Hernia Mesh Devices Market Report Overview

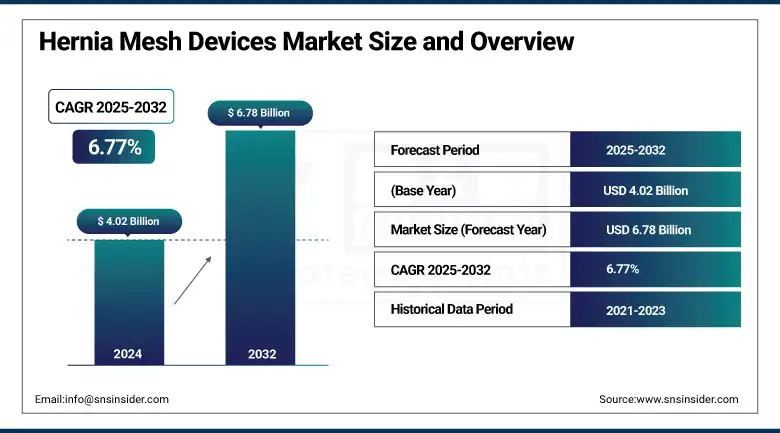

The Hernia Mesh Devices Market size was valued at USD 4.02 billion in 2024 and is expected to reach USD 6.78 billion by 2032, growing at a CAGR of 6.77% over 2025-2032.

The hernia mesh devices market is witnessing promising innovation trends with increasing surgical volumes, technological innovation, and long-term patient outcomes. The increasing prevalence of hernia, especially in the elderly and obese patient cohort, is a major growth factor beneficial for driving the need for efficient surgeries, which in turn leads to the higher uptake of innovative mesh implants. The popularity of MI surgeries, favorable reimbursement strategies, and clinical evidence in favor of biologic and hybrid meshes are also aiding the expansion of the global hernia mesh devices market. The U.S. hernia mesh devices market is particularly known for playing a pivotal role, whereby several frontrunner healthcare systems have been keen on minimizing the rate of surgical recurrence using long-acting resorbable meshes, as reported in an ACS study in 2025 that reported the lowest five-year recurrence with such mesh solutions.

To Get more information On Hernia Mesh Devices Market - Request Free Sample Report

Moreover, legal disputes and product recalls have stretched the limits of innovation, leading to greater investment in R&D and quality control. Companies including BD, Medtronic, and Tela Bio are out ahead with strong pipelines, and Tela Bio has received FDA clearance for its OviTex IHR mesh, and Absolutions was designated a breakthrough device for its unique offering. These latest trends are influencing the hernia mesh devices market share, with newcomers working to take the place of the old guard. Regulatory entities, such as the FDA, shape the market landscape by enforcing rigorous post-market surveillance and implementing updated safety protocols, driving the trend towards more biocompatible materials.

The global hernia mesh devices market is further expected to be driven by growing funding for the advancement of medical devices, the filing of patents (Hexagon Health vs. Medtronic), and hospital preferences for meshes having proven clinical knowledge. The global market will witness increased demand for products with improved infection resistance, better tissue incorporation, and rapid recovery. The hernia mesh devices market trends for hybrid and biologic are seeing uptake quicker with respect to the low complications of the products over synthetic ones. With production in more countries and a broader range of products, the hernia mesh devices vendors are set to gain market growth in high-volume surgical areas.

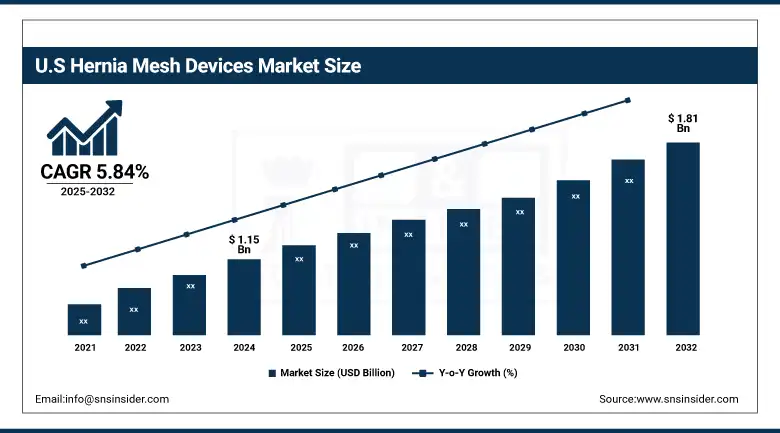

The U.S. hernia mesh devices market size was valued at USD 1.15 billion in 2024 and is expected to reach USD 1.81 billion by 2032, growing at a CAGR of 5.84% over 2025-2032.

