Rapid Thermal Processing Equipment Market Report Scope & Overview:

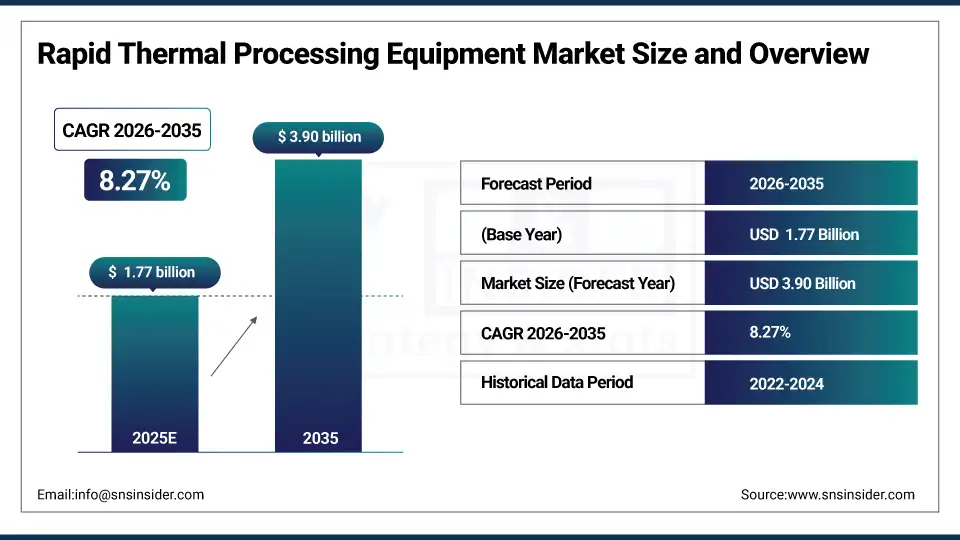

The Rapid Thermal Processing Equipment Market size was valued at USD 1.77 Billion in 2025 and is projected to reach USD 3.90 Billion by 2035, growing at a CAGR of 8.27% during 2026–2035.

The Rapid Thermal Processing Equipment Market is a manufacturing equipment market, and it deals with equipment used for the rapid heating of semiconductor wafers to extremely high temperatures for short periods of time, thus providing precise control of material characteristics, which is essential for semiconductor manufacturing. The market is driven by the increasing demand for advanced semiconductor chips, high-end computing, AI, IoT, and 5G technologies, as well as investments in semiconductor fabrication facilities and new and improved thermal processing equipment technologies.

Rapid Thermal Processing Equipment (RTP) Market Size and Forecast:

-

Market Size in 2025: USD 1.77 Billion

-

Market Size by 2035: USD 3.90 Billion

-

CAGR: 8.27% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Rapid Thermal Processing Equipment Marke - Request Free Sample Report

Rapid Thermal Processing Equipment Market Key Trends:

-

Increasing adoption of advanced semiconductor nodes (5 nm, 3 nm, and below) is driving demand for high-precision rapid thermal processing equipment in wafer fabrication.

-

Rising global investments in semiconductor fabrication plants (fabs) are accelerating the deployment of advanced thermal processing technologies.

-

Growing demand for AI chips, high-performance computing, and 5G devices is increasing the need for efficient wafer annealing and thin-film processing systems.

-

Technological advancements in automation, temperature control, and process uniformity are improving the efficiency and reliability of RTP equipment.

-

Expansion of automotive electronics and electric vehicles is boosting semiconductor production, thereby increasing the adoption of rapid thermal processing solutions.

