Coffee Substitute Market Report Scope & Overview:

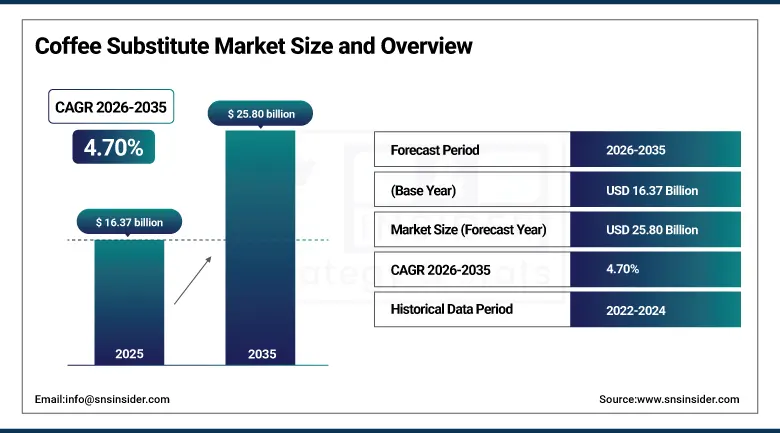

The Coffee Substitute Market was valued at USD 16.37 Billion in 2025 and is expected to reach USD 25.80 Billion by 2035, growing at a CAGR of 4.70% from 2026 to 2035.

The global coffee substitute market has been one of the fastest growing segments in the functional and health-conscious beverage industry, a trend that mirrors a broader consumer movement away from traditional caffeinated beverages toward plant-based, adaptogenic and nutrient-enhanced alternatives. Growing awareness of caffeine sensitivity, chronic health conditions, the burgeoning vegan lifestyle movement and the quest for clean-label beverage experiences have fuelled an ever more diverse portfolio of products made from chicory root, roasted grains, herbal botanicals, adaptogenic mushrooms and proprietary natural blends. Coffee alternatives are being increasingly marketed as health drinks that contain prebiotics, antioxidants, nootropics and gut-health ingredients, making them appealing not only to people who are sensitive to caffeine but also to the broader market of health-conscious consumers.

Nestlé S.A. reported that its coffee brands sourced approximately 32% of green coffee through regenerative agriculture programs in 2024, highlighting the growing consumer and industry focus on sustainable, wellness-oriented beverage ecosystems that are also influencing innovation and purchasing decisions within the coffee substitute market.

Market Size and Forecast

-

Market Size in 2026E: USD 17.06 Billion

-

Market Size by 2035: USD 25.80 Billion

-

CAGR: 4.70% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get more information on Coffee Substitute Market - Request Free Sample Report

Coffee Substitute Market Trends

-

Rising demand for caffeine-free functional beverages is boosting adoption of mushroom and herbal coffee alternatives.

-

Expansion of online retail channels is increasing access to specialty coffee substitute brands worldwide.

-

Clean-label and organic trends are driving innovation in chicory- and grain-based products.

-

Growing health and wellness awareness is fueling demand for functional coffee substitutes with added nutritional benefits.

-

Premiumization of RTD beverages is creating opportunities for innovative coffee alternative product launches.

The U.S. Coffee Substitute Market Outlook

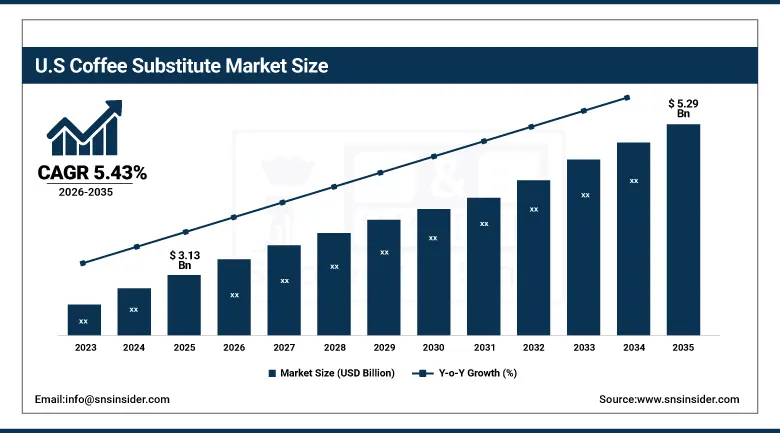

The U.S. Coffee Substitute Market was valued at USD 3.13 Billion in 2025 and is expected to reach USD 5.29 Billion by 2035, growing at a CAGR of 5.43%.

