Companion Diagnostics Market Report Scope & Overview:

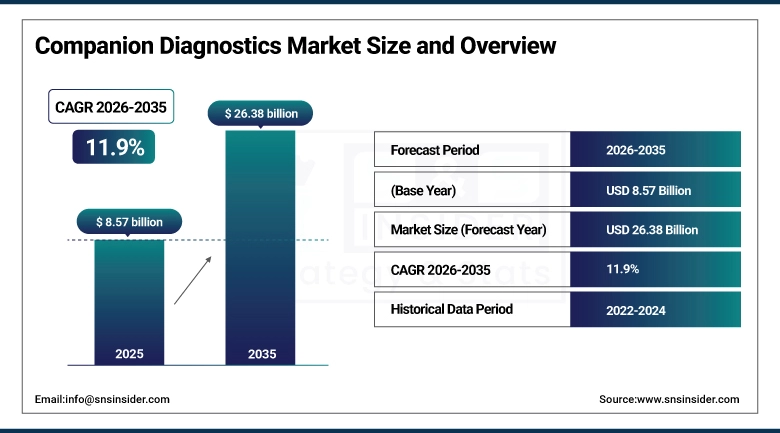

The Companion Diagnostics Market size was valued at USD 8.57 billion in 2025 and is projected to reach USD 26.38 billion by 2035, expanding at a CAGR of 11.9% throughout the forecast period of 2026–2035.

The market for Companion Diagnostics is growing rapidly due to the rise in precision medicine, the increased occurrence of cancer and genetic diseases, and the rising need for treatment options that target specific conditions.

Further advancements in biomarker discoveries, next generation sequencing, and molecular diagnostics have made significant contributions toward its growth. The regulatory support provided for the development of drugs along with diagnostic tests, coupled with more funding from pharmaceuticals and biotechnology companies, have contributed immensely to its adoption in hospitals and laboratories.

For instance, in March 2024, a report published in a leading oncology journal highlighted that the use of companion diagnostics in targeted cancer therapies improved treatment response rates by over 80%, significantly influencing clinical adoption across oncology care settings.

Companion Diagnostics Market Size and Forecast:

-

Market Size in 2025: USD 8.57 billion

-

Market Size by 2035: USD 26.38 billion

-

CAGR: 11.9% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Companion Diagnostics Market - Request Free Sample Report

Companion Diagnostics Market Trends:

-

Growing utilization of biomarker-based testing to guide targeted therapies, particularly in oncology, is driving widespread adoption across clinical settings.

-

Increased collaboration between pharmaceutical and diagnostic companies to co-develop drug-diagnostic combinations aimed at improving therapeutic precision.

-

Rising integration of next-generation sequencing and multiplex assays into companion diagnostics platforms to enable comprehensive genomic profiling.

-

Expansion of companion diagnostics applications beyond oncology into areas such as neurology, infectious diseases, and cardiovascular disorders.

-

Advancements in liquid biopsy technologies allowing non-invasive detection and monitoring of disease progression, enhancing patient compliance and clinical outcomes.

-

Growing emphasis on regulatory approvals and standardized validation processes to ensure accuracy, reliability, and market acceptance of diagnostic tests.

-

Increasing deployment of digital health tools and data analytics platforms to support real-time interpretation of diagnostic results and clinical decision-making.

