Oncology Companion Diagnostic Market Report Scope & Overview:

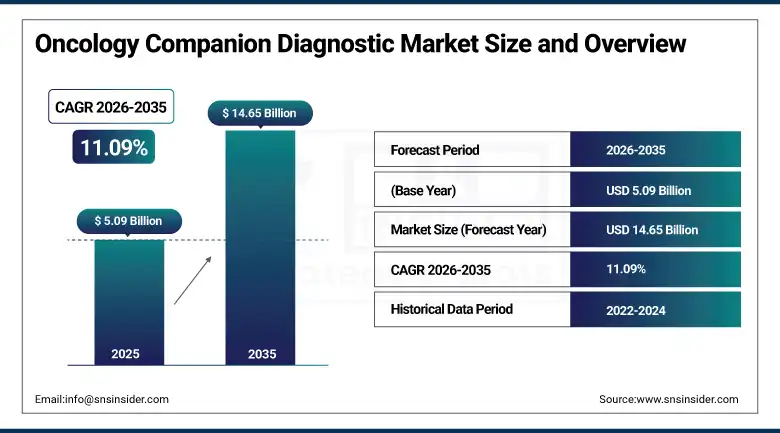

The Oncology Companion Diagnostic Market was valued at USD 5.09 Billion in 2025 and is expected to reach USD 14.65 Billion by 2035, growing at a CAGR of 11.09% from 2026–2035.

Oncology companion diagnostics are in vitro diagnostic tests specifically developed, validated, and FDA or equivalent regulatory authority co-approved for use alongside a specific therapeutic drug to identify patients most likely to benefit from the treatment, confirm potentially serious side-effect risks, or monitor therapeutic response in ways that optimize clinical outcome for the patient and commercial success for the therapy. The paradigm shift from empirical cancer treatment, where all patients with a given tumor type receive identical systemic therapy, toward molecularly stratified precision oncology, where biomarker testing identifies the specific genetic alteration, protein overexpression, or pathway activation that makes an individual tumor responsive to a specific targeted agent. This has made oncology companion diagnostics the fastest-growing segment within the clinical diagnostics industry.

In February 2025, Roche introduced an advanced companion diagnostic assay designed to identify novel biomarker signatures for improving patient stratification and enabling more accurate therapy selection across multiple oncology indications. The assay's capability to assess multiple biomarker parameters simultaneously from a single tissue sample addressed the growing clinical demand for comprehensive tumor molecular profiling that informs not only initial targeted therapy selection but also the sequential treatment decisions that arise as tumor molecular evolution creates resistance to first-line targeted agents, positioning Roche's companion diagnostic platform as a continuous clinical decision support tool throughout the patient's treatment journey.

Key Market Size and Forecast

-

Market Size in 2026E: USD 5.65 Billion

-

Market Size by 2035: USD 14.65 Billion

-

CAGR: 11.09% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Oncology Companion Diagnostic Market - Request Free Sample Report

Key Market Trends

-

Next-generation sequencing (NGS)-based comprehensive genomic profiling is increasingly replacing single-gene testing for precision oncology applications.

-

Liquid biopsy companion diagnostics are gaining adoption as minimally invasive tools for cancer detection, monitoring, and treatment selection.

-

Expanding use of tumor mutational burden (TMB) and microsatellite instability (MSI) biomarkers is supporting broader immunotherapy eligibility.

-

AI-powered image analysis is improving the accuracy, consistency, and efficiency of companion diagnostic testing.

-

Pharmaceutical companies are integrating companion diagnostics earlier in oncology drug development to improve clinical trial success and targeted therapy outcomes.

