HIV Diagnostics Market Report Scope & Overview:

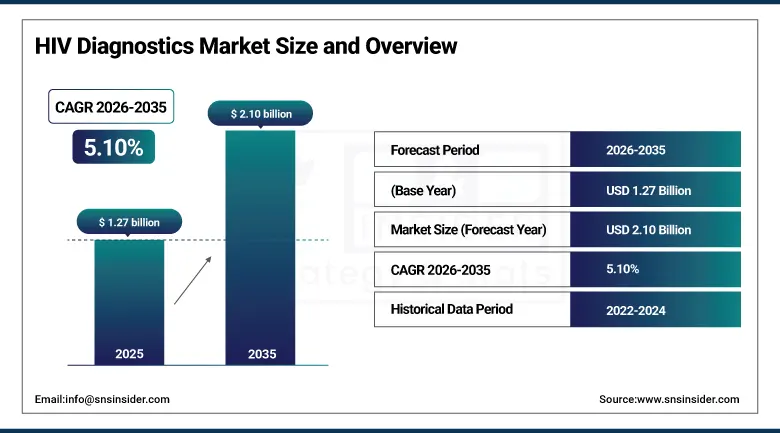

The HIV Diagnostics Market was valued at USD 1.27 Billion in 2025 and is expected to reach USD 2.10 Billion by 2035, growing at a CAGR of 5.10% from 2026–2035.

The global HIV diagnostics market is growing at a broad-based pace. HIV diagnostics encompass the full spectrum of laboratory and point-of-care tests used to detect HIV infection. These include antibody screening assays, fourth-generation combined antigen/antibody tests, molecular nucleic acid amplification tests, viral load quantification platforms, CD4 cell count instruments, and rapid point-of-care test devices. The market is driven by the rising incidence of HIV which continues to fuel demand for advanced diagnostic platforms, increased public awareness of early testing benefits, improved healthcare access, and next-generation diagnostic technology advancing point-of-care testing capability.

In 2024, Abbott launched its ARCHITEST HIV Ag/Ab Combo Plus assay for the ARCHITECT analyzer platform, incorporating enhanced p24 antigen detection sensitivity that reduces the window period for HIV detection by several days. The improvement directly supports the CDC's HIV testing guideline recommendation for fourth-generation combination testing as the standard of care, whose adoption across U.S. clinical laboratories creates structured Abbott platform procurement that benefits from installed ARCHITECT base expansion.

Market Size and Forecast

-

Market Size in 2026E: USD 1.34 Billion

-

Market Size by 2035: USD 2.10 Billion

-

CAGR: 5.10% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on HIV Diagnostics Market - Request Free Sample Report

HIV Diagnostics Market Trends

-

Fourth-generation HIV antigen/antibody assays replace older tests, improving early detection and reducing diagnostic window period.

-

At-home HIV self-testing kits expand due to regulatory approvals, stigma reduction, and improved accessibility in remote regions.

-

HIV viral load nucleic acid testing becomes more accessible through cost reduction and global health procurement programs like PEPFAR.

-

AI-enabled point-of-care HIV test reading improves accuracy and supports digital reporting through smartphone-based systems.

-

Multiplex STI/HIV testing platforms enhance efficiency by enabling simultaneous detection and faster diagnostic turnaround.

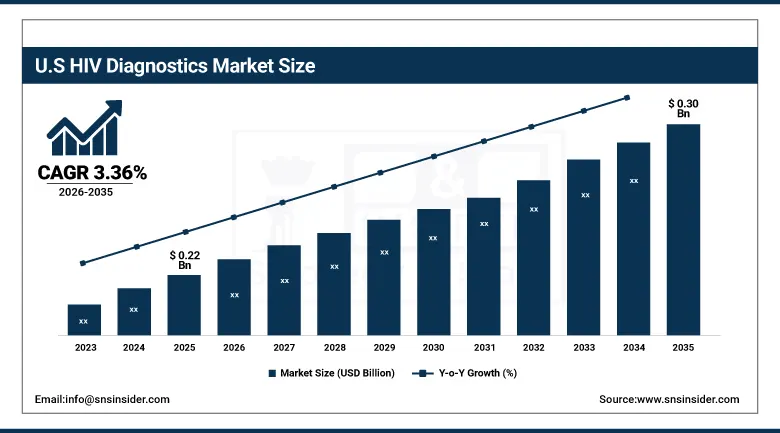

The U.S. HIV Diagnostics Market Outlook

The U.S. HIV diagnostics market was valued at approximately USD 0.22 Billion in 2025 and is expected to reach approximately USD 0.30 Billion by 2035, growing at a CAGR of approximately 3.36%.

