Hysteroscopy Instrument Market Size Analysis:

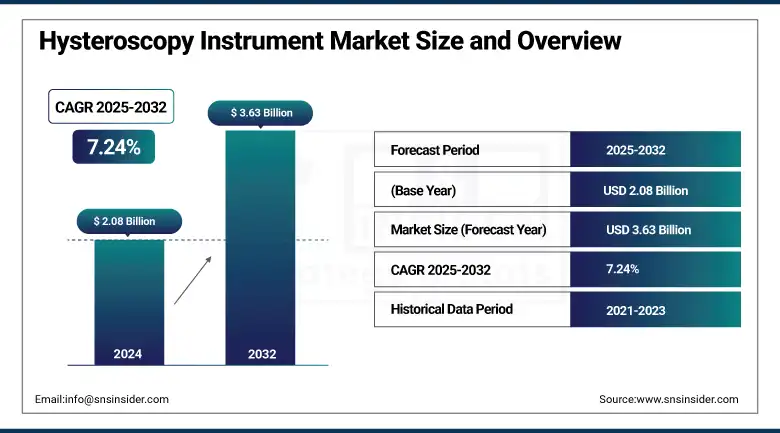

The Hysteroscopy Instrument Market size was valued at USD 2.08 billion in 2024 and is expected to reach USD 3.63 billion by 2032, growing at a CAGR of 7.24% over the forecast period of 2025-2032.

The hysteroscopy instrument market share is gaining significant traction owing to the growing prevalence of gynecological disorders like abnormal uterine bleeding, fibroids, and infertility. Between 7–10% of American women aged 15–44 suffer from infertility, according to the Centers for Disease Control and Prevention (CDC), which results in diagnostic procedures such as hysteroscopy. Technological development-tools miniaturization, and handheld hysteroscopy appliances have increased the success of procedures while increasing ambulatory devices. The single-use hysteroscopy instrument market is expanding with growing infection control concerns and cost consciousness in ambulatory surgical centers (over 60% of outpatient surgeries in the U.S.).

To Get more information On Hysteroscopy Instrument Market - Request Free Sample Report

For instance, the International Society for Gynecologic Endoscopy (ISGE) in 2024 also highlighted the need for training in office hysteroscopy with small and disposable instruments to improve accessibility in low-resource settings.

The global hysteroscopy instrument market will further be driven by the ever-widening healthcare spending around the world and favorable regulatory guidelines (such as ACOG’s recommendation of hysteroscopy for intrauterine pathology). Incidentally, the WHO database shows that rates of surgical procedures have continued to climb worldwide, suggesting that the procedural demand is increasing. The study by NIH also highlights the expansion of R&D in high-precision and flexible optics, capturing innovation. Further, investment in R&D for women’s health is increasing, as SWHR has recorded an upswing in funding for uterine health research in recent years, indicating sustained hysteroscopy instrument market growth. Growing levels of supply chain efficiency and strategic alliances among hysteroscopy instrument companies are also eliminating bottlenecks to production and speeding up U.S. hysteroscopy instrument market penetration.

For instance, research published in The Journal of Minimally Invasive Gynecology indicated that the trend in the direction of see-and-treat hysteroscopy procedures is successful in cutting down diagnostic-to-treatment time by more than 30%, which benefits the patients and is driving the hysteroscopy instrument market trends.

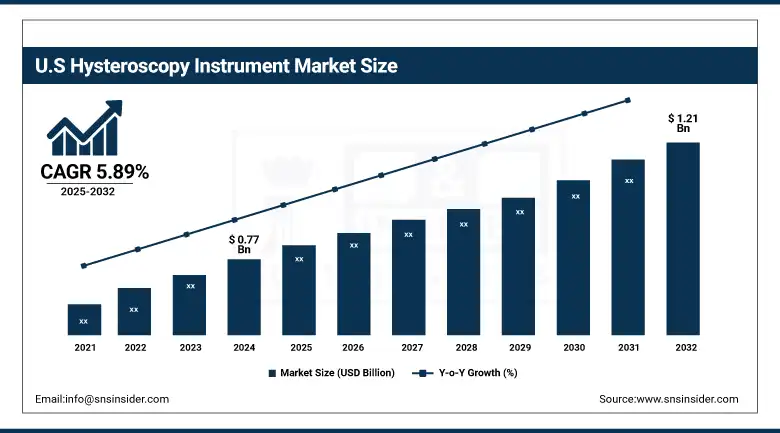

The U.S. hysteroscopy instrument market size was valued at USD 0.77 billion in 2024 and is expected to reach USD 1.21 billion by 2032, growing at a CAGR of 5.89% over the forecast period of 2025-2032

