistency are seeing synthetic fiber as the leading material, impacting the total geotextile market size for transportation, industrial, and construction applications.

Natural geotextile is the fastest-growing segment with a CAGR of 6.92% in the forecast period of 2025 to 2032. Jute emerges as the leading material with the nature of being eco-friendly, biodegradable, and cost-effective. The USDA NRCS Code 342 recommends jute geotextile for preventing topsoil erosion. It is a popular practice in agricultural reclamation and runoff control. Continual environmental standards and efforts for sustainable farming methods are the rising tide for natural materials. These trends underpin long-term growth and diversification of the geotextile marketplace as industries look to employ more sustainable and regenerative land-use options.

By Product

Non-woven geotextile accounted for 63.5% of the market in 2024. Medium-weight non-woven is the prevailing choice because it offers significantly improved filtering and is very easy to use. According to the FHWA rockery guidelines, a non-sprayed layer of type 1-B non-woven fabric is required for sub-surface drainage. These geotextiles are used in drainage, separation, and stabilization applications. Their rapid deployment and versatility over soil types are also ideal for highway construction, landfills, and other civil projects. Heavy federal acceptance and a strong track record have made nonwoven geotextiles the go-to product in the geotextile industry.

Woven geotextile is projected as the fastest-growing segment with a CAGR of 6.96% in the forecast period of 2025 to 2032. Woven high-strength fabrics predominate because of their good tensile strength as well as soil retention features. They are listed by AASHTO M 288 as being one of the accepted types of wall facing for mechanically stabilized earth (MSE) structures. These are designed for use in retaining walls, loading platforms, and geotechnical support systems. Robust structural performance and growing demand in slope stabilization applications are driving growth. They are suitable for load-bearing applications and are particularly popular in civil infrastructure and road development applications.

By Application

Road construction dominated the geotextiles market with a 37.8% market share in 2024. Subgrade separation using non-woven geotextiles is the key driver. FHWA FP-24 requires their use under base aggregates in federally funded road projects. These fabrics extend pavement life and improve stability. DOTs nationwide follow this mandate, ensuring consistent application. Their effectiveness in preventing soil migration and maintaining road performance has made geotextiles a standard in both urban and rural construction. As infrastructure upgrades continue, this segment remains critical to geotextile market growth.

Erosion control emerged as the fastest-growing segment with a CAGR of 7.53% in the forecast period of 2025 to 2032. Non-woven silt fences dominate due to mandatory use under the EPA’s NPDES permit. All U.S. construction sites over one acre must apply erosion control measures using geotextiles. These fences trap sediment, control runoff, and meet stormwater compliance. This strong regulatory backing makes them essential on nearly all development projects. As environmental regulations tighten and green infrastructure expands, erosion control is seeing fast adoption across the geotextile industry.

By End-use Industry

The construction sector dominated the geotextile market with a 41.4% share in 2024. Non-woven fabrics are widely used for roadways, drainage, and retaining walls. FHWA rockery standards require geotextiles for drainage and soil separation, making them mandatory in many public projects. Contractors favor geotextile fabric for reducing settlement and improving long-term structure stability. This segment dominates due to high infrastructure spending, predictable product use, and government standards that promote consistency in engineering and materials selection across multiple civil construction applications.

Agriculture is the fastest-growing end-use industry with a CAGR of 7.66% in the forecast period of 2025 to 2032. Jute geotextiles dominate, driven by use in erosion control, runoff management, and farm slope protection. USDA NRCS Code 342 endorses jute mats for soil conservation, boosting demand under watershed and sustainability programs. As environmental awareness rises and farmers seek natural alternatives, the adoption of geotextile fabric increases. The support from agricultural grants and regulatory programs accelerates geotextile market growth in agriculture and expands its reach into rural infrastructure initiatives.

Regional Analysis:

