Power Quality Equipment Market Report Scope & Overview:

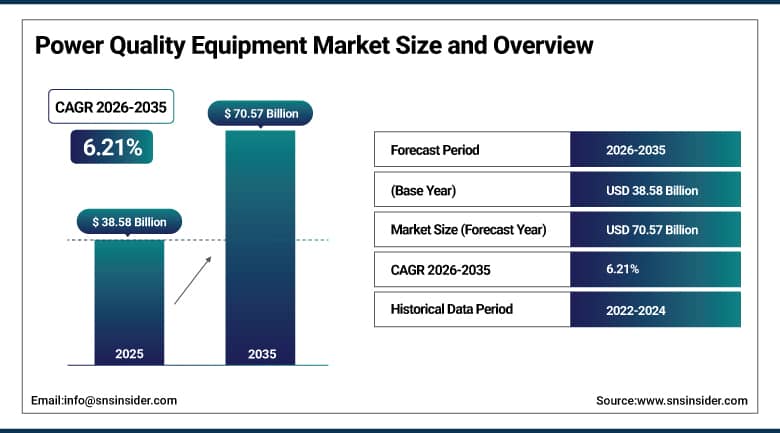

The Power Quality Equipment Market was valued at USD 38.58 Billion in 2025 and is expected to reach USD 70.57 Billion by 2035, growing at a CAGR of 6.21% from 2026–2035.

The global power quality equipment market is growing at a sustained and commercially broad-based pace. Power quality equipment encompasses voltage regulators, surge protection devices, harmonic filters, uninterruptible power supplies, and power conditioning systems that protect electrical infrastructure from disturbances including voltage sags, swells, harmonics, transients, and interruptions. The market is driven by the transition toward digital infrastructure and smart grid systems, increasing adoption of automation and digital control technologies, and the growing reliance on clean and stable power supply in data centres, manufacturing facilities, and utilities. Rising investments in grid modernisation and energy-efficient technologies are reinforcing market growth, while renewable energy integration’s variable generation creates new power quality challenges that demand advanced equipment solutions.

In 2024, Eaton Corporation launched its 9PX lithium-ion UPS series with enhanced runtime extension modules and predictive diagnostics, targeting data centre and critical facility operators seeking higher energy density, reduced footprint, and IoT-enabled battery health monitoring. The launch reflects the commercial direction of UPS product development toward intelligent energy storage management whose lithium-ion battery chemistry creates superior lifecycle economics relative to conventional VRLA battery alternatives while enabling the remote monitoring capability that modern facility management requires.

Market Size and Forecast

-

Market Size in 2026E: USD 40.98 Billion

-

Market Size by 2035: USD 70.57 Billion

-

CAGR: 6.21% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Power Quality Equipment Market - Request Free Sample Report

Power Quality Equipment Market Trends

-

Data centre power quality investments are increasing as hyperscale and colocation facilities require highly reliable electrical infrastructure.

-

Adoption of lithium-ion UPS systems is accelerating due to their higher energy density, longer lifespan, and reduced maintenance requirements.

-

Renewable energy integration is creating new power quality challenges across electrical grids. Inverter-based solar and wind generation can introduce harmonics and voltage fluctuations, driving demand for mitigation solutions.

-

Smart power quality monitoring technologies are enabling real-time diagnostics and predictive maintenance. These capabilities help improve equipment reliability, reduce downtime, and optimize operational performance.

-

Expansion of EV charging infrastructure is increasing the need for power quality management solutions.

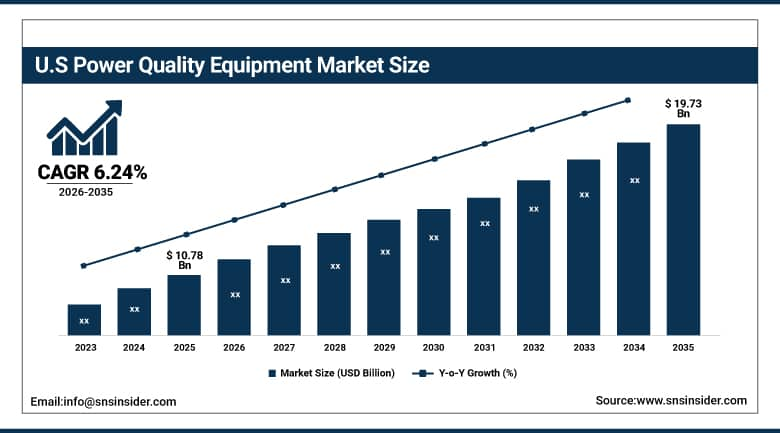

U.S. Power Quality Equipment Market Outlook:

