Hydraulic Hammer Market Report Scope & Overview:

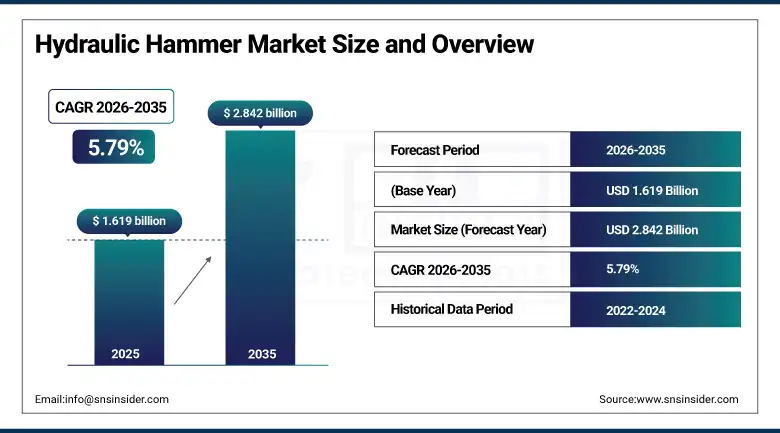

Hydraulic Hammer Market was valued at USD 1.619 billion in 2025 and is expected to reach USD 2.842 billion by 2035, growing at a CAGR of 5.79% from 2026–2035.

The hydraulic hammer market is experiencing consistent growth due to the increasing global infrastructure development, urban redevelopment initiatives, mining activities, and growing need for effective demolition equipment. The hydraulic hammer, otherwise known as a hydraulic breaker, is a common tool that is widely used in construction, quarrying, mining, tunneling, and road construction for demolition of rocks, concrete, asphalt, and reinforced materials. Increasing investment in transportation infrastructure development, smart city developments, and commercial constructions is boosting demand for high-efficiency hydraulic demolition tools on a global level. Moreover, increasing mining activities for necessary minerals and aggregates used by the renewable energy industry and infrastructure are also helping in boosting the market. Advanced technological solutions like automatic lubrication systems, vibration dampening technology, noise dampening technology, energy efficiency, and IoT based monitoring system are improving the performance of the machinery, which helps in the growth of the market till 2035.

The 5.79% CAGR of the hydraulic hammers market from 2026 to 2035 is based on the structural certainty of demand resulting from global infrastructure spending, which exceeds USD 12.1 trillion per year in 2025 and is projected to grow to USD 16 to 17 trillion by 2030, representing the largest and most extended period of sustained demand for rock and concrete-breaking tools seen in the history of the market. The development and introduction of the HB01 and HB02 hydraulic hammers for compact excavators by Volvo CE in March 2025 and the PC220LCi-12 excavator with the latest generation of Intelligent Machine Control by Komatsu in April 2025 at Bauma 2025 indicate continued innovation in the hydraulic hammer market.

Market Size and Forecast

-

Market Size in 2026E: USD 1.71 Billion

-

Market Size by 2035: USD 2.842 Billion

-

CAGR 2026-2035: 5.79%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Hydraulic Hammer Market - Request Free Sample Report

Hydraulic Hammer Market Trends

-

The increasing electrification of hydraulic hammers is aiding in the implementation of zero-emissions in demolition and mining activities, especially those performed in urban construction and underground settings that have tight emissions and ventilation control policies worldwide.

-

The increased use of Internet-of-Things (IoT)-based monitoring solutions is facilitating real-time monitoring of equipment diagnostics, tool wear, preventive maintenance, and analytics in construction and mining equipment.

-

The rising need for quiet and vibration-resistant hydraulic hammers is boosting their usage in urban demolition and road construction applications with occupational safety and noise control policies.

-

Growing use of hydraulic hammers in renewable energy infrastructure projects is supporting excavation, rock breaking, and foundation preparation activities for wind farms, solar installations, and transmission infrastructure development.

-

Growing aftermarket services for hydraulic hammers are creating recurring income through maintenance, replacement of chisels, lubrication services, nitrogen filling, and repairs for the huge number of installed equipment in the world.