Hernia Mesh Devices Market Dynamics

Drivers:

-

Increasing Surgical Demand, Technological Advancements, and Regulatory Momentum Propel Market Growth

The hernia mesh devices market growth is largely driven by the increasing adoption of hernia mesh in surgeries, the rising geriatric population, new product developments, and a favorable reimbursement scenario for hernia mesh repair. Globally, more than 20 million hernias are repaired annually, with the use of mesh being the standard in greater than 90% of these. This large demand is pushing for the manufacturing and invention of new mesh devices. Rising adoption is being fueled by increasing acceptance of minimally invasive and robotic-assisted surgeries.

Investing in R&D is also picking up, with companies such as Gore and Cook Medical working on anti-adhesion coatings and rates of mesh incorporation. Based on NIH statistics, biologic mesh innovation has increased 35% over the past five years. Regulatory momentum is another factor; several next-gen mesh products are FDA-approved through 510(k) and de novo routes, facilitating quicker entry into the market. In addition, industry partnerships and investment, including start-ups to produce bioengineered mesh, are increasing supply. Moreover, patients' clamor for minimizing the recurrence and reducing the infection risk is also influencing acquisition and utilization, and thereby fueling the global hernia mesh devices market growth.

Restraints:

-

Legal Liabilities, Safety Concerns, and Product Recalls Hinder Market Expansion

In the rapidly moving innovation environment, the market for hernia mesh devices will be delayed by legal, clinical, and reputational obstacles. Thousands of lawsuits have been filed globally over the past 10 years against companies, including Bard and Ethicon, with claimants telling of chronic pain, mesh migration, and perforation of organs. In 2023 alone, BD (Bard’s parent) resolved most of its hernia mesh litigation, representing hundreds of millions in liability. The events have caused hospitals and surgeons to pay closer attention to mesh brand names, decreasing the demand for some synthetic meshes.

Safety is more prevalent with recalls, such as the retention of Physiomesh (Ethicon), resulting in supply shortages and a lack of confidence among surgeons. The FDA makes ongoing post-market surveillance recommendations and safety notices, most recently the 2023 notification that clarifies the hazards of intraperitoneal mesh placement. Furthermore, the expensive cost of biologic mesh that is not fully reimbursed restricts its application to cost-containment healthcare systems. These concerns directly impact manufacturer reputation, investor interest, and end-user confidence, limiting the hernia mesh products market share and clinical possibility for use of new technologies.

Hernia Mesh Devices Market Segmentation Analysis

By Type

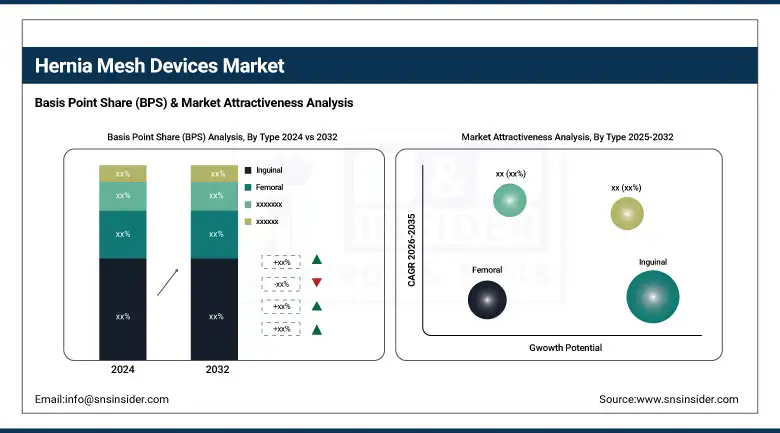

In 2024, the inguinal hernia mesh devices category led the market owing to the high incidence of inguinal hernias globally, with more than 70% of all types of abdominal wall hernias being inguinal. This predominance is also reinforced by the universal use of mesh-based laparoscopic and open-surgical repairs. The ventral hernia segment, on the other hand, is expected to grow at the fastest CAGR during the forecast period. The growth is driven by the increase in obesity, post-surgical incisional hernias, and clinical support for mesh reinforcement for complex abdominal wall reconstructions, particularly when the patient is high risk.

By Product

Synthetic mesh accounted for the highest market share of 66.6% in 2024 on account of its cost-effectiveness, easy availability, and consistent performance in lowering the rate of recurrence in regular hernia surgeries. Being durable and used in both open and laparoscopic approaches, it is a common tool in almost all surgical rooms. Conversely, the biological mesh segment is anticipated to demonstrate the fastest growth, based on its application in contaminated areas, lower infection risk, and a rising preference for bioengineered products that facilitate tissue regeneration, especially in complex or recurrent hernia procedures.