Hysteroscopy Instrument Market Dynamics:

Drivers:

-

Technological Innovation, Expanding Clinical Applications, and Regulatory Backing are Propelling Demand in the Hysteroscopy Instrument Market

Growth in the hysteroscopy instruments market is driven by the increasing adoption of hysteroscopy procedures, the growing global prevalence of gynecological diseases, and the increasing incidence of post-menopausal bleeding. The increase in endometrial pathologies (endometrial polyps and IUA) has resulted in an increased number of diagnostic and operative hysteroscopies. According to the American Journal of Obstetrics & Gynecology (2022), the 27% rise in outpatient hysteroscopies over the last 5 years is being attributed to advances in optics and energy systems. Secondly, the 510(k) clearances issued by the FDA for next-generation hysteroscopic systems have also been responsible for market growth.

Companies are spending billions of dollars on R&D, for instance, patent applications in the field of miniaturization of electrosurgical tools for hysteroscopy have increased by more than 15% from 2020 onwards (USPTO, 2023).

The pressure to use single-use devices continues to increase, particularly in ambulatory and rural practices and facilities, because of infection processes and sterilization considerations. Furthermore, programs like the National Institute of Healthcare Uterine Fibroid Research Network’s multi-million-dollar commitment demonstrate research investment in the uterus. International organizations such as ACOG and NICE have increased the penetration of physicians for hysteroscopy as the gold standard for the assessment of intrauterine pathology due to their clinical guidelines, which in turn drives the hysteroscopy instrument market analysis. This favorable regulatory backdrop and clinical need provide the basis for continued market momentum.

Restraints:

-

Cost Barriers, Limited Specialist Availability, and Procedural Risks Restrain the Hysteroscopy Instrument Market

The high startup expense of capital equipment and the operational cost of sustaining sterility in reusable systems discourage addressing under-resourced health care settings. The Journal of Minimally Invasive Gynecology (2017) reports that 40% of community clinics still do not have hysteroscopic equipment in place because of cost restrictions. In addition, procedural complications, including uterine perforation (0.12–1.5%) and fluid overload complications, mandate experienced operators and limit broad availability to smaller centers.

A 2023 review published in Current Opinion in Obstetrics & Gynecology also remarked on a shortage of trained hysteroscopists, particularly in rural areas, that limited service provision. Furthermore, bureaucratic hurdles and strict quality criteria, particularly in emerging countries, have led to slowed device approvals and commercialization. Post-COVID, the whirlwind of supply chain swings also affects how to receive essential components, such as optics and micro-electrosurgical units. Finally, varying reimbursement structures can make providers less inclined to invest in newer systems, especially in the outpatient or ASC setting. These collective combinations of factors represent barriers to broader utilization and largely render the hysteroscopy instrument market analysis constrained, particularly for resource-limited and cost-constrained settings.

Hysteroscopy Instrument Market Segmentation Analysis:

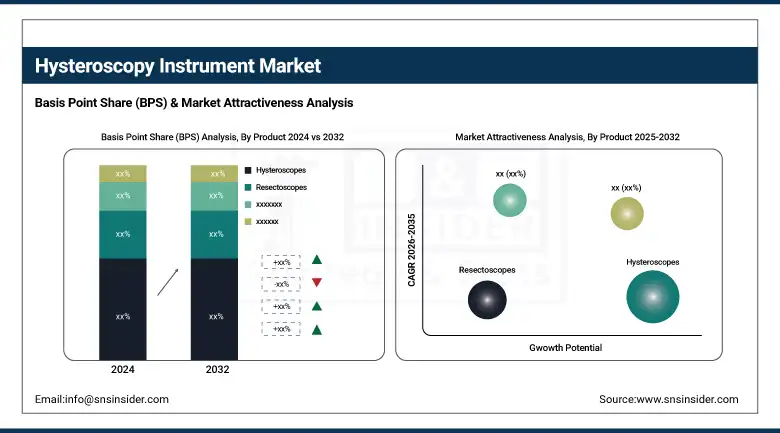

By Product

Among hysteroscopes, the hysteroscopes held the largest share of 39.9% in 2024, due to the increasing number of both diagnostic and operative hysteroscopic surgeries. Growth has been driven by the widespread take-up of high-definition flexible and rigid hysteroscopes, especially in outpatient and ambulatory care sites. Simplified painless insertion, improved visual clarity, and compatibility with video platforms make hysteroscopes a mandatory tool among gynecologists. Their contributions in the detection of intrauterine pathologies such as fibroids, adhesions, and polyps further lend them their clinical significance.

