Grey Hydrogen Market Report Scope & Overview:

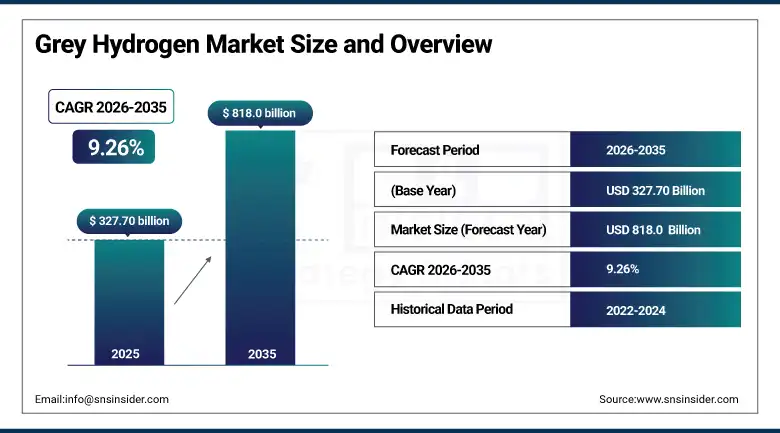

The Grey Hydrogen market was valued at USD 327.70 billion in 2025 and is expected to reach USD 818.0 billion by 2035, growing at a CAGR of 9.26% from 2026–2035.

Grey hydrogen represents the dominant form of hydrogen production in the global hydrogen economy, defined by its production from fossil fuel feedstocks including natural gas, coal, and petroleum derivatives through thermochemical conversion processes including steam methane reforming, coal gasification, and partial oxidation that generate hydrogen alongside carbon dioxide emissions that are vented to the atmosphere rather than captured and stored, distinguishing grey hydrogen from blue hydrogen where equivalent fossil fuel-based production processes incorporate carbon capture and storage to reduce the net CO2 emissions intensity per kilogram of hydrogen produced. Despite its carbon intensity disadvantage relative to green hydrogen produced through renewable-powered water electrolysis, grey hydrogen currently supplies approximately 95% of global hydrogen production across all applications and will remain the dominant hydrogen production pathway for the foreseeable future given the vast scale of existing fossil fuel-based hydrogen production infrastructure, the significant cost advantage of steam methane reforming over electrolysis at current electricity prices, and the enormous capital investment required to transition even a fraction of existing grey hydrogen production to lower-carbon alternatives.

The International Energy Agency's 2025 Global Hydrogen Review confirming that global hydrogen demand reached 97 million tonnes in 2024, with over 90 million tonnes produced from fossil fuels without carbon capture, demonstrates the extraordinary scale of the existing grey hydrogen market whose industrial applications represent demand that cannot be rapidly substituted regardless of the policy ambitions of national green hydrogen strategies whose production volumes remain a small fraction of current grey hydrogen output.

Market Size and Forecast

-

Market Size in 2026E: USD 357.94 Billion

-

Market Size by 2035: USD 818.0 Billion

-

CAGR: 9.26% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Grey Hydrogen Market - Request Free Sample Report

Grey Hydrogen Market Trends

-

Expanding petroleum refinery hydrogen consumption as increasingly stringent transportation fuel sulphur and aromatic content specifications require deeper hydro processing of crude oil fractions that consume hydrogen in proportion to the extent of sulphur removal and molecular restructuring required to produce Euro VI, EPA Tier 3, and equivalent clean fuel standards that regulators in major markets are implementing on accelerated timelines.

-

Growing ammonia production from grey hydrogen driven by expanding global fertilizer demand as the world's population growth and dietary improvement in developing economies collectively expand agricultural production requirements that nitrogen fertilizers support, with ammonia's central role in the Haber-Bosch synthesis process creating inelastic hydrogen demand that scales with global food production requirements.

-

Increasing deployment of hydrogen in steel direct reduction applications as steel producers in regions including Middle East, India, and North Africa invest in direct reduction iron facilities that use hydrogen as a reducing agent rather than the coke-fueled blast furnace route, with the DRI-EAF route providing cost and quality advantages over blast furnace steelmaking when competitively priced hydrogen is accessible.

-

Progressive deployment of carbon capture equipment at existing steam methane reforming facilities converting grey hydrogen production to blue hydrogen as carbon price mechanisms, corporate net-zero commitments, and regulatory mandates create financial justification for CO2 capture retrofit investment, gradually reducing grey hydrogen's share of total production while the SMR infrastructure base itself continues expanding.