The U.S. is a commercially sophisticated HIV diagnostics market within North America’s dominant revenue position. Abbott, Siemens Healthineers, Roche Diagnostics, Hologic, and OraSure Technologies serve the domestic market across laboratory, point-of-care, and self-testing channels. CDC’s recommendation for routine HIV screening in healthcare settings, HRSA’s Ryan White HIV/AIDS Programme funding, and the Biden Administration’s Ending the HIV Epidemic in the U.S. initiative collectively create structured institutional procurement that sustains consistent testing volume growth. OraQuick’s FDA-approved at-home HIV test and INSTI’s point-of-care platforms demonstrate the U.S. market’s advanced self-testing and rapid testing infrastructure.

Hologic launched its Aptima HIV-1 Quant Dx assay in 2024, a next-generation HIV-1 viral load test for the Panther system providing accurate quantification from 30 to 10,000,000 copies/mL with enhanced performance in samples with complex matrices. The assay’s broad dynamic range and single-assay format eliminate the separate high-range confirmatory testing requirement, reducing laboratory workflow complexity and turnaround time for viral load monitoring in antiretroviral therapy management programmes.

HIV Diagnostics Market Segment Analysis

-

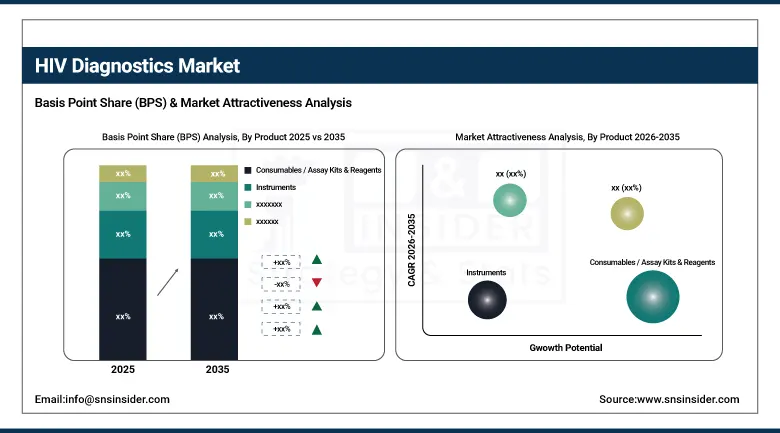

By Product, the consumables segment dominated the market with approximately 45.5% share in 2025, while the instruments segment is the fastest growing.

-

By Test Type, the monitoring tests segment dominated the market with approximately 38% share in 2025, while the early infant diagnosis tests segment is the fastest growing.

-

By End User, the diagnostic laboratories segment dominated the market with approximately 52% share in 2025, while the home care settings/self-testing segment is the fastest growing.

By Product, consumables dominate, instruments grow fastest

Consumables retained the dominant product position with approximately 45.5% of the HIV diagnostics market in 2025. HIV diagnostic consumables’ commercial primacy reflects the recurring purchase model whose test kit, reagent, and assay consumable replenishment creates consistent per-laboratory and per-hospital commercial relationships that sustain above-average revenue visibility. Each HIV testing programme creates structured consumable procurement whose volume scales with testing throughput. Government-funded HIV screening programmes, PEPFAR’s antiretroviral therapy monitoring infrastructure, and national blood safety programmes collectively create institutional consumable procurement whose policy motivation sustains demand through healthcare budget cycle variation.

