Healthcare Architecture Market Report Scope & Overview:

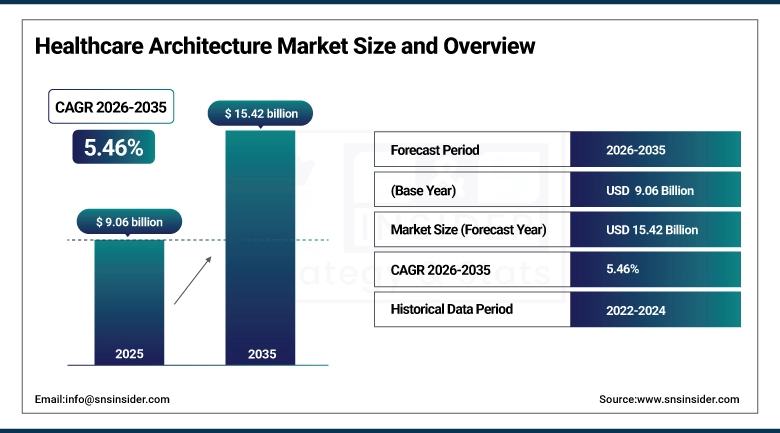

The Healthcare Architecture Market was estimated at USD 9.06 billion in 2025 and is expected to reach USD 15.42 billion by 2035 and grow at a CAGR of 5.46% over the forecast period of 2026-2035.

The global healthcare architecture market is at a pivotal inflection point, as healthcare systems worldwide simultaneously grapple with the imperative to replace ageing infrastructure-built decades ago, accommodate the rapid proliferation of new medical technologies that require purpose-designed spaces, and fundamentally rethink the patient experience through evidence-based design principles that demonstrably improve clinical outcomes and operational efficiency. Healthcare architecture encompasses the comprehensive design and construction of hospitals, ambulatory surgical centres, medical diagnostic facilities, rehabilitation centres, and long-term care institutions, with specialised expertise in infection control, patient flow optimisation, medical gas and power distribution, radiation shielding, and the complex functional relationships between clinical departments that define effective healthcare delivery. The global ageing population is creating an intensifying demand for new and expanded healthcare infrastructure across all major economies, while urbanisation is concentrating populations in cities where new tertiary hospitals and specialist medical centres are required to serve growing patient catchment areas. Investment in healthcare architecture is being simultaneously driven by public sector hospital modernisation programmes and private sector healthcare group expansion into ambulatory and specialty care formats that offer more cost-effective care delivery alternatives to traditional inpatient hospitalisations.

The integration of health information technology into the design process of health buildings like teleconsultation rooms, imaging technology, electronic health record systems, and building automation technology for infection control and energy management has brought about the emergence of a new kind of healthcare building that operates intelligently. For example, HOK, in June 2023, constructed a 264-bed hospital facility with a total investment of USD 920 million in Michigan, while in the same month, CannonDesign delivered an extended emergency department project for the University of Chicago. This extension added 41,000 sq ft of operational capacity, showcasing the level of health architecture projects in development in North American health systems, which are expected to grow at a CAGR of 5.46% between 2026 and 2035.

Market Size and Forecast

-

Market Size in 2025: USD 9.06 Billion

-

Market Size by 2035: USD 15.42 Billion

-

CAGR: 5.46% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Healthcare Architecture Market - Request Free Sample Report

Healthcare Architecture Market Trends

-

The increasing application of modular and prefabricated construction techniques in healthcare building development, providing an advantage of accelerated timelines, improved quality control, less disruption of operations during construction, and lower costs compared to conventional on-site construction techniques.

-

The growing incorporation of evidence-based design (EBD) concepts in hospitals, whereby spatial planning, natural lighting, acoustics, wayfinding, and design of patient rooms are based on clinical research data showing their positive impact on recovery rates, well-being of the healthcare professionals, and infection levels.

-

The increased popularity of sustainable healthcare buildings owing to net-zero goals of many healthcare systems, LEED and WELL standards, and the cost benefits that accrue from the efficient operation of the building over time due to its constant operation day and night.

-

Increasing demand for versatile design of healthcare facilities that can be easily converted to meet changes in clinical programmes, technologies, and surge capacity needs during public health emergencies, which includes the ability to easily convert spaces into patient rooms and other medical facilities.

-

Increasing focus on designing ambulatory healthcare facilities, as healthcare organizations move away from expensive hospital-based care toward affordable ambulatory surgery centres, urgent care centres, and specialty outpatients clinics that provide better patient experience at reduced cost.

