Helium Market Report Scope & Overview:

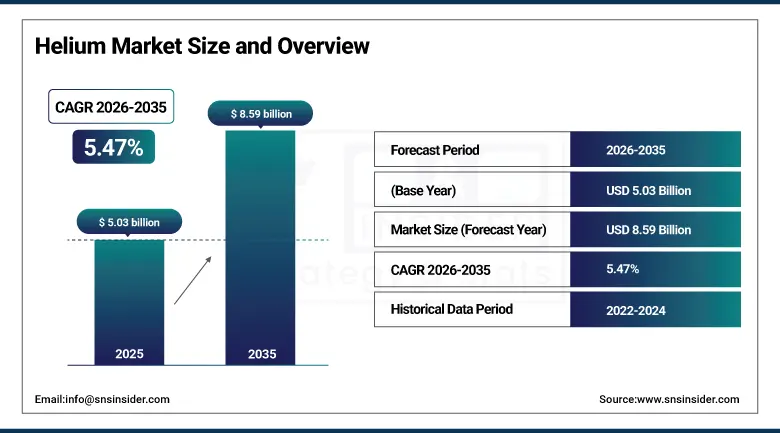

The Helium Market was valued at USD 5.03 Billion in 2025 and is expected to reach USD 8.59 Billion by 2035, growing at a CAGR of 5.47% from 2026–2035.

The Helium Market functions based on the characteristics of the gas, such as extremely low boiling point, chemical inertness, high heat conductivity, and low density. These attributes make helium an essential gas for multiple industries, such as medicine, science, and aerospace engineering. The gas is extensively used in MRIs, semiconductor fabrication, fiber optic manufacturing, leak testing, welding, and space missions, where there is no other available substitute. Although helium is the second most plentiful gas in the universe, it is considered to be a scarce substance on Earth and produced at just a few plants around the globe.

In October 2023, North American Helium initiated operations at its seventh helium purification plant in Cadillac, near Ponteix, Saskatchewan, with production capacity of 22 million cubic feet per year and expansion planned for 2024. The facility's commissioning reflected the commercial strategy of developing North American helium supply independent of the geopolitical concentrations in Qatar and Russia whose disruption risk motivates end-use industries to support new Western hemisphere supply development.

Market Size and Forecast

-

Market Size in 2026E: USD 5.30 Billion

-

Market Size by 2035: USD 8.59 Billion

-

CAGR: 5.47% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Helium Market - Request Free Sample Report

Helium Market Trends

-

Helium recycling and recovery systems are gaining adoption to reduce consumption, improve supply security, and mitigate price volatility

-

Expansion of quantum computing infrastructure is creating a rapidly growing demand source for liquid helium cooling systems

-

New helium production projects are diversifying global supply and reducing dependence on traditional producing regions

-

Semiconductor manufacturing expansion is driving increased helium consumption in wafer fabrication and chip production processes

-

Growing MRI installations in emerging economies are expanding helium demand across the global healthcare sector

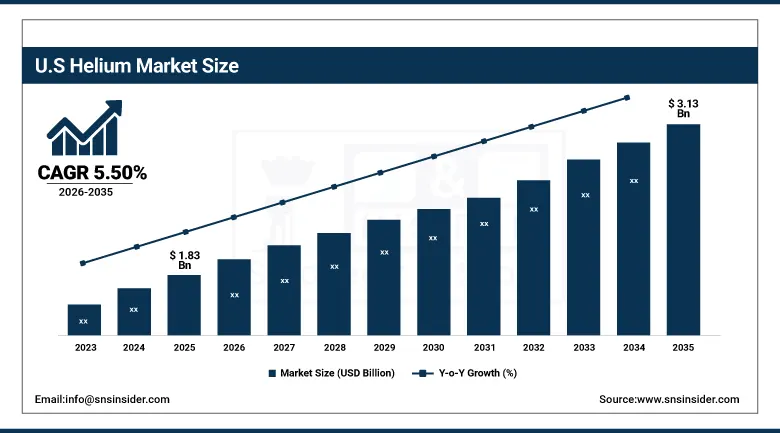

U.S. Helium Market Outlook

The U.S. Helium Market was valued at approximately USD 1.83 Billion in 2025 and is expected to reach approximately USD 3.13 Billion by 2035, growing at a CAGR of approximately 5.50%.

The U.S. helium industry is witnessing a major change in its structure owing to the closure of the Federal Helium Reserve, leading to the dependency of consumers on commercial providers and making them more vulnerable to international markets. This has impacted the supply chains and cost of helium for consumers within the U.S. As well as that, huge investments in the semiconductor industry have led to the emergence of another significant market player for helium in terms of demand from the industry.

