Ice Skating Equipment Market Report Scope & Overview:

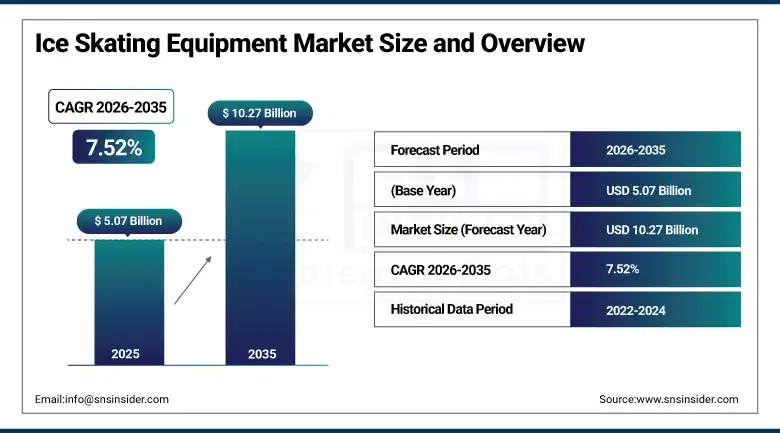

The Ice Skating Equipment Market was valued at USD 5.07 Billion in 2025 and is expected to reach USD 10.27 Billion by 2035, growing at a CAGR of 7.52% from 2026 to 2035.

The market for ice skating equipment is unique in the world-wide sports and recreational equipment industry in that the industry has a very diverse group of participants, with the most elite competitive athletes competing at the international championship level, the youth recreational athlete trying winter sports for the first time and the casual adult skater taking to the ice as a seasonal recreational activity. The market includes a variety of product categories such as performance ice skates designed to meet the specific biomechanical demands of hockey, figure skating, speed skating, and recreational sports; protective equipment systems; specialized skating apparel; blade accessories; and training equipment designed to improve skill development and prevent injuries for skaters of all levels.

Bauer Hockey LLC, one of the world's leading ice hockey equipment manufacturers, reported that its global retail sell-through of performance skate products grew at a double-digit rate in 2024, with its flagship Vapor and Supreme skate lines driving average selling price increases of 12% as consumers upgraded to higher-specification boot and blade configurations supported by expanded retail customization services across key North American and European markets.

Market Size and Forecast

-

Market Size in 2026E: USD 5.35 Billion

-

Market Size by 2035: USD 10.27 Billion

-

CAGR: 7.52% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Ice Skating Equipment Market - Request Free Sample Report

Ice Skating Equipment Market Trends

-

Rising adoption of heat-moldable skate boots is improving personalized fit and on-ice performance.

-

Growing recreational and synchronized skating participation is boosting demand for entry-level and mid-range equipment.

-

Expansion of online sales channels is accelerating premium equipment accessibility and market competition.

-

Increasing youth ice hockey participation across Asia-Pacific is driving growth in beginner and intermediate gear segments.

-

Advanced blade materials and precision sharpening technologies are enhancing performance in competitive skating disciplines.

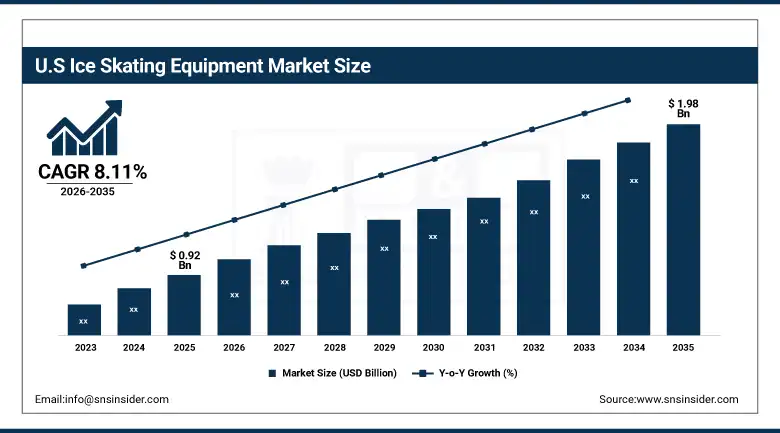

The U.S. Ice Skating Equipment Market Outlook

The U.S. Ice Skating Equipment Market was valued at USD 0.92 Billion in 2025 and is expected to reach USD 1.98 Billion by 2035, growing at a CAGR of 8.11%.