The hysterosheaths segment is growing faster as surgical procedures require better fluid management and clarity due to the increased acceptance of hysteroscopy procedures. The introduction of disposable, ergonomic hysterosheaths minimizes the risk of contamination and operation time, favoring high-throughput outpatient clinics. The increasing popularity of office-based hysteroscopies is driving further growth in this segment, the largest and one of the most lucrative, of the hysteroscopy instrument market trends.

By Usability

The disposable type segment dominated the market in 2024, accounting for 68.5% of the hysteroscopy instrument market share, owing to an increase in awareness regarding infection control and the necessity to minimize the sterilization load in healthcare settings. Disposables for hysteroscopy eliminate the risk of cross-contamination, save time, and allow rapid patient turnover - factors that are especially important for ambulatory surgery centers and gynecology practices with high patient throughput. In addition, global trends towards value-based care and increasing regulatory standards for reprocessing of reusable devices have led to greater adoption of single-use solutions.

The reusable segment is expected to grow the fastest, which is driven by the cost-effectiveness of the product in the long run and growing investment in the hospital sterilization infrastructure. New materials, combined with new designs, have prolonged lifespan of re-usable instruments and have improved their accuracy, thus decreasing the need for replacement. Hospitals and tertiary care centers are building up their reusable stocks in line with sustainable procurement policies, especially in situations where the cost of purchasing disposables regularly is out of the question. This twofold need is continuing to drive the hysteroscopy instrument market growth.

By Application

Operative hysteroscopy was the largest segment in 2024, accounting for 66.3% of the market, owing to its growing use to treat an array of intrauterine pathologies, including fibroids, endometrial polyps, and septa. With the advent of electrosurgical instruments and fluid control systems, operative hysteroscopy offers low-impact, outpatient interventions that allow patients to return to their usual activities immediately following the procedure. This has drastically minimized the need for more invasive surgical solutions that frequently require more extended hospital stays and are more costly to health care consumers. Surgical hysteroscopy has also benefited from the trend toward see-and-treat, or achieving a diagnosis and treatment during a single visit, which increases efficiency for both patients and physicians. It is also the fastest-growing segment, driven by technological advancement and expanded physician training. Rising cases of infertility and postmenopausal bleeding diagnoses are driving physicians to use operative procedures to provide an increased therapeutic vision for both hospital and ambulatory treatment over the long term, which in turn drives the global hysteroscopy instrument market.

By End Use

Hospitals generated the highest revenue share of 54.9% in 2024 as they possess advanced facilities for diagnostic and operative hysteroscopy. Most hospitals have specialized teams and facilities for gynecology procedures, which carry advanced surgical instruments, immediate-enabling imaging devices, and experienced staff, making this an ideal environment for more complex or high-risk procedures. In addition, they have ample budgets that allow the purchase of high-end hysteroscopy equipment in large quantities. Reimbursement models are available are digital workflow systems that also support their end-to-end solution offer.

The growth in the hospital end-use segment is the highest, as the changing patient pool (which is at an all-time high) in urban areas is leading to the demand for more women's health services in hospitals. Investments in OR modernization and standalone women’s health units help drive increased procedural volume. The skilled labor, infrastructure, and financial resources lead to a faster uptake of innovative devices in hospitals; these factors are also driving hospitals as the growth engine of the U.S. hysteroscopy instrument market.

