Greenhouse Climate Controller Market Report Scope & Overview:

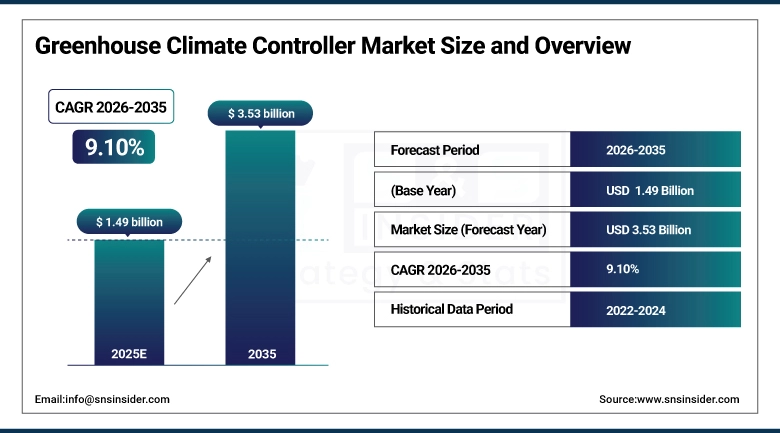

The Greenhouse Climate Controller Market size was valued at USD 1.49 Billion in 2025 and is projected to reach USD 3.53 Billion by 2035, growing at a CAGR of 9.10% during 2026–2035.

A greenhouse without climate control is a glass box that amplifies environmental variation rather than moderating it. Temperature swings between day and night, humidity that spikes after irrigation, CO₂ levels that drop as photosynthesis accelerates in the morning hours each of these deviations from optimal growing conditions translates directly into slower growth rates, higher disease susceptibility, and yield inconsistency that commercial growers cannot absorb in competitive produce markets. Climate controllers solve this not by eliminating environmental variation but by detecting it faster than a human operator can and responding with coordinated adjustments across heating, ventilation, cooling, irrigation, and supplemental CO₂ systems before the deviation becomes a crop problem.

Market Size and Forecast:

-

Market Size in 2025: USD 1.49 Billion

-

Market Size by 2035: USD 3.53 Billion

-

CAGR: 9.10% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Greenhouse Climate Controller Market - Request Free Sample Report

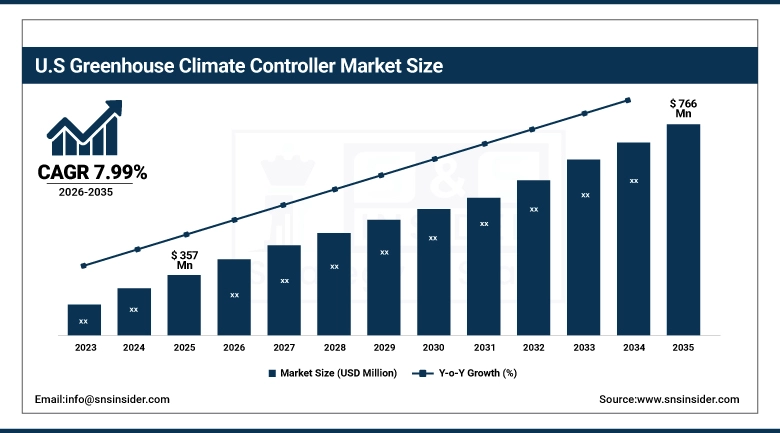

The U.S. Greenhouse Climate Controller Market was valued at USD 357 Million in 2025 and is projected to reach USD 766 Million by 2035, growing at a CAGR of 7.99% during 2026–2035. The U.S. market reflects the dual character of American greenhouse horticulture: a large established sector of conventional greenhouse vegetable and flower growers who are upgrading aging control infrastructure, and a fast-growing vertical and indoor farming segment that is deploying sophisticated multi-parameter climate control as a baseline operational requirement rather than an optional upgrade.

Key Greenhouse Climate Controller Market Trends:

-

Smart IoT controllers replacing conventional systems, enabling remote access, centralized management, and integrated farm data dashboards.