-

Increased incorporation of biophilia in healthcare facility design in the use of natural materials, incorporation of natural scenery, natural light optimization, and gardens for healing purposes, as studies show that biophilic design helps to relieve stress in patients, improves their pain perception, and accelerates the rate of healing.

-

Increased focus on infection control design of healthcare facilities, including the inclusion of single-patient rooms, negative pressure isolation capacity, efficient ventilation, use of antimicrobial surfaces, and spatial separation of dirty and clean processes to reduce healthcare-associated infections.

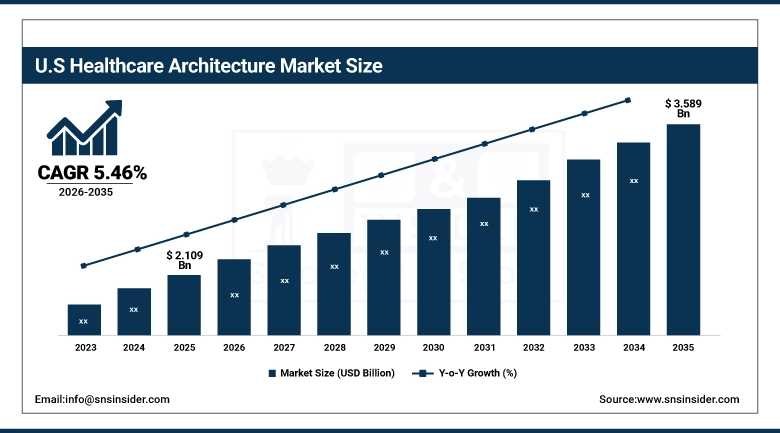

The U.S. Healthcare Architecture Market was valued at USD 2.109 billion in 2025 and is expected to reach USD 3.589 billion by 2035, registering a CAGR of 5.46% during 2026–2035.

The United States represents one of the world's largest and most sophisticated healthcare architecture markets, reflecting the country's extraordinary annual healthcare capital expenditure and the continuous need to replace, expand, and modernise the enormous installed base of U.S. hospital and clinical facilities. The U.S. healthcare construction market is driven by ageing hospital infrastructure built in the 1950s through 1970s that requires comprehensive replacement or major renovation, the rapid growth of ambulatory surgical center and outpatient care formats as healthcare delivery shifts away from inpatient settings, and the expanding needs of a rapidly ageing population requiring greater long-term care and rehabilitation facility capacity. Leading healthcare architecture firms with major U.S. practices including HDR, HKS, Perkins and Will, NBBJ, CannonDesign, and Stantec continuously deliver landmark hospital projects that set architectural standards for the global healthcare design profession.

The June 2023 HOK hospital design for USD 920 million in Michigan featuring 264 private inpatient rooms designed to convert to intensive care space represents the post-pandemic standard of U.S. hospital design, where maximum flexibility, infection control optimisation, and patient-centred private room environments are non-negotiable design requirements that command premium architectural investment. This level of design complexity and ambition across thousands of U.S. hospital projects simultaneously creates the sustained, high-value healthcare architecture demand that will sustain the U.S. market's growth trajectory through the 2026 to 2035 forecast period.

Healthcare Architecture Market Segment Analysis

-

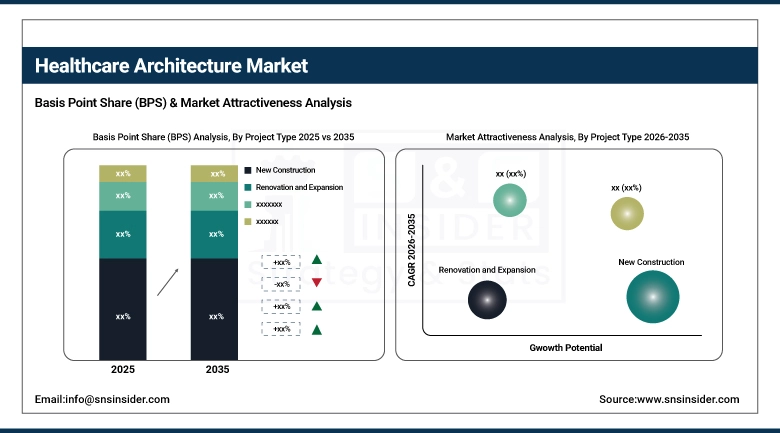

According to Project Type, New Construction dominated with the largest market share in 2025; Renovation and Expansion is projected to grow strongly as ageing global hospital infrastructure requires comprehensive modernisation investment.

