Hydrophobic Coating Market Report Scope & Overview:

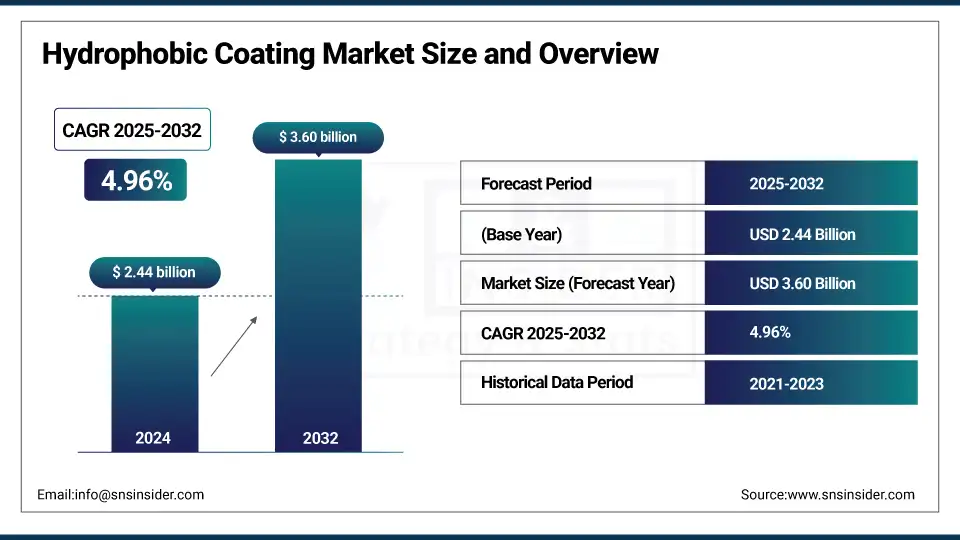

The Hydrophobic Coating market size was valued at USD 2.44 billion in 2024 and is expected to reach USD 3.60 billion by 2032, growing at a CAGR of 4.96% over the forecast period of 2025-2032.

The hydrophobic coating market demand is fueled by automotive surface coatings that enhance durability and self-cleaning coatings for solar panels and facades. Nanocoatings offering anti-corrosion coatings are being adopted in marine sectors, while hydrophobic coatings companies like 3M launched advanced surface treatments reducing maintenance. Water-repellent coatings for electronics and textiles show rising popularity within functional coatings.

To Get more information On Hydrophobic Coating Market - Request Free Sample Report

U.S. National Renewable Energy Laboratory reports a 35% drop in ice adhesion, and EPA notes a 20% decline in slip incidents using protective coatings. Nippon Paint’s Q1 hydrophobic coating market size update shows a 5% rise, while PPG Industries’ release highlights hydrophobic coating market growth and a 32% hydrophobic coating market share in automotive exteriors. Hydrophobic coating market trends show demand for transparent coatings and oil-resistant coatings, supported by recent hydrophobic coating market analysis.

Market Dynamics:

Drivers:

-

Integration Of Water-Repellent Coatings In Solar Panels Supports Energy Efficiency Goals

Hydrophobic coating market growth benefits from rising adoption of water-repellent coatings in photovoltaic modules. The U.S. Department of Energy’s Solar Energy Technologies Office noted a 4% efficiency gain on panels using hydrophobic layers that reduce dust accumulation. This trend aligns with expanding renewable installations and demand for functional coatings that combine anti-corrosion coatings and self-cleaning coatings, ultimately increasing the lifespan of energy assets and supporting hydrophobic coating market size across utility-scale and commercial solar projects.

-

Emergence Of Transparent Coatings For Automotive Displays And Heads-Up Systems

Hydrophobic coating market trends highlight rising demand for transparent coatings used in digital dashboards and heads-up displays to repel moisture and smudges. In 2024, Continental AG unveiled display panels featuring proprietary hydrophobic coatings that improve visibility by 15% under humid conditions. These coatings address consumer comfort while aligning with broader growth in automotive surface coatings, supporting hydrophobic coating market share gains as automakers focus on connected, touch-enabled cabin technology integrated into premium vehicle segments.