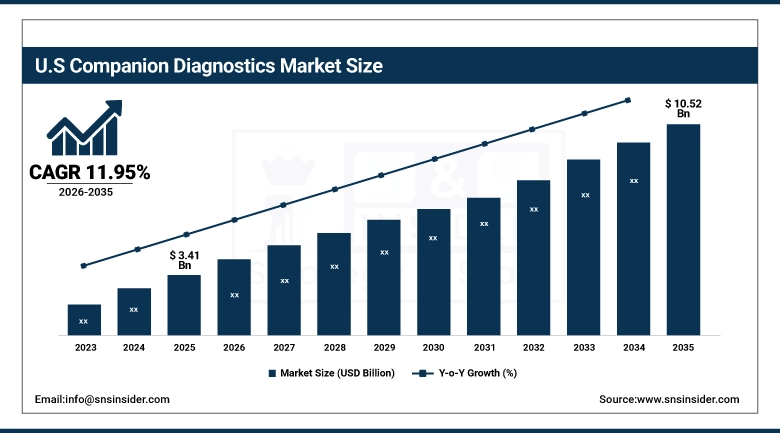

The U.S. Companion Diagnostics Market was valued at USD 3.41 billion in 2025 and is expected to reach USD 10.52 billion by 2035, growing at a CAGR of 11.95% from 2026–2035. The U.S. still retains its leadership position in the companion diagnostics industry across the globe owing to its solid healthcare system, leading players in the pharmaceuticals and biotechnology sectors, and use of advanced diagnostics technology.

Positive regulatory environments that promote the concurrent development of diagnostics and drugs, along with high health care expenditure, are contributing to continued market growth. On the other hand, increasing knowledge about the benefits of personalized medicine and the rise in cases of diseases such as cancers are increasing the need for companion diagnostics. The nation also has an innovative environment for molecular diagnostics and healthy competition, which helps in quick adoption of diagnostic systems.

Companion Diagnostics Market Growth Drivers:

-

Growing Demand for Precision Medicine and Targeted Therapies is Accelerating the Companion Diagnostics Market Growth

As medicines are becoming more and more tailored to individual genetic features, it has led to the rise of precision medicines needing even greater numbers of companion diagnostics. To help increase the effectiveness of therapies while reducing side effects, drug manufacturers and biotech firms are developing companion diagnostics. This combination has clinical significance and is increasingly being encouraged by regulatory bodies such as the FDA in the drug development process. This combination between the two expands application beyond cancer into infectious diseases, among others, propelling market growth across the globe.

For instance, in July 2024, the FDA approved multiple targeted oncology therapies alongside companion diagnostic tests, further strengthening the co-development model and accelerating adoption across clinical settings.

Companion Diagnostics Market Restraints:

-

High Development Costs and Complex Regulatory Pathways are Limiting the Companion Diagnostics Market Growth

However, the path involved in developing and launching the companion diagnostics is not only expensive but also time-taking due to significant costs being incurred at different stages such as biomarker discovery, validation, and approvals process. The coordination of the timelines involved in the drug therapy and its associated diagnostic test complicates the situation. Also, regional disparities in regulations and requirement for clinical data serve as entry barriers to smaller diagnostic companies. On top of that, the uncertainty of payment schemes in some countries also hampers the growth potential.

Companion Diagnostics Market Opportunities:

-

Advancements in Genomic Technologies and Expanding Oncology Applications are Creating Significant Opportunities for the Companion Diagnostics Market

Technological advancements, such as those witnessed in next generation sequencing and multiplexed biomarker tests, among other forms of genomic sequencing technology, are creating new avenues for growth in the companion diagnostics market. This is due to technological advancements in sequencing are making possible more efficient detection of genetic mutations, and thus the development of more effective drug treatments. Companion diagnostics is no longer only used in cancer but also in neurology and orphan diseases, widening the market even more. Furthermore, the increasing partnerships between diagnostic firms and the pharmaceutical industry will boost innovation and growth potential in this industry.

For instance, in May 2024, several leading diagnostics firms announced strategic collaborations with biopharmaceutical companies to develop next-generation sequencing based companion diagnostic panels, enhancing personalized treatment capabilities and expanding clinical utility.