-

In terms of Facility Type, Hospitals held the largest revenue share in 2025 due to their scale and construction complexity; Ambulatory Surgical Centers are the fastest-growing facility type as healthcare delivery shifts toward cost-effective outpatient care models.

-

By End-User, Public healthcare infrastructure accounted for the largest market share in 2025 driven by government hospital construction and modernisation programmes; Private healthcare is the fastest-growing segment in emerging markets.

By Project Type, New Construction segment dominates the Healthcare Architecture Market, Renovation and Expansion segment showing strong growth

New Construction projects dominated the Healthcare Architecture Market in 2025, driven by the substantial investment in new hospital facilities across both developed economies replacing ageing infrastructure and emerging economies expanding healthcare system capacity to serve rapidly growing urban populations. New hospital construction projects represent the highest-value healthcare architecture engagements, requiring comprehensive master planning, advanced medical equipment planning, complex engineering systems integration, and extensive regulatory compliance documentation that commands premium professional service fees. The global ambulatory care facility construction wave is creating a significant volume of new construction projects as health systems build purpose-designed outpatient surgical and diagnostic facilities in community locations closer to patient populations.

Renovation and Expansion projects represent a substantial and growing market segment, driven by the enormous global inventory of hospitals constructed between 1950 and 1990 that require comprehensive internal reorganisation to accommodate modern clinical models, digital health infrastructure, and infection control standards that were inconceivable when these facilities were originally designed. Major hospital renovation projects present complex architectural challenges including infection control during construction within live clinical environments, structural integration of new systems into existing building fabric, and phased delivery that maintains continuous clinical service provision throughout multi-year construction programmes.

By Facility Type, Hospitals dominate, Ambulatory Surgical Centers expected to grow fastest

Hospitals retained the dominant facility type position in the Healthcare Architecture Market in 2025, reflecting their status as the most capital-intensive and architecturally complex healthcare building type. A modern tertiary hospital encompasses hundreds of specialised clinical departments, each with unique spatial, engineering, infection control, and regulatory requirements that must be coordinated within a single complex building system. The hospital facility type's dominance is sustained by ongoing replacement construction of ageing inpatient facilities, expansion programmes driven by population growth and demographic ageing, and the increasing clinical sophistication of modern hospitals incorporating advanced imaging suites, robotic surgery theatres, and integrated research and education facilities.

Ambulatory Surgical Centers are projected to grow at the fastest CAGR through 2035, driven by the fundamental restructuring of healthcare delivery models toward outpatient care that offers equivalent clinical outcomes to inpatient procedures at significantly lower cost. ASCs are specifically designed for efficiency, enabling surgical teams to perform procedures in optimised single-specialty or multi-specialty environments with turnaround times and patient experience standards that exceed traditional hospital operating theatre settings. The growing list of procedures safely performable in ASC environments, combined with insurance payer incentives favouring outpatient over inpatient care and patient preference for convenient community-based facilities, is creating sustained demand for purpose-designed ASC architecture globally.

Regional Insights

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~75% |

|

Europe |

Germany |

~31% |

|

Asia Pacific |

China |

~47% |

|

Middle East & Africa |

UAE |

~28% |

|

Latin America |

Brazil |

~43% |

North America Healthcare Architecture Market Insights

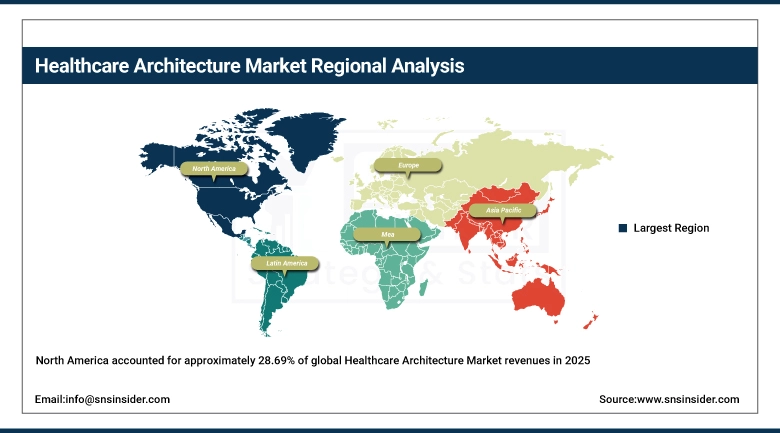

North America accounted for approximately 28.69% of global Healthcare Architecture Market revenues in 2025, led by the United States. The U.S. market is characterised by the world's most capital-intensive healthcare system, continuous hospital replacement and expansion investment, and the commercial concentration of the world's leading specialist healthcare architecture firms. Strong healthcare funding through public insurance programmes combined with substantial private health system capital investment programmes sustains exceptional healthcare architecture demand, while the regulatory complexity of U.S. healthcare facility approval processes creates competitive barriers that favour established specialist healthcare architecture practices.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Healthcare Architecture Market Insights