Instruments are the fastest-growing product because the progressive automation of HIV diagnostic testing in both high-income and emerging market laboratory settings is creating capital equipment procurement that replaces manual ELISA and rapid test procedures with automated analyzer platforms whose throughput, reproducibility, and quality documentation capability improve laboratory operational economics. Each laboratory that installs an automated HIV testing platform creates a multi-year instrument service relationship whose reagent consumption sustains commercial revenue across the instrument’s operational lifetime. WHO-prequalified automated HIV testing platforms whose procurement through PEPFAR, Global Fund, and USAID creates structured emerging market instrument adoption sustains instruments’ fastest-growing product status.

By Test Type, monitoring tests dominate, early infant diagnosis grows fastest

Monitoring tests retained the dominant test type position with approximately 38% of the HIV diagnostics market in 2025. The 39 million people living with HIV globally whose antiretroviral therapy management requires regular viral load quantification and CD4 cell count monitoring creates the most commercially consistent and highest-volume HIV diagnostic testing category. Each HIV-positive person on ART creates a minimum of two viral load tests per year whose aggregate across the global ART patient population creates hundreds of millions of annual viral load test procurement.

Early infant diagnosis is the fastest-growing test type because the Prevention of Mother-to-Child Transmission programme’s expansion across sub-Saharan Africa and Asia Pacific is creating growing demand for NAT-based HIV DNA testing in HIV-exposed infants whose positive serological antibody status from maternal transfer cannot distinguish active HIV infection from passive antibody transfer. Each newborn of an HIV-positive mother creates an EID testing requirement at 4-6 weeks, 9 months, and 18 months whose three-point testing creates per-infant procurement that compounds with the growing PMTCT programme coverage in high-HIV-burden countries.

By End User, diagnostic labs dominate, home care grows fastest

Diagnostic laboratories retained the dominant end-user position with approximately 52% of the HIV diagnostics market in 2025. The centralized high-volume laboratory testing infrastructure’s role in HIV screening, confirmatory testing, blood safety testing, and viral load monitoring creates the most commercially significant aggregate HIV diagnostic procurement volume. Each national HIV testing programme, blood bank system, and ART clinic network creates laboratory testing procurement whose institutional scale sustains consistent commercial relationships with major HIV diagnostic suppliers.

Home care settings and self-testing is the fastest-growing end-user category because the extraordinary commercial momentum of HIV self-test adoption is creating a new testing channel whose growth compounds with regulatory approvals, stigma reduction, and price accessibility improvements. Each country that approves over-the-counter HIV self-test sales creates a retail and online distribution channel whose reach substantially exceeds the clinic testing network, potentially identifying previously undiagnosed HIV infections in populations whose perceived stigma creates barriers to facility-based testing.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

South Africa |

44.2% |

|

Latin America |

Brazil |

44.2% |

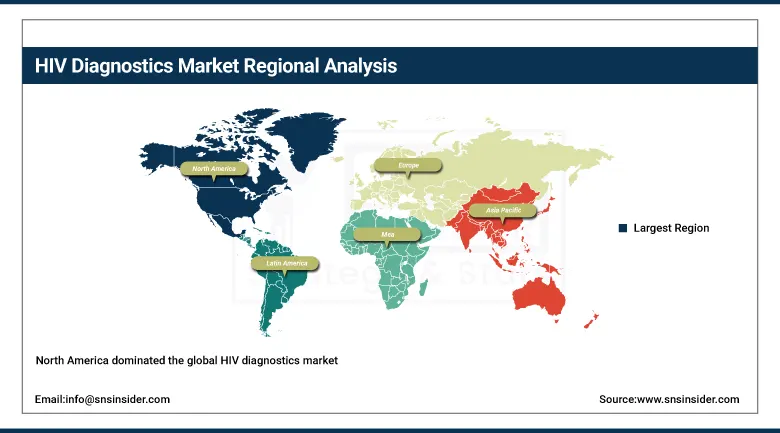

North America HIV Diagnostics Market Insights

North America dominated the global HIV diagnostics market in 2025 as the highest healthcare expenditure region with advanced diagnostic infrastructure. The United States accounts for approximately 87.4% of North American revenues through Abbott, Hologic, Siemens Healthineers, and OraSure Technologies’ commercial operations. CDC’s Ending the HIV Epidemic in the U.S. initiative’s targeted screening investment in high-burden jurisdictions, HRSA’s Ryan White programme’s ART monitoring infrastructure, and the advanced laboratory network’s fourth-generation testing adoption collectively sustain the U.S. as the most commercially sophisticated HIV diagnostics market globally on a per-capita basis.

