Harmonic Filter Market Report Scope & Overview:

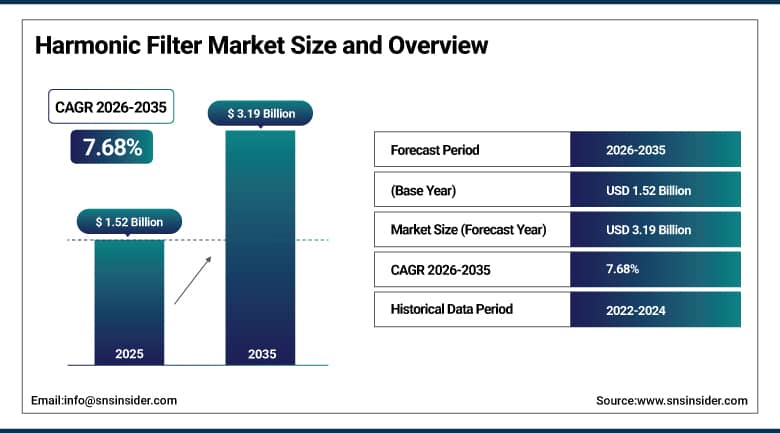

Harmonic Filter Market was valued at USD 1.52 billion in 2025 and is expected to reach USD 3.19 billion by 2035, growing at a CAGR of 7.68% from 2026-2035.

There are several factors fueling the growth of the Harmonic Filter Market, including increased industrial automation, rising penetration of VFDs, and rising renewable energy generation which creates harmonics in electricity. Besides, stringent power quality standards, rising demand for energy efficiency, and rapid growth of data centers, EV charging stations, and smart factories are also driving market growth.

The International Electrotechnical Commission's IEC 61000-3-2 and IEC 61000-3-12 standards perform the equivalent function in European and international markets, creating compliance-driven harmonic filter procurement wherever their requirements are enforced.

Harmonic Filter Market Size and Forecast

-

Market Size in 2025: USD 1.52 Billion

-

Market Size by 2035: USD 3.19 Billion

-

CAGR: 7.68% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Harmonic Filter Market - Request Free Sample Report

Harmonic Filter Market Trends

-

Data center harmonic mitigation is becoming a major harmonic filter demand driver as hyperscale data center construction adds millions of kilowatts of IT power supply load each power supply a non-linear load to utility distribution systems whose harmonic injection concentrations exceed IEEE 519 and EN 61000 limits at data center utility interconnect points.

-

EV charging infrastructure harmonic management is emerging as a growing application as high-power DC fast chargers whose switch-mode power supplies create significant harmonic injection at 25-350 kW per charger are deployed in concentrations at charging plazas whose aggregate harmonic impact requires active harmonic filter mitigation.

-

Active harmonic filter adoption is growing relative to passive filter market share as active filters' adaptive compensation capability adjusting compensation in real time as load characteristics change provides superior performance in industrial environments whose load profiles vary continuously with production scheduling.

-

Renewable energy integration harmonic management where photovoltaic inverters, wind turbine converters, and battery storage inverters inject harmonics at solar farms and wind parks is creating utility-scale harmonic mitigation requirements that medium voltage harmonic filter procurement addresses.

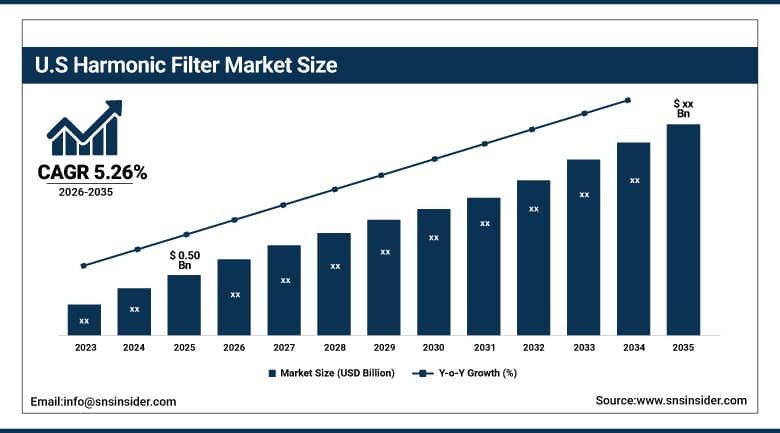

U.S. Harmonic Filter Market was valued at USD 0.50 billion in 2025 and is expected to grow at a CAGR of 5.26% from 2026-2035.

