Identity as a Service (IDaaS) Market Report Scope & Overview:

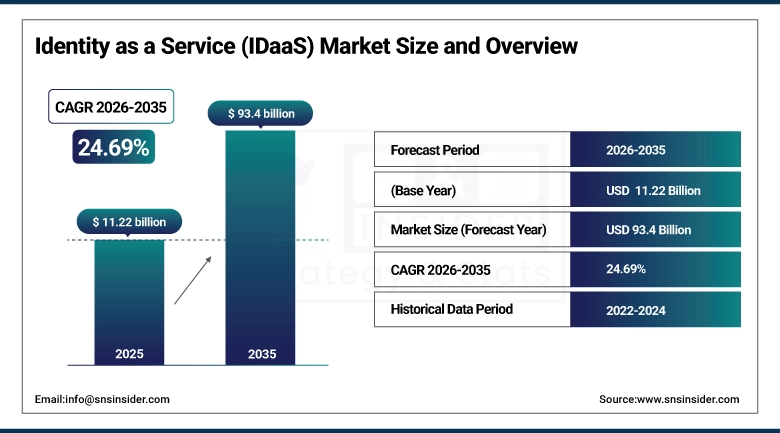

The Identity as a Service (IDaaS) Market was valued at USD 11.22 billion in 2025 and is expected to reach USD 93.4 billion by 2035, growing at a CAGR of 24.69% from 2026–2035.

Identity as a Service (IDaaS) is the delivery of identity and access management (IAM) capabilities through cloud-based platforms on a subscription basis. These services encompass user authentication, Single Sign-On (SSO) across enterprise applications, Multi-Factor Authentication (MFA), user lifecycle provisioning and deprovisioning, privileged access management, and compliance reporting. The market is experiencing explosive growth as organizations respond to the convergence of multiple structural forces: the irreversible shift to cloud applications that require centralized identity management, the proliferation of remote and hybrid work models that make traditional perimeter-based security obsolete, and an escalating wave of credential-based cyberattacks that make robust authentication a board-level priority. The zero-trust security model—which assumes no user, device, or network is inherently trustworthy—is driving systematic IDaaS adoption as its foundational enabling technology.

By 2023, in Asia Pacific companies were facing on average 1,963 attacks each week, where roughly 25% were linked to espionage. According to the FBI, there have been 880,418 incidents of cyber crimes in the US with total losses standing at $12.5 billion – 21% more than the previous year. The figures clearly indicate that identity protection has moved beyond being an IT concern.

The combination of artificial intelligence and behavioral analysis in IDaaS solutions is ushering in a new wave of authentication technologies that evaluate the risk of a user throughout the entire duration of their session rather than just during authentication. The system will be able to monitor any kind of behavior deviation such as suspicious logins from unfamiliar locations or on different devices, and trigger a need for step-up authentication or even end the user session.

Market Size and Forecast:

-

Market Size in 2025: USD 11.22 Billion

-

Market Size by 2035: USD 93.4 Billion

-

CAGR: 24.69% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Identity as a Service (IDaaS) Market - Request Free Sample Report

Identity as a Service (IDaaS) Market Trends

-

Zero-trust security model adoption making IDaaS the foundational access control layer for enterprise cybersecurity architecture.

-

AI-powered behavioral analytics and continuous authentication replacing static password-based access for enhanced security.

-

Passwordless authentication with biometrics, hardware keys based on FIDO2 standard, and push notifications becoming more popular.

-

Identity platforms that combine customer identities (CIAM), workforce identities, and privileged access management in one solution.

-

Decentralized identity with blockchain technology providing verifiable credentials and user-controlled digital identities.

-

The BYOD approach and multi-device workforce requiring device trust to be built into IDaaS platforms.

-

Automation of regulatory compliance through IDaaS platforms creating audit trails, access certifications, and compliance reports automatically.

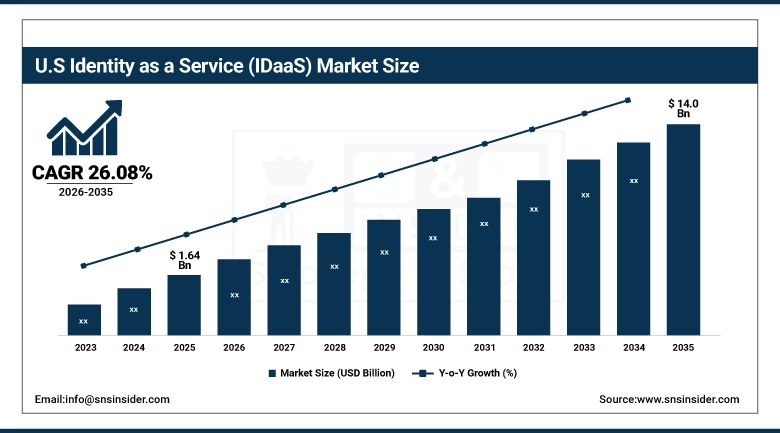

U.S. Identity as a Service (IDaaS) Market was valued at USD 1.64 billion in 2025 and is expected to reach USD 14.0 billion by 2035, at a CAGR of 26.08% from 2026 to 2035.