Canada contributes approximately 12.6% of North American revenues through its public health HIV testing programme, the laboratory network’s automated HIV testing platform investment, and the growing at-home testing market whose regulatory expansion creates new procurement channels.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe HIV Diagnostics Market Insights

Europe is a technically sophisticated HIV diagnostics market where European Centre for Disease Prevention and Control’s HIV testing guidelines, the European AIDS Clinical Society’s management recommendations, and ECDC’s HIV testing week campaign create structured institutional procurement. Germany accounts for approximately 22.3% of European revenues through its advanced clinical laboratory infrastructure, the pharmaceutical sector’s HIV research programme, and Siemens Healthineers’ domestic market presence.

The United Kingdom, France, and Spain are significant secondary markets where national HIV prevention programmes, sexual health clinic testing infrastructure, and PrEP programme HIV monitoring requirements create consistent procurement. WHO Europe’s HIV testing coverage targets create policy motivation that sustains institutional testing programme investment.

Asia Pacific HIV Diagnostics Market Insights

Asia Pacific is the fastest-growing regional HIV diagnostics market, driven by the rising HIV burden across India, China, Thailand, Vietnam, and the Philippines, growing healthcare infrastructure investment enabling laboratory testing expansion, and PEPFAR and Global Fund programme support creating point-of-care diagnostic procurement. China accounts for approximately 44.8% of Asia Pacific revenues through its expanding HIV testing programme, the national laboratory network’s testing infrastructure, and the government’s HIV prevention programme investment.

India represents the most commercially dynamic emerging market within Asia Pacific where the National AIDS Control Organization’s integrated counselling and testing center network creates structured point-of-care and laboratory HIV testing procurement whose government programme scale sustains consistent commercial demand that international diagnostic suppliers serve through domestic distribution partnerships.

MEA & Latin America HIV Diagnostics Market Insights

Sub-Saharan Africa represents the most commercially significant HIV diagnostics demand concentration globally with South Africa leading MEA revenues at approximately 44.2% through the world’s largest HIV-positive national population whose ART programme monitoring creates extraordinary viral load and CD4 testing volume. PEPFAR and Global Fund investments in sub-Saharan African HIV diagnostic infrastructure create structured public health procurement whose institutional scale sustains the most commercially significant emerging market HIV diagnostic demand of any regional market globally.

Brazil leads Latin American revenues at approximately 44.2% through its comprehensive national HIV testing programme, the Ministry of Health’s universal ART provision creating monitoring test demand, and the federal government’s domestic diagnostic industry support whose combined commercial environment sustains consistent HIV diagnostic procurement growth.

Market Dynamics

Growth Drivers: Rising global HIV burden creating monitoring test demand and point-of-care testing technology democratizing access

The global HIV burden’s persistence, with approximately 39 million people living with HIV and approximately 1.3 million new infections annually, creates the most structurally certain HIV diagnostics demand driver. Each person living with HIV requires lifelong viral load monitoring whose testing frequency creates per-patient annual diagnostic procurement that compounds with the global ART patient population’s progressive expansion. UNAIDS’ 95-95-95 targets, whose goal of 95% of HIV-positive people knowing their status, 95% on ART, and 95% achieving viral suppression, creates structured global public health investment in HIV diagnostic infrastructure whose PEPFAR and Global Fund procurement translates into commercial market demand.

Point-of-care testing technology democratization is creating new HIV diagnostic market development in previously underserved settings. Rapid antigen/antibody combination tests, GeneXpert HIV VL’s viral load quantification at point-of-care, and at-home self-test devices collectively create testing capability deployment beyond the laboratory infrastructure whose geographic restriction previously limited HIV diagnostic market penetration in resource-limited settings.

Restraints: High cost of molecular testing platforms in resource-limited settings and HIV testing stigma reducing testing uptake

Nucleic acid testing platforms’ instrument and reagent cost creates adoption barriers in resource-limited healthcare settings whose per-test cost economics require donor programme subsidy to achieve procurement volumes that sustain commercial viability. Each PEPFAR or Global Fund programme funding reduction creates procurement uncertainty that moderates testing infrastructure expansion investment in high-HIV-burden developing country markets whose domestic healthcare budget cannot substitute for international donor support.