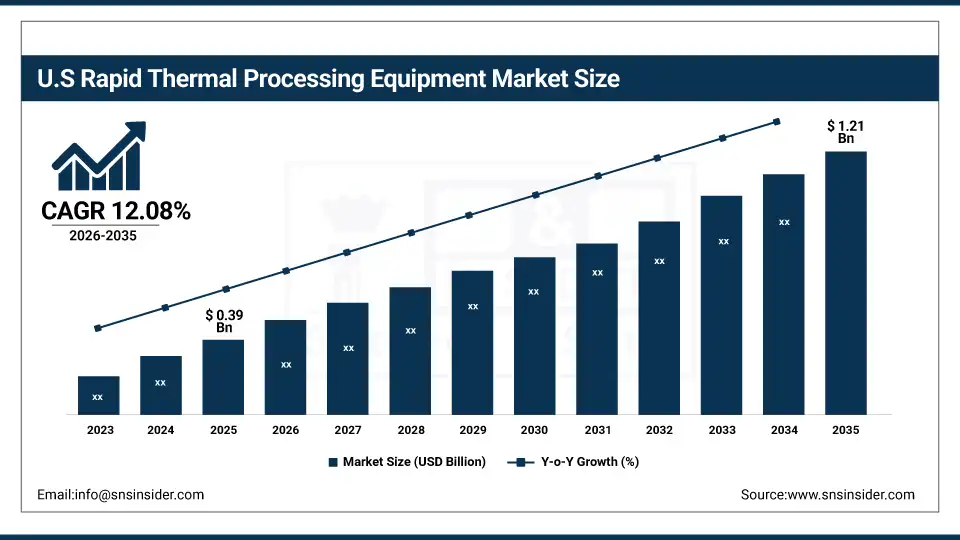

The U.S. Rapid Thermal Processing (RTP) Equipment Market is valued at USD 0.39 Billion in 2025 and is expected to reach USD 1.21 Billion in 2035, growing at a CAGR of 12.08% from 2026 to 2035. Growth is driven by increasing semiconductor fabrication, advanced node chip production, rising AI and 5G chip demand, government incentives, and expansion of high-performance electronics manufacturing.

Rapid Thermal Processing Equipment Market Key Drivers:

-

Increasing demand for advanced semiconductor chips for AI, 5G, IoT, and high-performance computing drives adoption of rapid thermal processing equipment.

The key factor that is fueling the expansion of the Rapid Thermal Processing Equipment market is the rapid expansion of semiconductor manufacturing and the production of advanced chip technologies. The semiconductor fabrication plants need precise and efficient technologies for thermal processing in semiconductor fabrication. The investments in building new semiconductor fabrication plants, the rising demand for consumer electronics, and the use of semiconductor in the automotive and telecommunication industries are boosting the RTP equipment market.

Rapid Thermal Processing Equipment Market Key Restraints:

-

High capital investment and complex semiconductor fabrication processes may limit the adoption of advanced rapid thermal processing systems.

One of the major challenges that the market is facing is the high cost that is incurred in the equipment installation, maintenance, and integration of the RTP equipment into the semiconductor fabrication lines. It is worth noting that the semiconductor manufacturing plants demand high capital costs. Moreover, the requirement for highly skilled personnel, along with the semiconductor market cycle, may also impede the growth of the market.

Rapid Thermal Processing Equipment Market Key Opportunities:

-

Increasing global semiconductor investments and development of advanced chip manufacturing technologies create significant growth opportunities.

Opportunities in the market are driven by expanding semiconductor fabrication capacity worldwide and the development of advanced semiconductor nodes such as 5 nm, 3 nm, and below. The rising demand for AI processors, electric vehicles, high-performance computing, and next-generation communication technologies is encouraging semiconductor manufacturers to adopt advanced thermal processing solutions. Government initiatives supporting semiconductor manufacturing and supply chain localization are also creating new growth opportunities for RTP equipment providers.

Rapid Thermal Processing Equipment Market Segments Analysis:

-

By Type: In 2025, Rapid Thermal Annealing (RTA) dominated with 42% share; Rapid Thermal Chemical Vapor Deposition (RTCVD) fastest growing segment during 2026-2035

-

By Wafer Size: In 2025, 300 mm dominated with 64% share; Above 300 mm fastest growing segment during 2026-2035

-

By Application: In 2025, Annealing dominated with 56% share; Chemical Vapor Deposition fastest growing segment during 2026-2035

-

By End-Use Industry: In 2025, Semiconductor Manufacturing dominated with 55% share; Automotive Electronics fastest growing segment during 2026-2035

By Type: Rapid Thermal Annealing Dominates, Rapid Thermal Chemical Vapor Deposition Fastest-Growing

Rapid Thermal Annealing (RTA) dominates the type segment of the Rapid Thermal Processing Equipment Market, accounting for a significant share due to its extensive use in dopant activation, defect repair, and improving electrical characteristics of semiconductor wafers. It is widely applied in advanced semiconductor fabrication processes, making it the most utilized RTP technology.

Rapid Thermal Chemical Vapor Deposition (RTCVD) is the fastest-growing segment, driven by increasing demand for thin film deposition and semiconductor device manufacturing

By Wafer Size: 300 mm Dominates, Above 300 mm Fastest-Growing

The 300 mm wafer segment dominates the market due to the fact that the majority of the semiconductor manufacturing facilities operate at 300 mm wafer sizes for the manufacturing of chips. It increases the manufacturing efficiency, cost of the chip, and productivity.