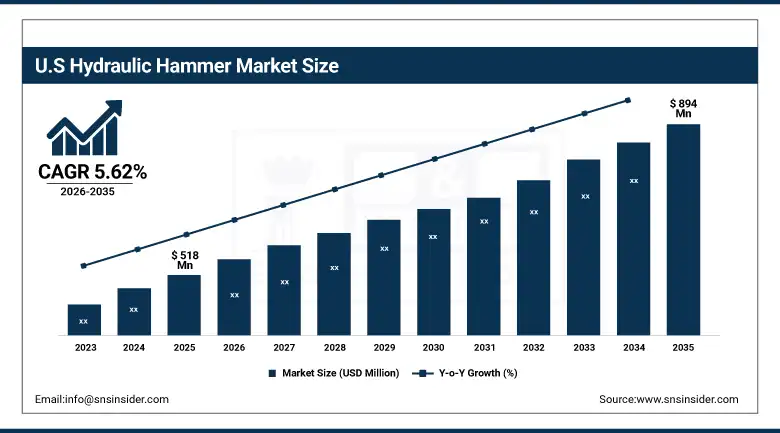

The U.S. Hydraulic Hammer Market Size Outlook

The U.S. Hydraulic Hammer Market was valued at approximately USD 518 million in 2025 and is expected to reach approximately USD 894 million by 2035, growing at a CAGR of 5.62% during 2026–2035.

The USA is considered the largest market for hydraulic hammers around the world due to the huge number of infrastructure renovation projects, massive urban renewal projects, and increased demand from the construction and demolition industries. Growing investments in the areas of road renovation, bridge construction, tunnel construction, and infrastructure renovations are boosting the application of hydraulic hammers in concrete demolition, rock excavation, and demolition operations. Moreover, ongoing mining activities in various minerals such as coal, copper, gold, and other essential minerals are sustaining the demand for hydraulic breakers in quarrying and rock crushing operations. The Bipartisan Infrastructure Law and other federal infrastructure investments are expected to drive the growth of market in the USA up to 2035.

In March 2025, Volvo CE launched the HB01 and HB02 hydraulic hammers for 1 to 3-tonne compact excavators, delivering stable impact performance, reduced noise, and greater precision for city, indoor, and utility applications, with a compact plug-and-play design and low service demand improving uptime. This product launch exemplifies the compact hydraulic hammer innovation addressing the growing urban infrastructure maintenance market where full-size hydraulic hammers cannot access the confined workspace of urban utility trenching, indoor demolition, and underground construction that represent a growing share of U.S. hydraulic hammer demand through the forecast period.

Hydraulic Hammer Market Segment Analysis

-

By Product Type, heavy-duty hydraulic hammers dominated the market in 2025; utility hydraulic hammers are the fastest-growing type.

-

By Operating Weight, the 500 to 1,000 kg segment dominated; the above 1,000 kg class is growing.

-

By Application, construction and demolition dominated with the largest revenue share in 2025; mining is the fastest-growing application.

-

By Sales Channel, OEM accounted for approximately 67.8% of market revenues in 2025; aftermarket is the fastest-growing channel at approximately 5.8 to 6.3% CAGR.

By product type, heavy-duty dominates, utility grows fastest

Heavy hydraulic hammers were the main types dominating the market in 2025 because of their widespread application in large-scale mining, quarrying, demolition, tunneling, and construction operations needing maximum impact energy and maximum productivity. Heavy hydraulic hammers are used for breaking reinforced concrete, hard rock, and quarry rocks in extreme conditions, and they are attached to large excavators for these purposes. Leading companies have been concentrating on increasing the durability and impact energy of heavy hydraulic hammers.

The utility hydraulic hammer is expected to experience the highest growth rate up to 2035 due to its rising use in applications such as urban construction, utility trenching, interior demolition, and infrastructure maintenance. The growing availability of rented equipment coupled with the rising demand for compact demolition equipment is fueling the growth of the utility hydraulic hammer market.

By application, construction and demolition dominates, mining grows fastest

Construction and demolition dominated the market in 2025 due to extensive demand from urban redevelopment, infrastructure rehabilitation, road maintenance, foundation excavation, and reinforced concrete demolition activities worldwide. The hydraulic hammer finds application in demolishing structures made of concrete, asphalt, bridges, and rock surfaces. The growth in investment in construction activities in the world coupled with the emergence of smart cities has been key in driving demand within the industry.