Drivers for the U.S. Harmonic Filter Market include the growth of automation in industries, the development of renewable energy, and more investments in data centers and EV charging stations. In addition, stringent power quality requirements, upgrade of old electrical grids, and more use of VFDs will also contribute to market expansion.

ABB's Power Quality division reports that data center harmonic mitigation contracts grew 45% in the most recently reported period as hyperscale cloud operators address the harmonic compliance requirements of their utility interconnect agreements.

Harmonic Filter Market Segment Analysis

-

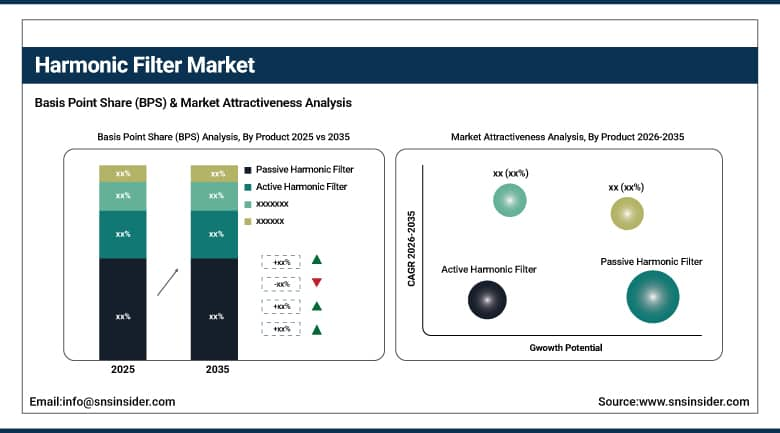

By Product, Passive Harmonic Filters dominated the market in 2025; Active and Hybrid growing at fastest CAGR driven by dynamic load environments.

-

By Voltage Level, Low Voltage dominated in 2025; Medium Voltage growing at fastest CAGR.

-

By End Use, Oil & Gas and Automotive significant; Semiconductor fastest growing.

By Product: Passive dominant, Active/Hybrid fastest CAGR

Passive Harmonic Filters held the dominant product position in the Harmonic Filter Market in 2025, reflecting their cost advantage where passive LC filter banks providing harmonic current diversion paths cost 30-50% less per kVA than active harmonic filters and their established track record in the bulk of industrial harmonic mitigation applications where load characteristics are relatively stable. Passive filters tuned to specific harmonic frequencies 5th, 7th, 11th are effective in applications with predictable harmonic spectra, including fixed-speed motor drives and constant-load switching power supplies. Active Harmonic Filters are growing at the fastest CAGR, driven by their superior performance in dynamic industrial environments where loads vary continuously and harmonic injection changes proportionally, requiring real-time compensation adjustment that passive filter fixed tuning cannot provide. Active harmonic filters' ability to compensate harmonics through the 50th order simultaneously not just specific tuned frequencies provides comprehensive mitigation in complex industrial environments whose harmonic spectra extend beyond the frequencies addressed by practical passive filter topologies.

By Voltage Level: Low Voltage dominant, Medium Voltage fastest CAGR

In the year 2025, Oil & Gas and Automotive were among the notable end-use sectors in the Harmonic Filter market due to their extensive use of variable frequency drives, high-power industrial machinery, automated systems, and high-power electrical equipment leading to the production of large amounts of harmonic distortions in electrical networks. The oil & gas sector needs harmonic filters to keep their drilling, refining, and pipeline operations stable, whereas, in the automotive sector, robotic technology and assembly line operations demand stability in power supply. The Semiconductors sector is the most rapidly growing one in terms of usage of harmonic filters due to the establishment of numerous semiconductor fabrication plants along with increased automation and power stability requirements.