The US is the biggest single country market in North America for coffee alternatives and one of the most innovative markets in the world, with a highly health literate consumer base, a vibrant startup ecosystem for functional foods and beverages, and the most developed health and wellness retail infrastructure in the world. The growing rates of anxiety disorders, caffeine-induced sleep disruption, and gastrointestinal sensitivity among U.S. consumers has created a structurally favourable demand environment for non-caffeinated beverage alternatives offering functional wellness benefits without the stimulant side effects of traditional coffee. The U.S. market is witnessing the rise of direct-to-consumer brands that use subscription models, social media marketing, and wellness-focused communities, driven by strong demand for premium and adaptogenic formulations.

MUD\WTR Inc., a leading U.S.-based coffee alternative brand, announced in 2025 that its mushroom-based morning ritual blends had surpassed 1 million cumulative subscribers, reflecting the scale of consumer willingness to replace conventional coffee with adaptogenic and functional beverage systems that deliver sustained energy, mental clarity, and immune support without caffeine dependency cycles.

Coffee Substitute Market Segment Analysis

-

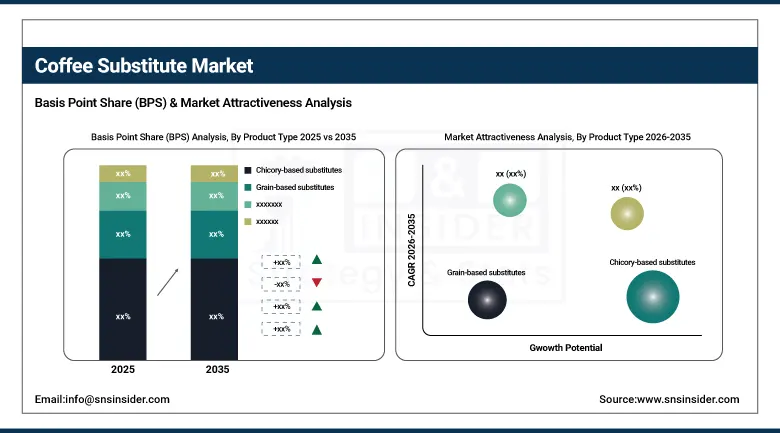

By Product Type, chicory-based substitutes dominated the market with 34.15% share in 2025, while mushroom-based coffee alternatives are the fastest growing product type with the highest CAGR of 5.69% from 2026 to 2035.

-

By Form, powder dominated the market with 42.16% share in 2025, while ready-to-drink (RTD) beverages is the fastest growing form with the highest CAGR of 5.60% from 2026 to 2035.

-

By Distribution Channel, supermarkets & hypermarkets dominated the market with 36.15% share in 2025, while online retail/e-commerce is the fastest growing channel with the highest CAGR of 5.95% from 2026 to 2035.

-

By End User, health-conscious consumers dominated the market with 37.15% share in 2025, while the fitness & wellness community is the fastest growing end user segment with the highest CAGR of 5.38% from 2026 to 2035.

By Product Type, chicory-based substitutes dominate the coffee substitute market, while mushroom-based coffee alternatives are the fastest-growing segment.

Chicory-based substitutes segment dominated the market with the highest revenue share of about 34.15% in 2025 due to their long-established market presence, familiar roasted flavor profile closely resembling traditional coffee, and wide availability across mainstream retail channels. Chicory root's well-documented inulin content providing prebiotic and digestive health benefits has made it the most commercially accessible and consumer-trusted category within the coffee substitute market, supporting strong repeat purchase rates across health-conscious and caffeine-sensitive consumer cohorts in North America and Europe.

Mushroom-based coffee alternatives segment is estimated to register the highest CAGR of 5.69% during the forecast period of 2026–2035 owing to surging consumer interest in adaptogenic functional ingredients, including lion's mane, chaga, reishi, and cordyceps mushrooms, which are associated with cognitive enhancement, immune modulation, and stress resilience. The segment's growth is further propelled by the proliferation of wellness influencer communities, functional beverage startups, and premium direct-to-consumer brands that have elevated adaptogenic mushroom beverages from niche wellness products into mainstream lifestyle categories.

By Form, powder dominates the coffee substitute market, while ready-to-drink (RTD) beverages is the fastest-growing segment.

Powder segment dominated the market with the largest revenue share of about 42.16% in 2025 attributed to its versatility in preparation, longer shelf life, and ease of customization in terms of serving size and blending with plant-based milks and functional additives. The powder format's compatibility with home brewing rituals and the consumer preference for preparing beverages that mirror conventional coffee preparation methods have sustained its dominant position across both health and wellness retail and direct-to-consumer e-commerce platforms globally.