The United States represents the largest national market in North America for ice skating equipment, driven by the country’s entrenched ice hockey culture at all levels of professional, collegiate, junior and recreational participation, a large figure skating community supported by hundreds of sanctioned competitive events each year, and a growing recreational skating participant base increasingly accessing the sport through expanded public rink infrastructure and year-round indoor ice facilities in non-traditional markets. The U.S. market has the highest concentration of specialty ice sports retailers in the world, many of whom offer sophisticated bespoke skate fitting, blade profiling and heat-molding services that create premium purchasing environments that sustain high average transaction values for performance equipment.

CCM Hockey disclosed that its North American market investment in skate technology development exceeded USD 40 Billion in the 2024–2025 period, with its AS-V Pro and Jetspeed FT series commanding premium retail positioning through proprietary carbon fiber boot constructions, scan-to-fit customization workflows, and enhanced energy return blade holder systems that have driven measurable market share gains in the U.S. specialty hockey retail channel.

Ice Skating Equipment Market Segment Analysis

-

By Product Type, ice skates dominated the market with 42.06% share in 2025, while skate accessories are the fastest growing product type with the highest CAGR of 8.03% from 2026 to 2035.

-

By Skate Type, hockey skates dominated the market with 44.06% share in 2025, while recreational skates are the fastest growing skate type with the highest CAGR of 8.47% from 2026 to 2035.

-

By End User, amateur & recreational skaters dominated the market with 49.06% share in 2025, while sports academies & clubs are the fastest growing end user segment with the highest CAGR of 7.84% from 2026 to 2035.

-

By Distribution Channel, specialty sports stores dominated the market with 34.15% share in 2025, while online retail is the fastest growing channel with the highest CAGR of 8.14% from 2026 to 2035.

By Product Type, ice skates dominate the ice skating equipment market, while skate accessories are the fastest-growing segment.

Ice skates segment dominated the market with the highest revenue share of about 42.06% in 2025 due to their position as the primary and non-substitutable equipment investment required for any form of ice skating participation, encompassing the full spectrum from entry-level recreational models to elite-performance competition boots engineered with carbon fiber reinforcement, precision-manufactured blade assemblies, and anatomically optimized liner systems. The centrality of the ice skate to the participant's performance experience, combined with the frequency of replacement purchases driven by youth size progression, blade wear cycles, boot structural fatigue, and performance upgrade aspirations among advancing skaters, creates a consistently high-volume, high-average-value revenue stream that anchors the product type's dominant commercial position across all regional markets.

Skate accessories segment is estimated to register the highest CAGR of 8.03% during the forecast period of 2026–2035 owing to growing consumer awareness of the performance, longevity, and safety benefits provided by blade guards, soakers, skate bags, lace tighteners, blade sharpening services, and boot care products that extend equipment lifespan and optimize on-ice performance. The expansion of online retail channels has significantly broadened consumer access to specialist accessory product ranges that were previously available only through dedicated ice sports retailers, driving accelerating adoption of premium accessories among recreational and competitive skaters who are increasingly informed about equipment maintenance best practices through digital communities and coaching networks.

By Skate Type, hockey skates dominate the ice skating equipment market, while recreational skates are the fastest-growing segment.