In 2024, Air Products and Chemicals Inc. finalised a long-term helium supply agreement with a major Asian semiconductor manufacturer to supply liquid helium from its expanded liquefaction and distribution network, securing multi-year offtake commitments that finance the supply chain infrastructure investment required to serve Asia Pacific's fastest-growing helium consumption market.

Helium Market Segment Analysis

-

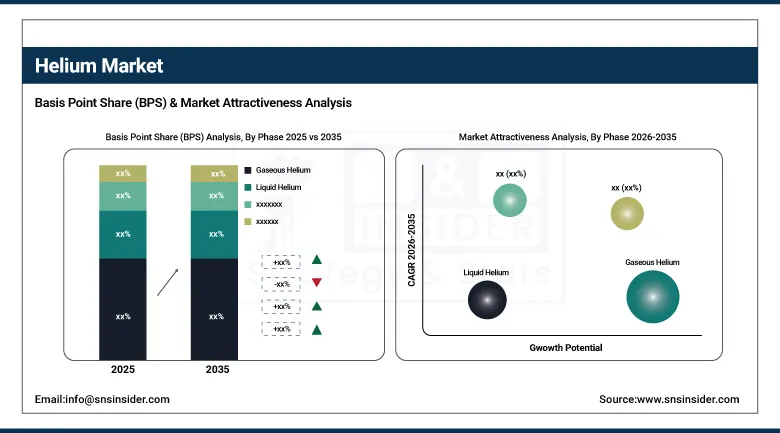

By Phase, the Gaseous Helium segment dominated the Helium Market with approximately 72% share in 2025, while the Liquid Helium segment is the fastest growing phase.

-

By Application, the Cryogenics segment dominated the Helium Market with the largest share in 2025, while the Controlled Atmospheres segment for semiconductor and optical fibre manufacturing is among the fastest growing applications during 2026 to 2035.

-

By End User, the Healthcare & Medical segment dominated the Helium Market with the largest share in 2025, while the Electronics & Semiconductors segment is the fastest growing end user.

By Phase, gaseous helium dominates, liquid grows fastest

The gaseous helium category was the leading category in the helium market during 2025, accounting for about 72% of the market share, owing to its wide range of applications in various industries such as industrial, aerospace, electronics, and manufacturing industries. Gaseous helium is a preferred choice because of its ease of transport, handling, and storage using cylinders, tube trailers, and gas distribution channels. It is widely used in welding processes, leakage testing, electronics manufacturing, pressurizing, purging processes, and scientific research requiring an inert gas atmosphere.

Liquid helium is growing fastest as the cryogenic applications requiring helium at temperatures below 4.2 Kelvin, primarily superconducting magnet cooling in MRI scanners, NMR spectroscopy systems, particle physics accelerators, and the emerging quantum computing infrastructure, require liquid phase delivery whose additional liquefaction cost and specialised Dewar vessel transport creates a premium market segment whose growth is driven by the expanding installed base of superconducting magnet systems globally.

By End User, healthcare dominates, electronics & semiconductors grows fastest

The Healthcare & Medical segment dominated the helium market in 2025 due to the critical role of helium in cooling superconducting magnets used in MRI systems. Helium is an essential and non-substitutable component for MRI operation, creating a stable and recurring demand base across hospitals, diagnostic centers, and healthcare facilities worldwide. The continuous expansion of medical imaging infrastructure, particularly in emerging economies, is further supporting demand. Growing investments in healthcare modernization and increasing adoption of advanced diagnostic technologies continue to reinforce the segment’s leading position in the global helium market.

The Electronics & Semiconductors segment is the fastest-growing end-user category in the helium market, driven by rapid expansion of global semiconductor manufacturing capacity. Helium is widely used in wafer fabrication, controlled atmosphere processing, cooling applications, equipment cleaning, and advanced chip production processes. Rising investments under semiconductor manufacturing initiatives and increasing demand for advanced electronic devices are accelerating helium consumption across fabrication facilities.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