-

Growing interest in coal gasification-based hydrogen production in China, India, and other coal-abundant economies where the relative cost advantage of coal over natural gas as a hydrogen feedstock makes gasification economically competitive despite higher CO2 emissions intensity per kilogram of hydrogen produced than natural gas SMR.

The U.S. Grey Hydrogen Market Outlook

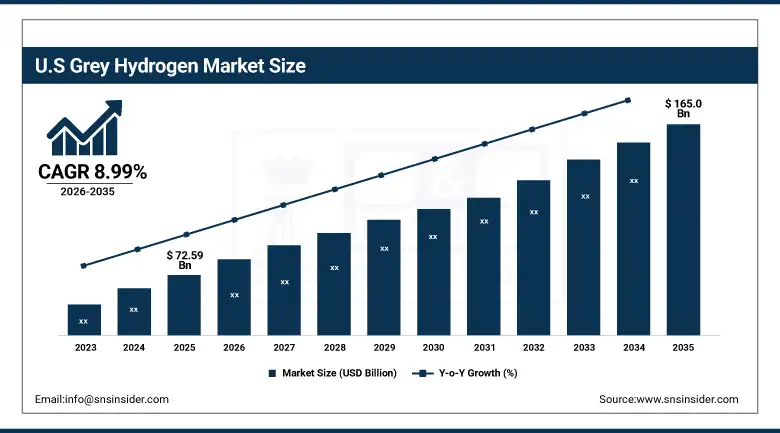

The U.S. Grey Hydrogen Market was valued at approximately USD 72.59 billion in 2025 and is expected to reach approximately USD 165.0 billion by 2035, growing at a CAGR of 8.99%, driven by high industrial demand from petroleum refineries and chemical sectors, abundant natural gas supply enabling cost-competitive SMR production, established hydrogen production and pipeline distribution infrastructure, and increasing investments in hydrogen-based energy solutions supporting large-scale industrial adoption.

The United States is the world's largest national grey hydrogen market by production volume and the geography with the most extensive hydrogen pipeline and distribution infrastructure, where the Gulf Coast hydrogen pipeline network connecting SMR facilities with petroleum refinery and chemical plant consumers represents one of the world's largest industrial gas distribution systems. The U.S. grey hydrogen market benefits from the world's second-largest natural gas reserves, a well-developed natural gas pipeline delivery system that provides reliable low-cost feedstock to hydrogen producers, and the world's largest and most energy-intensive petroleum refinery sector whose hydro processing operations represent the single largest hydrogen consuming application in the American industrial economy.

The American Chemistry Council's 2025 chemical industry production survey confirming that U.S. ammonia plants produced approximately 17.5 million metric tonnes annually, each tonne requiring approximately 177 kilograms of hydrogen feedstock, provides a single-application demand anchor that alone justifies multi-billion-dollar annual hydrogen procurement from domestic SMR producers whose production economics are tightly linked to the natural gas market price that determines their feedstock cost competitiveness.

Grey Hydrogen Market Segment Analysis

-

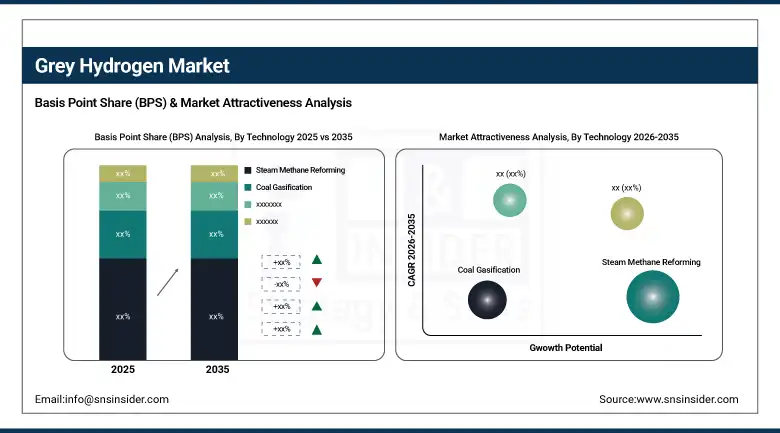

By Technology, steam methane reforming (SMR) dominated with approximately 49% share in 2025 as the most established, widely deployed, and cost-effective hydrogen production process using natural gas feedstock that is widely available in major industrial economies. Coal gasification is expected to grow progressively driven by China and India's abundant coal reserves and existing gasification infrastructure.