-

Integrated multi-parameter controllers optimize temperature, humidity, CO₂, lighting, and irrigation for coordinated crop performance outcomes.

-

Data-driven crop steering drives demand for highly precise, programmable controllers beyond traditional on/off or PID systems.

-

Vertical farming expansion increases demand for dense, reliable climate control systems without natural environmental fallback support.

-

Energy-focused controllers integrate monitoring, demand optimization, and renewable energy alignment for cost-efficient greenhouse operations.

Greenhouse Climate Controller Market Growth Drivers:

-

Rising Commercial Greenhouse Expansion, Food Security Priorities, and the Proven Yield Impact of Precision Climate Management Are Sustaining Consistent Investment in Climate Controller Upgrades and New Installations

Greenhouse production has been growing as a share of global vegetable, fruit, and cut flower supply for decades, and the commercial logic behind that shift higher yields per land area, year-round production independent of outdoor climate, reduced pesticide uses in controlled environments, shorter supply chains to urban markets has not weakened. What has changed is the scale at which that logic is now being acted on. The Netherlands, Spain, China, and increasingly Mexico have all expanded protected agriculture footprints significantly since 2020, and each new greenhouse structure requires climate control hardware and software as a functional prerequisite for commercial operation. Existing greenhouse operators upgrading aging control infrastructure represent an equally important demand channel.

Greenhouse Climate Controller Market Restraints:

-

High System Complexity, Upfront Investment Costs, and the Technical Skills Required for Optimal Deployment Are Limiting Adoption Among Small and Medium-Scale Greenhouse Operators

The performance case for advanced greenhouse climate control is well established, but the barriers to acting on it are real for the large segment of the global greenhouse sector that consists of small and medium-scale operations. A fully integrated multi-parameter climate control system sensors for temperature, humidity, CO₂, light intensity, and soil moisture; actuators for ventilation, heating, cooling, shading, and irrigation; a controller platform with programming capability and remote access; and integration with weather data feeds and crop management software represents a capital outlay that a small greenhouse operation may not be able to finance against uncertain payback timelines.

Greenhouse Climate Controller Market Opportunities:

-

AI-Integrated Climate Optimization, Emerging Market Greenhouse Expansion, and Cannabis Cultivation Infrastructure Are Creating Commercial Growth Pathways That Extend Well Beyond Traditional Horticulture Applications

The integration of machine learning models into greenhouse climate control platforms is moving from proof-of-concept demonstration to commercial product deployment, and the value proposition is specific enough to drive purchasing decisions: AI-driven climate optimization that learns crop response patterns across growing cycles and adjusts setpoints to track moving optima rather than fixed targets can deliver incremental yield improvements even in operations that are already running conventional digital control well. For high-value crops like tomatoes, peppers, herbs, and cannabis where per-kilogram revenues justify technology investment at granular levels, the ROI calculation works.

Greenhouse Climate Controller Market Segment Analysis:

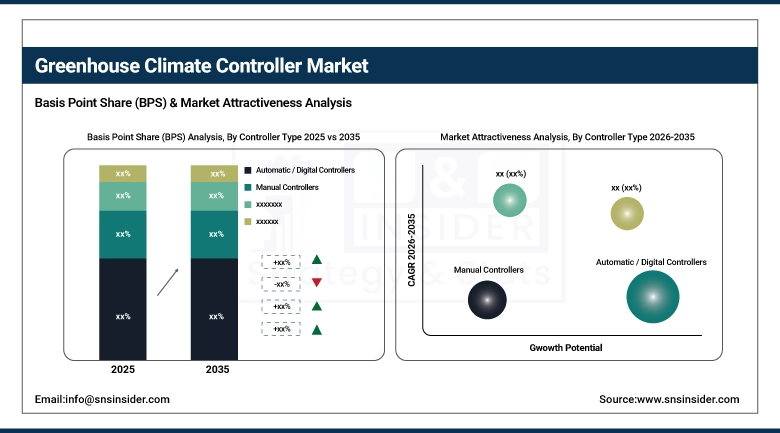

By Controller Type: Automatic / Digital Controllers Lead While Smart IoT-Enabled Controllers Drive the Fastest Growth Through 2035

Automatic / Digital Controllers dominated with a 41.35% share in 2025, valued at approximately USD 614 Million, while Smart IoT-Enabled Controllers are expected to grow at the fastest CAGR of approximately 12.83% through 2035.