The United States of America is the topmost market for IDaaS owing to the existence of stringent data security guidelines both on the federal and state levels, including HIPAA, CCPA, SOX, and FedRAMP. The implementation of IDaaS in American businesses is a result of their zero-trust architecture model, driven by some highly publicized cases of data breaches, which include SolarWinds, Colonial Pipeline, and the case involving Okta, emphasizing the need for a well-designed system of identity management. Companies based in the United States, such as Okta, Microsoft, and Ping Identity, are top competitors in the worldwide IDaaS market, with their domestic clients comprising a significant portion of the American market.

There has been a huge push in the adoption of IDaaS solutions in the U.S. federal government since the issuance of the executive order on May 2021, which mandates all federal agencies to implement zero-trust architecture. Many federal agencies such as the Department of Defense (DOD), Homeland Security, and important federal departments are adopting IDaaS solutions across the enterprise level.

Identity as a Service (IDaaS) Market Segment Insights

-

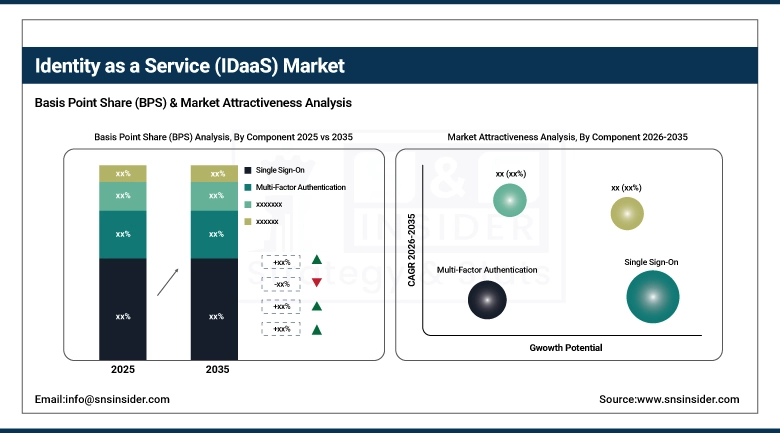

Based on Component, Single Sign-On (SSO) held 29% share in 2025; Multi-Factor Authentication (MFA) is growing fastest driven by regulatory mandates and zero-trust adoption.

-

Based on Deployment, Public Cloud led with 49% share for scalability; Hybrid Cloud is growing fastest for organizations requiring flexibility with on-premises control.

-

Based on Enterprise Size, Large Enterprises held 65% share; SMEs are growing fastest as affordable, scalable IDaaS becomes accessible to smaller organizations.

-

Based on End-Use, BFSI holds the largest share; Healthcare is growing fastest driven by telemedicine expansion and patient data protection requirements.

By Component: Single Sign-On (SSO) dominates, Multi-Factor Authentication (MFA) fastest growing CAGR

SSO allows users to log in only once and gain access to various applications/systems without having to enter their credentials again and again. SSO is the most commonly used module of IDaaS as it effectively solves the most common challenge that organizations face in terms of productivity — the issue of password fatigue because they have to manage many different sets of credentials to access their cloud applications. The enterprise-grade SSO offered by Okta, Microsoft Azure AD, and Ping Identity is integrated with thousands of SaaS applications.

Multi-factor authentication involves users proving their identities by validating themselves using two or more factors of identification. Factors include something they know (the password), something they have (a phone or a hardware token), and something they are (biometrics). Multi-factor authentication has become the fastest-growing IDaaS technology since regulatory demands such as PCI DSS, HIPAA, and now state cyber insurance mandates require organizations to use multi-factor authentication when accessing systems that contain sensitive data. Some examples of multi-factor authentication mechanisms include authenticator applications, push notification, SMS one-time passwords, hardware tokens, and biometric authentication.

By Deployment: Public Cloud (49% share) dominates, Hybrid Cloud fastest growing CAGR

Public cloud IDaaS is the dominant deployment model because it enables organizations to deploy enterprise-grade identity management without hardware investment, with near-instant scalability, automatic software updates, and access from any network location. SaaS-delivered IDaaS platforms from Okta, Microsoft Azure Active Directory, and Ping Identity serve thousands of enterprise customers from shared cloud infrastructure. Public cloud deployment is particularly well-suited to organizations that have largely completed their migration to cloud applications and no longer have significant on-premises identity infrastructure to maintain.