-

By Application, chemical applications dominated with approximately 56% in 2025 as hydrogen is extensively used in ammonia production and methanol synthesis serving the world's agricultural and chemical manufacturing industries. Petroleum refinery is the fastest-growing application driven by increasing hydrogen consumption for hydrocracking, desulfurization, and the production of cleaner transportation fuels meeting progressively stringent fuel quality standards.

-

By Transportation Mode, pipeline dominated with approximately 71% share in 2025 as the most cost-effective, safe, and efficient method for transporting large volumes of hydrogen over long distances between production facilities and industrial consumers. Cryogenic liquid tankers are the fastest-growing transportation mode driven by increasing demand for flexible long-distance hydrogen transport to markets without pipeline infrastructure.

By Technology, SMR dominates, coal gasification is fastest-growing

Steam methane reforming retained the dominant technology position with approximately 49% of the grey hydrogen market in 2025, as the chemical process that reacts natural gas with high-temperature steam over a catalyst to produce hydrogen and carbon monoxide, followed by the water-gas shift reaction converting carbon monoxide and water to additional hydrogen and carbon dioxide, remains the most commercially deployed and economically proven hydrogen production route globally. SMR's dominance reflects its well-established process engineering base accumulated over eight decades of commercial operation, the universal availability of natural gas as a feedstock in major industrial economies, and the SMR process's inherent efficiency advantage that produces the highest hydrogen yield per unit of feedstock energy input among commercial fossil fuel hydrogen production routes.

Coal gasification to grow progressively, reflecting China's position as the world's largest coal gasification-based hydrogen producer where the combination of abundant domestic coal reserves, established gasification engineering expertise from decades of industrial coal chemistry investment, and the cost competitiveness of coal relative to natural gas in Chinese markets makes gasification the preferred hydrogen production route for the country's enormous fertilizer and chemical manufacturing sectors.

By Application, chemical dominates, petroleum refinery is fastest-growing

Chemical applications retained the dominant position with approximately 56% of the grey hydrogen market in 2025, with ammonia synthesis through the Haber-Bosch process representing the single largest hydrogen consuming application globally where the combination of nitrogen from air separation and hydrogen from steam methane reforming or coal gasification produces the ammonia that is the precursor for all nitrogen fertilisers that support global agricultural production at its current scale. The Haber-Bosch process consumes approximately 1.4% of total global primary energy and produces approximately 150 million tonnes of ammonia annually, each tonne requiring approximately 177 kilograms of hydrogen whose production from SMR or coal gasification creates the largest single industrial hydrogen demand that is inelastic to hydrogen price fluctuations within the range that agricultural commodity economics support. Methanol synthesis represents the other major chemical hydrogen consumption application where hydrogen and carbon monoxide from SMR or gasification are combined at elevated pressure to produce methanol that serves as a chemical feedstock for formaldehyde, acetic acid, and a growing range of fuel and energy applications including methanol fuel cell applications and methanol-to-olefins chemical production.

Petroleum refinery is the fastest-growing application, reflecting the global petroleum refining sector's increasing hydrogen consumption intensity driven by the processing of heavier, higher-sulphur crude oil grades who’s refining to meet clean fuel specifications requires substantially more hydrogen per barrel of crude processed than the lighter, sweeter crude oils that refineries were originally designed to process. The IMO 2020 sulphur cap's reduction of marine fuel sulphur content to 0.5% has simultaneously increased marine fuel desulphurization hydrogen consumption and redirected high-sulphur fuel oil toward residual upgrading operations that consume additional hydrogen to convert refinery residuals into transportation fuels meeting the global sulphur reduction mandates that are progressively extending from marine fuel to diesel, gasoline, and aviation fuel specifications.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