The U.S. Power Quality Equipment Market was valued at approximately USD 10.78 Billion in 2025 and is expected to reach approximately USD 19.73 Billion by 2035, growing at a CAGR of approximately 6.24%.

The U.S. is the world’s most commercially sophisticated power quality equipment market within North America’s dominant revenue position. Eaton, Emerson Electric, Schneider Electric’s U.S. operations, and ABB’s commercial presence define the domestic power quality equipment commercial landscape. The data centre sector’s extraordinary capital investment creates above-average UPS and power conditioning procurement. Manufacturing sector’s Industry 4.0 adoption, the utility sector’s grid modernisation investment under the Bipartisan Infrastructure Law, and the commercial building sector’s digital control system adoption collectively sustain consistent power quality equipment demand across multiple end-user categories.

Schneider Electric launched its Galaxy VX UPS system for large data centres and industrial applications in 2024, featuring modular design for scalability up to 1.5 MW per frame, 99% efficiency in ECO mode, and integrated EcoStruxure monitoring connectivity. The system targets the hyperscale data centre market whose power capacity requirements and efficiency mandates create premium UPS specification whose per-installation commercial value sustains above-average market revenue contribution per project.

Power Quality Equipment Market Segment Analysis

-

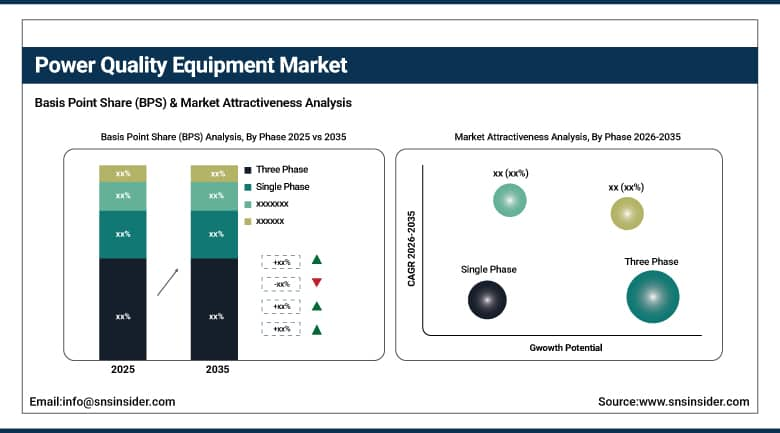

By Phase, the Three Phase segment dominated the Power Quality Equipment Market with approximately 72.50% share in 2025, while the Single Phase segment is the fastest growing.

-

By Equipment Type, the UPS segment dominated the Power Quality Equipment Market with approximately 34.80% share in 2025, while the Harmonic Filters segment is the fastest growing.

-

By End User, the Industrial & Manufacturing segment dominated the Power Quality Equipment Market with approximately 46.00% share in 2025, while the Data Centres segment is the fastest growing.

By Phase, three phase dominates, single phase grows fastest

Three phase retained the dominant phase position in the power quality equipment market in 2025. Three-phase power quality equipment serves the majority of market revenue because the industrial, utility, data centre, and large commercial applications that constitute the highest-value end-user segments universally operate on three-phase electrical infrastructure whose power quality equipment specification creates above-average per-installation commercial value. Industrial UPS systems, three-phase harmonic filters for variable frequency drive installations, and three-phase voltage regulators for critical manufacturing processes each represent equipment categories whose individual system commercial value substantially exceeds equivalent single-phase alternatives.