Above 300 mm wafer segment is expected to grow at the fastest rate due to ongoing research and development for next-generation semiconductor manufacturing technologies and increasing demand for higher processing capacity.

By Application: Annealing Dominates, Chemical Vapor Deposition Fastest-Growing

Annealing segment holds the largest share of the Rapid Thermal Processing Equipment Market, as it is the most critical segment for the activation of dopants and repairing of crystal defects in semiconductor materials, as semiconductor chip manufacturing is involved.

Chemical Vapor Deposition (CVD) applications are witnessing the fastest growth, as the demand for semiconductor materials is increasing rapidly.

By End User: Semiconductor Manufacturing Dominates, Automotive Electronics Fastest-Growing

Semiconductor manufacturing segment dominates the market because RTP equipment is primarily used in wafer fabrication facilities for chip production. The increasing demand for microprocessors, memory chips, and logic devices across industries continues to drive adoption in this segment.

Automotive electronics is the fastest-growing end-user segment due to the rapid expansion of electric vehicles, advanced driver-assistance systems (ADAS), and increasing semiconductor content in modern vehicles.

Rapid Thermal Processing Equipment Market Regional Analysis:

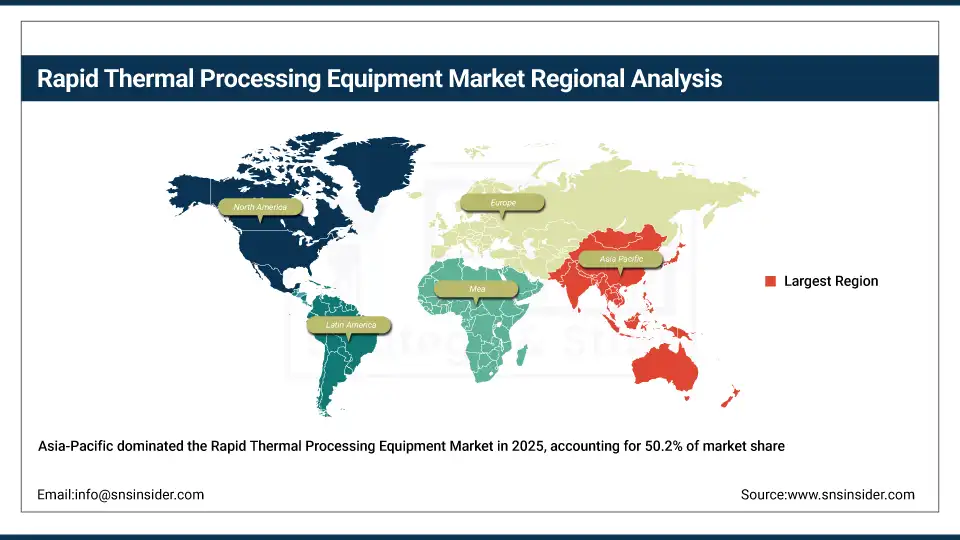

Asia-Pacific Rapid Thermal Processing Equipment Market Insights:

Asia-Pacific is the dominant region in the Rapid Thermal Processing Equipment Market, holding approximately 50.2% market share. The region’s leadership is driven by the presence of major semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan, where demand for advanced node chips and high-volume wafer fabrication is strong. Expanding industries such as consumer electronics, automotive electronics, and 5G technologies further accelerate adoption. Large-scale investments in semiconductor fabs and government support for technological advancement are key factors sustaining market dominance.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Rapid Thermal Processing Equipment Market Insights:

North America is the fastest-growing region in the Rapid Thermal Processing Equipment Market, with a CAGR of 12.60% from 2026 to 2035. Growth is driven by increasing investments in advanced semiconductor fabrication facilities, AI and high-performance computing chip production, and 5G technology deployment. The U.S. leads the region due to substantial government support, R&D initiatives, and early adoption of cutting-edge wafer processing technologies, while Canada contributes through specialized semiconductor research and industrial electronics manufacturing.

Europe Rapid Thermal Processing Equipment Market Insights:

Europe is experiencing steady growth in the Rapid Thermal Processing Equipment Market, driven by increasing demand for automotive semiconductors, industrial electronics, and high-tech manufacturing applications. The region benefits from strong R&D capabilities, government initiatives supporting semiconductor innovation, and adoption of advanced wafer fabrication technologies. Countries such as Germany, France, and the UK are focusing on smart manufacturing, Industry 4.0, and semiconductor process optimization, which are boosting the deployment of rapid thermal processing systems across the region.