The U.S. Oncology Companion Diagnostic Market Outlook

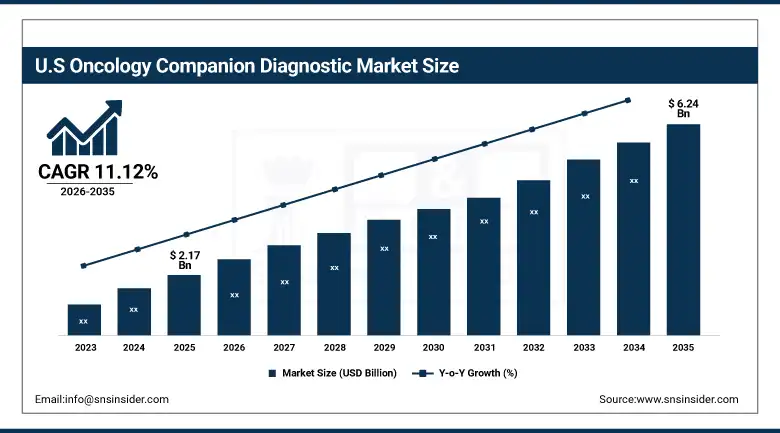

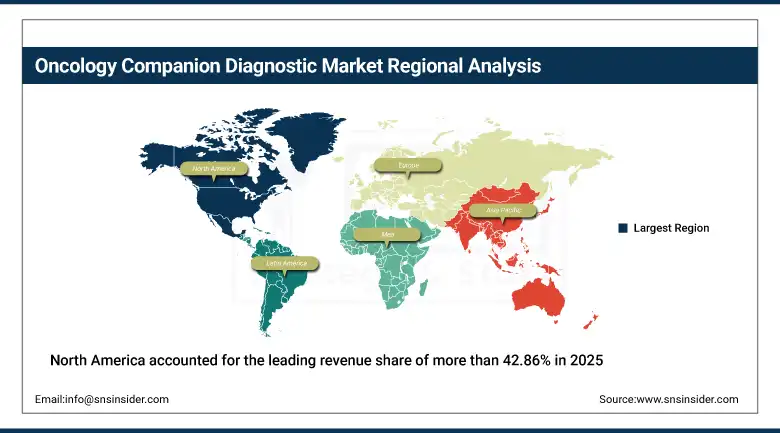

The U.S. Oncology Companion Diagnostic Market was valued at approximately USD 2.17 Billion in 2025 and is expected to reach approximately USD 6.24 Billion by 2035, growing at a CAGR of approximately 11.12%. North America accounted for the leading revenue share of more than 42.86% in 2025, underpinned by a highly developed healthcare ecosystem, stringent regulatory oversight for precision medicine, and consistent investments in biomarker-driven diagnostic technologies.

The United States oncology companion diagnostic market is driven by the FDA's precision oncology regulatory leadership whose companion diagnostic approval pathway, established through seminal co-approvals including the HER2 FISH test with trastuzumab and EGFR mutation testing with erlotinib, has created the most extensive and commercially mature companion diagnostic regulatory framework globally. The FDA's requirement for companion diagnostic co-approval with targeted therapies as a condition of drug approval for biomarker-defined patient populations creates non-discretionary clinical adoption whose implementation across hospital pathology departments and reference laboratories generates sustained test volume growth with each new targeted therapy approval. The National Comprehensive Cancer Network's treatment guidelines, which specify companion diagnostic testing as a prerequisite for targeted therapy prescription in their oncology treatment algorithms.

In 2023, Guardant Health received FDA approval for the Guardant360 CDx as a companion diagnostic for Lumakras (soterasib) in KRAS G12C-mutated non-small cell lung cancer, marking the first FDA approval of a liquid biopsy companion diagnostic using circulating tumour DNA from a blood sample to identify patients eligible for a targeted therapy. The approval demonstrated the regulatory acceptance of liquid biopsy companion diagnostics for treatment selection and validated the commercial pathway for blood-based molecular profiling as an equivalent alternative to tissue biopsy for companion diagnostic purposes in advanced NSCLC.

Oncology Companion Diagnostic Market Segmentation Analysis

-

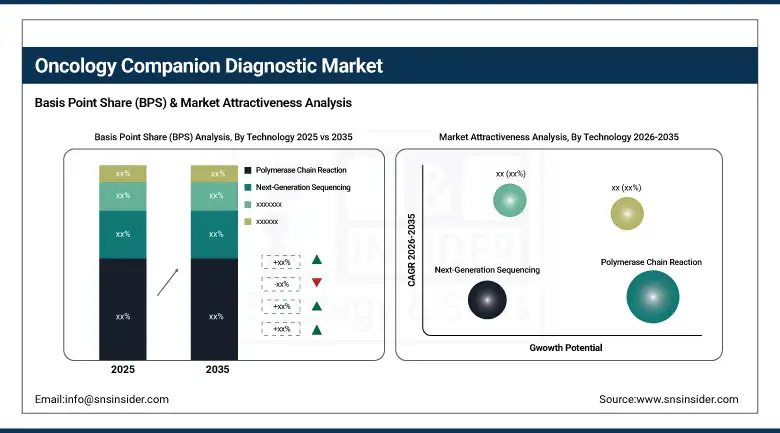

By Technology, polymerase chain reaction segment dominated the oncology companion diagnostic market in 2025, while the next-generation sequencing segment is the fastest growing technology with a CAGR of approximately 12.64%, driven by demand for comprehensive genomic profiling.