Single-phase power quality equipment is the fastest-growing segment because the convergence of residential electrification, EV home charging infrastructure, smart home control system adoption, and small commercial and telecommunications application growth is creating expanding demand for compact single-phase UPS, surge protectors, and voltage regulators. Each new EV home charger installation creates a single-phase power quality requirement whose grid connection quality impact motivates utility-grade surge protection investment. Each new data centre edge node and telecommunications base station creates single-phase UPS procurement that compounds with the distributed digital infrastructure’s geographic expansion.

By Equipment Type, UPS dominates, harmonic filters grow fastest

UPS systems retained the dominant equipment type position in the power quality equipment market in 2025. The UPS market’s commercial leadership reflects the equipment’s non-discretionary status in critical facility power protection whose failure creates immediate operational, financial, and safety consequences that no facility operator can accept. Data centres whose entire revenue depends on continuous computing availability, hospitals whose life-safety systems require uninterrupted power, and telecommunications infrastructure whose service continuity creates regulatory obligations collectively create UPS procurement whose non-discretionary character sustains demand through economic cycle variation. The AI infrastructure build-out’s extraordinary data centre power capacity growth is creating the most commercially significant UPS procurement wave in the market’s history.

Harmonic filters are the fastest-growing equipment type because the proliferation of non-linear electrical loads across industrial, commercial, and grid-connected renewable energy applications is creating harmonic distortion levels that standard electrical infrastructure cannot tolerate without active mitigation. Each new variable frequency drive installation creates harmonic injection whose management requires filter investment. Each new solar and wind energy inverter grid connection creates harmonic content that accumulates with renewable energy penetration. Each new EV charging station creates harmonic disturbance that compounds with charging infrastructure density growth, creating systematic harmonic filter procurement that grows proportionally with electrification investment.

By End User, industrial dominates, data centres grow fastest

Industrial and manufacturing retained the dominant end-user position with approximately 46% of the power quality equipment market in 2025. The manufacturing sector’s adoption of automation, robotics, and precision process control creates sensitive electronic infrastructure whose power quality requirements are the most demanding of any commercial end-user category. CNC machining centres, semiconductor fabrication equipment, pharmaceutical manufacturing clean rooms, and food processing automation each require power quality specifications whose violation creates product quality failures, equipment damage, or safety events that motivate premium power quality equipment specification. Each new smart factory investment creates power quality equipment procurement whose intelligent specification creates above-average per-facility commercial value.

Data centres are the fastest-growing end-user at approximately 9.2% CAGR because the AI infrastructure investment wave’s extraordinary data centre construction pace is creating power quality equipment procurement that is growing faster than any other end-user category. Each new hyperscale GPU cluster campus requires UPS infrastructure covering millions of watts of computing load, harmonic filters for the power conversion equipment, and voltage regulation for the precision power requirements of high-density server racks. The commercial scale of this procurement compounding with the extraordinary pace of data centre construction creates data centre power quality equipment demand growth that substantially exceeds any other end-user category.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

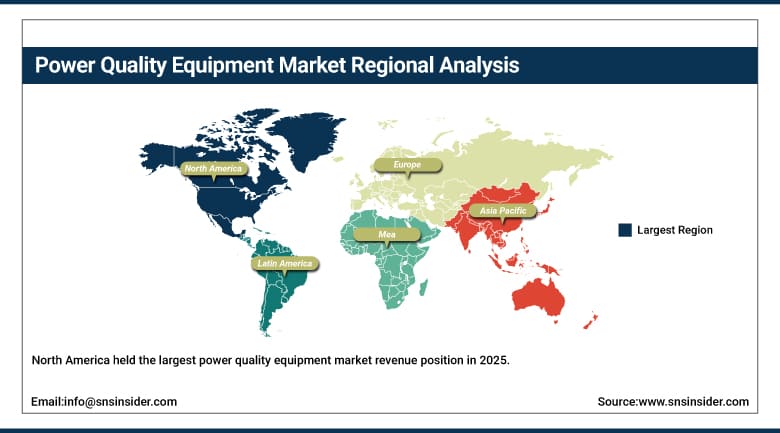

North America Power Quality Equipment Market Insights

North America held the largest power quality equipment market revenue position in 2025, supported by stringent regulatory frameworks focusing on power efficiency and reliability, early adoption of advanced technologies, and established energy infrastructure. The United States accounts for approximately 87.4% of North American revenues through Eaton, Emerson Electric, and Schneider Electric’s commercial dominance whose combined portfolio defines the domestic power quality equipment standard. Data centre concentration in Northern Virginia, Phoenix, and Dallas creates geographically concentrated UPS and power conditioning procurement whose commercial scale sustains above-average North American market density.