The use of hybrid cloud IDaaS solutions enables organizations to leverage cloud identity solutions together with directory services that operate internally within the organization, such as the Microsoft Active Directory, thereby enabling them to merge their processes of authentication on cloud applications and maintain control of their systems and data at the same time. This is very advantageous for financial institutions, healthcare organizations, and others that have to keep specific applications within the premises due to legal or operational reasons. Hybrid cloud IDaaS offers organizations a phased migration solution where the cloud identity services are incorporated into local systems gradually.

By End-Use: BFSI dominates; Healthcare is fastest growing CAGR

Banking, financial services, and insurance organizations are the largest IDaaS end-use segment because of the extreme sensitivity of financial data, heavy regulatory requirements from PCI DSS, SOX, FFIEC, and financial sector regulators, high fraud risk, and the complexity of managing access across legacy core banking systems, modern digital banking applications, and remote workforce environments. Financial institutions use IDaaS for customer-facing authentication in digital banking, employee access management, third-party vendor access control, and privileged access management for administrators who handle critical financial systems.

Healthcare is the fastest-growing IDaaS end-use segment driven by the rapid expansion of telemedicine requiring secure remote clinician access, the sensitivity of patient health information under HIPAA, integration of EHR systems with numerous point-of-care applications requiring SSO, and the critical need to prevent unauthorized access to life-critical systems. Healthcare organizations must balance security with clinical workflow efficiency—physicians cannot wait through complex authentication procedures during patient emergencies—making smart MFA solutions that assess context and risk level particularly important.

Identity as a Service (IDaaS) Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

77% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

China |

42% |

|

Middle East & Africa |

UAE |

38% |

|

Latin America |

Brazil |

49% |

North America Identity as a Service (IDaaS) Market Insights

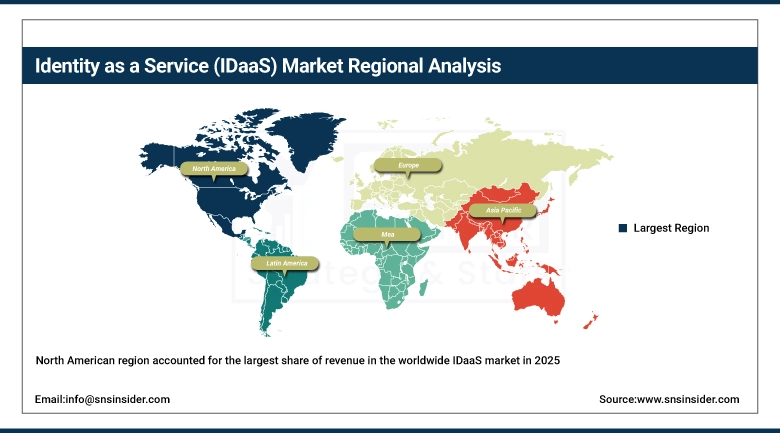

The North American region accounted for the largest share of revenue in the worldwide IDaaS market in 2025, owing to high enterprise cloud usage in the U.S., rigorous data security rules in place at both the federal and state levels, and presence of the greatest number of IDaaS technology vendors across the globe. The zero trust framework mandated by the U.S. government adds to this segment’s significance.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Identity as a Service (IDaaS) Market Insights

Europe represents a key IDaaS market where the implementation of GDPR has played a pivotal role as an enabler of identity management spending. The need for a legal basis for processing, consent management, and subject data rights under GDPR necessitates technical identity management considerations, which can be handled using IDaaS solutions. The main markets are Germany, the UK, and France. The upcoming NIS2 directive and the EU digital identity framework represent key drivers of investment going forward.

Asia Pacific Identity as a Service (IDaaS) Market Insights

APAC is the most rapidly growing region for IDaaS due to the accelerated pace of digital transformation in the banking sector, government offices, and enterprise IT in countries such as China, India, Singapore, and Australia. APAC enterprises have been targeted by almost 2,000 cyberattacks weekly in 2023 alone. The development of digital identity management systems in APAC governments, India's growth in its digital economy, and China's adoption of smart city initiatives are the main factors driving demand.

Middle East & Africa and Latin America Identity as a Service (IDaaS) Market Insights

There is extensive investment by the countries in the Middle East region to undergo digital transformation for various services such as banking and government services including smart cities. Digital initiatives in Saudi Arabia under Vision 2030 and advanced services provided by e-governments in the UAE need an effective identity management system. High use of smartphones among the people is favorable for IDaaS implementation.