HIV testing stigma remains a persistent barrier to testing uptake whose commercial consequence is reduced testing volume below the epidemiologically indicated testing rate that national HIV programme monitoring targets define.

Opportunities: HIV self-testing market expansion and PEPFAR monitoring test infrastructure investment

HIV self-testing market expansion represents the most commercially dynamic near-term growth opportunity whose regulatory approval pipeline, price accessibility improvement, and national programme integration creates new testing channel procurement beyond the clinical facility setting. Each country that launches a national HIV self-test programme creates procurement through both public programme distribution and retail pharmacy channels whose combined scale creates commercial market development. Oraquick Advance’s OTC FDA approval precedent and WHO’s self-testing guidelines endorsement create the regulatory and policy framework that sustains national programme adoption globally.

PEPFAR’s viral load testing scale-up investment creates the most commercially certain near-term monitoring test procurement opportunity. PEPFAR’s USD 6+ billion annual programme investment, whose viral load monitoring component creates structured procurement for high-volume automated viral load platforms and point-of-care alternatives, sustains commercial demand in the 50+ countries where PEPFAR supports HIV programmes.

Recent Developments:

-

2026: OraSure Technologies advanced HIV self-testing portfolio expansion, increasing accessibility of at-home diagnostics across emerging and high-risk markets.

-

2025: Abbott expanded next-generation HIV Ag/Ab diagnostic platforms, improving early detection sensitivity and reducing diagnostic window period globally.

-

2025: Roche enhanced molecular HIV viral load testing solutions, supporting higher-throughput laboratories and strengthening global infectious disease monitoring networks.

HIV Diagnostics Market key players are:

-

Abbott Laboratories

-

F. Hoffmann-La Roche Ltd. (Roche Diagnostics)

-

Siemens Healthineers AG

-

Danaher Corporation

-

Thermo Fisher Scientific Inc.

-

bioMérieux SA

-

Becton, Dickinson and Company

-

Hologic Inc.

-

Qiagen N.V.

-

Bio-Rad Laboratories Inc.

-

OraSure Technologies Inc.

-

Grifols S.A.

-

Trinity Biotech plc

-

Chembio Diagnostics (BioSynex)

-

Wondfo Biotech Co., Ltd.

-

Getein Biotech Inc.

-

Meril Diagnostics Pvt. Ltd.

-

BioLytical Laboratories Inc.

-

Sysmex Corporation

-

AccuBioTech Co., Ltd.

HIV Diagnostics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.27 Billion |

| Market Size by 2035 | USD 2.10 Billion |

| CAGR | CAGR of 5.10% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Consumables/Assay Kits & Reagents, Instruments, Software & Services) • By Test Type (Antibody Tests/Screening, Viral Load Tests, CD4 Count Tests, Early Infant Diagnosis Tests, Confirmatory Tests/Western Blot & ELISA, Rapid/Point-of-Care Tests) • By End User (Diagnostic Laboratories, Hospitals & Clinics, Home Care Settings/Self-Testing, Blood Banks, Academic & Research Institutes) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories, F. Hoffmann-La Roche Ltd. (Roche Diagnostics), Siemens Healthineers AG, Danaher Corporation, Thermo Fisher Scientific Inc., bioMérieux SA, Becton, Dickinson and Company, Hologic Inc., Qiagen N.V., Bio-Rad Laboratories Inc., OraSure Technologies Inc., Grifols S.A., Trinity Biotech plc, Chembio Diagnostics (BioSynex), Wondfo Biotech Co., Ltd., Getein Biotech Inc., Meril Diagnostics Pvt. Ltd., BioLytical Laboratories Inc., Sysmex Corporation, AccuBioTech Co., Ltd. |

Frequently Asked Questions

The market was valued at USD 1.27 Billion in 2025.

Rising global HIV burden with approximately 39 million people living with HIV requiring lifelong viral load and CD4 monitoring.

Consumables dominated the market with approximately 45.5% share in 2025.

North America dominated the HIV Diagnostics Market in 2025.

Get in Touch