Latin America Rapid Thermal Processing Equipment Market Insights:

Latin America is witnessing gradual growth in the Rapid Thermal Processing Equipment Market, driven by increasing adoption in industrial electronics and consumer semiconductor applications. Key countries like Brazil and Mexico are slowly expanding semiconductor manufacturing and electronics production, creating opportunities for RTP system deployment and technology upgrades across industries.

Middle East & Africa (MEA) Rapid Thermal Processing Equipment Market Insights:

The MEA region is an emerging market for Rapid Thermal Processing Equipment, supported by investments in industrial electronics, semiconductor research, and smart technology initiatives. Countries such as the UAE, Saudi Arabia, and South Africa are driving demand through government-backed projects, growing electronics manufacturing, and the adoption of advanced wafer processing technologies. Increasing focus on industrial automation, high-tech manufacturing, and innovation is creating new opportunities for RTP equipment providers across the region.

Rapid Thermal Processing Equipment Market Competitive Landscape:

Applied Materials, Inc. is a U.S.-based company founded in 1967 and headquartered in Santa Clara, California, specializing in materials engineering solutions used to produce semiconductor chips and advanced electronic devices. The company provides semiconductor manufacturing equipment, including deposition, etching, inspection, and thermal processing systems used in advanced wafer fabrication.

-

In July 2024, Applied Materials introduced advanced rapid thermal processing solutions designed to improve wafer annealing precision and support next-generation semiconductor nodes for AI, high-performance computing, and 5G devices.

Tokyo Electron Limited is a Japanese company established in 1963 and headquartered in Tokyo, Japan, focusing on semiconductor production equipment and flat-panel display manufacturing systems. The company offers a wide range of semiconductor fabrication solutions, including coating, developing, etching, deposition, and thermal processing equipment used in chip manufacturing.

-

In September 2024, Tokyo Electron launched next-generation thermal processing equipment aimed at improving temperature uniformity and process control for advanced semiconductor nodes, supporting high-volume chip production and improved device performance.

Rapid Thermal Processing Equipment Companies are:

-

Applied Materials, Inc.

-

Kokusai Electric Corporation

-

ASM International N.V.

-

SCREEN Semiconductor Solutions Co., Ltd.

-

Mattson Technology (Beijing E-Town Semiconductor Technology)

-

Veeco Instruments Inc.

-

Aixtron SE

-

CVD Equipment Corporation

-

Centrotherm International AG

-

Ferrotec Holdings Corporation

-

KLA Corporation

-

Ulvac, Inc.

-

Hitachi High-Tech Corporation

-

Nikon Corporation

-

Canon Machinery Inc.

-

SÜSS MicroTec SE

-

Oxford Instruments plc

-

Plasma-Therm LLC

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.77 Billion |

| Market Size by 2035 | USD 3.90 Billion |

| CAGR | CAGR of 8.27% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type: (Rapid Thermal Annealing (RTA), Rapid Thermal Oxidation (RTO), Rapid Thermal Chemical Vapor Deposition (RTCVD), Rapid Thermal Processing Systems) • By Wafer Size: (Up to 200 mm, 300 mm, Above 300 mm) • By Application: (Annealing, Oxidation, Chemical Vapor Deposition, Diffusion) • By End User: (Semiconductor Manufacturing, Consumer Electronics, Automotive Electronics, Telecommunications, Industrial Electronics) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Applied Materials, Inc., Tokyo Electron Limited, Kokusai Electric Corporation, ASM International N.V., SCREEN Semiconductor Solutions Co., Ltd., Mattson Technology (Beijing E-Town Semiconductor Technology), Lam Research Corporation, Veeco Instruments Inc., Aixtron SE, CVD Equipment Corporation, Centrotherm International AG, Ferrotec Holdings Corporation, KLA Corporation, Ulvac, Inc., Hitachi High-Tech Corporation, Nikon Corporation, Canon Machinery Inc., SÜSS MicroTec SE, Oxford Instruments plc, Plasma-Therm LLC. |

Frequently Asked Questions

The Rapid Thermal Processing Equipment Market is expected to grow at a CAGR of 8.27% during 2026–2035.

The market was valued at USD 1.77 Billion in 2025 and is projected to reach USD 3.90 Billion by 2035.

The key drivers of the Rapid Thermal Processing Equipment Market include rising semiconductor demand, advanced node chip manufacturing, expanding semiconductor fabs, growth of AI and 5G technologies, and increasing investment in wafer processing equipment.

The Rapid Thermal Annealing (RTA) segment dominated during the projected period.

Asia-Pacific dominated the Rapid Thermal Processing Equipment Market in 2025.

Get in Touch