Mining is projected to witness the fastest growth through 2035 driven by rising global investments in critical mineral extraction including copper, lithium, cobalt, nickel, and rare earth elements required for renewable energy and electric vehicle production. Hydraulic hammers are increasingly utilized in quarrying, underground mining, tunnel development, and secondary rock breaking operations requiring high-impact and precision rock fragmentation solutions.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82% |

|

Europe |

Germany |

29% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

Saudi Arabia |

29% |

|

Latin America |

Brazil |

43% |

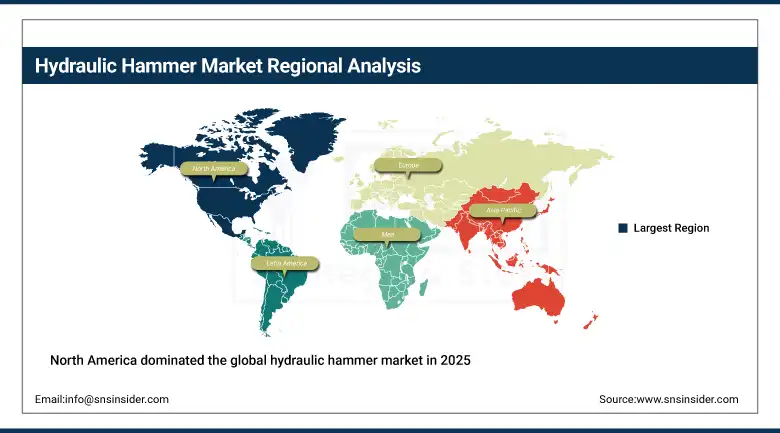

North America Hydraulic Hammer Market Insights

North America dominated the global hydraulic hammer market in 2025, led by the United States which accounted for approximately 82% of North American revenues at USD 518 million. U.S. market leadership is driven by the Bipartisan Infrastructure Law's multi-year construction programme, the most extensive urban demolition and renewal market of any developed economy, and the largest mining industry in the Western Hemisphere. The U.S. rental equipment market's integration of hydraulic hammers as standard fleet items across national rental companies including United Rentals, Sunbelt Rentals, and HERC Holdings provides broad market access for contractors of all sizes.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Hydraulic Hammer Market Insights

Asia Pacific is the fastest-growing regional hydraulic hammer market, driven by China's continued infrastructure construction including Belt and Road Initiative projects, India's National Infrastructure Pipeline investment programme, and Southeast Asia's rapid urban development and industrial expansion. China leads Asia Pacific with approximately 44% of regional revenues through its world-largest construction equipment market and mining industry, combined with a mature domestic hydraulic hammer manufacturing industry including Soosan's China operations and multiple domestic manufacturers. India's Smart Cities Mission and ambitious national highway expansion programme are creating growing hydraulic hammer demand.

Europe Hydraulic Hammer Market Insights

Europe represents a technically sophisticated market anchored by Germany, France, and the Nordic countries' construction and mining sectors, combined with the European headquarters of leading hydraulic hammer manufacturers including Atlas Copco, Sandvik, Montabert, and Rammer that drive product technology development. European environmental regulations driving urban demolition noise and emission restrictions are creating particular demand for noise-reduced and electric hydraulic hammer technology that these manufacturers are pioneering in their European home market applications.

Latin America and MEA Hydraulic Hammer Market Insights

Latin America and MEA are growing markets driven by mining expansion and infrastructure development. Brazil takes the lead in Latin American earnings with its mining industry as well as infrastructure construction investments, whereas the copper mining activities of Chile and Peru generate considerable demands for hydraulic hammers in secondary breaking and tunnel construction. The demand for MEA is due to the large infrastructure projects in Saudi Arabia like NEOM and Vision 2030, which involve huge rock-breaking and demolition tasks along with increased mining in Africa.

Market Dynamics

Growth Drivers: Global infrastructure expansion and critical minerals mining driving hydraulic hammer demand

The market is primarily driven by rising global infrastructure investment, rapid urban redevelopment, and expanding mining activities worldwide. The massive investments made in roadways, bridges, tunnels, railway networks, smart city initiatives, and infrastructure projects have resulted in increased demand for hydraulic breakers used for demolition, excavating, and rock breaking purposes. Apart from that, the rising critical minerals mining for the production of electric cars, renewable energy systems, and batteries has fueled the adoption of hydraulic hammers in quarrying and mining applications. Some of the latest technologies incorporated in the industry include electric hydraulic breakers, intelligent machine control, IoT-based monitoring solutions, noise reduction techniques, and urban demolition machines. The constant upgrading of machinery and growing infrastructure rehabilitation works will drive future growth until 2035.

Restraints: High equipment costs and strict urban noise regulations restraining market expansion

A significant restraint on the hydraulic hammer market is the substantial capital cost of new hydraulic hammer equipment ranging from USD 5,000 for small utility hammers through USD 200,000 or more for large mining-class breakers, combined with the carrier excavator that must be sized and configured for hydraulic hammer attachment, creating total capital investment requirements that limit adoption among small contractors who do not have the equipment fleet scale to justify dedicated hydraulic hammer ownership. Given that the hydraulic hammer industry is affected by the cyclic nature of construction and mining investments, any economic slowdown, fall in commodity prices, and decrease in infrastructure spending will result in steep declines in demand, which cannot be completely covered by equipment replacements.