Harmonic Filter Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

88% |

|

Europe |

Germany |

27% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

Saudi Arabia |

40% |

|

Latin America |

Brazil |

48% |

North America Harmonic Filter Market Insights

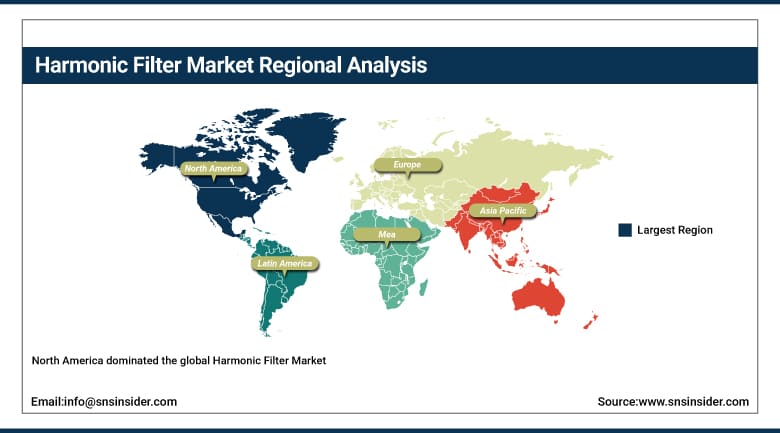

North America dominated the global Harmonic Filter Market, driven by IEEE 519-2022 enforcement, data center construction, and industrial automation expansion. The U.S. market's commercial sophistication extends to utility-side harmonic filter procurement — where utilities install harmonic filter banks at distribution substations serving industrial areas with high harmonic injection — whose scale and regulatory backing creates significant filter procurement volume beyond individual facility-level mitigation.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Harmonic Filter Market Insights

Europe's Harmonic Filter Market is growing with the EU's rigorous IEC 61000 series enforcement implemented through CE marking requirements that mandate power quality compliance for electrical equipment placed on the European market and the energy efficiency imperative that drives harmonic loss reduction as part of industrial energy management programs. Germany's large industrial base and the European Union's energy transition whose renewable energy systems and heat pumps create additional non-linear loads across residential and commercial buildings sustain consistent harmonic filter demand growth.

Asia Pacific Harmonic Filter Market Insights

Asia Pacific is the fastest-growing regional Harmonic Filter Market, driven by China's massive industrial automation expansion whose motor drive installations across manufacturing create the primary harmonic injection that requires mitigation India's growing industrial electrical infrastructure, and the region's rapidly expanding semiconductor manufacturing whose clean power requirements demand sophisticated harmonic management. China's domestic harmonic filter manufacturers including Sieyuan Electric and Kehua Tech compete with international brands across the middle and low-end market segments whose price sensitivity sustains domestic brand adoption.

MEA and Latin America Harmonic Filter Market Insights

The Middle East's Harmonic Filter Market is growing with the Gulf states' industrial expansion where petrochemical facilities, desalination plants, and data centers create harmonic injection that utility power quality requirements mandate mitigation and the region's ambitious renewable energy projects whose inverter-based generation requires grid harmonic management. Latin America's market concentrates in Brazil's industrial and utilities sectors and Mexico's manufacturing corridor.

Harmonic Filter Market Growth Drivers:

-

Industrial automation proliferation and power quality regulations driving sustained harmonic filter market growth globally

The Harmonic Filter Market's 7.68% CAGR is driven by the structural growth in non-linear electrical load density where the electrification of industrial drives, commercial HVAC, data center IT equipment, and transportation creates compounding harmonic injection that power quality regulations increasingly require mitigation for and the parallel tightening of those regulations as utilities install the power quality monitoring infrastructure that enables compliance measurement and enforcement. The data center buildout wave driven by cloud computing, AI training infrastructure, and streaming media is creating concentrated harmonic injection at utility interconnect points whose scale requires active harmonic filter installation as a condition of utility interconnection agreements.