Automatic and digital controllers maintain their leading position because they represent the installed base standard across commercial greenhouse operations globally the majority of operating greenhouses that have progressed past manual control are running digital controller platforms that manage setpoints programmatically and coordinate multiple systems within a defined zone. These platforms are functionally adequate for a large proportion of commercial growing operations and are familiar to the grower workforce.

By Control Parameter: Temperature Control Leads While Multi-Parameter / Integrated Control Drives the Fastest Growth Through 2035

Temperature Control dominated with a 34.72% share in 2025, valued at approximately USD 516 Million, while Multi-Parameter / Integrated Control is expected to grow at the fastest CAGR of approximately 12.05% through 2035.

Temperature control retains its leading share because it is the foundational parameter of greenhouse management every greenhouse climate controller, regardless of sophistication level, manages temperature as its primary function, and temperature sensor and actuator hardware represents the largest component of climate control installation costs. The parameter's physiological primacy ensures its market share stability even as more complex control approaches gain adoption.

By Application: Vegetable & Fruit Farming Leads While Commercial & Industrial Greenhouses Drive the Fastest Growth Through 2035

Vegetable & Fruit Farming dominated with a 34.27% share in 2025, valued at approximately USD 509 Million, while Commercial & Industrial Greenhouses are expected to grow at the fastest CAGR of approximately 11.88% through 2035.

Vegetable and fruit farming holds its leading application share because it represents the commercial core of protected agriculture tomatoes, cucumbers, peppers, lettuce, and strawberries grown under glass or film cover constitute the largest segment of greenhouse-grown food by volume and value globally, and their climate sensitivity makes controller investment directly economically justifiable.

By End-User: Large-Scale Commercial Growers Lead and Are Also Expected to Grow Fastest Through 2035

Large-Scale Commercial Growers dominated with a 38.72% share in 2025, valued at approximately USD 575 Million, and are also expected to grow at the fastest CAGR of approximately 10.23% through 2035, holding both the dominant and fastest-growing positions in this segment. Large commercial operations hold their leadership because they concentrate capital, agronomic expertise, and energy management focus in ways that justify sophisticated climate control investment and generate the scale of procurement that shapes vendor product roadmaps. Their sophistication as buyers also accelerates the capability advancement of the controller platforms they purchase enterprise growers specify features and integration requirements that suppliers then bring to the broader market.

Greenhouse Climate Controller Market Regional Analysis:

Europe Greenhouse Climate Controller Market Insights

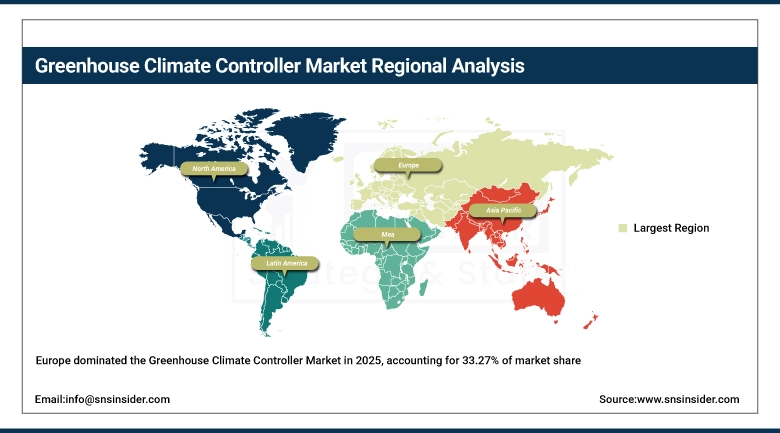

Europe led the Greenhouse Climate Controller Market in 2025, accounting for 33.27% of market share, valued at USD 494 Million, and is expected to reach USD 1.05 Billion by 2035 at a CAGR of 7.88% during the forecast period. Europe's market leadership is anchored in the Netherlands, which is home to the world's most technologically sophisticated commercial greenhouse sector by unit area, and in Spain, where the Almeria province’s vast plastic greenhouse complex represents the largest concentration of protected vegetable cultivation in Europe.