The IDaaS industry in Latin America is rising with the development in digital banking, improvement in government services through IT, and increasing understanding of cybersecurity threats in the corporate world. There is increased investment in IDaaS due to the introduction of LGPD laws in Brazil, similar to the GDPR framework, making Brazil the biggest market in the region for IDaaS solutions.

Identity as a Service (IDaaS) Market Growth Drivers

Rising cyber threats and zero-trust architecture adoption are the primary growth drivers

Credential-based attacks—including phishing, credential stuffing, and social engineering—account for the majority of data breaches globally, making identity security the most critical cybersecurity investment priority. The zero-trust model's principle of 'never trust, always verify' makes IDaaS the foundational technology of modern enterprise security architecture. Organizations that previously relied on perimeter security (firewalls and VPNs) are discovering those controls are insufficient against modern attack techniques, driving urgency around IDaaS adoption.

Regulatory compliance is becoming a standalone factor driving the growth of IDaaS. The cyber-insurance guidelines, financial regulations, healthcare privacy laws, and government security standards now mandate certain identity security measures, especially multifactor authentication (MFA). Thus, regulatory pressure guarantees that organizations within a particular industry adopt IDaaS, irrespective of their cybersecurity readiness.

Identity as a Service (IDaaS) Market Restraints

Integration complexity with legacy systems and user resistance to new authentication create adoption barriers

Organizations with extensive on-premises legacy applications—particularly older ERP systems, mainframes, and custom-built applications that predate SAML and OAuth authentication standards—face significant technical challenges integrating these systems with cloud IDaaS platforms. Custom integration work can be expensive and time-consuming, delaying ROI realization. Additionally, some user populations, particularly older workers less comfortable with smartphones, resist new authentication methods like authenticator apps, creating change management challenges that slow adoption.

Identity as a Service (IDaaS) Market Opportunities

Decentralized identity and AI-powered identity verification represent transformative opportunities

The blockchain-enabled decentralized approach, in which the individuals manage the verifiable credentials on their personal devices without involving any central identity provider organizations, can be said to offer an entirely new concept of identity management. The W3C Decentralized Identifiers (DIDs) and Verifiable Credentials standards being used for portable digital identity applications are currently being pilot tested by Microsoft, IBM, and governments. The AI-driven solution for verifying the customer's identity in a matter of seconds for onboard purposes, in terms of authentication, is one of the growing niches of the IDaaS marketplace.

Recent Developments

-

2026: Okta expanded its identity security platform with AI agent identity management and resilience-focused capabilities. The company also partnered with Commvault to strengthen identity recovery and enterprise security for AI-driven workloads and cloud-native environments.

-

2026: SailPoint introduced AI-powered identity security enhancements including automated privilege discovery, non-human identity governance, and AI agent connectors. The company expanded integrations with Microsoft Copilot, Amazon Bedrock, Snowflake Cortex AI, and ServiceNow AI platforms.

-

2026: CyberArk strengthened its machine identity security strategy by expanding certificate lifecycle management, workload identity governance, and AI agent security capabilities. The company positioned machine identity protection as a core growth driver within zero-trust security architectures.

Key Players

Some companies in the Identity as a Service (IDaaS) Market:

-

Okta Inc.

-

Microsoft Corporation

-

Ping Identity Corporation

-

IBM Corporation

-

Oracle Corporation

-

SailPoint Technologies Inc.

-

CyberArk Software Ltd.

-

Saviynt Inc.

-

JumpCloud Inc.

-

OneLogin Inc.

-

Google LLC

-

Thales Group

-

RSA Security LLC

-

ForgeRock Inc.

-

Cisco Systems Inc.

-

VMware Inc.

-

HID Global Corporation

-

SecureAuth Corporation

-

Broadcom Inc.

-

Entrust Corporation

Identity as a Service (IDaaS) Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.22 Billion |

| Market Size by 2035 | USD 93.4 Billion |

| CAGR | CAGR of 24.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Single Sign-On, Multi-Factor Authentication, Provisioning, Privacy Management, Password Management, Others) • By Deployment (Public Cloud, Private Cloud, Hybrid Cloud) • By Enterprise Size (Large Enterprises, Small & Medium Enterprises) • By End-Use (BFSI, Healthcare, IT & Telecom, Government, Retail & E-Commerce, Education, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Okta Inc., Microsoft Corporation, Ping Identity Corporation, IBM Corporation, Oracle Corporation, SailPoint Technologies Inc., CyberArk Software Ltd., Saviynt Inc., JumpCloud Inc., OneLogin Inc., Google LLC, Thales Group, RSA Security LLC, ForgeRock Inc., Cisco Systems Inc., VMware Inc., HID Global Corporation, SecureAuth Corporation, Broadcom Inc., Entrust Corporation |

Get in Touch