Restraints:

-

Complex Regulatory Pathways For Anti-Corrosion Coatings Slow Product Launches

Hydrophobic coating market share in heavy industries can be limited by strict regulatory reviews. The European Chemicals Agency’s latest 2024 directive added extended approval timelines for new anti-corrosion coatings containing certain fluorinated compounds. Companies must increase testing to demonstrate environmental safety, lengthening time-to-market and adding compliance costs. This barrier particularly affects SMEs, slowing hydrophobic coating market growth in sectors like marine and offshore that rely heavily on advanced protective coatings to meet durability standards.

Segmentation Analysis:

By Product Type

Fluoropolymer-based coatings held a dominant Hydrophobic Coating Market share of 37.2% in 2024 due to their exceptional chemical resistance, durability, and corrosion protection. PTFE formulations, in particular, are widely used in automotive and industrial equipment. The U.S. Environmental Protection Agency highlighted that these coatings reduce corrosion-related failures by 25%, encouraging adoption in pipelines and machinery. Their superior performance in anti-corrosion and self-cleaning applications ensures sustained preference, supporting the Hydrophobic Coating Market Share in industrial and high-performance sectors.

Nanoparticle-based coatings are the fastest growing with the highest CAGR of 5.54% during the forecast period over 2025 to 2032, driven by their application in silica nanoparticle thin films for touchscreens and photovoltaic glass. The U.S. Department of Energy reported a 3% increase in solar panel transmittance using nanocoatings, improving energy yield. Growing adoption of functional and water-repellent coatings across electronics and renewable energy sectors is supporting accelerated Hydrophobic Coating Market Growth.

By Functionality

Anti-corrosion coatings held a dominant Hydrophobic Coating Market share of 41.8% in 2024 due to their effectiveness in prolonging asset life under harsh conditions. Marine-grade anti-corrosion layers are widely used in offshore and heavy industries. The U.S. Department of Transportation noted that protective coatings on steel bridges reduced maintenance costs by 30%. Their ability to protect industrial infrastructure and machinery aligns with growing adoption of protective coatings, sustaining Hydrophobic Coating Market Size in critical sectors.

Self-cleaning coatings are the fastest growing with the highest CAGR of 5.6% during the forecast period over 2025 to 2032, driven by photocatalytic glass coatings for building facades and solar panels. The U.S. General Services Administration reported that these coatings reduced manual cleaning by 25%. Growing preference for energy-efficient, low-maintenance solutions and water-repellent coatings ensures widespread use, supporting Hydrophobic Coating Market Trends across architectural and renewable energy applications.

By Material

Fluoropolymers held a dominant Hydrophobic Coating Market share of 52.5% in 2024 due to their exceptional chemical inertness and long-term performance. PTFE and PVDF blends are preferred for automotive, aerospace, and industrial pipelines. The U.S. Department of Energy highlighted their ability to minimize maintenance downtime in energy infrastructure. Their extensive use in anti-corrosion and protective coatings across demanding sectors supports sustained Hydrophobic Coating Market Share.

Fluoroalkylsilanes are the fastest growing with the highest CAGR of 5.49% during the forecast period over 2025 to 2032, driven by C6-based formulations offering hydrophobicity and environmental compliance. The U.S. Environmental Protection Agency reported increased registration of C6 coatings for electronics and construction. Their adoption in transparent and advanced surface treatments supports functional coating applications, ensuring accelerated Hydrophobic Coating Market Growth.

By Substrate Type

Glass held a dominant Hydrophobic Coating Market share of 32.7% in 2024 due to architectural glazing applications and solar panels. Hydrophobic coatings reduce soiling losses on PV modules by 3%, as reported by the U.S. National Renewable Energy Laboratory. The use of water-repellent and self-cleaning coatings improves maintenance efficiency and durability. These advantages reinforce Hydrophobic Coating Market Size leadership in construction and renewable energy sectors, supporting increased adoption of transparent coatings.

Polymers are the fastest growing with the highest CAGR of 5.45% during the forecast period over 2025 to 2032, driven by smartphone housings and consumer electronics applications. The National Institute of Standards and Technology highlighted polymer-compatible hydrophobic coatings improving scratch resistance and durability in 2024. Adoption in oil-resistant coatings and functional coatings enhances consumer convenience, supporting accelerated Hydrophobic Coating Market Growth in electronic and high-value polymer applications.