Qatar |

68.4% |

|

Latin America |

Brazil |

43.8% |

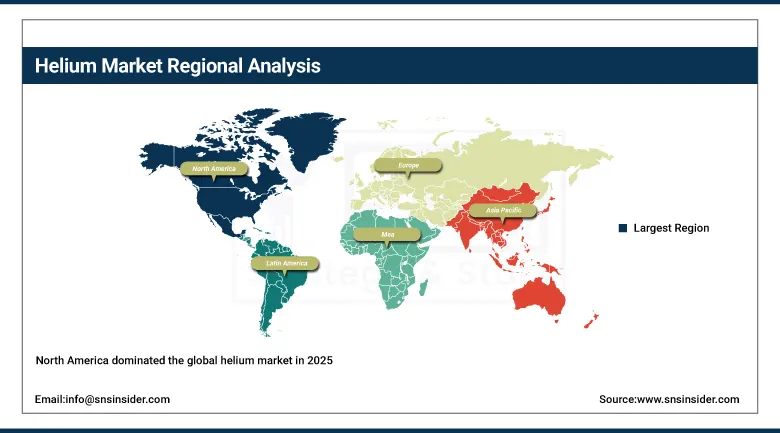

North America Helium Market Insights

North America dominated the global helium market in 2023, accounting for the largest regional revenue share through its combination of significant domestic helium production infrastructure, the world's most extensive MRI installed base creating the largest single application demand pool, and the concentration of aerospace, semiconductor, and research laboratory helium consumers whose combined consumption sustains the region's market leadership.

The United States accounts for approximately 82.5% of North American revenues through its dual role as both producer and the world's largest consumer of helium across healthcare, aerospace, and industrial applications whose combined demand creates the foundational commercial case for North American helium supply infrastructure investment.

Canada is growing as a helium supply contributor as Saskatchewan's helium-bearing geological formations are developed by companies including North American Helium, Royal Helium, and Helium Evolution whose progressive production capacity expansion provides geopolitically diversified supply for both domestic Canadian consumption and export to U.S. and Asian markets.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Helium Market Insights

Europe held a significant share of the global Helium Market in 2025. Germany, France, the United Kingdom, the Netherlands, and Switzerland are the leading national markets whose pharmaceutical and medical device manufacturing, semiconductor and electronics production, research institution, and aerospace and defence industries create diverse and consistent helium demand.

Germany accounts for approximately 28.5% of European revenues through the helium consumption of its world-leading chemical industry, pharmaceutical manufacturers, and the Helmholtz Association's large research infrastructure whose superconducting magnet systems create significant liquid helium demand.

European helium demand is navigating the post-2022 supply disruption landscape where Russian helium supply reduction created acute shortages across European industrial users whose alternatives from Qatar, U.S., and new African sources required logistics investment and long-term supply contract restructuring.

Asia Pacific Helium Market Insights

Asia Pacific is the fastest-growing regional helium market, driven by the extraordinary pace of semiconductor capacity expansion across Taiwan, South Korea, Japan, and China, the rapid growth of the MRI installed base as healthcare infrastructure investment extends advanced medical imaging across the region's population, and the development of quantum computing research programmes at national laboratory and commercial technology company facilities.

China accounts for approximately 38.5% of Asia Pacific revenues through its growing semiconductor manufacturing sector, rapidly expanding MRI fleet in major hospital networks, and the industrial helium consumption of its aerospace and space launch programmes.

Japan, South Korea, and Taiwan contribute premium regional demand through their world-leading semiconductor and electronics industries whose per-facility helium consumption is among the highest of any industrial application.

MEA & Latin America Helium Market Insights

The Middle East leads MEA helium revenues through Qatar's position as the world's second-largest helium producer whose Ras Laffan helium facilities operated by RasGas and Qatargas supply approximately 25 to 30% of global helium demand.

Qatar accounts for approximately 68.4% of MEA revenues as both the regional production hub and a supplier to Asian and European markets, with the UAE, Saudi Arabia, and Israel contributing regional consumption from healthcare, aerospace, and research applications.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its MRI healthcare infrastructure investment, industrial manufacturing helium consumption, and the growing research laboratory sector. Argentina and Mexico contribute growing secondary market demand through their healthcare sector MRI deployment and industrial helium applications in aerospace and manufacturing sectors.

Market Dynamics

Growth Drivers: MRI healthcare infrastructure expansion across emerging economies and semiconductor capacity proliferation creating above-trend helium demand growth from its two largest application categories

The growth in the global helium market is attributed to the increase in the consumption by the health care industry owing to the need for liquid helium for the effective functioning of MRI systems. With more health care establishments being set up and an increase in accessibility of high-quality diagnostic technology in emerging countries located in the Asia-Pacific, Latin America, and Middle East regions, there will be new opportunities for helium demand growth.

On another hand, the fast growth of production capacities in the semiconductor industry becomes a strong factor of helium demand growth. Indeed, helium is used for different purposes in wafer processing including cooling, purging, and controlled atmosphere processes. With the development of government-supported semiconductor projects and advanced fabrication plants in other countries, the demand for industrial helium is growing.