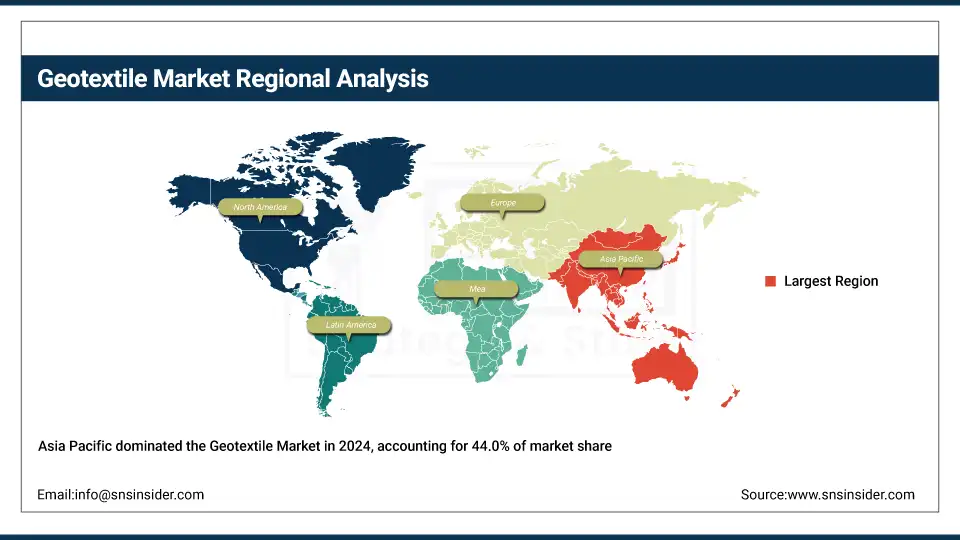

Asia Pacific dominated the geotextile market in 2024 with the largest market share of around 44.0%, driven by large-scale infrastructure investment in China and India. China’s Ministry of Transport mandates geotextile fabric in expressway base layers and slope protection. India’s Bharatmala project under MoRTH integrates non-woven geotextiles for pavement strength and drainage. Rapid urbanization and public infrastructure funding across ASEAN nations also boost adoption. These trends, backed by government mandates, drive the Asia Pacific geotextile market and reinforce its leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America is the second-dominant region with a market share of around 26.0% in the geotextile market in 2024, driven by robust infrastructure development in the U.S. and Canada. The U.S. Department of Transportation mandates non-woven geotextile fabric in federal highway construction under FHWA FP-24. Canada is adopting similar standards for road stabilization and erosion control. State DOTs also mandate geotextile use in stormwater management. Continued investment in transportation infrastructure across the U.S. and growing demand for erosion control fabrics in Canada support regional geotextile market growth.

Europe held an 18.0% market share of the geotextile market in 2024 and is the fastest-growing region with a 7.41% CAGR in the forecasted period of 2025 to 2032. Germany and France lead in non-woven geotextile use for road and rail infrastructure under CEN standards. EU Green Deal funding encourages erosion control and sustainable construction using geotextile fabric. Public procurement regulations support environmentally responsible materials, boosting geotextile market growth. The European Environment Agency’s land protection policies continue to enhance regional demand for biodegradable and synthetic geotextiles.

Latin America is a growing region in the geotextile market due to increasing adoption in road reinforcement and flood management. Brazil leads, supported by DNIT’s use of geotextile fabric in federal road maintenance. Mexico is expanding its use in erosion control and landfill construction. Governments promote sustainable infrastructure with erosion prevention projects funded through public programs. The region’s rising awareness of soil conservation and regulatory backing for environmentally friendly construction materials positions it for steady geotextile market growth.

The Middle East & Africa are emerging in the geotextile market, with rising demand from infrastructure and desert land stabilization projects. The UAE uses non-woven geotextiles in road construction and stormwater systems under the Ministry of Energy and Infrastructure. South Africa’s Department of Water and Sanitation includes geotextile fabric in soil erosion control programs. These nations prioritize sustainable engineering, driving the geotextile market growth. Public infrastructure funding and desertification control efforts further accelerate adoption across the region’s growing construction sector.

Key Players:

The major geotextile market competitors include Propex Operating Company, LLC, NAUE GmbH & Co. KG, Officine Maccaferri S.p.A., Fibertex Nonwovens A/S, HUESKER Synthetic GmbH, SKAPS Industries, Thrace Group, AGRU America, Machina-TST, and Gayatri Polymers & Geo-synthetics.

Recent Developments:

-

In May 2024, Eloor Municipality used coir geotextiles along Panchathodu canal banks to prevent erosion before monsoon, promoting eco-friendly solutions under a ₹2 crore irrigation project in Kerala.

-

In June 2023, Kerala’s Coir Corporation supplied coir geotextiles to Odisha iron ore mines for slope stabilization, supporting erosion control and sustainable mining practices with biodegradable materials.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 7.99 billion |

| Market Size by 2032 | USD 13.40 billion |

| CAGR | CAGR of 6.69% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Material (Natural [Jute, and Others], and Synthetic [Polypropylene, Polyester, Polyethylene, and Others]), •By Product (Woven [Slit Tape Woven, and High Strength Woven], Non-Woven [Light Weight, Medium Weight, Heavy Weight, and Paving Fabrics], and Knitted), •By Application (Road Construction, Erosion Control, Reinforcement, Drainage System, Lining System, Asphalt Overlays and Others), •By End-use Industry (Construction, Transportation, Environmental, Agriculture, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Propex Operating Company, LLC, NAUE GmbH & Co. KG, Officine Maccaferri S.p.A., Fibertex Nonwovens A/S, HUESKER Synthetic GmbH, SKAPS Industries, Thrace Group, AGRU America, Machina-TST, and Gayatri Polymers & Geo-synthetics |

Frequently Asked Questions

UV degradation in non-woven geotextile fabric limits its durability and use in prolonged exposed outdoor conditions.

Top geotextile companies include Solmax, Propex, TenCate Geosynthetics, NAUE, HUESKER, and Fibertex Nonwovens A/S.

Smart geotextiles with sensors and eco-friendly jute-based geotextile fabric are key emerging geotextile market trends.

Federal infrastructure funding and adoption of non-woven geotextile fabric in construction projects are driving strong geotextile market growth.

The global geotextile market size stood at approximately USD 7.99 billion as of 2024.

Get in Touch