Harmonic Filter Market Restraints:

-

High installation costs and technical complexity creating harmonic filter market adoption challenges in cost-sensitive markets

Harmonic filter procurement is constrained by the electrical engineering expertise required for accurate harmonic assessment and filter specification where incorrect filter sizing or tuning creates resonance conditions more damaging than the original harmonic problem that sustains dependence on specialist power quality consultants whose availability creates bottlenecks in small and medium enterprise harmonic mitigation programs. The capital cost of complete harmonic mitigation where active harmonic filters for medium-voltage applications represent USD 100,000-500,000 per installation creates budget barriers for smaller industrial operators whose harmonic problems are real but whose capital commitment capacity is limited.

Harmonic Filter Market Opportunities:

-

EV charging infrastructure harmonic management and data center power quality creating significant harmonic filter market growth globally

EV charging infrastructure represents the harmonic filter market's highest-volume emerging application opportunity where the planned deployment of hundreds of thousands of 50-350 kW DC fast chargers creates concentrated harmonic injection whose utility grid impact requires active harmonic compensation at charging plaza level. As EV charging site developers negotiate utility interconnection for large charging depots whose aggregate power demand approaches 10-50 MW, utility power quality requirements for harmonic injection at the point of common coupling will systematically require harmonic filter installation as an interconnection condition creating mandatory procurement rather than optional mitigation investment.

Recent Developments:

-

2026: ABB launched its PCS100 AHF+ Active Harmonic Filter achieving 600A compensation current capacity in a compact cabinet format with AI-powered harmonic prediction that anticipates load changes from production schedule data 15 minutes ahead enabling proactive harmonic compensation that eliminates the response latency of reactive compensation systems, reporting 99.97% power quality compliance achievement at semiconductor fab installations where even momentary harmonic exceedances trigger equipment shutdown interlocks.

-

2025: Schneider Electric launched EasyPact PowerVar HF-DC a harmonic filter specifically designed for DC fast EV charging station installations, providing active compensation for the non-characteristic harmonics generated by modern high-power SiC-based charger power electronics receiving UL 1082 certification for EV charging station power quality equipment and achieving deployment at 50 major U.S. highway charging corridor sites whose utility interconnection agreements require IEEE 519-2022 compliance at 5% total harmonic voltage distortion.

Harmonic Filter Market Key Players

Some of the Harmonic Filter Market Companies

-

ABB Ltd.

-

Schneider Electric SE

-

Eaton Corporation plc

-

Siemens AG

-

Emerson Electric Co.

-

Danfoss A/S

-

Comsys AB

-

TDK-Lambda Corporation

-

Schaffner Holding AG

-

MTE Corporation

-

Sinexcel Power Co. Ltd.

-

Sieyuan Electric Co. Ltd.

-

Delta Electronics Inc.

-

Honeywell International Inc.

-

General Electric Company

-

Rockwell Automation Inc.

-

Yaskawa Electric Corporation

-

Kehua Tech Co. Ltd.

-

Mirus International Inc.

-

REFUsol GmbH

Harmonic Filter Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.52 Billion |

| Market Size by 2035 | USD 3.19 Billion |

| CAGR | CAGR of 7.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Passive Harmonic Filter, Active Harmonic Filter, Hybrid Harmonic Filter) • By Voltage Level (Low Voltage, Medium Voltage, High Voltage) • By End Use (Oil & Gas, Automotive, Food & Beverage, Chemical Processing, Semiconductor, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd.; Schneider Electric SE; Eaton Corporation plc; Siemens AG; Emerson Electric Co.; Danfoss A/S; Comsys AB; TDK-Lambda Corporation; Schaffner Holding AG; MTE Corporation; Sinexcel Power Co. Ltd.; Sieyuan Electric Co. Ltd.; Delta Electronics Inc.; Honeywell International Inc.; General Electric Company; Rockwell Automation Inc.; Yaskawa Electric Corporation; Kehua Tech Co. Ltd.; Mirus International Inc.; REFUsol GmbH. |

Frequently Asked Questions

The Harmonic Filter Market was valued at USD 1.52 billion in 2025.

North America dominated; Asia Pacific is the fastest growing regional market.

Medium Voltage is growing fastest; Low Voltage dominated in 2025.

Passive Harmonic Filters dominated; Active and Hybrid growing at the fastest CAGR.

The Harmonic Filter Market is expected to grow at a CAGR of 7.68% from 2026 to 2035.

Get in Touch