Asia Pacific is projected to register the fastest regional CAGR for Healthcare Architecture through 2035, driven by the extraordinary scale of healthcare infrastructure investment across China, India, Japan, South Korea, and Southeast Asia. China's government healthcare expansion programme is creating hundreds of new hospital projects annually, while India's rapidly expanding private hospital sector is commissioning sophisticated new tertiary facilities across major metropolitan areas. Japan and South Korea's ageing populations are driving significant long-term care facility and specialist geriatric hospital construction, while Southeast Asian healthcare systems are investing in modern hospital infrastructure to support growing medical tourism industries.

Europe Healthcare Architecture Market Insights

Europe represents a mature and technically sophisticated healthcare architecture market, driven by public hospital modernisation programmes across EU member states, public-private partnership hospital construction models particularly in the UK and France, and growing private healthcare investment across Central and Eastern Europe. The emphasis on sustainable healthcare building design in European construction procurement, combined with stringent infection control standards and patient environment quality requirements, creates a premium design market where specialist healthcare architecture expertise commands premium professional fees. Germany leads European healthcare construction investment through its federal hospital modernisation fund, while the UK, France, and the Netherlands are significant secondary European markets.

Middle East & Africa and Latin America Healthcare Architecture Market Insights

MEA and Latin America are growing healthcare architecture markets driven by significant government investment in new hospital infrastructure. The UAE and Saudi Arabia are executing ambitious healthcare facility expansion programmes as part of Vision 2030 economic diversification, constructing technologically advanced hospitals designed to world-class standards by international specialist architecture firms. Brazil leads Latin American healthcare architecture revenues at approximately 43% of regional share, driven by its large public hospital network requiring ongoing investment and the rapidly expanding private hospital sector serving Brazil's growing middle class.

Healthcare Architecture Market Growth Drivers:

-

Ageing global population creating irreversible structural demand for expanded and modernised healthcare facility infrastructure

The primary structural growth driver for the Healthcare Architecture Market is the irreversible global demographic transition toward an older population that creates exponentially greater demand for healthcare services and the specialised facilities that deliver them. With the WHO projecting 2.1 billion people aged 60 or older by 2050, healthcare systems worldwide face the compound challenge of simultaneously expanding inpatient, surgical, rehabilitation, and long-term care capacity to serve this population surge while replacing the ageing infrastructure built during earlier population expansion periods that is approaching or exceeding its functional design life. Healthcare infrastructure investment is a governmental and institutional priority that is relatively resistant to economic cycles, creating predictable, long-duration demand for healthcare architecture professional services through the forecast period.

The rising demand for healthcare infrastructure investment in developing economies across Asia, Africa, the Middle East, and Latin America is creating a global healthcare architecture market growth dynamic that extends well beyond the traditional North American and European demand base, as emerging market governments and private healthcare groups commission sophisticated new facilities designed to international standards of patient care, clinical technology integration, and sustainable building performance. This geographical expansion of sophisticated healthcare architecture demand is broadening the market's addressable opportunity and sustaining the industry's steady CAGR growth trajectory through the 2026 to 2035 forecast period.

Healthcare Architecture Market Restraints

-

Rising construction costs, complex regulatory approval processes, and extended project delivery timelines limiting healthcare capital programme execution

A significant restraint on the Healthcare Architecture Market is the extraordinary escalation of healthcare construction costs driven by specialised medical equipment costs, complex infection control requirements, life safety systems, advanced engineering installations, and skilled labour scarcity that makes healthcare facilities among the most expensive building types per square foot globally. The regulatory approval process for new healthcare facilities, encompassing planning permission, building code compliance, fire safety certification, healthcare regulator approval, and infection control sign-off, creates multi-year pre-construction timelines that delay market revenue realisation for architecture firms committed to complex hospital projects. Managing the integration of rapidly evolving medical technologies into building designs that have long lead times creates significant design obsolescence risk, requiring architecture firms to develop adaptable design strategies that anticipate technology change without creating overdesigned facilities that are economically impractical.