Ready-to-drink (RTD) beverages segment is projected to witness the fastest CAGR of 5.60% during 2026–2035 due to rising consumer preference for on-the-go functional beverage consumption, the expansion of cold chain retail infrastructure, and the growing appetite for convenient premium wellness beverages among time-pressed urban professionals and fitness-oriented demographics. The segment's growth is also supported by increasing product innovation in cold-brew-style coffee substitute RTDs that deliver both functional benefits and sensory experiences comparable to conventional coffee shop beverages.

By Distribution Channel, supermarkets & hypermarkets dominate the coffee substitute market, while online retail/e-commerce is the fastest-growing channel.

Supermarkets & hypermarkets segment emerged as the market leader with a dominant share of around 36.15% in 2025 owing to their expansive shelf space allocation for health and wellness products, their role as the primary purchasing destination for mainstream grocery shopping, and the increasing placement of coffee substitute products within dedicated organic and functional food sections across major retail chains in North America and Europe. The segment benefits from broad consumer access, impulse purchasing behavior, and the growing integration of private-label coffee substitute offerings by major supermarket chains.

Online retail/e-commerce segment is anticipated to record the fastest CAGR of 5.95% throughout the forecast period of 2026–2035 driven by the explosive growth of direct-to-consumer brand ecosystems, the effectiveness of social media-driven product discovery for wellness categories, and the subscription commerce model which delivers high consumer lifetime value and repeat purchase frequency. The low barriers to market entry through e-commerce platforms have enabled a new generation of specialized coffee substitute brands to achieve national and international scale without legacy retail distribution dependencies.

By End User, health-conscious consumers dominate the coffee substitute market, while the fitness & wellness community is the fastest-growing segment.

Health-conscious consumers segment dominated the coffee substitute market with the highest revenue share of about 37.15% in 2025 owing to their proactive engagement with functional nutrition, willingness to pay premium pricing for clean-label and organic-certified products, and their role as early adopters and brand ambassadors within the broader wellness beverage category. This consumer cohort's growing awareness of the physiological effects of chronic caffeine consumption, including adrenal fatigue, sleep disruption, and anxiety amplification, has made coffee substitutes an attractive permanent dietary modification rather than a temporary lifestyle experiment.

Fitness & wellness community segment is projected to witness the fastest CAGR of 5.38% during the forecast period of 2026–2035 due to the rapid expansion of the global fitness economy, the integration of functional adaptogens and nootropics into athletic performance and recovery protocols, and the growing alignment between coffee substitute product positioning and the pre-workout, cognitive enhancement, and stress management use cases that resonate with active lifestyle consumers. Rising brand collaborations between coffee substitute companies and fitness influencers, gym chains, and sports nutrition retailers are further accelerating segment penetration.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.54% |

|

Europe |

Germany |

31.13% |

|

Asia Pacific |

China |

40.20% |

|

Middle East & Africa |

UAE |

31.60% |

|

Latin America |

Brazil |

44.10% |

North America Coffee Substitute Market Insights

North America is the second-largest coffee substitute market worldwide, holding a 24.06% revenue share in 2025, with the United States accounting for 82.54% of North American revenues. The region's market dynamics include the highest concentration of functional beverage start-up activity in the world, the largest direct-to-consumer e-commerce ecosystem for wellness products, and a consumer base that is more open to adoptogenic mushroom and plant-based coffee alternatives with cognitive and stress-resilience benefits. The expanding wellness retail infrastructure and health-conscious urban demographic base, a step behind U.S. trends, provide incremental growth opportunities for Canada throughout the forecast period.

More than 70% of U.S. consumers actively seek functional food and beverage products, supporting demand for mushroom-, chicory-, and adaptogen-based coffee alternatives. The region records some of the world's highest subscription-based wellness beverage adoption rates, with over 45 million Americans subscribed to recurring consumer goods services.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Coffee Substitute Market Insights