By Fabrication Method

Sol-gel process held a dominant Hydrophobic Coating Market share of 34.5% in 2024 due to low-temperature processing for glass and ceramics. Silica sol-gel coatings improve solar panel transmittance by 2%, according to the U.S. Department of Energy. Cost efficiency and versatility in applying protective and functional coatings across architectural and industrial substrates reinforce Hydrophobic Coating Market Share. This method continues to lead due to wide applicability in durable water-repellent coatings.

Chemical vapor deposition is the fastest growing with the highest CAGR of 5.87% during the forecast period over 2025 to 2032, driven by thin-film electronics coatings. The National Institute of Standards and Technology reported successful application on flexible displays, improving lifespan by 10%. Integration of oil-resistant and functional coatings in advanced devices ensures increased adoption, supporting Hydrophobic Coating Market Growth in consumer electronics and high-performance substrates.

By End-Use Industry

Automotive & transportation held a dominant Hydrophobic Coating Market share of 35.8% in 2024 due to exterior panel coatings reducing dirt accumulation and corrosion. Nissan tests showed 2% drag reduction in simulated rain with hydrophobic coatings, improving fuel efficiency. The combination of anti-corrosion and self-cleaning coatings supports maintenance reduction and lifecycle cost benefits, reinforcing Hydrophobic Coating Market Size leadership in the automotive sector.

Electronics & semiconductors are the fastest growing with the highest CAGR of 5.49% during the forecast period over 2025 to 2032, driven by hydrophobic coatings for smartphone displays. The National Institute of Standards and Technology reported a 15% improvement in scratch resistance in coated devices in 2024. Increasing demand for transparent and oil-resistant coatings supports accelerated Hydrophobic Coating Market Growth across consumer electronics and semiconductor applications.

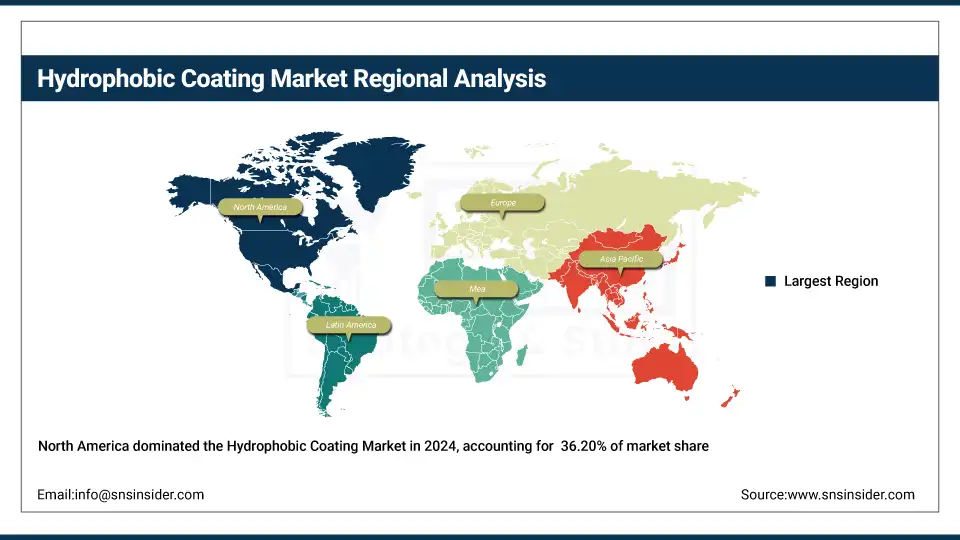

Regional Analysis

North America dominates the Hydrophobic Coating Market with 36.20% share, led by demand for advanced surface treatments in automotive surface coatings and aerospace. The US remains the key contributor, where the U.S. Department of Energy highlighted that oil-resistant coatings reduced equipment downtime by 15%, driving adoption. Canada’s investments in self-cleaning coatings for solar panels, reported by Natural Resources Canada, further push Hydrophobic Coating Market Growth. Strong R&D, consumer electronics expansion, and strict environmental policies reinforce regional leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific is the fastest-growing region with 5.31% CAGR, fueled by rapid adoption of nanocoatings in consumer electronics and renewable energy. China leads, as the Ministry of Industry and Information Technology reported water-repellent coatings reduced defects in smartphone production by 18%. Japan drives Hydrophobic Coating Market Growth through transparent coatings in solar panels and OLED screens. Expanding urbanization, cost-effective manufacturing, and demand for innovative protective coatings ensure this region’s dynamic surge.