Get Customized Report as per Your Business Requirement - Enquiry Now

Netherlands Greenhouse Climate Controller Market Insights

The Netherlands is the dominant national market within Europe and one of the most influential globally in setting the technical standard for greenhouse climate control systems. Dutch greenhouse operators function as technology early adopters whose specifications become the baseline for what the rest of the global industry expects from a production-grade climate controller.

North America Greenhouse Climate Controller Market Insights

North America held a 27.84% share of the Greenhouse Climate Controller Market in 2025, valued at USD 413 Million, and is expected to reach USD 906 Million by 2035 at a CAGR of 8.20% during the forecast period. The region's market is shaped by two overlapping procurement drivers: the upgrade cycle among established greenhouse vegetable growers in Ontario, Ohio, Pennsylvania, and Texas who are replacing equipment installed during the early 2000s greenhouse expansion wave, and the new installation activity from vertical farming operators, cannabis cultivation facilities, and food manufacturer-owned controlled environment agriculture programs that are deploying IoT-connected climate control as standard infrastructure.

U.S. Greenhouse Climate Controller Market Insights

The United States accounts for 86.3% of North American demand in 2025. The U.S. Greenhouse Climate Controller Market was valued at USD 357 Million in 2025 and is projected to reach USD 766 Million by 2035, growing at a CAGR of 7.99% during 2026–2035. The cannabis cultivation sector has been a particularly important demand driver in states with established adult-use or medical cultivation frameworks, where operations specify precision climate control platforms as a standard production input and where the revenue per square foot justifies controller investment at levels that conventional horticulture economics would not support.

Asia Pacific Greenhouse Climate Controller Market Insights

Asia Pacific is expected to grow at the fastest CAGR of approximately 11.64% from 2026 to 2035, rising from USD 355 Million in 2025 to USD 1.07 Billion by 2035. The region’s growth leadership reflects greenhouse infrastructure expansion programs in China, Japan, South Korea, India, and Southeast Asia that are building protected agriculture capacity to address food security, climate adaptation, and import substitution objectives simultaneously. China’s investment in domestic greenhouse vegetable production to reduce dependence on seasonal outdoor supply from distant growing regions is generating large-scale procurement of climate control systems at both national demonstration farm projects and private commercial greenhouse construction programs. Japan’s plant factory sector, which has operated for decades at the technical frontier of fully controlled indoor growing, is a reference market for the most sophisticated multi-parameter and AI-integrated climate control systems deployed anywhere globally.

China Greenhouse Climate Controller Market Insights

China is the dominant national market within Asia Pacific by volume, driven by the scale of its protected agriculture expansion, government subsidy programs for smart greenhouse technology adoption, and the rapid growth of domestic climate controller suppliers who are producing systems competitive with European and Japanese products at lower price points.

Latin America and Middle East & Africa Greenhouse Climate Controller Market Insights

Latin America held approximately 8.46% of the global Greenhouse Climate Controller Market in 2025, valued at USD 126 Million, and is expected to reach USD 290 Million by 2035 at a CAGR of 8.78% during the forecast period. Mexico is the primary market, anchored by the Sinaloa, Sonora, and Baja California greenhouse clusters that supply a large share of winter vegetable exports to the United States. These operations have been investing in climate controller upgrades driven both by crop quality requirements from U.S. retail buyers and by water management needs in water-scarce growing regions where precision irrigation-integrated climate control reduces consumption per kilogram of output. Middle East & Africa held approximately 6.52% of market share in 2025, valued at USD 97 Million, and is expected to reach USD 221 Million by 2035 at a CAGR of 8.62% during the forecast period. UAE and Saudi Arabia are the most advanced markets, where government food security programs have funded substantial controlled environment agriculture infrastructure including sophisticated climate-controlled greenhouse and vertical farming facilities.