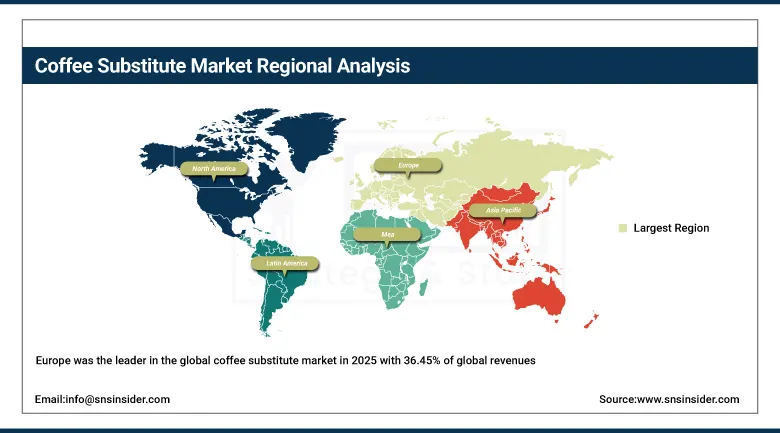

Europe was the leader in the global coffee substitute market in 2025 with 36.45% of global revenues and Germany leading in regional revenue. The market leadership in Europe is a reflection of the continent's deeply embedded coffee culture coupled with one of the world's most health-literate and regulatory-aware consumer populations, providing ideal conditions for the adoption of chicory-based and herbal coffee alternatives that have historical precedents across German, Belgian and French culinary traditions. The maturity of the European organic food and beverage market and the strict clean-label regulatory standards under the EU food safety frameworks have made Europe the global benchmark for production and consumption of quality-certified coffee substitutes.

Europe accounts for over 85% of global chicory root production, making it the historical center of chicory-based coffee substitute consumption. Germany alone consumes over 160 liters of coffee and coffee-like beverages per capita annually, creating a strong market for caffeine-free alternatives

Asia Pacific Coffee Substitute Market Insights

Asia Pacific is the fastest growing coffee substitute market with a CAGR of 5.51% through 2035. China represents roughly 35.20% of the Asia-Pacific revenues, boosted by the nation’s massive and rapidly growing middle class, deep cultural familiarity with herbal and botanical beverage traditions that supports consumer acceptance of non-coffee plant-based alternatives, and government support for the development of the functional food and nutraceutical industry as part of the Healthy China 2030 initiative. India is a high-growth, country-level opportunity with expanding urban wellness consumer demographics and rising e-commerce penetration enabling access to speciality coffee substitute brands, and the country’s established cultural affinity for herbal and Ayurvedic functional beverages that are philosophically aligned with the coffee substitute product category.

The functional beverage sector in Asia Pacific has expanded by more than 60% over the past five years, driven by growing wellness awareness. Japan and South Korea collectively represent over 25 million regular consumers of functional and fortified beverages, supporting coffee substitute adoption.

MEA & Latin America Coffee Substitute Market Insights

Middle East and Africa and Latin America are commercially strategic emerging market opportunities for the coffee substitute industry, both regions exhibiting rising functional food and beverage consumption patterns in line with growing middle-class health awareness and urbanisation trends. The UAE, which accounts for MEA regional revenues, is the most important hub for regional market development based on its high per-capita consumer spending capacity, its well-developed retail infrastructure that includes premium supermarket chains and health speciality stores, and its significant health-conscious expatriate population that imports wellness consumption trends from Western markets. Brazil is the leader in the Latin American market, due to its strong agricultural processing capabilities and a growing urban middle class population that is adopting wellness-focused eating habits.

Brazil has over 40 million consumers actively purchasing health-oriented food and beverage products, creating opportunities for coffee alternative brands. GCC countries import over 90% of their specialty food and beverage products, facilitating market entry for premium coffee substitutes. Wellness-focused consumer spending in the Middle East has risen by more than 35% since 2020, increasing demand for functional beverage alternatives.

Market Dynamics

Growth Drivers: Rising health consciousness and functional beverage demand

The fundamental demand driver for the coffee substitute market across all regions and demographic segments is the reorientation of global consumer structures to preventive health management, reduction of risk for chronic disease, and holistic wellness lifestyles. Growing clinical and consumer awareness linking excessive caffeine consumption to anxiety disorders, cardiovascular stress, sleep architecture disruption and adrenal fatigue has prompted a significant and growing cohort of consumers to permanently transition from conventional coffee to functional alternatives that offer similar morning ritual satisfaction without the physiological dependencies and side effects associated with caffeine. Coffee alternatives are seeing traction among traditional health-conscious consumers as adaptogenic mushrooms gain mainstream awareness, thanks to endorsements from athletes, wellness influencers and functional medicine practitioners.

Restraints: Consumer taste skepticism and premium pricing barriers

The coffee substitute market faces meaningful demand-side friction from the deeply entrenched sensory expectations of conventional coffee consumers, whose taste preferences for the specific flavor profile, aroma chemistry, and caffeine stimulation of roasted coffee beans represent a significant behavioral barrier to product trial and sustained adoption of substitute alternatives. Despite continuous product development investment by leading manufacturers to narrow the sensory gap between coffee substitutes and conventional coffee, the organoleptic differentiation remains a material purchase barrier for the majority of global coffee consumers who are not primarily motivated by health concerns. The premium pricing of mushroom-based and botanical coffee substitutes, often 200–400% higher than conventional coffee, limits adoption among price-sensitive consumers and in emerging markets.