Canada contributes approximately 12.6% of North American revenues through its manufacturing sector’s automation investment, utility sector’s grid modernisation, and the growing data centre sector’s power quality infrastructure procurement.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Power Quality Equipment Market Insights

Europe is a technically sophisticated power quality equipment market where EU energy efficiency directives, stringent power quality standards, and the manufacturing sector’s above-average automation investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its industrial automation leadership, the data centre sector’s Frankfurt concentration, and Siemens’ domestic market presence.

The United Kingdom, France, and Scandinavia are significant secondary markets where data centre investment, manufacturing automation, and utility grid modernisation create consistent procurement. ABB’s Swiss headquarters and Schneider Electric’s French operations sustain European power quality equipment supply from established regional commercial presences.

Asia Pacific Power Quality Equipment Market Insights

Asia Pacific is the fastest-growing regional power quality equipment market, driven by rapid industrialisation in China, India, and Southeast Asia, expanding power infrastructure in emerging economies, and increasing renewable energy installations whose grid integration creates new power quality management requirements. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary manufacturing scale, data centre investment, and government grid modernisation investment whose combined power quality equipment demand creates the largest regional volume procurement globally.

India and Southeast Asia are the most commercially dynamic emerging markets where manufacturing sector growth, data centre expansion, and utility infrastructure investment are creating above-average first-time power quality equipment adoption whose structural growth compounds with the regions’ industrial development pace.

MEA & Latin America Power Quality Equipment Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through ARAMCO’s industrial power quality investment, the data centre sector’s commercial infrastructure development, and Vision 2030’s manufacturing development. Brazil leads Latin American revenues at approximately 44.2% through its manufacturing sector’s automation investment, the utility sector’s power grid reliability programme, and the data centre market’s growing infrastructure investment.

The UAE’s data centre expansion, South Africa’s industrial power quality investment, and Colombia’s manufacturing sector development collectively represent growing MEA and Latin American power quality equipment procurement that sustains regional market growth.

Market Dynamics:

Growth Drivers: Data centre AI infrastructure and industrial automation creating systematic power quality investment

Data centre AI infrastructure investment is the power quality equipment market’s most commercially dynamic near-term growth driver. Each GPU cluster commissioned creates UPS, power conditioning, and harmonic filter procurement whose scale compounds with the extraordinary pace of hyperscale data centre construction. AWS, Microsoft, Google, and Meta’s combined data centre capital investment programmes of over USD 200 billion for 2024-2026 create proportional power quality equipment demand whose per-megawatt power protection investment creates commercial opportunity that sustains above-average market growth.

Industrial automation’s systematic adoption of robots, CNC machines, and precision process control creates sensitive electronic infrastructure whose power quality requirements create non-discretionary power quality equipment procurement. Each new automated production facility creates structured power quality investment whose intelligent specification grows with the automation investment’s sophistication level. Industry 4.0’s real-time production data systems, whose momentary power quality disturbances can cause data loss and process interruption, creates above-average motivation for premium power quality equipment specification.

Restraints: High capital cost of premium UPS systems and harmonic filter installation complexity

Premium three-phase UPS systems for large data centre and industrial critical facility applications represent substantial capital investments whose payback period analysis must demonstrate operational continuity value that justifies above-standard equipment specification. Budget-constrained procurement environments including small manufacturing operations, commercial buildings, and residential applications create resistance to premium power quality equipment specification where lower-cost protection alternatives provide perceived adequate protection.