Competitive Landscape for Greenhouse Climate Controller Market:

Priva is a Dutch agricultural technology company that has operated at the center of greenhouse climate control development for over sixty years. The company’s climate control platforms built around the Priva Connext and Priva Compass software environments — are the reference standard for large-scale commercial greenhouse operations globally, with deployments spanning high-wire tomato and cucumber operations in the Netherlands, berry production in Spain and Morocco, and food manufacturer-owned greenhouse facilities in North America and the Middle East.

In February 2025, Priva announced the release of Priva Connext 5.0, incorporating an AI-driven climate advisor module that analyzes historical crop response data alongside real-time environmental measurements to generate setpoint recommendations calibrated to the specific crop, growth stage, and energy tariff conditions of each individual greenhouse operation.

Argus Control Systems is a Canadian greenhouse automation company that has built a strong position in the North American commercial greenhouse market through its Argus Titan and Argus Supervisor climate control platforms. The company serves large-scale vegetable and cannabis production operations across Canada and the United States, with particular depth in the Ontario and British Columbia greenhouse corridors where some of North America’s largest commercial tomato and pepper operations are concentrated. Argus’s systems are known among commercial growers for their reliability in high-humidity, high-temperature environments, their flexibility in handling non-standard greenhouse structures and heating system configurations, and the responsiveness of their technical support operation to grower-specific commissioning requirements.

In April 2025, Argus Control Systems launched a new version of its Argus Supervisor web interface with native mobile application support, allowing growers to monitor and control all greenhouse zones, view real-time sensor readings, receive threshold-based alerts, and execute override commands from iOS and Android devices without requiring a VPN connection.

Greenhouse Climate Controller Market Key Players:

-

Priva Holding B.V.

-

Argus Control Systems Ltd.

-

Ridder Group

-

Hoogendoorn Growth Management

-

Certhon B.V.

-

Netafim Ltd.

-

Climate Control Systems Inc.

-

Delta-T Solutions

-

DENSO Corporation

-

Heliospectra AB

-

Autogrow Systems Ltd.

-

Sensaphone

-

Link4 Corporation

-

Growlink

-

Agricultural Electronics Corporation

-

HortiMaX

-

Logiqs B.V.

-

LettUs Grow

-

Rough Brothers Inc.

-

Munters

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.49 Billion |

| Market Size by 2035 | USD 3.53 Billion |

| CAGR | CAGR of 9.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Controller Type Segmentation (Manual Controllers, Automatic / Digital Controllers, Hybrid Controllers, and Smart IoT-Enabled Controllers) • By Control Parameter (Temperature Control, Humidity Control, CO₂ / Gas Concentration Control, and Multi-Parameter / Integrated Control) • By Application (Horticulture & Floriculture, Vegetable & Fruit Farming, Research & Academic Greenhouses, and Commercial & Industrial Greenhouses) • By End-User (Small & Medium Farmers, Large-Scale Commercial Growers, Research Institutions, and Government / Agricultural Agencies) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Priva Holding B.V., Argus Control Systems Ltd., Ridder Group, Hoogendoorn Growth Management, Certhon B.V., Netafim Ltd., Climate Control Systems Inc., Delta-T Solutions, DENSO Corporation, Heliospectra AB, Autogrow Systems Ltd., Sensaphone, Link4 Corporation, Growlink, Agricultural Electronics Corporation, HortiMaX, Logiqs B.V., LettUs Grow, Rough Brothers Inc., Munters. |

Frequently Asked Questions

The Greenhouse Climate Controller Market is expected to grow at a CAGR of 9.10% from 2026-2035.

North America dominated the Greenhouse Climate Controller Market in 2025.

Automatic / Digital Controllers dominated the Greenhouse Climate Controller Market.

Rising demand for precision agriculture, automation, energy efficiency, and high-yield crop production drives market growth.

The Greenhouse Climate Controller Market size was USD 1.49 Billion in 2025 and is expected to reach USD 3.53 Billion by 2035.

Get in Touch