Hockey skates segment dominated the market with the largest revenue share of about 44.06% in 2025 attributed to the global scale of organized ice hockey participation, the high replacement frequency driven by the demanding mechanical environment of competitive and recreational hockey play, and the premium pricing commanded by performance-tier hockey skate constructions that incorporate advanced carbon composite boot materials, titanium or stainless steel blade holders, and precision-engineered steel blades designed to deliver the edge retention and energy transfer characteristics required for competitive play. The established global distribution infrastructure for hockey equipment, including dedicated specialty hockey pro shops, major sporting goods retail chains, and expanding online specialist retailers, ensures broad commercial accessibility across all performance tiers of the hockey participation pyramid.

Recreational skates segment is projected to witness the fastest CAGR of 8.47% during 2026–2035 due to rapid expansion of casual and family-oriented ice skating participation globally, increasing investment in public skating rink infrastructure in urban centers across Asia Pacific and the Middle East, and the growing popularity of ice skating as an accessible, socially engaging winter recreational activity among health-conscious adult demographics seeking low-impact cardiovascular exercise alternatives. The ongoing premiumization of recreational skate product categories by leading manufacturers, incorporating improved comfort liner systems, easier entry mechanisms, and more aesthetically compelling designs, is further elevating average transaction values and driving repeat purchasing within this growth segment.

By End User, amateur & recreational skaters dominate the ice skating equipment market, while sports academies & clubs is the fastest-growing segment.

Amateur & recreational skaters segment dominated the ice skating equipment market with the highest revenue share of 49.06% in 2025 due to the sheer scale of the global casual skating participant base, which vastly exceeds the elite and semi-professional athlete community in numerical terms and collectively generates aggregate equipment expenditures that are disproportionately large relative to individual transaction values. The structural diversity within this segment, encompassing first-time skaters purchasing entry-level equipment, intermediate recreational participants investing in mid-tier performance upgrades, and adult hobbyists maintaining regular recreational participation, creates a commercially resilient demand base that exhibits relatively low sensitivity to competitive season cycles and maintains consistent purchasing activity throughout the calendar year.

Sports academies & clubs’ segment is projected to register the highest CAGR of 7.84% during the forecast period of 2026–2035 owing to accelerating institutional investment in structured ice sports development programs, particularly across emerging market regions in Asia Pacific and the Middle East where government-backed sports academies and private athletic development facilities are incorporating ice skating disciplines into their program portfolios for the first time. The bulk procurement patterns and multi-year equipment supply relationships characteristic of institutional buyers, combined with growing demand for branded equipment packages and uniform outfitting services from sports academies, create structurally attractive revenue opportunities for equipment manufacturers and specialist distributors.

By Distribution Channel, specialty sports stores dominate the ice skating equipment market, while online retail is the fastest-growing segment.

Specialty sports stores segment dominated the ice skating equipment market with the highest revenue share of 34.15% in 2025 owing to the high-touch service requirements associated with ice skate purchasing decisions, where professional fitting expertise, heat-molding capabilities, blade profiling services, and informed product guidance are critical determinants of purchase satisfaction and customer loyalty. The specialist retail environment uniquely accommodates the complex biomechanical considerations involved in selecting ice skates for competitive or serious recreational use, creating a differentiated commercial proposition that sustains premium pricing and high average transaction values relative to mass-market sporting goods retail formats that cannot replicate the same depth of product knowledge and fitting service quality.

Online retail segment is anticipated to record the fastest CAGR of 8.14% throughout the forecast period of 2026–2035 driven by the progressive refinement of digital commerce experiences for equipment categories that previously required in-store assessment, including the deployment of virtual fitting tools, AI-powered skate recommendation engines, detailed size conversion resources, and expanded consumer review ecosystems that collectively reduce the information asymmetry and purchase uncertainty that historically limited online channel adoption for performance ice skating equipment. The accelerating penetration of direct-to-consumer e-commerce strategies by leading equipment brands is further intensifying the structural shift toward online purchasing across all end user segments of the ice skating equipment market.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