Opportunities: Product innovation and expanding e-commerce distribution

The coffee substitute market is on the verge of a major innovation cycle led by advances in flavour science, functional ingredient extraction technology and personalised nutrition with the potential to dramatically close the sensory and functional gap between substitute products and conventional coffee. Fermentation-based flavour development and precision botanical blending and encapsulation technologies for adaptogenic botanicals are facilitating the creation of a new generation of coffee replacement products that more closely mimic the roasted coffee sensory experience while providing superior functional benefit profiles. E-commerce, subscription selling and social media-driven product discovery are all helping coffee substitute brands reach consumers and scale more efficiently at lower marketing and distribution costs.

Recent Developments:

-

2026: Four Sigmatic Foods Inc. introduced a new line of single-serve compostable capsule coffee substitutes compatible with standard pod brewing systems, combining organic mushroom extract blends with fair-trade roasted grain bases for premium home brewing convenience.

-

2026: RYZE Superfoods LLC secured Series B growth funding and announced expansion of its mushroom coffee substitute distribution into European markets, with initial retail partnerships established in the United Kingdom, Germany, and the Netherlands.

-

2025: Nestlé S.A. expanded its wellness beverage portfolio with a new range of mushroom-infused coffee substitute blends incorporating lion's mane and chaga extracts, targeting the mainstream health and wellness retail channel across European and North American markets.

-

2025: MUD\WTR Inc. launched its upgraded mushroom latte mix with enhanced adaptogenic dosing and a new RTD ready-to-drink format targeting on-the-go wellness consumers across U.S. convenience and specialty retail outlets.

Coffee Substitute Market Key Players are:

-

Nestlé S.A.

-

Teeccino Caffe Inc.

-

Postum Holdings LLC

-

Rasa Inc.

-

MUD\WTR Inc.

-

Four Sigmatic Foods Inc.

-

Laird Superfood Inc.

-

Dandy Blend Inc.

-

Pero Foods Inc.

-

Caf-Lib USA Inc.

-

Nature's Cupboard Pty Ltd. (Nature's Cuppa)

-

Chikko Not Coffee GmbH

-

Barleycup Ltd.

-

Bambu Instant GmbH (A.Vogel)

-

Mount Hagen GmbH

-

Crio Bru LLC

-

Om Mushroom Superfood LLC

-

Renude Inc.

-

RYZE Superfoods LLC

-

London Nootropics Ltd.

Coffee Substitute Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 16.37 Billion |

| Market Size by 2035 | USD 25.80 Billion |

| CAGR | CAGR of 4.70 % From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Chicory-based Substitutes, Grain-based Substitutes (Barley, Rye, Roasted Grains), Herbal Coffee Substitutes, Mushroom-based Coffee Alternatives, Others (Date Seed, Carob, Blends)) • By Form (Powder, Instant Mix, Ready-to-Drink (RTD) Beverages, Capsules/Pods) • By Distribution Channel (Supermarkets & Hypermarkets, Health & Wellness Stores, Online Retail/E-commerce, Specialty Stores (Organic/Functional Foods), Cafés & Foodservice) • By End User (Health-Conscious Consumers, Caffeine-Sensitive Individuals, Vegan/Clean-Label Consumers, Fitness & Wellness Community, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Nestlé S.A., Teeccino Caffe Inc., Postum Holdings LLC, Rasa Inc., MUD\WTR Inc., Four Sigmatic Foods Inc., Laird Superfood Inc., Dandy Blend Inc., Pero Foods Inc., Caf-Lib USA Inc., Nature's Cupboard Pty Ltd (Nature's Cuppa), Chikko Not Coffee GmbH, Barleycup Ltd., Bambu Instant GmbH (A.Vogel), Mount Hagen GmbH, Crio Bru LLC, Om Mushroom Superfood LLC, Renude Inc., RYZE Superfoods LLC, London Nootropics Ltd. |

Frequently Asked Questions

The coffee substitute market is expected to grow at a CAGR of 4.70% from 2026 to 2035.

The Coffee Substitute Market was valued at USD 16.37 Billion in 2025.

The primary growth drivers include rising health consciousness, increasing caffeine sensitivity, growing demand for plant-based and functional beverages, and expanding e-commerce access to specialty coffee substitute products.

Mushroom-based Coffee Alternatives is the fastest-growing product type in the coffee substitute market, with a CAGR of 5.69% from 2026 to 2035.

Europe dominated the coffee substitute market in 2025, holding 36.45% of global revenues, with Germany accounting for 26.13% of European revenues.

Get in Touch