-

By Product, assay kits & reagents segment dominated the oncology companion diagnostic market with the largest share in 2025, while the others segment is the fastest growing product type driven by growing demand for specialty diagnostic testing outsourcing to reference laboratories.

-

By Cancer Type, non-small cell lung cancer segment dominated the oncology companion diagnostic market with approximately 31% share in 2025, while the breast cancer segment is the fastest growing cancer type during the forecast period.

-

By End User, pharmaceutical & biopharmaceutical companies segment dominated the oncology companion diagnostic market with approximately 46.27% share in 2025, while the contract research organizations segment is growing as outsourced companion diagnostic development and clinical trial biomarker testing expand.

By Technology, polymerase chain reaction (PCR) dominates, next-generation sequencing (NGS) grows fastest

Polymerase chain reaction retained the dominant technology position in 2025, reflecting its established clinical validation, regulatory approval track record, and operational familiarity in hospital pathology and reference laboratory settings across the foundational companion diagnostic applications including EGFR mutation detection in NSCLC, KRAS mutation testing in colorectal cancer, and BRAF V600E mutation assessment in melanoma whose high-volume clinical testing requirements sustain PCR-based companion diagnostic procurement at scale. PCR's technical attributes, including its high analytical sensitivity, excellent specificity for targeted mutation detection, rapid turnaround time compatible with clinical decision urgency, and cost-effective operation within established laboratory infrastructure, create a performance profile that sustains its clinical utility for defined single-gene and small panel companion diagnostic applications despite the broader analytical capability of next-generation sequencing.

Next-generation sequencing is the fastest-growing technology as comprehensive genomic profiling's clinical adoption expands from specialist academic cancer centres into community oncology and general hospital pathology settings whose growing awareness of actionable genomic alterations is creating demand for broad-panel analysis beyond the single-gene and small-panel PCR tests that traditional companion diagnostic testing has relied upon. Each new targeted therapy approval whose companion diagnostic specifies an actionable genomic alteration adds to the clinical argument for comprehensive NGS testing that assesses the full spectrum of potentially actionable biomarkers simultaneously rather than sequential single-gene testing whose per-result cost compounds with each additional test ordered.

By Cancer Type, non-small cell lung cancer (NSCLC) dominates, breast cancer grows fastest

Non-small cell lung cancer retained the dominant cancer type position with approximately 31% of the oncology companion diagnostic market in 2025, reflecting the extraordinary breadth and depth of companion diagnostic-guided therapy development in NSCLC whose actionable molecular subtypes, including EGFR mutations, ALK rearrangements, ROS1 fusions, BRAF V600E, MET exon 14 skipping, RET fusions, NTRK fusions, and KRAS G12C, collectively account for over 50% of advanced NSCLC patients and whose companion diagnostic testing requirements create the highest per-tumor-type molecular profiling test volume in oncology. The clinical standard of comprehensive molecular profiling at advanced NSCLC diagnosis, mandated by NCCN, ESMO, and IASLC guidelines, creates systematic companion diagnostic ordering across every new advanced NSCLC diagnosis that sustains NSCLC's commercial leadership in companion diagnostic utilization.

Breast cancer is the fastest-growing cancer type as the expansion of HER2-low companion diagnostic testing for novel antibody-drug conjugate therapy eligibility, the clinical adoption of PIK3CA mutation testing for alpelisib eligibility in HR-positive HER2-negative advanced breast cancer, and the growing breast cancer homologous recombination deficiency testing for PARP inhibitor eligibility collectively create a rapidly expanding breast cancer companion diagnostic test portfolio that adds new clinical indications above the foundational HER2 FISH and IHC testing that has sustained breast cancer companion diagnostic volume for over two decades.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

28.5% |

|

Asia Pacific |

China |

38.5% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Oncology Companion Diagnostic Market Insights

North America accounted for the leading revenue share of more than 42.86% in 2025 within the global oncology companion diagnostic market. The United States accounts for approximately 82.5% of North American revenues through its leadership in targeted oncology drug approvals generating companion diagnostic co-approval requirements, the highest commercial cancer diagnostic laboratory infrastructure density globally, and the most extensive pharmaceutical and biotechnology industry investment in precision oncology companion diagnostic development. Canada contributes supplementary demand through its provincial cancer care network's progressive adoption of molecular profiling standards aligned with U.S. NCCN guidelines.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Oncology Companion Diagnostic Market Insights

Europe held a significant share of the global oncology companion diagnostic market in 2025. Germany, France, the United Kingdom, Italy, and Spain are the leading national markets whose universal healthcare cancer care programmes, academic oncology centres, and progressive European Medicines Agency regulatory framework for companion diagnostic co-approval create consistent molecular diagnostic demand. Germany accounts for approximately 28.5% of European revenues through the commercial presence of Roche Diagnostics and its cobas EGFR and HER2 companion diagnostic platforms, the large oncology care infrastructure at university medical centres, and the comprehensive cancer genetics service whose testing volumes sustain reagent procurement.