Opportunities: Electric hydraulic breakers and predictive maintenance solutions creating strong market opportunities

The hydraulic hammer market offers significant growth potential owing to increasing use of electric hydraulic breakers, growing equipment rental markets, and IoT-based predictive maintenance solutions. Electric hydraulic hammers have seen an increase in demand for their use in urban demolition, indoor construction, and underground mining activities because of their low emission levels, low noise pollution, and adherence to stringent environmental laws. Increasing penetration of rental equipment in developing countries is also providing entry into the market for contractors looking for more economical ways of operating without owning equipment. Furthermore, companies are now offering IoT-based monitoring services and predictive maintenance solutions, which provide benefits such as real-time monitoring, preventive maintenance, minimal downtime, and low operational expenses.

Recent Developments:

-

2026: Epiroc AB expanded its electric hydraulic breaker portfolio with new zero-emission demolition solutions designed for urban infrastructure projects and underground mining applications requiring reduced noise and emissions.

-

2026: Komatsu Ltd. introduced advanced AI-integrated hydraulic hammer control systems for intelligent excavators, improving impact precision, fuel efficiency, and predictive maintenance capabilities across heavy construction operations.

-

2026: Volvo Construction Equipment AB launched next-generation compact hydraulic hammers optimized for mini-excavators and urban demolition projects, featuring enhanced vibration reduction and IoT-enabled performance monitoring systems.

Hydraulic Hammer Companies are:

-

Epiroc AB

-

Sandvik AB

-

Atlas Copco AB

-

Montabert SAS

-

Furukawa Rock Drill Co. Ltd.

-

Soosan Heavy Industries Co. Ltd.

-

NPK Construction Equipment Inc.

-

EVERDIGM Co. Ltd.

-

MKB Brekers BV

-

MSB Corporation

-

Rammer

-

Toku Pneumatic Co. Ltd.

-

Caterpillar Work Tools

-

Komatsu Ltd.

-

Volvo Construction Equipment AB

-

Hyundai Construction Equipment Co. Ltd.

-

Hitachi Construction Machinery Co. Ltd.

-

JCB Ltd.

-

Chicago Pneumatic

-

Bobcat Co.

Hydraulic Hammer Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.619 Billion |

| Market Size by 2035 | USD 2.842 Billion |

| CAGR | CAGR of 5.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Utility, Heavy-Duty) • By Operating Weight (Below 500 kg, 500 to 1,000 kg, Above 1,000 kg) • By Application (Construction and Demolition, Road Building and Rehabilitation, Mining, Others) • By End-User Industry (Construction Companies, Mining Companies, Infrastructure Development, Others) • By Sales Channel (OEM, Aftermarket) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Epiroc AB, Sandvik AB, Atlas Copco AB, Montabert SAS, Furukawa Rock Drill Co. Ltd., Soosan Heavy Industries Co. Ltd., NPK Construction Equipment Inc., EVERDIGM Co. Ltd., MKB Brekers BV, MSB Corporation, Rammer, Toku Pneumatic Co. Ltd., Caterpillar Work Tools, Komatsu Ltd., Volvo Construction Equipment AB, Hyundai Construction Equipment Co. Ltd., Hitachi Construction Machinery Co. Ltd., JCB Ltd., Chicago Pneumatic, Bobcat Co. |

Frequently Asked Questions

Mining is the fastest-growing application through 2035.

North America dominated the market in 2025, led by the United States with the Bipartisan Infrastructure Law driving sustained construction programme demand, the most extensive urban demolition and infrastructure renewal market of any developed economy, and the largest mining industry in the Western Hemisphere, combined with the most active hydraulic hammer rental market providing broad contractor access to hydraulic breaking capability.

Heavy-Duty Hydraulic Hammers dominated the market in 2025.

Global infrastructure investment exceeding USD 12.1 trillion annually creating sustained rock and concrete breaking demand across new construction in emerging economies and ageing infrastructure rehabilitation in developed economies, combined with critical minerals mining expansion for EV and clean energy technology manufacturing requiring hydraulic hammer applications in secondary breaking, tunnel development, and quarrying operations.

The market was valued at USD 1.619 billion in 2025.

The Hydraulic Hammer Market is expected to grow at a CAGR of 5.79% from 2026 to 2035.

Get in Touch