Europe ranks third with 22.60% Hydrophobic Coating Market share, driven by functional coatings in automotive and building glass sectors. Germany leads, supported by Fraunhofer Institute’s research on anti-corrosion coatings that increase steel lifespan by 25%. France follows with rising protective coatings demand in luxury automotive brands, while Italy focuses on transparent coatings for architectural glass facades. Together, sustainability targets and EU-backed R&D ensure consistent Hydrophobic Coating Market Analysis growth across diverse industrial applications.

Key Players:

The major hydrophobic coating market competitors include 3M Company, AccuCoat Inc., Aculon Inc., Akzo Nobel N.V., Allegiance NanoSolutions, Artekya Teknoloji (Nasiol), BASF SE, Cytonix LLC, DryWired, Lotus Leaf Coatings Inc., Nanokote PTY Ltd., NEI Corporation, NeverWet LLC (Rust-Oleum / RPM International), Nippon Paint Holdings Co., Ltd., P2i Ltd., PPG Industries, Inc., Rust-Oleum (part of RPM International), SilcoTek Corporation, The Sherwin-Williams Company, and UltraTech International, Inc.

Recent Developments:

-

In December 2024, PPG Industries rolled out Sigma Contour Aqua-PU with LTA+ technology in Italy, featuring grease- and dirt-repellent properties ideal for educational environments.

-

In October 2024, P2i published “The Future of Electronics Protection” press release, showcasing conformal hydrophobic coatings that significantly improve device moisture reliability.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.44 billion |

| Market Size by 2032 | USD 3.60 billion |

| CAGR | CAGR of 4.96% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Product Type (Fluoropolymer-Based Coatings, Silane-Based Coatings, Nanoparticle-Based Coatings, Silicone-Based Coatings, Others) •By Functionality (Anti-microbial, Anti-icing/wetting, Anti-fouling, Anti-corrosion, Self-cleaning, Others) •By Material (Polysiloxanes, FluoroAlkylsilanes, Fluoropolymers, Others) •By Substrate Type (Metals, Glass, Concrete, Polymers, Ceramics, Others) •By Fabrication Method (Sol-Gel Process, Chemical Vapor Deposition (CVD), Physical Vapor Deposition (PVD), Electrochemical Deposition, Spray Coating, Dip Coating, Others) •By End-Use Industry (Automotive & Transportation, Aerospace & Defense, Building & Construction, Healthcare & Medical, Electronics & Semiconductors, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | 3M Company, AccuCoat Inc., Aculon Inc., Akzo Nobel N.V., Allegiance NanoSolutions, Artekya Teknoloji (Nasiol), BASF SE, Cytonix LLC, DryWired, Lotus Leaf Coatings Inc., Nanokote PTY Ltd., NEI Corporation, NeverWet LLC (Rust-Oleum / RPM International), Nippon Paint Holdings Co., Ltd., P2i Ltd., PPG Industries, Inc., Rust-Oleum (part of RPM International), SilcoTek Corporation, The Sherwin-Williams Company, UltraTech International, Inc. |

Frequently Asked Questions

Fluoropolymers dominate due to unmatched chemical resistance and durability, widely applied in automotive, aerospace, and industrial protective coatings.

Hydrophobic coatings protect screens against smudges, moisture, and scratches, improving device durability, visual clarity, and consumer satisfaction in premium electronics.

Nanocoatings enhance scratch resistance and transparency in smartphones and solar panels, driving demand as advanced surface treatments in high-tech applications.

Automotive surface coatings, building facades, electronics, and renewable energy sectors remain the largest consumers, supported by functional coatings that extend product lifespan.

Rising use of water-repellent coatings in automotive displays, solar panels, and marine anti-corrosion coatings significantly boosts hydrophobic coating market growth globally.

Get in Touch