The EMA's companion diagnostic regulatory framework, which requires companion diagnostic development in parallel with EU oncology drug regulatory submissions, is creating growing European investment in companion diagnostic co-development by both European and U.S. pharmaceutical companies whose European drug approval strategies require European-validated companion diagnostic solutions addressing the distinct regulatory requirements from U.S. FDA submissions.

Asia Pacific Oncology Companion Diagnostic Market Insights

Asia Pacific is the fastest-growing regional oncology companion diagnostic market with a CAGR of 12.34%, driven by expanding healthcare infrastructure investment, growing precision oncology adoption, and changing regulatory frameworks across China, India, Japan, and South Korea. China accounts for approximately 38.5% of Asia Pacific revenues through its rapidly growing comprehensive cancer centre network, the NMPA's progressive companion diagnostic co-approval framework development, and the expanding domestic molecular diagnostic industry whose NGS-based comprehensive genomic profiling adoption is creating large companion diagnostic test volumes.

Japan and South Korea contribute premium regional demand through their advanced oncology infrastructure, high cancer genomic testing penetration, and the local pharmaceutical industries' growing investment in companion diagnostic-accompanied targeted therapy development for both domestic and global markets. India and Southeast Asian markets are growing rapidly as cancer diagnosis infrastructure investment and health insurance expansion create new molecular oncology testing demand.

MEA & Latin America Oncology Companion Diagnostic Market Insights

The UAE leads MEA revenues of the regional total through its world-class oncology infrastructure at Cleveland Clinic Abu Dhabi and other international-standard cancer centres whose molecular testing programmes approach Western practice standards. Saudi Arabia's expanding cancer care network and growing precision oncology investment create growing companion diagnostic demand from an increasingly sophisticated oncology clinical community.

Brazil leads Latin American revenues at approximately 43.8% of the regional total through its growing oncology infrastructure at leading public and private cancer centres, the progressive adoption of molecular profiling standards in the INCA national cancer programme, and the expanding private health insurance sector's coverage of molecular diagnostic testing for oncology treatment selection.

Growth Drivers: Rapid expansion of targeted oncology therapies requiring companion diagnostic co-approval and precision medicine adoption creating mandatory molecular profiling at cancer diagnosis

The oncology companion diagnostic market's growth is structurally driven by the pharmaceutical industry's productive targeted therapy pipeline whose each new FDA approval requiring a companion diagnostic co-approval adds a new permanent clinical testing volume to the oncology diagnostic landscape. The oncology drug pipeline is at its historically most productive stage, with over 1,000 oncology drugs in clinical development, a growing proportion of which target biomarker-defined patient populations whose precision medicine approach requires companion diagnostic development as an integral component of regulatory strategy. Each new targeted therapy approval that mandates companion diagnostic testing before prescription creates a non-discretionary test volume that grows with each new patient diagnosed with the relevant cancer type and scales with the commercial success of the therapy whose companion diagnostic is the gateway to prescription.

Restraints: Tissue biopsy accessibility challenges and companion diagnostic development complexity creating barriers to timely molecular profiling in resource-limited clinical settings

Tissue biopsy acquisition for companion diagnostic testing creates a procedural barrier for patients with inaccessible tumor locations, poor performance status precluding biopsy, or insufficient archival tissue from prior surgical procedures whose companion diagnostic testing requirements cannot be met without new invasive tissue acquisition. The companion diagnostic development process, which requires analytical validation, clinical validation, regulatory submission, and manufacturing process qualification whose combined timeline of three to seven years from assay development to regulatory approval creates a development investment whose commercial risk must be managed through co-development partnerships between diagnostic and pharmaceutical companies whose aligned interests sustain long-term contractual commitment.