Companion Diagnostics Market Segment Analysis

-

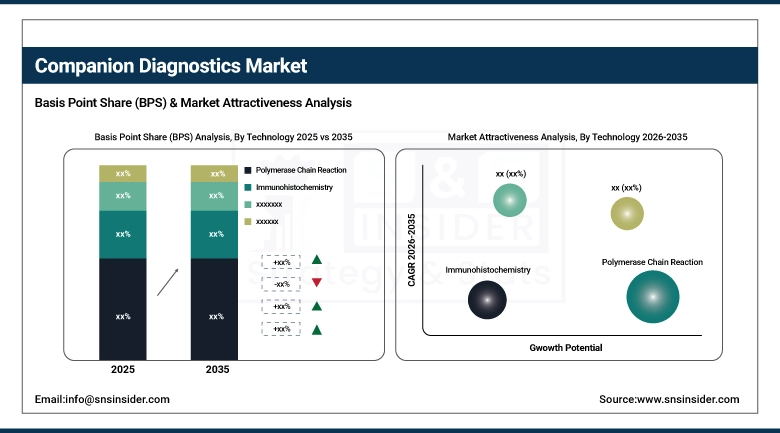

By technology, polymerase chain reaction accounted for the largest share of approximately 41.82% in 2025, while next generation gene sequencing is projected to witness the fastest growth with a CAGR of 12.64%.

-

By indication, cancer dominated the market with a share of nearly 67.35% in 2025, whereas infectious diseases are expected to register the highest growth at a CAGR of 12.18%.

-

By end-user, pharmaceutical and biopharmaceutical companies held the leading share of around 46.27% in 2025, while contract research organizations are anticipated to grow at the fastest CAGR of 12.52%.

By Technology, Polymerase Chain Reaction Leads the Market, While Next Generation Gene Sequencing Exhibits Strongest Growth

The Polymerase Chain Reaction (PCR) section was the biggest revenue contributor in 2025 with a market share of around 41.82%. Its feature of high sensitivity, rapid detection time, and reliability in detecting genetic mutations involved with targeted drug therapies are some factors contributing to its wide acceptance across clinical diagnostic applications.

On the other hand, the next generation sequencing market is expected to experience the fastest CAGR of 12.64% during the forecast period between 2026 and 2035, driven by increased demands for advanced genomic analysis, advancements in sequencing platforms, and increasing use of personalized treatments. The growth is being fuelled by increased investments in biomarker identification and clinical applications.

By Indication, Cancer Holds the Largest Share, While Infectious Diseases Show Accelerated Growth

Cancer accounted for the majority of the market, estimated at around 67.35% in 2025, due to their wide use in cancer care for patient stratification, therapeutic selection and response monitoring. Given the rapid rise of cancer and an expanding pipeline of targeted therapies, the need for diagnostic co-development has never been higher.

Conversely, the infectious diseases category is projected to record the highest compound annual growth rate of 12.18%. The factors driving growth include the increasing need for quick and precise diagnosis tools for infections and re-emerging infections. Moreover, the trend toward personalized treatment of infectious diseases has also played a significant role in boosting the growth of this market segment.

By End-user, Pharmaceutical and Biopharmaceutical Companies Dominate, While Contract Research Organizations Register Fastest Growth

Pharmaceutical and biopharmaceutical companies accounted for the largest market share of 46.27% in 2025, due to their growing involvement in the adoption of companion diagnostics during clinical trials and regulation for specific treatments. This sector will keep investing heavily in co-development initiatives for optimizing drug efficiency and securing successful approvals.

It is expected that contract research organizations will record the highest CAGR of 12.52% from 2026 to 2035, owing to increasing outsourcing in the clinical trial industry, biomarker testing, and diagnostic research. With clinical research becoming more complicated, there is a higher need for specialized skills, hence making CROs increasingly important.