Regional Insights:

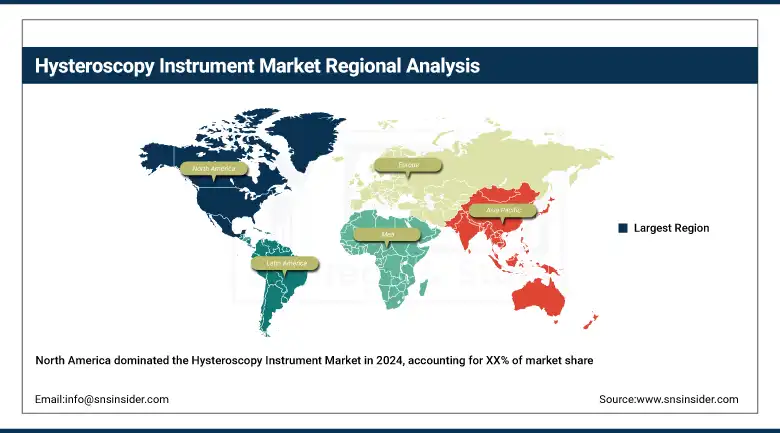

North America was the largest regional market owing to a well-developed healthcare infrastructure, high awareness levels about minimally invasive gynecology procedures, and favorable reimbursement schemes. , owing to a high number of gynecological procedures and strong presence of hospitals and ambulatory surgery centers (ASCs). The CDC states that about 500,000 hysterectomies are conducted each year in the U.S., which would create the need for hysteroscopy instruments. However, increasing demand for office and outpatient hysteroscopy is anticipated to skyrocket the market demand.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe is the second most significant contributor to the hysteroscopy instrument market due to increased affordability, early introduction of endoscopy technology, strong government support, and focus on overall health and well-being. Germany is the first in the region with its high-tech surgical equipment and a growing number of outpatient hysteroscopies. The nation also has enormous R&D spending and local production of good-quality medical devices. France and the UK also have a strong share due to the implementation of a national screening and the awareness of fertility issues. Italy and Spain are growing from both an increasing elderly female population and the modernization of health care.

The Asia Pacific region is the fastest-growing region of the hysteroscopy instruments market, primarily due to enhancements in healthcare facilities, an increasing number of patients, and a rising level of awareness about the advantages of minimally invasive gynecology treatment. China is one of the largest contributors because of fast urbanization, private hospitals' proliferation, and the utilization of more modern diagnostic methods. China's rising fertility services and better maternal care are also expected to further drive demand for hysteroscopy equipment, as WHO numbers show.

Key Players:

Leading hysteroscopy instrument companies operating in the market are KARL STORZ, Olympus, Richard Wolf GmbH, Stryker, Medtronic, B. Braun, Cooper Surgical, Hologic, Medicon, and Boston Scientific.

Recent Developments in the Hysteroscopy Instrument Market:

-

In Feb 2025, Materna Medical shared promising preliminary results from an online study focused on women experiencing vaginal muscle tightness and painful intercourse, highlighting the potential for innovative non-invasive therapeutic solutions in pelvic health. This supports growing R&D interest in minimally invasive gynecological care.

-

In May 2024, Elfa International, in partnership with NTT DATA, upgraded the hysteroscope unit at Lal Ded Hospital in Jammu and Kashmir to enhance maternity healthcare services, marking a key development in advancing women’s health infrastructure in the region.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.08 Billion |

| Market Size by 2032 | USD 3.63 Billion |

| CAGR | CAGR of 7.24% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Handheld instruments (Forceps, Scissors, Dilators, and Other handheld instruments), Hysteroscopes (Rigid, Flexible), Resectoscopes (Bipolar, Unipolar), Hysterosheaths) • By Usability (Reusable, Disposable) • By Application (Diagnostic hysteroscopy, Operative hysteroscopy (Myomectomy, Polypectomy, Endometrial ablation, and Tubal sterilization)) • By End Use (Hospitals, Ambulatory Surgery Centers, and Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | KARL STORZ, Olympus, Richard Wolf GmbH, Stryker, Medtronic, B. Braun, Cooper Surgical, Hologic, Medicon, and Boston Scientific. |

Frequently Asked Questions

North America is the dominant region in the Hysteroscopy Instrument Market.

The high startup expense of capital equipment and the operational cost of sustaining sterility in reusable systems discourage addressing under-resourced health care settings.

Growth in the hysteroscopy instruments market is driven by the increasing adoption of hysteroscopy procedures, the growing global prevalence of gynecological diseases, and the increasing incidence of post-menopausal bleeding.

By 2032, the Hysteroscopy Instrument Market is expected to reach USD 3.63 billion, up from USD 2.08 billion in 2024.

The Hysteroscopy Instrument Market is projected to grow at a CAGR of 7.24% during the forecast period.

Get in Touch