75.49% |

|

Europe |

Germany |

33.46% |

|

Asia Pacific |

China |

42.19% |

|

Middle East & Africa |

UAE |

37.21% |

|

Latin America |

Brazil |

43.21% |

North America Ice Skating Equipment Market Insights

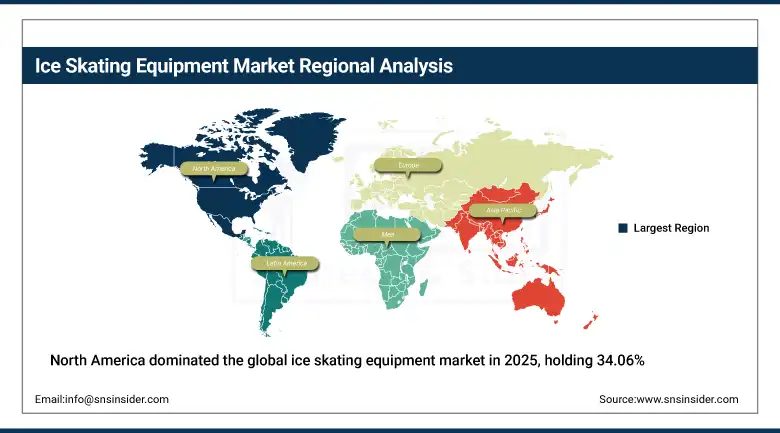

North America dominated the global ice skating equipment market in 2025, holding 34.06% of global revenues, with the United States accounting for 75.49% of regional revenue. The region's dominant market position reflects the unparalleled depth of ice sports cultural integration across Canada and the United States, where ice hockey occupies the status of a national sport in Canada and commands an exceptionally loyal and equipment-intensive participant base, and where figure skating and recreational ice skating maintain strong participation rates supported by thousands of indoor rink facilities operating year-round across both countries.

Canada contributes disproportionately to global ice skating equipment spending due to its exceptionally high hockey participation rates and strong culture of youth and elite player development, which drives sustained demand for premium skating equipment.

The North American ice hockey equipment market generates annual retail revenues exceeding USD 1.8 billion across all product categories, with Canada contributing an estimated 35–40% of total regional equipment spending despite representing less than 12% of the combined North American population, reflecting the extraordinary per capita equipment intensity of the Canadian hockey participation culture.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Ice Skating Equipment Market Insights

Europe constitutes the second-largest regional ice skating equipment market, sustained by the continent's rich heritage of competitive and recreational ice sports across a geographically and culturally diverse participant base. Germany, Sweden, Finland, Russia, the Czech Republic, and Switzerland collectively represent the core of the European competitive ice hockey market, each maintaining highly developed national league systems, significant youth development programs, and strong traditions of equipment investment at all levels of the participation pyramid. The figure skating discipline maintains particularly robust commercial relevance across Central and Eastern European markets, with Russia, Ukraine, and several Eastern European nations producing disproportionately high concentrations of internationally competitive figure skaters whose equipment requirements support premium market segments.

Europe operates more than 5,000 indoor and outdoor ice rinks, providing one of the world's largest infrastructures supporting year-round demand for ice skating equipment across competitive and recreational users. More than 70% of advanced-performance skate sales in Northern Europe are concentrated in Sweden, Finland, Germany, Switzerland, and the Czech Republic, where ice sports participation rates significantly exceed the European average.

Asia Pacific Ice Skating Equipment Market Insights

Asia Pacific is the fastest-growing regional ice skating equipment market at a CAGR of 8.23% through 2035. The region's growth trajectory is primarily driven by China's extraordinary investment in winter sports infrastructure and participation development following the country's co-hosting of the 2022 Beijing Winter Olympics, which catalyzed a government-backed initiative to develop 300 billion winter sports participants from a historically limited base, directly stimulating the construction of hundreds of new indoor ice facilities. The establishment of structured ice hockey and figure skating training academies, and the emergence of a commercially significant domestic ice skating equipment market where international premium brands are competing for first-mover positioning alongside growing domestic manufacturers.