Companion Diagnostics Market Regional Highlights:

North America Companion Diagnostics Market Insights:

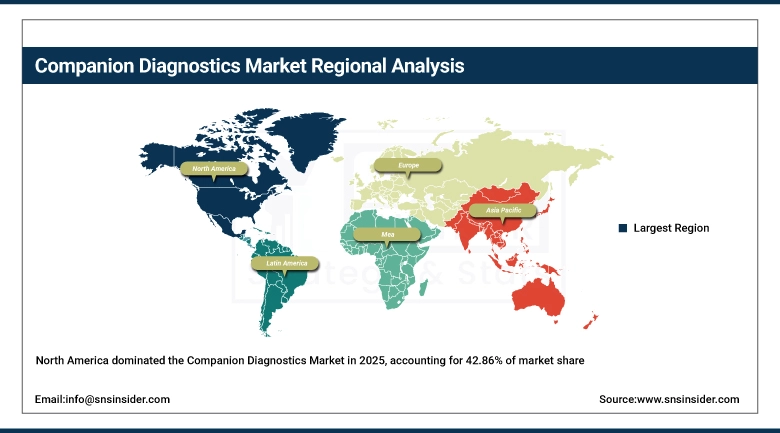

North America dominated the Companion Diagnostics market, with a revenue market share more than 42.86% in 2025E. The region's dominance is driven by its well-developed healthcare system, stringent regulatory policies on precision medicines, and investment in biomarker diagnostics technology.

The United States continues to act as the central stage of growth, as pharmaceutical companies, clinical labs, and oncology facilities integrate companion diagnostics with targeted drugs in an attempt to achieve better outcomes in terms of efficacy and regulatory compliance. Positive payment policies, active clinical trials, and greater adoption of personalized medicine contribute to the dominance of the region and its high revenues in the market from 2026 to 2035.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Companion Diagnostics Market Insights:

Asia Pacific region is the fastest growing in the Companion Diagnostics market, projected to grow with a CAGR of 12.34%. These dynamics will be driven by continuous developments in the healthcare infrastructure and increased focus on precision oncology in countries such as China, India, Japan, and South Korea. An increasing incidence of cancer, increasing awareness about targeted therapy, and advancements in diagnostic technology continue to boost the market in this region.

Sustained support by the government in the areas of genomics development, clinical trial expansion, and enhancing biotechnology capacities continues to drive its implementation. The rising number of patients along with an inclination toward customized therapy methods makes the area ideal for the development of companion diagnostics.

Europe Companion Diagnostics Market Insights:

Europe is the second largest regional market for Companion Diagnostics due to the presence of established healthcare systems, high standards of regulation for in vitro diagnostics and an increased focus on personalized medicine in Germany, the UK, France, and Italy. The presence of a defined reimbursement process, use of biomarker tests in clinical practice guidelines, and collaborative efforts between pharmaceutical companies and diagnostic firms contribute to its growth.

Conformity with the In-Vitro Diagnostic Regulation framework in addition to continuous investments made toward developing the molecular diagnostics infrastructure also drives market growth. In addition, increased emphasis on achieving success in improving the outcome of cancer care and selection of therapy options further strengthens the use of companion diagnostics in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Companion Diagnostics Market Insights:

Latin America and the Middle East & Africa regions are witnessing an increasing uptake of Companion Diagnostics, driven by increased accessibility to healthcare services, growing incidence rates of cancer, and rising spending on diagnostics facilities. Brazil, Mexico, the United Arab Emirates (UAE), and Saudi Arabia have become prominent regions for growth, with both private and government health sector players investing in advanced molecular diagnostics and targeted treatments.

Better lab facilities, increased collaboration between labs and diagnostics companies, and as favourable policy developments are facilitating capture of market entry. The increasing awareness of the benefits offered by personalized medicine along with increasing healthcare expenditure will also help to maintain market growth and overall acceptance in the region through 2035.

Companion Diagnostics Market Competitive Landscape:

Hoffmann-La Roche Ltd. (est. 1869) is a long-established pioneer in in vitro diagnostics and personalized healthcare solutions. Release, it provides a full portfolio of high-quality companion diagnostic tests, itsNHL molecular test platform and therapy alignment solutions for the specific therapy. Leveraging its cobas test platforms and biomarker analysis expertise, the company enables accurate treatment decisions in oncology, immunology, and infectious diseases.