23.8% |

|

Asia Pacific |

China |

58.3% |

|

Middle East & Africa |

Saudi Arabia |

35.7% |

|

Latin America |

Brazil |

41.6% |

North America Grey Hydrogen Market Insights

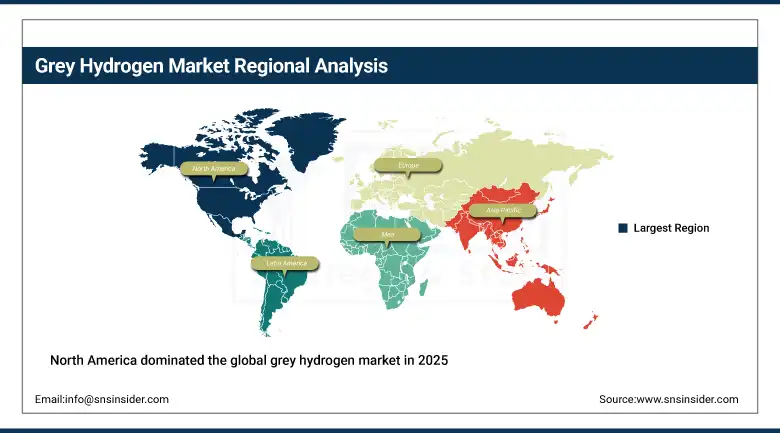

North America dominated the global grey hydrogen market in 2025, with the United States accounting for approximately 87.4% of North American revenues as the world's largest national hydrogen market by both production volume and industrial consumption. The region's market leadership reflects the world's largest petroleum refinery sector concentrated along the Gulf Coast, the most extensive domestic natural gas infrastructure enabling cost-competitive SMR production, and the enormous fertiliser and chemical manufacturing sector whose ammonia and methanol production creates inelastic hydrogen demand. The Gulf Coast hydrogen pipeline network interconnecting SMR producers with refinery and chemical plant consumers across Texas, Louisiana, and the broader Gulf Coast industrial complex represents the world's most developed hydrogen distribution infrastructure outside specific industrial clusters in Europe and Japan.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Grey Hydrogen Market Insights

Europe is a major grey hydrogen consuming region where the enormous demand from petroleum refineries, chemical manufacturing including BASF and Evonik's ammonia and specialty chemical operations, and the steel industry's direct reduction hydrogen requirements create substantial and growing hydrogen procurement. Germany accounts for approximately 23.8% of European grey hydrogen revenues as the EU's largest industrial economy with significant refinery, chemical manufacturing, and emerging steel DRI hydrogen demand. The EU Hydrogen Strategy and REPowerEU programme create both a framework for transitioning grey hydrogen toward blue and green alternatives over the long term and an acknowledgment that fossil-based hydrogen will remain the dominant supply for European industrial applications throughout the transition period.

Asia Pacific Grey Hydrogen Market Insights

Asia Pacific is the fastest-growing grey hydrogen market, driven by China's extraordinary scale as the world's largest hydrogen producer and consumer, India's rapidly expanding refinery and fertilizer hydrogen demand, Japan's industrial hydrogen consumption, and the petrochemical-intensive economies of South Korea and Southeast Asia whose refinery and chemical manufacturing sectors create substantial hydrogen procurement. China accounts for approximately 58.3% of Asia Pacific grey hydrogen revenues through its combination of the world's largest coal gasification-based hydrogen production, enormous ammonia and fertilizer manufacturing capacity serving domestic and export agricultural markets, and rapidly expanding petroleum refining sector whose hydro processing hydrogen demand scales with the country's transport fuel production for 1.4 billion residents.

MEA & Latin America Grey Hydrogen Market Insights

The Middle East and Africa and Latin America are growing grey hydrogen markets where petroleum refining, fertilizer production, and in the Middle East the energy-intensive desalination and petrochemical industries create substantial and growing hydrogen demand. Saudi Arabia leads MEA grey hydrogen revenues at approximately 35.7% of regional revenues through its combination of Saudi Aramco's world-largest petroleum refining operations, SABIC's ammonia and petrochemical production, and the country's downstream industrial development programme that is creating new hydrogen-intensive manufacturing capacity. Brazil leads Latin American revenues at approximately 41.6% through its petroleum refining sector, growing fertilizer production for the country's enormous agricultural export sector, and Petrobras's refinery hydrogen programme.

Market Dynamics

Growth Drivers: Expanding petroleum refinery hydrogen consumption driven by clean fuel standards

The primary structural growth drivers for the grey hydrogen market are the expanding petroleum refinery hydrogen consumption driven by progressive global implementation of cleaner transportation fuel standards that require deeper desulfurization and molecular restructuring of crude oil fractions, combined with the fundamental inelasticity of global agricultural fertilizer hydrogen demand whose scale is determined by population growth and dietary improvement trajectories that create an inexorable demand growth baseline for ammonia synthesis hydrogen that is indifferent to hydrogen production carbon intensity. The emergence of hydrogen as a reducing agent in steel manufacturing through the direct reduction iron route is creating a new large-scale industrial hydrogen consumption application that adds to chemical and refinery demand without substituting for it, expanding the total industrial hydrogen market.