China's commitment to winter sports development resulted in the construction of over 650 new ice rinks between 2018 and 2024, nearly tripling the country's indoor ice facility capacity and generating a structural foundation of equipment demand estimated to be growing at rates exceeding 15% annually as new participant cohorts enter the market for the first time across youth hockey, figure skating, and recreational disciplines.

MEA & Latin America Ice Skating Equipment Market Insights

Middle East and Africa and Latin America regions represent commercially developing ice skating equipment markets whose growth dynamics are driven primarily by infrastructure investment and the leisure aspirations of rapidly expanding urban middle-class populations rather than by established cultural traditions of ice sports participation. The UAE leads MEA regional revenues at 30.45% of the total, supported by the country's well-developed air-conditioned entertainment and leisure infrastructure that incorporates indoor ice rinks as flagship attractions in major shopping centers and dedicated entertainment complexes across Dubai, Abu Dhabi, and Sharjah, serving both the expatriate population with pre-existing ice sports backgrounds and a growing local population engaging with ice skating as a novel recreational activity.

In Latin America, Brazil, anchored by a small but growing urban ice sports community centered in major metropolitan areas where air-conditioned indoor rinks serve as premium recreational destinations. Mexico and Argentina represent the region's next-tier growth opportunities, with increasing foreign retail brand presence and growing awareness of ice sports through televised international competition creating gradual but sustained market development across their urban consumer bases.

Latin America hosts more than 250 commercial ice skating facilities, with Brazil, Mexico, Argentina, and Chile representing the largest centers of ice skating participation and equipment consumption. Rental and facility-operated equipment accounts for nearly 35% of skate utilization within MEA, significantly higher than in mature ice sports markets due to the large proportion of first-time and casual participants.

Market Dynamics

Growth Drivers: Recreational participation growth and winter sports infrastructure investment

The most structurally significant driver of sustained commercial growth in the ice skating equipment market is the broad expansion of organized and recreational ice skating participation across both established and emerging market geographies, driven by the convergence of increasing disposable income allocation toward experiential leisure activities, expanding access to indoor ice skating infrastructure in previously underserved urban markets, and the growing cultural resonance of winter sports driven by major international competitive events that consistently deliver elevated public engagement and participation inspiration. The rapid expansion of indoor ice rinks across China, Southeast Asia, and the Middle East is creating new consumer bases for ice skating equipment, driving demand for both entry-level products and future premium equipment upgrades.

Restraints: High cost of participation and climate dependency of outdoor ice

The substantial aggregate cost of ice skating participation, encompassing skate purchase or rental, rink admission fees, lesson costs, protective gear, and apparel investments, represents a meaningful access barrier for price-sensitive consumer segments that limits market penetration depth beyond the middle- and upper-income demographics that currently constitute the core buyer base for most regional ice skating equipment markets. The equipment intensity of competitive ice hockey participation in particular, where a fully outfitted competitive player requires investments across skates, helmet, shoulder pads, elbow pads, gloves, shin guards, pants, and sticks. The high cost of skates and protective equipment creates affordability barriers that can limit participation among lower-income youth, even in regions with adequate rink infrastructure.

Opportunities: Asian market expansion and direct-to-consumer digital commerce

The ongoing development of ice sports infrastructure and participation culture across the Asia Pacific region, and China in particular, represents the most commercially significant medium to long-term growth opportunity for global ice skating equipment manufacturers, offering access to a potential participant base of hundreds of Billions of consumers who are encountering ice skating for the first time through newly constructed facilities, government-supported development programs, and the inspirational commercial impact of elite Chinese athletic performance on domestic sports participation choices. Brands investing early in localized products, distribution partnerships, and retail expansion across China and Asia-Pacific are well-positioned to capture significant market growth opportunities through 2035.