-

In February 2025, Roche introduced an advanced companion diagnostic assay designed to identify novel biomarker signatures, improving patient stratification and enabling more accurate therapy selection across oncology treatment centers.

QIAGEN N.V. (est. 1984) is one of the major players in providing technologies for sample preparation and assays with particular emphasis on companion diagnostics. It provides products including molecular test kits, next generation sequencing panels, and bioinformatics. QIAGEN integrates its diagnostic platforms with advanced data analytics to facilitate biomarker discovery and targeted therapies.

-

In June 2025, QIAGEN N.V. partnered with Incyte to develop a next-generation NGS-based companion diagnostic panel targeting mutant CALR and other clinically relevant gene alterations in myeloproliferative neoplasms (MPNs), enhancing precision testing in hematological oncology.

Agilent Technologies, Inc. (est. 1999) is an international corporation that develops solutions for the analysis and diagnostics market, focusing on the field of genomics, pathology, and biomarkers. Agilent’s line of companion diagnostics encompasses tests based on tissues, genomic profile analyses, and automatic staining devices for use by pharmaceutical companies and laboratories.

-

In March 2026, Agilent Technologies, Inc. received U.S. FDA approval for its PD-L1 IHC 22C3 pharmDx companion diagnostic for esophageal and gastroesophageal junction carcinoma, enabling clinicians to identify patients likely to benefit from anti-PD-1 therapy with KEYTRUDA.

Companion Diagnostics Market Key Players:

-

F. Hoffmann-La Roche Ltd.

-

QIAGEN N.V.

-

Agilent Technologies, Inc.

-

Thermo Fisher Scientific Inc.

-

Abbott Laboratories

-

Illumina, Inc.

-

bioMérieux SA

-

Danaher Corporation

-

Myriad Genetics, Inc.

-

Guardant Health, Inc.

-

Foundation Medicine, Inc.

-

Sysmex Corporation

-

Bio-Rad Laboratories, Inc.

-

Hologic, Inc.

-

Invitae Corporation

-

NeoGenomics Laboratories, Inc.

-

Exact Sciences Corporation

-

Fujirebio Diagnostics, Inc.

-

ArcherDX, Inc.

-

Genomic Health, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.57 Billion |

| Market Size by 2035 | USD 26.38 Billion |

| CAGR | CAGR of 11.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technology (Polymerase Chain Reaction, Immunohistochemistry, In-situ Hybridization, Next Generation Gene Sequencing, Others) • By Indication (Cancer, Neurological Diseases, Infectious Diseases, Others) • By End-user (Pharmaceutical & Biopharmaceutical Companies, Reference Laboratories, Contract Research Organizations (CROs)) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | F. Hoffmann-La Roche Ltd., QIAGEN N.V., Agilent Technologies Inc., Thermo Fisher Scientific Inc., Abbott Laboratories, Illumina Inc., bioMérieux SA, Danaher Corporation, Myriad Genetics Inc., Guardant Health Inc., Foundation Medicine Inc., Sysmex Corporation, Bio-Rad Laboratories Inc., Hologic Inc., Invitae Corporation, NeoGenomics Laboratories Inc., Exact Sciences Corporation, Fujirebio Diagnostics Inc., ArcherDX Inc., Genomic Health Inc. |

Frequently Asked Questions

The Companion Diagnostics Market size was valued at USD 8.57 billion in 2025 and is expected to witness strong growth over the forecast period.

The market is projected to reach USD 26.38 billion by 2035, reflecting substantial expansion driven by precision medicine and targeted therapies.

The market is anticipated to grow at a compound annual growth rate (CAGR) of 11.9% during the forecast period of 2026–2035.

Key growth drivers include the rising adoption of personalized medicine, increasing prevalence of cancer, growing demand for targeted therapies, and advancements in biomarker-based diagnostics.

Companion diagnostics are widely used in oncology, cardiology, neurology, and infectious diseases, with oncology being the dominant segment.

Get in Touch