By End-user

The hospitals and clinics segment dominated and held a 56.2% share of the global hernia repair devices market in 2024, driven by a large number of hernia repair surgeries performed in these facilities. They were the most used center for mesh-based procedures, due to access to the state-of-the-art surgical facilities, specialists, and insurance. On the other hand, ambulatory surgery centers (ASCs) are expected to grow the fastest. With the growing trend toward outpatient surgery and a decrease in hospital LOS, reduced costs, and faster recovery times, ASCs have become an appealing option for elective hernia repairs, especially in developed healthcare systems.

Global Hernia Mesh Devices Market Regional Outlook

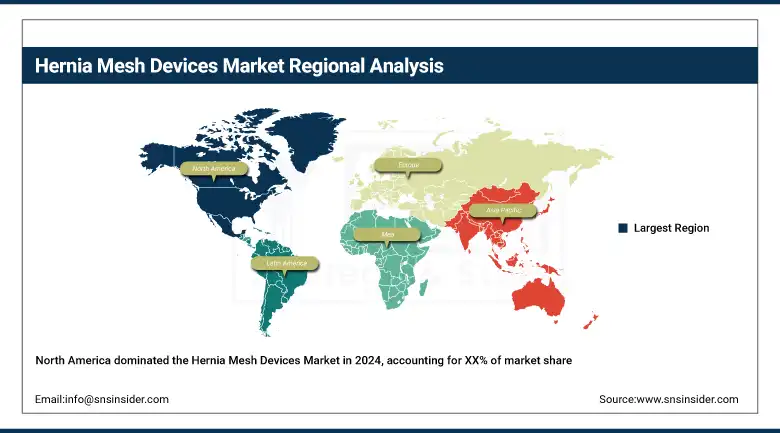

The hernia mesh devices market is dominated by North America in 2024, as the region has a large number of hernia repair procedures, a well-established healthcare sector, and favorable reimbursement policies. The U.S. is the regional leader with more than 1 million hernia repairs annually, with over 90% of patients receiving mesh. The nation also has high levels of clinical research, technical innovation, and early utilization of biologic mesh products. Having BD and Medtronic as major players in the space will guarantee that supply is not an issue and that innovation will not be in short supply. There is also an increase in the usage of mesh-based procedures in Canada as knowledge grows, and with public healthcare. Mexico is a small market, but increasing surgical cases and healthcare modernization are driving regional growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second largest region, driven by a growing geriatric population and higher acceptance for laparoscopic surgeries. The regional market is dominated by Germany on account of the large volume of surgical procedures, the presence of well-equipped centers, and mesh used for open and minimally invasive procedures. For nations, such as the U.K. and France, a greater focus on the development of biologic and hybrid meshes is being seen as their healthcare systems demand diminished post-operative complications. Eastern Europe, such as Poland and Turkey, is also gaining prominence with increasing procedure numbers and medical tourism, where patients travel across borders for affordable treatments.

Asia Pacific is the highest growing market globally, with growth driven by greater healthcare spending, urbanization, an increasingly obese and aging patient population, and the hernia. China is at the forefront of the rise of more hernia operations by scale of intensive hospital construction and government-led medical policy transformation. India also contributes substantially, driven by increasing access to affordable surgical care, and the rise of disposable income, spending on elective surgery is growing due to the emergence of a large middle-class population and availability of mesh products. Early adopters of advanced and minimally invasive surgery techniques are Japan and South Korea, with governments investing in the innovation of surgery and their elderly populations.

Key Players in the Hernia Mesh Devices Market

Leading hernia mesh devices companies operating in the market include Johnson & Johnson Services, C.R. Bard, W.L. Gore & Associates, Atrium Medical (Getinge), LifeCell, B. Braun SE, Baxter International, Cook Medical, Herniamesh S.r.l., Medtronic plc and Others

Recent Trends and Developments in Hernia Mesh Devices

In June 2025, the American College of Surgeons highlighted that long-acting resorbable meshes demonstrated the lowest five-year recurrence rates in ventral hernia repairs, significantly impacting hospital procurement patterns and supporting hernia mesh devices market trends.

In May 2024, A lawsuit by Hexagon Health against Medtronic for patent infringement underscores intense competition and R&D-driven differentiation in the global hernia mesh devices market, pushing for unique technologies and innovative delivery systems.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 4.02 billion |

| Market Size by 2032 | USD 6.78 billion |

| CAGR | CAGR of 6.77% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Inguinal, Femoral, Ventral, and Others) • By Product (Biological Mesh, Synthetic Mesh) • By End-user (Hospitals & Clinics, Ambulatory Surgical Centers, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Johnson & Johnson Services, C.R. Bard, W.L. Gore & Associates, Atrium Medical (Getinge), LifeCell, B. Braun SE, Baxter International, Cook Medical, Herniamesh S.r.l., and Medtronic plc |

Get in Touch