Harmonic filter system integration complexity in existing industrial electrical infrastructure creates implementation challenges whose engineering cost and installation downtime requirement create adoption barriers in facilities where production continuity prevents maintenance window access for filter installation. Each harmonic filter installation requires electrical system characterisation, filter specification, and integration commissioning whose combined engineering cost adds to the capital equipment investment.

Opportunities: Lithium-ion UPS lifecycle economics and EV charging infrastructure power quality management

Lithium-ion UPS adoption represents the most commercially transformative product technology transition in the power quality equipment market. Li-ion’s smaller footprint, longer cycle life of 10+ years versus VRLA’s 3-5 years, higher energy density, and lower total cost of ownership over the equipment lifetime create economic advantages that are progressively winning data centre and industrial procurement specifications as the technology matures and price premiums decline toward VRLA alternatives.

EV charging infrastructure power quality management represents a growing commercial opportunity whose scale compounds with EV adoption’s global momentum. Each high-power EV charging hub creates voltage regulation, harmonic mitigation, and surge protection requirements at the grid connection point whose commercial value per installation grows with charging power level. Utility-scale EV fleet charging at logistics hubs, bus depots, and commercial vehicle facilities creates power quality equipment procurement whose aggregate grows with commercial vehicle electrification.

Recent Developments:

-

2024: Eaton Corporation launched its 9PX lithium-ion UPS series with enhanced runtime extension modules and predictive diagnostics in 2024, targeting data centre and critical facility operators with higher energy density, reduced footprint, and IoT-enabled battery health monitoring.

-

2024: Schneider Electric launched its Galaxy VX UPS system for large data centres in 2024, featuring modular design scalable to 1.5 MW per frame, 99% efficiency in ECO mode, and integrated EcoStruxure monitoring connectivity.

-

2024: ABB launched its PCS100 active voltage conditioner with enhanced harmonic compensation capability in 2024, targeting industrial and commercial facilities requiring protection against voltage dips, swells, and harmonic distortion in renewable energy-integrated grid environments.

Power Quality Equipment Market Key Players:

-

Eaton Corporation

-

Emerson Electric Co.

-

Schneider Electric

-

ABB Ltd.

-

Siemens AG

-

General Electric (GE Vernova)

-

Mitsubishi Electric

-

Legrand S.A.

-

Vertiv Group Corp.

-

Socomec Group

-

Huawei Technologies

-

Delta Electronics

-

AMETEK Inc.

-

Tripp Lite (Eaton)

-

CyberPower Systems

-

Piller Power Systems

-

Active Power (Piller)

-

Toshiba International

-

Riello Elettronica

-

Controlled Power Company

Power Quality Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 38.58 Billion |

| Market Size by 2035 | USD 70.57 Billion |

| CAGR | CAGR of 6.21% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Equipment Type (UPS/Uninterruptible Power Supplies, Harmonic Filters, Voltage Regulators, Surge Protection Devices, Power Conditioners, Others) • by Phase (Three Phase, Single Phase) • by End User (Industrial & Manufacturing, Commercial, Data Centres, Utilities/T&D, Residential, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Eaton Corporation, Emerson Electric Co., Schneider Electric, ABB Ltd., Siemens AG, General Electric (GE Vernova), Mitsubishi Electric, Legrand S.A., Vertiv Group Corp., Socomec Group, Huawei Technologies, Delta Electronics, AMETEK Inc., Tripp Lite (Eaton), CyberPower Systems Piller Power Systems, Active Power (Piller), Toshiba International, Riello Elettronica, Controlled Power Company |

Frequently Asked Questions

The Power Quality Equipment Market is expected to grow at a CAGR of 6.21% from 2026 to 2035.

The Power Quality Equipment Market was valued at USD 38.58 Billion in 2025.

Data centre AI infrastructure investment creating extraordinary UPS and power conditioning procurement, and industrial automation adoption creating sensitive electronic infrastructure whose power quality requirements drive non-discretionary equipment investment across manufacturing facilities.

Industrial & Manufacturing dominated the Power Quality Equipment Market with approximately 46% share in 2025, while Data Centres is the fastest growing with a CAGR of approximately 9.2%.

North America held the largest power quality equipment market revenue position in 2025, while Asia Pacific is the fastest-growing region.

Get in Touch