Restraints: Geographic supply concentration and price volatility creating procurement security risk for helium-dependent industries and constraining market development in price-sensitive applications

The helium market faces a significant challenge due to the concentration of global supply among a limited number of producers and regions. This dependence on a small group of suppliers increases vulnerability to geopolitical events, production disruptions, and transportation constraints, creating supply uncertainty for industrial users. As a result, many organizations are investing in long-term supply agreements, helium recovery systems, and diversified sourcing strategies to improve supply security and reduce operational risk.

Another key restraint is the continued rise in helium prices, which has outpaced general inflation over the long term. Increasing costs are placing pressure on helium-consuming industries and encouraging efforts to improve efficiency, reduce consumption, and adopt recycling technologies. In some non-critical applications, rising prices are also motivating the exploration of alternative gases and technologies that can reduce dependence on helium.

Opportunities: Quantum computing helium demand and new supply geography development in Tanzania and Saskatchewan represent transformative market expansion and supply security improvement frontiers

The fast evolution of quantum computers is a major growth avenue for the market of helium. The superconducting quantum computers need to operate in extremely low temperatures that can be provided using liquid helium cooling equipment. As technology firms and laboratories keep investing into quantum computers, there is likely to emerge an additional source of demand for helium that cannot be underestimated.

On the other hand, new production facilities in such countries as Tanzania and Saskatchewan will contribute to increased diversification of the supply chain in the industry. This means that the new helium producers have the potential to decrease the reliance on existing production facilities and ensure long-term safety of the supply chain in all the industries using helium.

Recent Developments:

-

2024: Air Products and Chemicals finalised a long-term liquid helium supply agreement with a major Asian semiconductor manufacturer to supply from its expanded liquefaction and distribution network, securing multi-year offtake commitments that finance supply chain infrastructure investment for Asia Pacific's fastest-growing helium consumption market.

-

2023: North American Helium initiated operations at its seventh helium purification plant in Saskatchewan with 22 million cubic feet per year capacity, expanding Western hemisphere supply diversification as part of the broader North American helium supply development programme reducing dependence on Middle Eastern and Russian sources.

-

2023: Linde PLC commissioned expanded helium liquefaction capacity at its U.S. Gulf Coast facility, increasing liquid helium production to serve growing demand from the medical MRI, quantum computing, and semiconductor fabrication sectors whose liquid phase consumption requirements are growing at above-market rates.

Helium Market Key Players

-

Air Products and Chemicals Inc.

-

Linde PLC

-

Air Liquide SA

-

Matheson Tri-Gas Inc. (TNSC)

-

RasGas Company Ltd. (QatarEnergy LNG)

-

Exxon Mobil Corporation

-

Gazprom PJSC

-

Messer SE & Co. KGaA

-

Iwatani Corporation

-

North American Helium Inc.

-

Royal Helium Ltd.

-

Desert Mountain Energy Corp.

-

Helium One Global Ltd.

-

Global Helium Corp.

-

Taiyo Nippon Sanso Corporation

-

Weil McLain Holdings Inc.

-

Proton World International SA

-

Quantum Industrial Group

-

Gulf Cryo

-

Cryogenic Industries Inc.

Helium Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.03 Billion |

| Market Size by 2035 | USD 8.59 Billion |

| CAGR | CAGR of 5.47% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Phase (Gaseous Helium, Liquid Helium) • by Application (Cryogenics, Pressurising & Purging, Welding, Controlled Atmospheres, Leak Detection, Breathing Mixes, Others) • by End User (Healthcare & Medical, Electronics & Semiconductors, Aerospace & Defense, Manufacturing, Energy, Research & Development, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Air Products and Chemicals Inc., Linde PLC, Air Liquide SA, Matheson Tri-Gas Inc. (TNSC), RasGas Company Ltd. (QatarEnergy LNG), Exxon Mobil Corporation, Gazprom PJSC, Messer SE & Co. KGaA, Iwatani Corporation, North American Helium Inc., Royal Helium Ltd., Desert Mountain Energy Corp., Helium One Global Ltd., Global Helium Corp., Taiyo Nippon Sanso Corporation, Weil McLain Holdings Inc., Proton World International SA, Quantum Industrial Group, Gulf Cryo, Cryogenic Industries Inc. |

Frequently Asked Questions

The Helium Market is expected to grow at a CAGR of 5.47% from 2026 to 2035.

Healthcare MRI infrastructure expansion across emerging economies, semiconductor capacity expansion under national investment programmes creating above-trend helium demand.

The Gaseous Helium segment dominated the Helium Market with approximately 72% share in 2025.

North America dominated the Helium Market in 2025, accounting for the largest regional share through its domestic production infrastructure and world-leading MRI.

Get in Touch