Opportunities: Liquid biopsy companion diagnostic approval expansion and AI-powered pathology image analysis improving companion diagnostic accuracy and throughput

Liquid biopsy companion diagnostics using circulating tumor DNA from blood samples represent the most transformative companion diagnostic technology advance since the introduction of FISH, enabling companion diagnostic testing without tissue biopsy whose procedural barrier, tissue adequacy uncertainty, and tumor heterogeneity sampling limitation each constrain the accessibility and comprehensiveness of tissue-based molecular profiling. The Guardant360 CDx's FDA approval for KRAS G12C-mutated NSCLC demonstrated the regulatory pathway for blood-based companion diagnostics whose approval expansion across additional tumor types and targeted therapy indications creates the largest near-term companion diagnostic market expansion opportunity. AI-powered pathology image analysis systems that improve the standardization, throughput, and accuracy of IHC-based companion diagnostic assessment for PD-L1, HER2, and mismatch repair protein expression create a technology upgrade market across hospital pathology departments whose manual scoring reproducibility limitations have created diagnostic consistency challenges.

Recent Developments:

-

2025: Roche introduced an advanced companion diagnostic assay for identifying novel biomarker signatures across multiple oncology indications, enabling comprehensive tumor molecular profiling from a single tissue sample to inform both initial targeted therapy selection and sequential treatment decisions.

-

2024: Thermo Fisher Scientific expanded its Oncomine Dx Target Test NGS-based companion diagnostic coverage to include additional actionable genomic alterations across NSCLC and other solid tumor types, advancing the clinical utility of comprehensive NGS companion diagnostic testing beyond single-gene PCR alternatives.

-

2023: Guardant Health received FDA approval for the Guardant360 CDx as the first liquid biopsy companion diagnostic for KRAS G12C-mutated NSCLC, marking a regulatory milestone for circulating tumour DNA-based treatment selection testing as a minimally invasive alternative to tissue biopsy.

Key Market Players

-

QIAGEN N.V.

-

Illumina, Inc.

-

Abbott Laboratories

-

Bio-Rad Laboratories, Inc.

-

Guardant Health, Inc.

-

Exact Sciences Corporation

-

Myriad Genetics, Inc.

-

NeoGenomics, Inc.

-

Foundation Medicine, Inc.

-

Sysmex Corporation

-

Natera, Inc.

-

Invivoscribe, Inc.

-

Danaher Corporation (Cepheid)

-

PERSONALIS, Inc.

-

Adaptive Biotechnologies Corporation

-

Biocartis Group NV

-

Genomic Health, Inc. (Exact Sciences)

Oncology Companion Diagnostic Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 5.09 Billion |

| Market Size by 2035 | USD 14.65 Billion |

| CAGR | CAGR of 11.09% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Polymerase Chain Reaction, Next-Generation Sequencing, In Situ Hybridization, Immunohistochemistry, Others) • By Product (Assay Kits & Reagents, Instruments, Others) • By Cancer Type (Non-Small Cell Lung Cancer, Breast Cancer, Colorectal Cancer, Melanoma, Leukaemia, Others) • By End User (Pharmaceutical & Biopharmaceutical Companies, Contract Research Organizations, Hospitals & Diagnostic Laboratories) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | F. Hoffmann-La Roche Ltd., QIAGEN N.V., Thermo Fisher Scientific Inc., Illumina, Inc., Agilent Technologies, Inc., Abbott Laboratories, Bio-Rad Laboratories, Inc., Guardant Health, Inc., Exact Sciences Corporation, Myriad Genetics, Inc., NeoGenomics, Inc., Foundation Medicine, Inc., Sysmex Corporation, Natera, Inc., Invivoscribe, Inc., Danaher Corporation (Cepheid), PERSONALIS, Inc., Adaptive Biotechnologies Corporation, Biocartis Group NV, and Genomic Health, Inc. (Exact Sciences) |

Frequently Asked Questions

The Oncology Companion Diagnostic Market is expected to grow at a CAGR of 11.09% from 2026 to 2035.

The Oncology Companion Diagnostic Market was valued at USD 5.09 Billion in 2025.

The Oncology Companion Diagnostic Market is driven by the rapid growth of targeted cancer therapies, increasing adoption of precision medicine, expanding use of NGS-based genomic profiling, and rising approval of liquid biopsy diagnostics for treatment selection.

The Non-Small Cell Lung Cancer segment dominated the Oncology Companion Diagnostic Market with approximately 31% share in 2025 through the broadest companion diagnostic-guided targeted therapy portfolio of any solid tumor type.

North America accounted for the leading revenue share of more than 42.86% in 2025.

Get in Touch