Healthcare Architecture Market Opportunities

-

Green healthcare building design, digital health infrastructure integration, and long-term care facility expansion

The global health system commitment to net-zero carbon operations is creating a premium market segment for green healthcare building design that integrates renewable energy generation, high-performance building envelopes, heat recovery ventilation, and smart building management systems within the specialised constraints of clinical facility design. Digital health infrastructure integration within new healthcare buildings, encompassing telehealth consultation suites, medical-grade Wi-Fi, electronic health record workstation networks, and smart patient room technology, represents a growing specification requirement that expands architecture firm service scope and fee potential. The rapidly growing long-term care facility sector, driven by global population ageing, represents a high-volume architecture market opportunity where purpose-designed dementia care, rehabilitation, and assisted living environments demonstrably improve resident outcomes and operational efficiency.

Recent Developments:

-

June 2023: HOK finalised the design of a 264-bed hospital for USD 920 million in Michigan, incorporating private inpatient rooms convertible to intensive care space, scheduled to open in 2025 as a landmark patient-centred facility design.

-

June 2023: CannonDesign announced completion of the expanded emergency department at the University of Chicago, adding 41,000 square feet of new capacity to the existing 35,000 square feet facility to increase patient volume and improve care flow.

-

2024: Perkins and Will continued advancing its sustainable healthcare design practice, completing several LEED Platinum-certified hospital projects incorporating passive energy strategies, renewable energy integration, and biophilic design elements targeting net-zero operational carbon performance.

-

2025: HDR expanded its healthcare architecture practice with enhanced digital health planning services, integrating telehealth infrastructure design and smart building technology specifications into standard hospital project delivery processes.

-

2024: Stantec completed multiple ambulatory surgical center designs across North America and Australia, incorporating evidence-based design principles optimised for single-day surgery patient flow, infection control, and staff efficiency that reduce per-procedure costs relative to traditional hospital operating theatres.

Healthcare Architecture Market Key Players

-

HDR Inc.

-

HKS Inc.

-

Perkins and Will

-

NBBJ

-

CannonDesign

-

Stantec Inc.

-

HOK Group Inc.

-

Jacobs Engineering Group Inc.

-

SmithGroup JJR

-

Gensler

-

Hammel Green and Abrahamson (HGA)

-

ZGF Architects LLP

-

AECOM

-

Medical Facilities Corporation

-

G2 Architecture

-

Page Southerland Page LLP

-

Robert AM Stern Architects

-

Orbis International

-

RKW Architektur

-

GMP Architekten

Healthcare Architecture Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.06 Billion |

| Market Size by 2035 | USD 15.42 Billion |

| CAGR | CAGR of 5.46% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Project Type (New Construction, Renovation and Expansion) • By Facility Type (Hospitals, Ambulatory Surgical Centers, Medical and Diagnostic Laboratories, Long-Term Care Facilities, Others) • By End-User (Public, Private) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | HDR Inc., HKS Inc., Perkins and Will, NBBJ, CannonDesign, Stantec Inc., HOK Group Inc., Jacobs Engineering Group Inc., SmithGroup JJR, Gensler, Hammel Green and Abrahamson (HGA), ZGF Architects LLP, AECOM, Medical Facilities Corporation, G2 Architecture, Page Southerland Page LLP, Robert AM Stern Architects, Orbis International, RKW Architektur, GMP Architekten |

Frequently Asked Questions

The Healthcare Architecture Market is expected to grow at a CAGR of 5.46% from 2026 to 2035.

The Healthcare Architecture Market was valued at USD 9.06 billion in 2025.

The irreversible global demographic transition toward an older population creating exponentially greater demand for healthcare services and specialised facilities, combined with the ageing of existing hospital infrastructure requiring comprehensive replacement and modernisation investment, and rising healthcare capital expenditure in emerging economies expanding their healthcare system capacity.

New Construction dominated the Healthcare Architecture Market in 2025, representing the highest-value healthcare architecture engagements encompassing new hospital facilities, ambulatory care centers, and specialty clinical facilities constructed in developing economies and to replace ageing infrastructure in established healthcare markets.

North America dominated the Healthcare Architecture Market in 2025, led by the United States which accounted for approximately 75% of North American revenues, driven by the world's most capital-intensive healthcare system, continuous hospital replacement and expansion investment, and the commercial concentration of world-leading specialist healthcare architecture firms.

Get in Touch