Restraints: Carbon price mechanisms and clean hydrogen incentives progressively improving the economics of blue and green hydrogen alternatives that will capture incremental demand growth as their cost disadvantages narrow

A significant restraint on the grey hydrogen market is the progressive improvement in the economics of lower-carbon hydrogen alternatives that are being accelerated by carbon pricing mechanisms in the EU, UK, and Canada, the IRA's clean hydrogen production tax credit in the United States, and the proliferating national green and blue hydrogen strategies whose subsidies are intended to create cost parity with grey hydrogen for industrial consumers who can demonstrate clean hydrogen utilization. Electrolyze cost reduction trajectories supported by manufacturing scale and technology improvement suggest that green hydrogen from renewable electricity will approach SMR grey hydrogen cost parity in high renewable energy resource regions within the 2030 to 2035 timeframe, creating a future competitive pressure on grey hydrogen demand in the refinery and chemical applications that are largest currently.

Opportunities: Carbon capture retrofit of existing SMR facilities converting grey to blue hydrogen, SMR capacity expansion in energy security-motivated markets

The carbon capture retrofit opportunity for existing steam methane reforming facilities represents the most immediately commercial pathway to reducing the hydrogen economy's carbon intensity without requiring the fundamental technology change and infrastructure development that green hydrogen requires, as post-combustion and pre-combustion carbon capture systems can be integrated with existing SMR facilities to capture 50 to 95% of CO2 emissions at costs that are substantially lower than equivalent green hydrogen production at current electrolyze prices.

Recent Developments:

-

2025: Air Products completed expansion of its SMR-based hydrogen production and pipeline distribution network in the U.S. Gulf Coast region, adding incremental SMR capacity serving growing petroleum refinery hydrogen demand from refineries undertaking capacity expansion and hydro processing unit upgrades to meet stricter clean fuel specifications.

-

2025: Linde plc announced a major SMR hydrogen production capacity addition in the United States, designed to serve industrial gas customers in the Gulf Coast chemical and refinery corridor, with the facility incorporating provisions for future carbon capture retrofit that would enable transition to blue hydrogen status as carbon pricing economics improve.

-

2025: CF Industries expanded its ammonia production capacity at its Donaldsonville, Louisiana facility incorporating a new SMR hydrogen unit designed specifically to support the Plant's ammonia synthesis capacity expansion, reflecting the sustained growth in nitrogen fertilizer demand that sustains the largest single grey hydrogen application category globally.

Grey Hydrogen Market Key Players are:

-

Air Products and Chemicals Inc.

-

Linde plc

-

Air Liquide S.A.

-

Messer Group GmbH

-

Iwatani Corporation

-

Taiyo Nippon Sanso Corporation

-

Matheson Tri-Gas Inc.

-

Shell plc

-

BP plc

-

ExxonMobil Corporation

-

Chevron Corporation

-

TotalEnergies SE

-

Saudi Aramco

-

SABIC (Saudi Basic Industries Corporation)

-

Sinopec Group

-

PetroChina Company Limited

-

PJSC Gazprom

-

Equinor ASA

-

CF Industries Holdings Inc.

-

Yara International ASA

Grey Hydrogen Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 327.70 Billion |

| Market Size by 2035 | USD 818.00 Billion |

| CAGR | CAGR of 9.26% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Technology (Steam Methane Reforming, Coal Gasification, Partial Oxidation of Oil, Others) •By Application (Chemical, Petroleum Refinery, Transportation, Power Generation, Others) •By Transportation Mode (Pipeline, Cryogenic Liquid Tankers, Tube Trailers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Air Products and Chemicals Inc., Linde plc, Air Liquide S.A., Messer Group GmbH, Iwatani Corporation, Taiyo Nippon Sanso Corporation, Matheson Tri-Gas Inc., Shell plc, BP plc, ExxonMobil Corporation, Chevron Corporation, TotalEnergies SE, Saudi Aramco, SABIC (Saudi Basic Industries Corporation), Sinopec Group, PetroChina Company Limited, PJSC Gazprom, Equinor ASA, CF Industries Holdings Inc., Yara International ASA |

Frequently Asked Questions

North America dominated the grey hydrogen market in 2025.

Steam Methane Reforming dominated with approximately 49% of revenues in 2025.

Expanding petroleum refinery hydrogen consumption driven by progressively stringent clean fuel standards.

The grey hydrogen market was valued at USD 327.70 billion in 2025.

The grey hydrogen market is expected to grow at a CAGR of 9.26% from 2026 to 2035.

Get in Touch