Recent Developments:

-

2026: CCM Hockey commercialized its AS-VI Pro performance skate platform featuring a full carbon fiber boot shell manufactured through an automated fiber placement process, integrated anatomical scan customization workflow available through authorized retail partners, and its next-generation SpeedBlade ONE holder system designed for enhanced stability and energy transfer.

-

2026: Powerslide Sportartikelvertriebs GmbH expanded its Nordic Skating product line with new integrated binding system designs targeting the growing outdoor touring and fitness skating segment across Scandinavian and Central European markets, supported by an expanded European specialty retail partnership network.

-

2025: Bauer Hockey LLC launched its new Hyperlite 3 ice hockey skate featuring an upgraded carbon composite boot construction, redesigned Tuuk Lightspeed EDGE blade holder, and enhanced heat-molding liner system targeting elite-level competitive and advanced recreational hockey players in North America and Europe.

-

2025: Jackson Ultima Skates introduced its Fusion X series recreational and beginner figure skate line incorporating a new dual-density foam liner system, improved stainless steel blade assembly, and extended sizing range to expand market coverage across youth and adult entry-level figure skating participants globally.

Ice Skating Equipment Market Key Players are:

-

Bauer Hockey LLC

-

CCM Hockey

-

Graf Skates AG

-

Jackson Ultima Skates

-

Riedell Shoes Inc.

-

EDEA Skates S.r.l.

-

SP-Teri Inc.

-

Risport Skates

-

Roces S.r.l.

-

Powerslide Sportartikelvertriebs GmbH

-

Rollerblade Inc. (Ice Skate Division)

-

Tempish s.r.o.

-

American Athletic Shoe Co. (A&R Sports)

-

MK Blades

-

John Wilson Skates

-

Sherwood Hockey Inc.

-

Winnwell Inc.

-

Botas a.s.

-

Viking Skates B.V.

-

Decathlon S.A. (Oxelo Ice Skating Equipment)

Ice Skating Equipment Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.07 Billion |

| Market Size by 2035 | USD 10.27 Billion |

| CAGR | CAGR of 7.52% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Ice Skates, Protective Gear, Apparel & Clothing, Skate Accessories, Training Aids & Equipment) • By Skate Type (Hockey Skates,Figure Skates Recreational Skates, Speed Skates) • By End User (Amateur & Recreational Skaters,Professional Athletes Sports, Academies & Clubs, Rental Facilities & Ice Rinks) • By Distribution Channel (Specialty Sports Stores, Sporting Goods Retailers, Online Retail, Direct Sales, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Bauer Hockey LLC, CCM Hockey, Graf Skates AG, Jackson Ultima Skates, Riedell Shoes Inc., EDEA Skates S.r.l., SP-Teri Inc., Risport Skates, Roces S.r.l., Powerslide Sportartikelvertriebs GmbH, Rollerblade Inc. (Ice Skate Division), Tempish s.r.o., American Athletic Shoe Co. (A&R Sports), MK Blades, John Wilson Skates, Sherwood Hockey Inc., Winnwell Inc., Botas a.s., Viking Skates B.V., Decathlon S.A. (Oxelo Ice Skating Equipment) |

Frequently Asked Questions

The ice skating equipment market is expected to grow at a CAGR of 7.52% from 2026 to 2035.

The ice skating equipment market was valued at USD 5.07 Billion in 2025.

Key growth drivers include expanding ice skating infrastructure in Asia-Pacific and the Middle East, steady equipment replacement demand in North America and Europe, and rising online sales of premium skating equipment globally.

Online Retail is the fastest-growing distribution channel in the ice skating equipment market, with a CAGR of 8.14% from 2026 to 2035.

North America dominated the ice skating equipment market in 2025, holding 34.06% of global revenues, with the United States accounting for 75.49% of North American revenues.

Get in Touch